AI Is STILL The Business Cycle

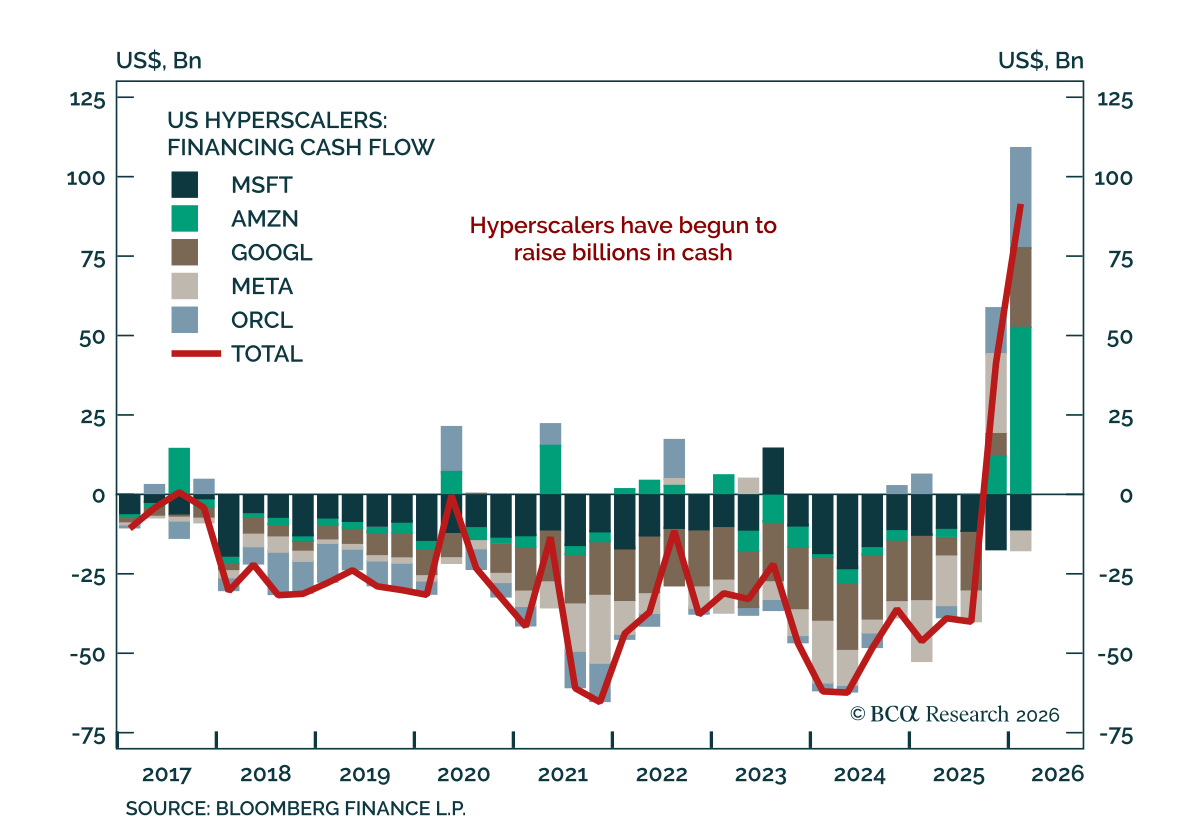

Our Global Asset Allocation strategists upgrade equities to overweight at the expense of cash, moving EU equities from overweight to underweight while upgrading the US to neutral. Our colleagues argue AI remains the central market thesis despite the oil shock. Recent hyperscaler results reinforce this view, as capex momentum is intact and showing early signs of positive return on investment. The Hormuz closure has ended the broadening trade that dominated early 2026, squeezing consumers globally and pushing easy monetary policy off the table for most central banks this year.

The AI investment cycle is what separates this shock from prior oil episodes. Our colleagues see AI-driven capex as endogenous. Firms are spending regardless of consumer health, buffering the cycle against demand destruction. EU households face disproportionately greater strain than US consumers, and with the US carrying substantially higher tech exposure, the relative case for American equities has widened since the conflict began.

Equity exposure has fallen sharply since the war started, creating a wall of worry for markets to climb. Positioning is considerably lighter than pre-war levels even as earnings remain constructive. The current administration's sensitivity to falling markets skews the return distribution to the upside. Our colleagues maintain tail risk hedges.