Cuts Exit The Fed Conversation

The April FOMC minutes clarified the hawkish shift that marked the meeting. The Fed held at its last meeting, but there were four dissents. While Governor Miran favored a 25 bps cut, regional presidents Hammack, Kashkari, and Logan supported a hold but voted against the easing bias in the statement.

A majority of the FOMC voted to keep the easing bias in the statement, but the minutes showed that a majority of participants (not voters), said that “some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%”. The minutes also show many officials would have preferred removing the easing bias. That is a meaningful shift from debating the timing of the next cut, and suggests the Fed is likely to stay on hold for a while.

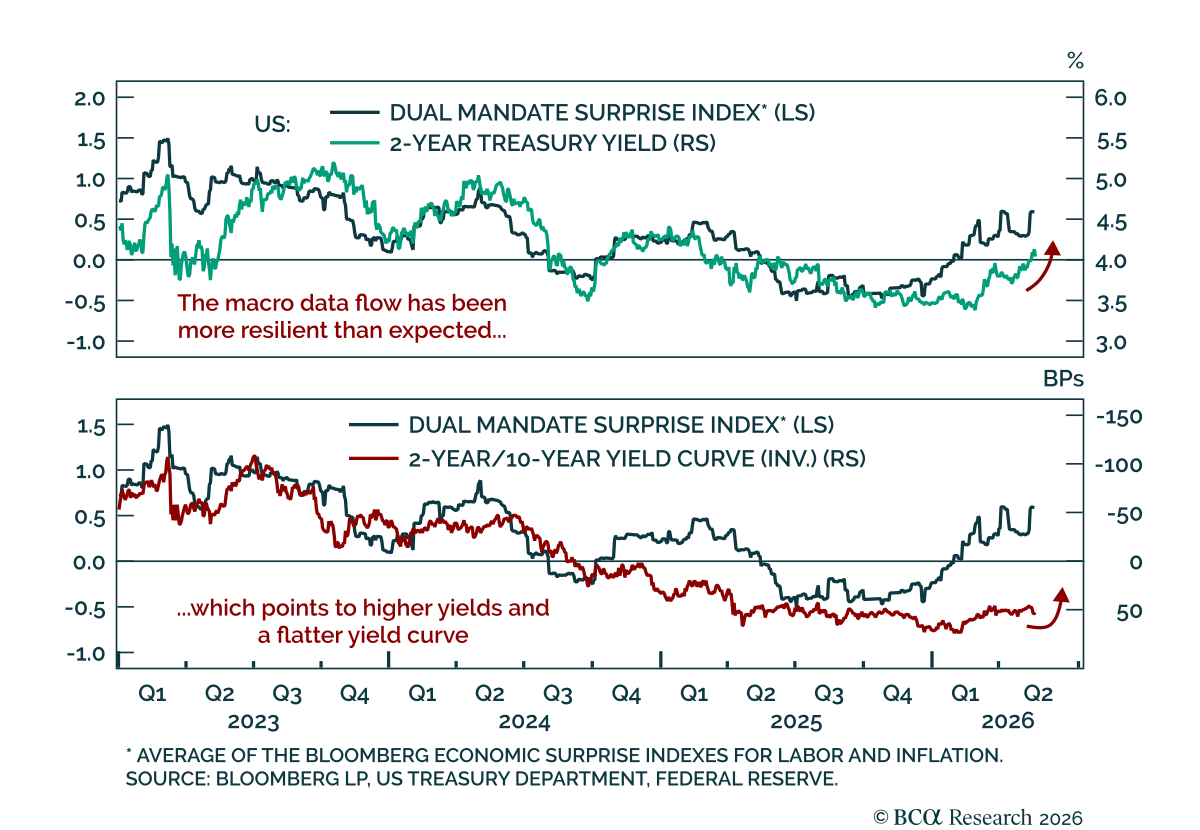

Our dual mandate surprise index, which combines employment and inflation surprises, points to some further upside for yields. Both sets of surprises were gaining momentum before the Iran war. Employment data has been more resilient than expected, while inflation surprises have picked up more recently. Our US growth diffusion index also points to resilient growth. Our Global and US Rates strategists are downgrading global and US portfolio duration from above- to at-benchmark, as the risk of hawkish monetary policy surprises is rising. We are not seeing second-round effects yet, but inflation expectations have risen and could trigger a more hawkish Fed.