Geopolitics

The outgoing Biden administration has launched a slew of macro-relevant executive orders and regulatory actions. The one with immediate macro implications are the sanctions against Russian oil traders and its “dark fleet” of oil tankers.

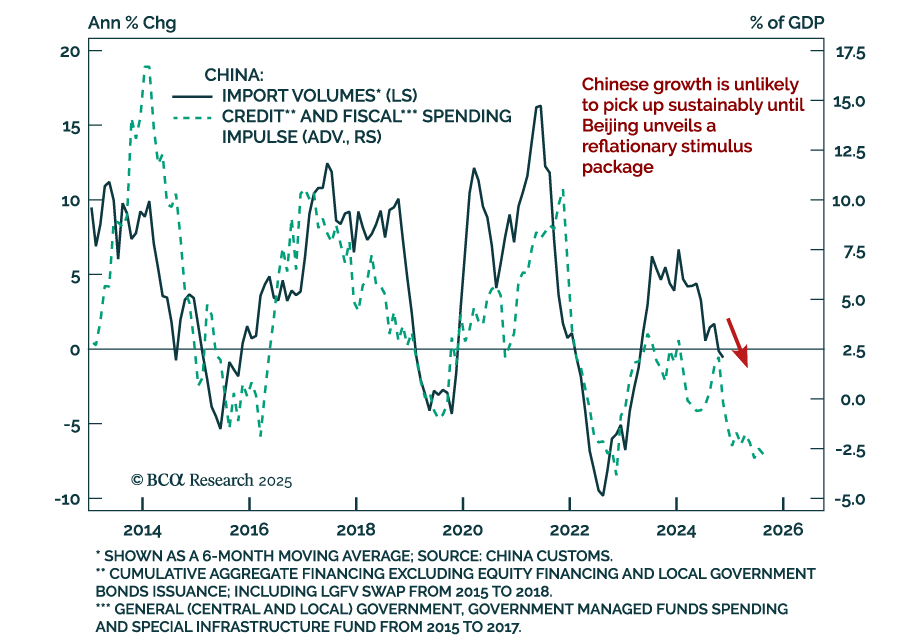

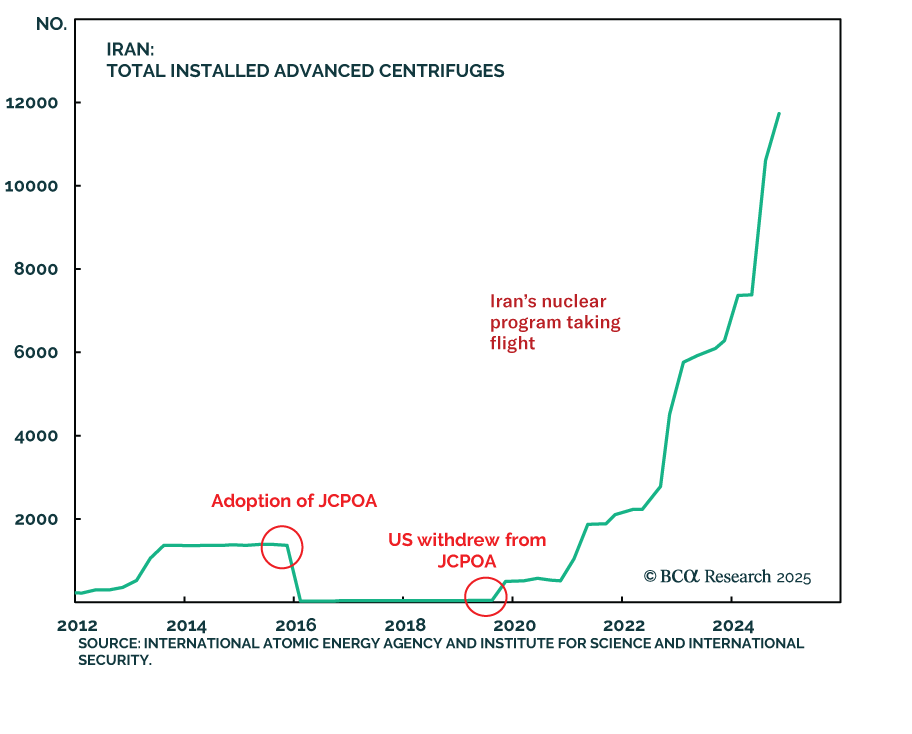

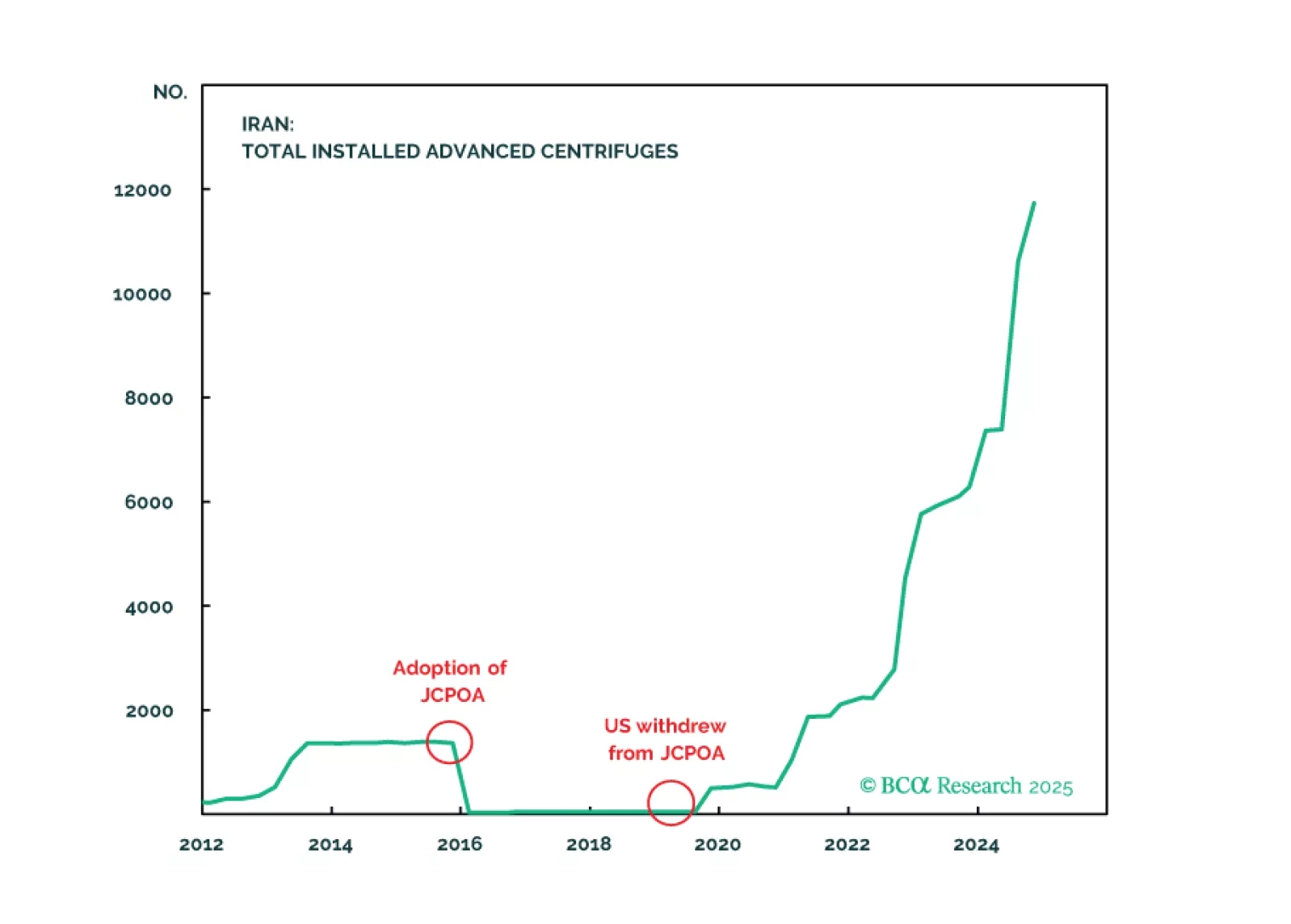

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.