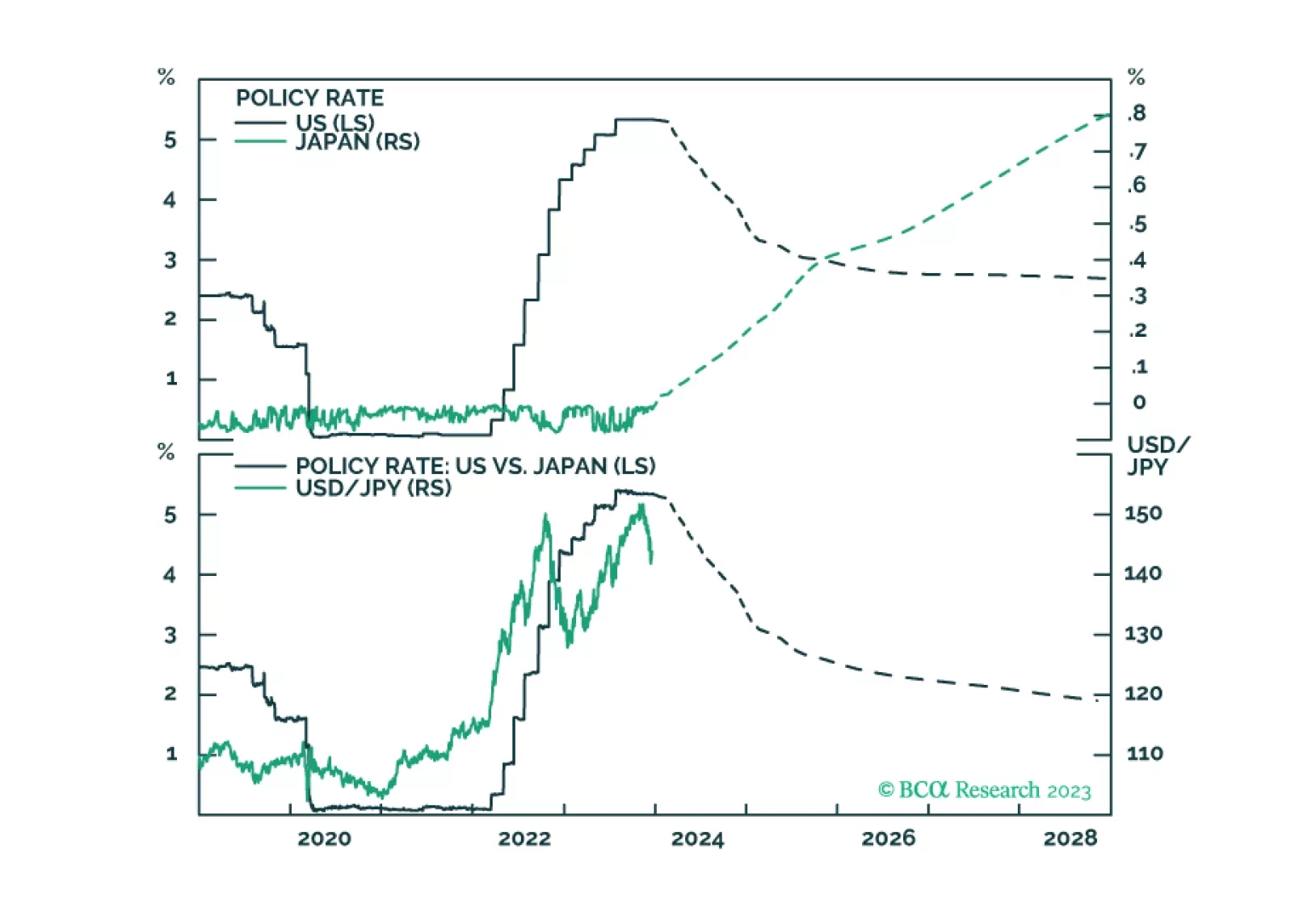

Japanese Yen

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

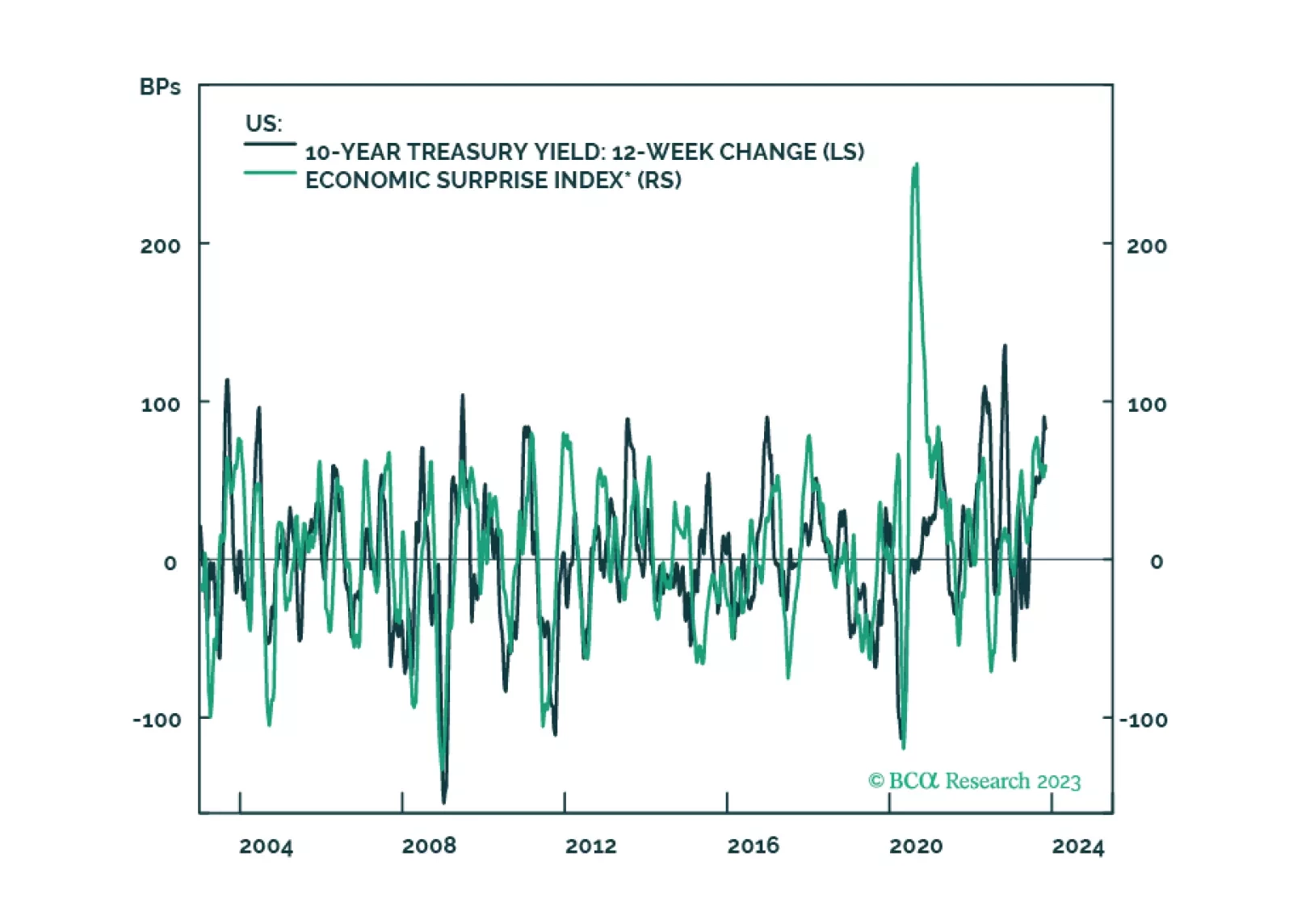

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

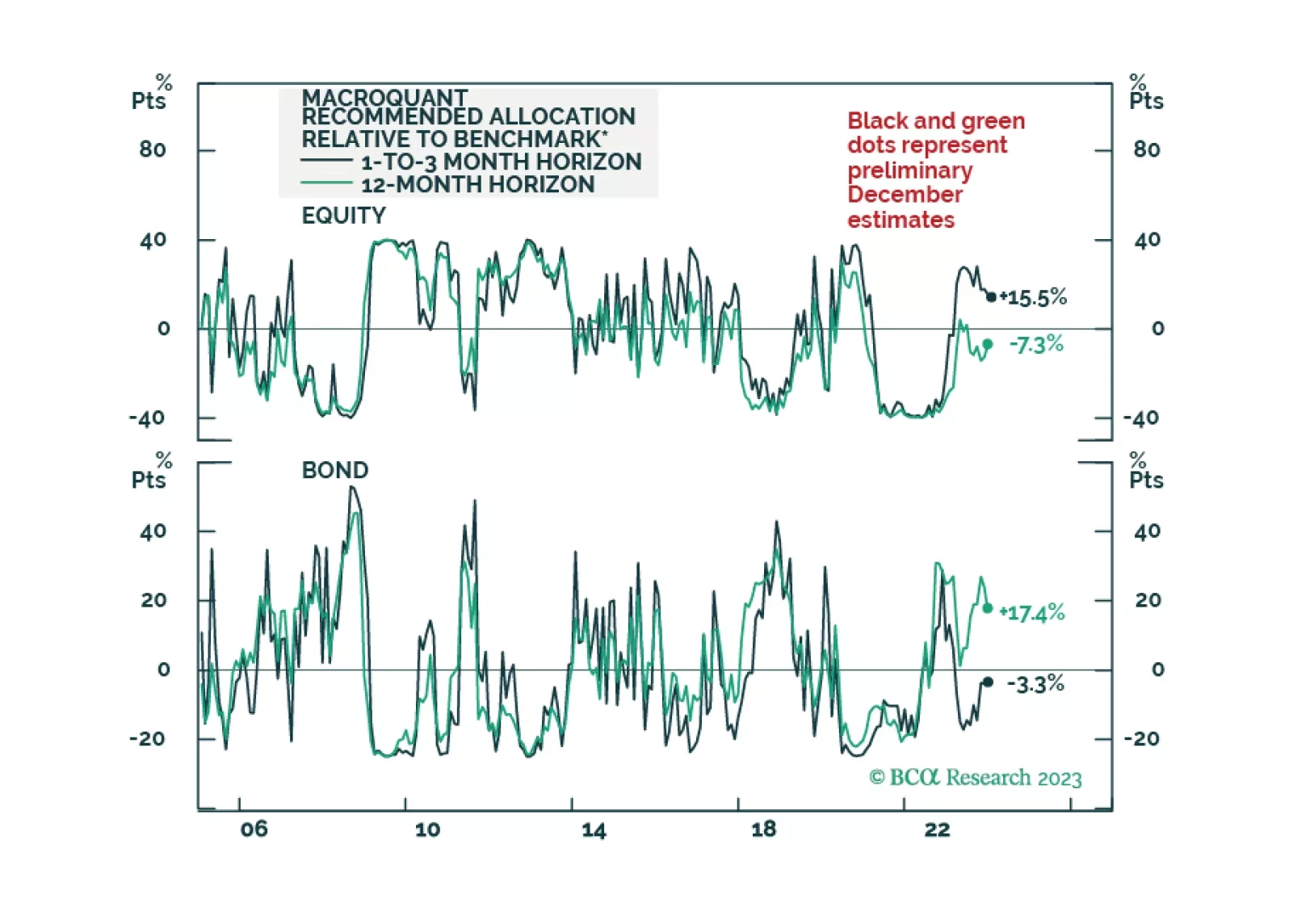

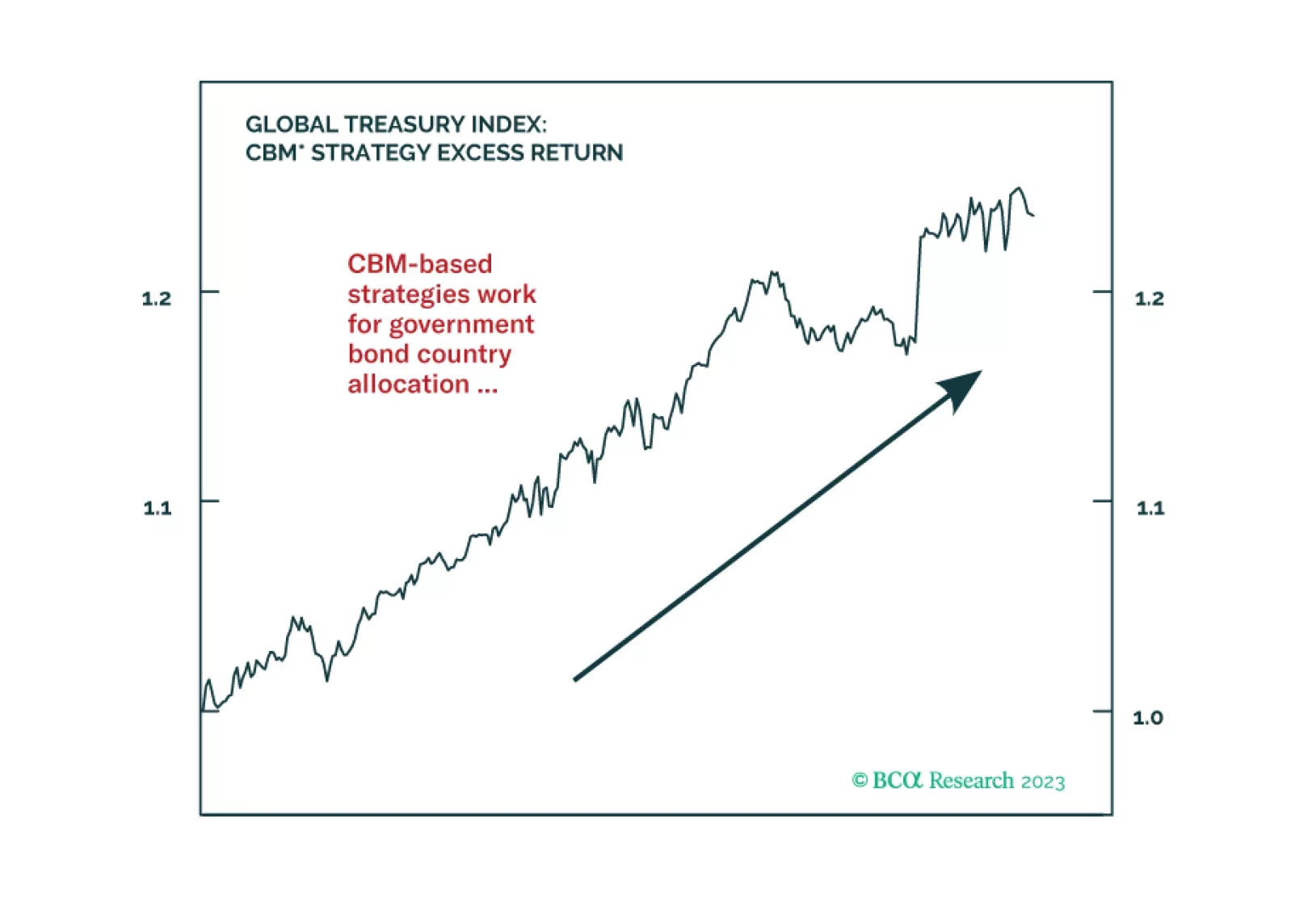

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.