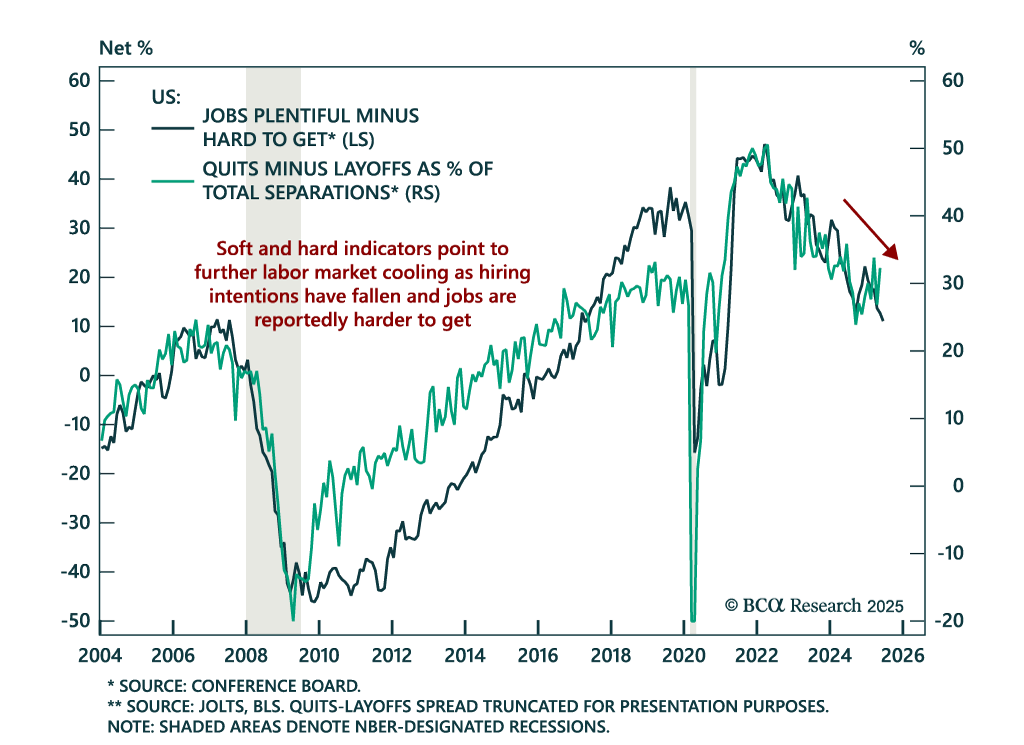

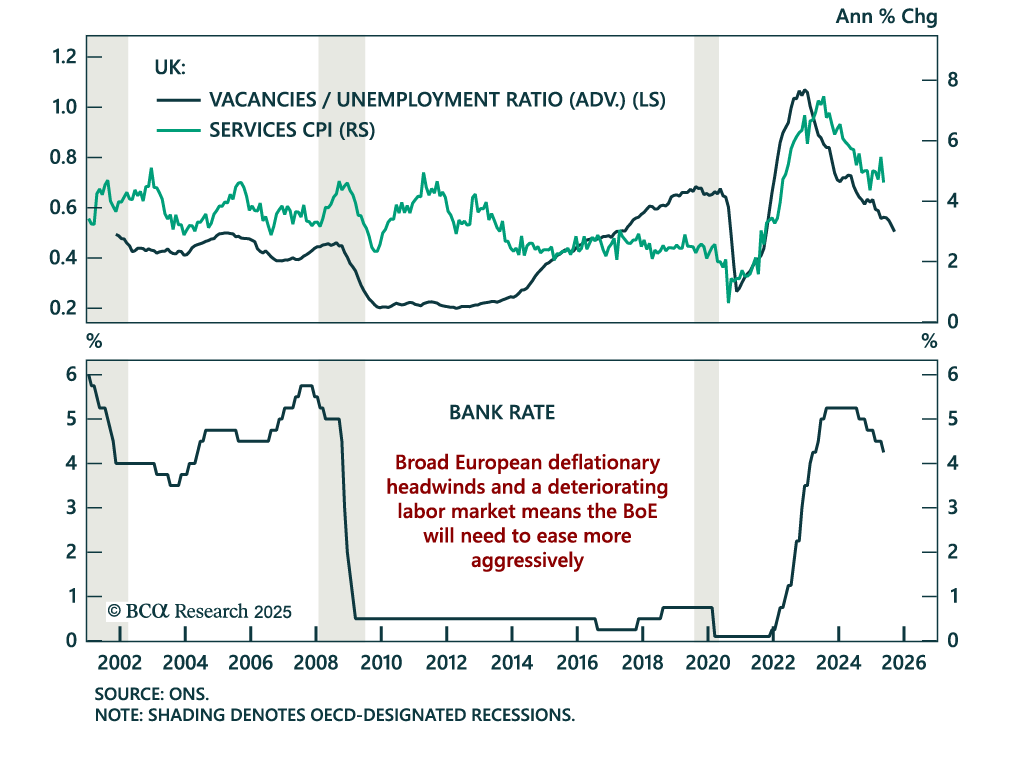

Labor Market

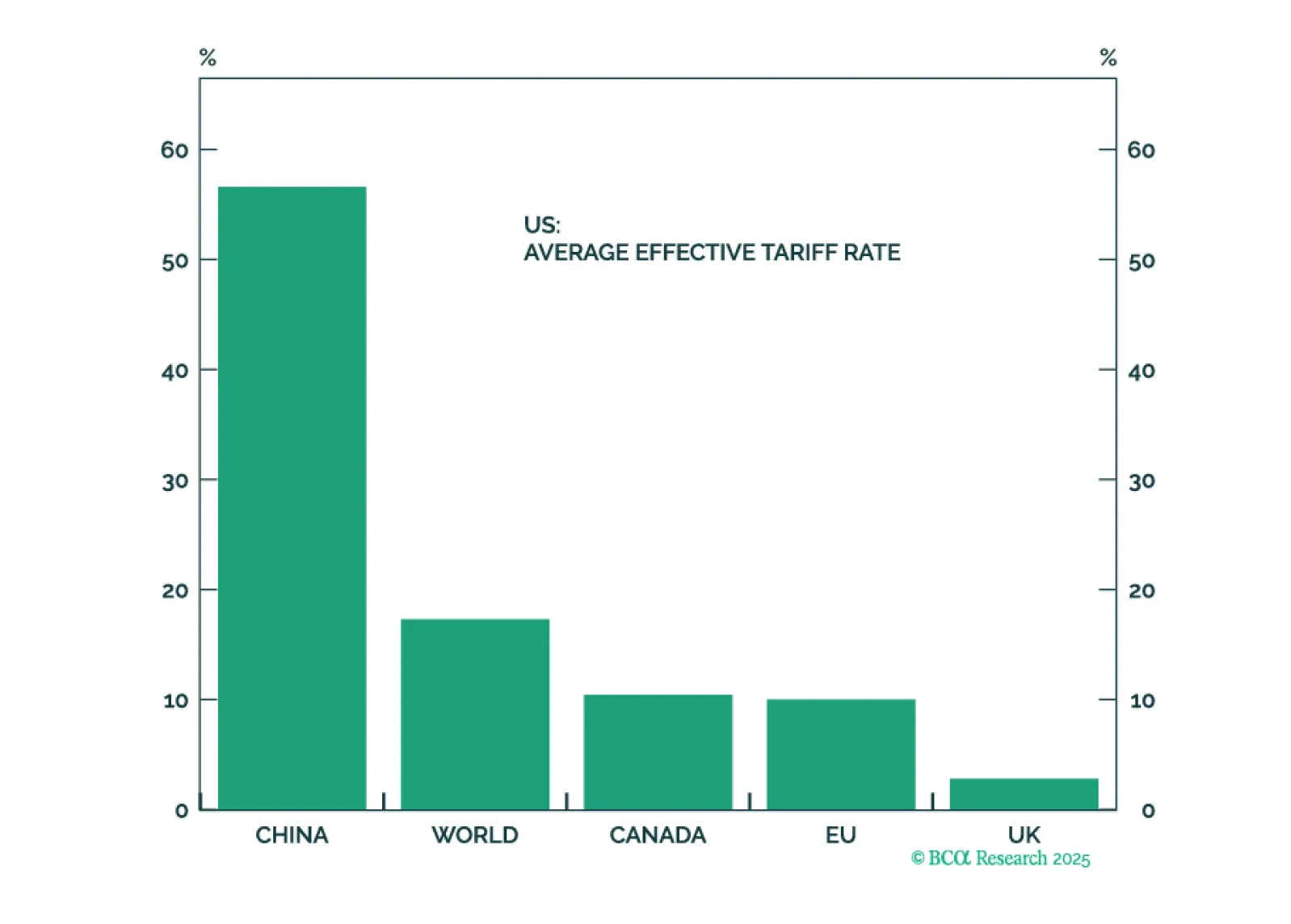

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

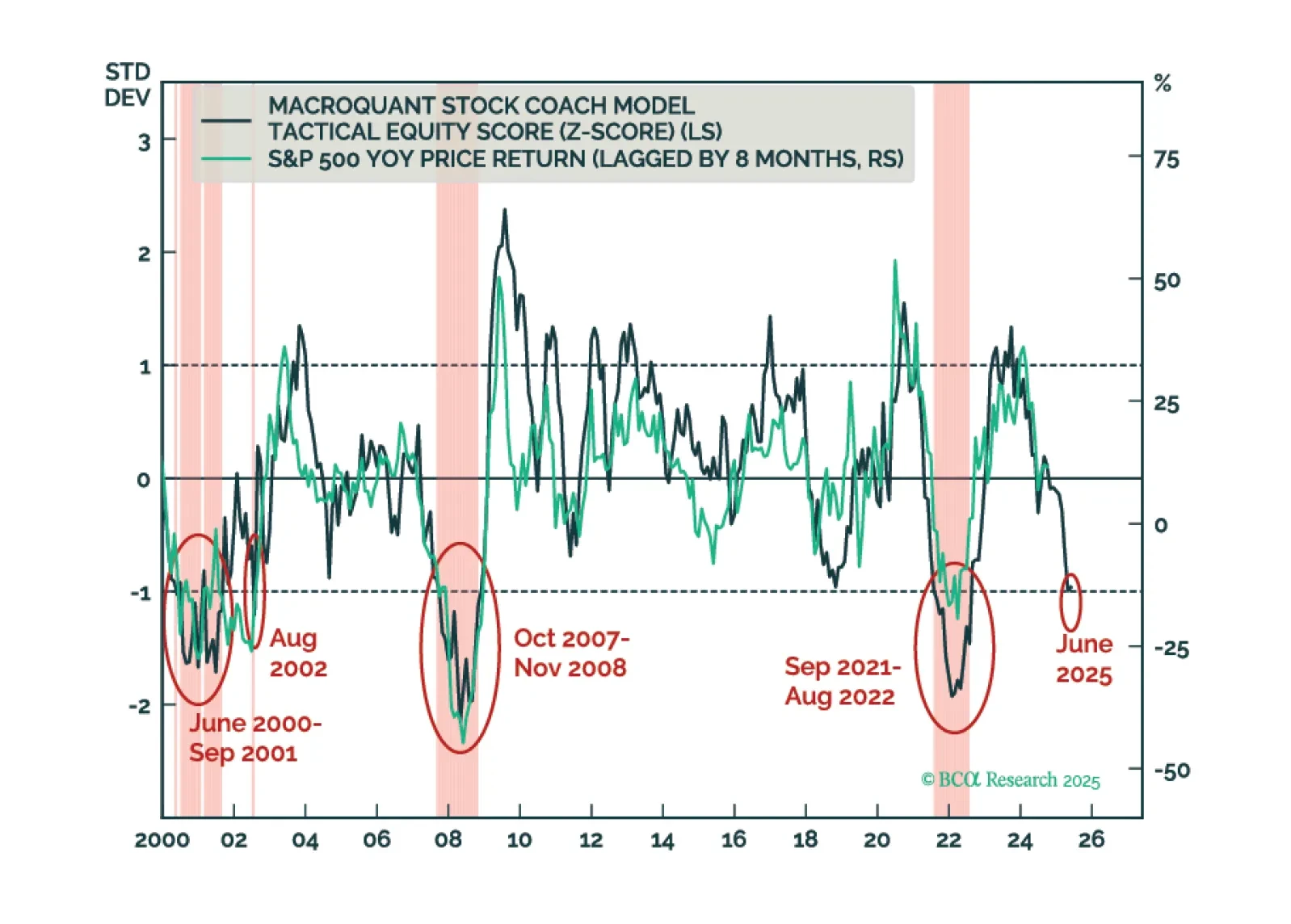

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

In Section II, Jonathan presents the bullish case for the US dollar over the coming year.

In Section I, Doug underscores that the full weight of tariffs has yet to be felt on the US and global economies, against the dangerous backdrop of a softening labor market. In Section II, Jonathan presents the bullish case for the US dollar over the coming year.

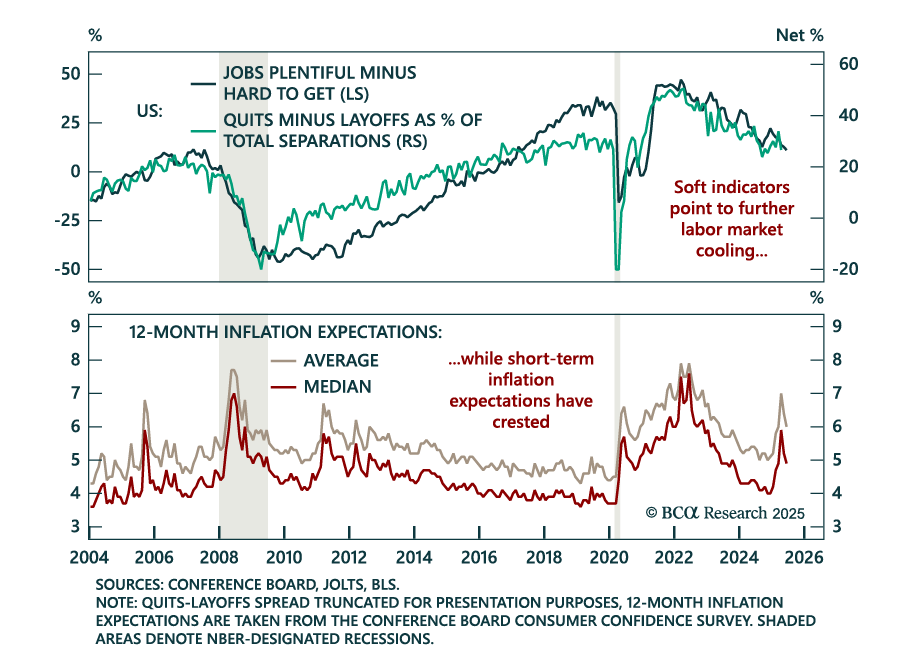

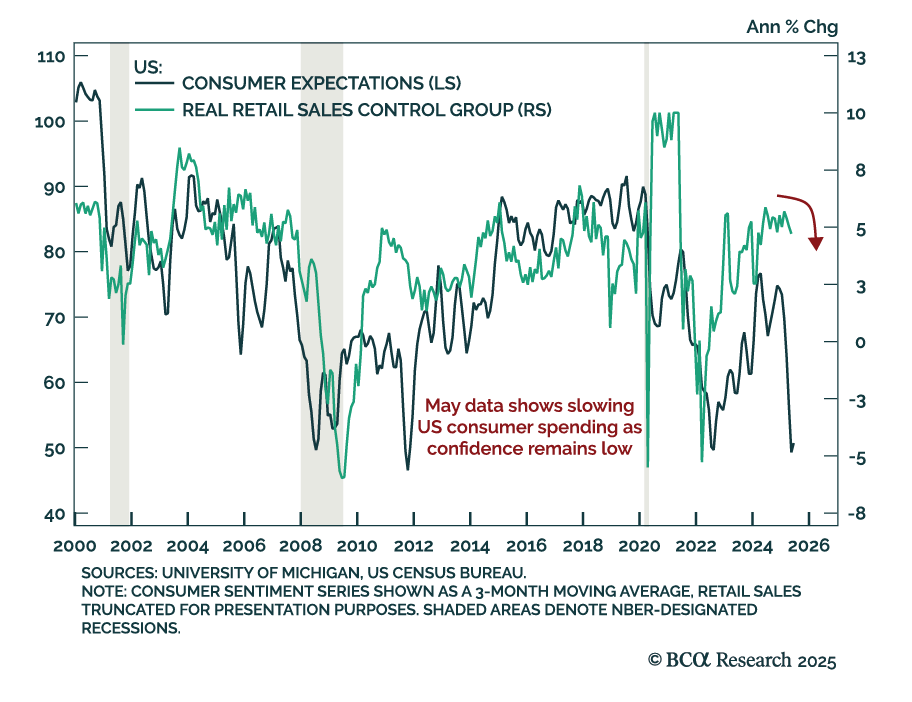

Following a rapid-fire review of issues related to household balance sheets, durable goods demand, the impact of tariffs, DOGE’s capacity to move the budget needle and the labor market’s ongoing cooling, we reiterate our defensive asset allocation recommendations.