Eurobonds And The Internationalization Of The Euro

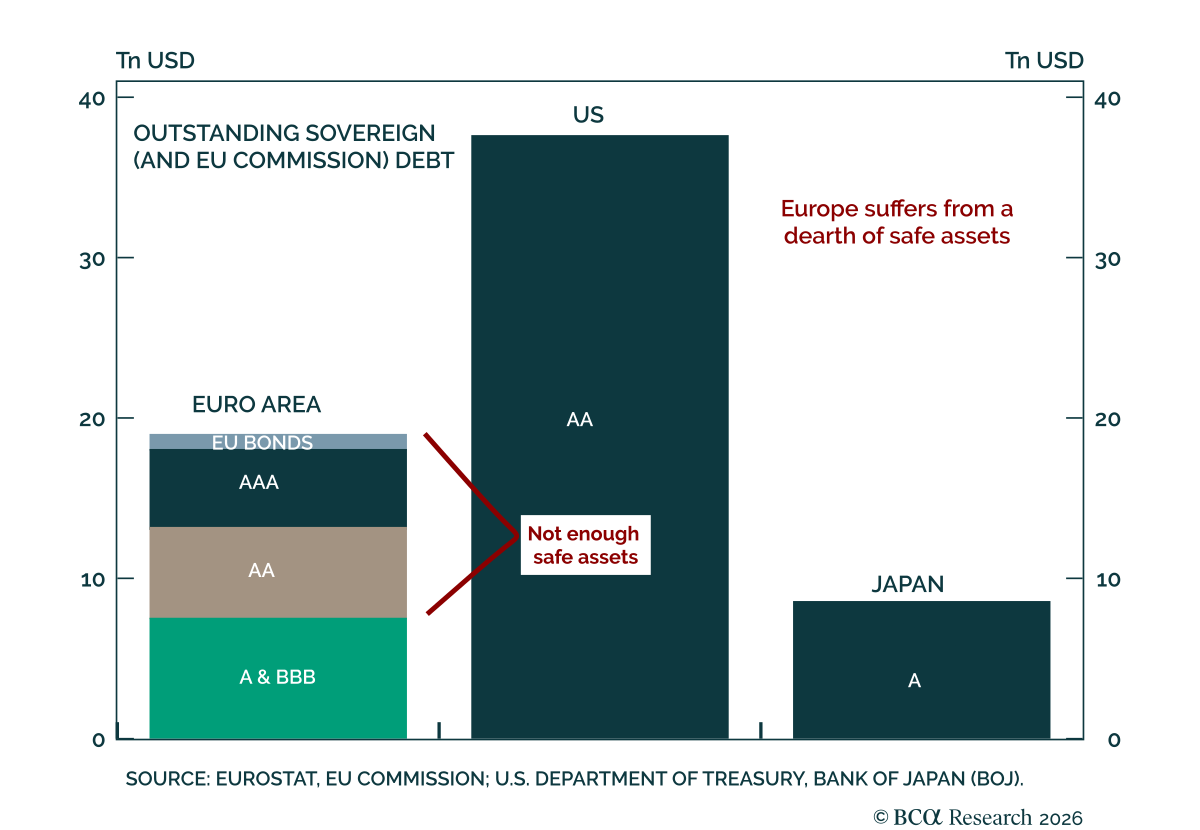

Our DM ex-US strategists make the case for the Eurobond as a structural necessity. The ECB has expanded EUREP (its global euro liquidity facility) to lay the groundwork for currency internationalization, but liquidity infrastructure without a deep pool of risk-free collateral achieves little. Euro-denominated safe assets amount to roughly 30% of the US equivalent, with German Bunds the only genuine safe-haven. That gap constrains EUREP collateral, fragments capital markets, and blocks the reserve flows needed to internationalize the euro.

Our colleagues are clear on the mechanics: Only a stock-and-flow model clears the €3–5 trillion threshold for genuine safe asset status. The Blanchard-Ubide proposal, which swaps national debt for senior Eurobonds up to 25% of GDP, has the broadest institutional backing and requires no Treaty change.

The forces behind the Eurobond debate (dollar fragility, record defense spending needs, and NGEU repayments) are structural rather than cyclical, and the political window is the narrowest since Maastricht. A credible common issuance program would be the first to transform the euro into a genuine reserve asset, eroding the dollar's structural monopoly. Our colleagues favor buying the EUR on dips and recommend betting on Central and Eastern European convergence.