Currencies

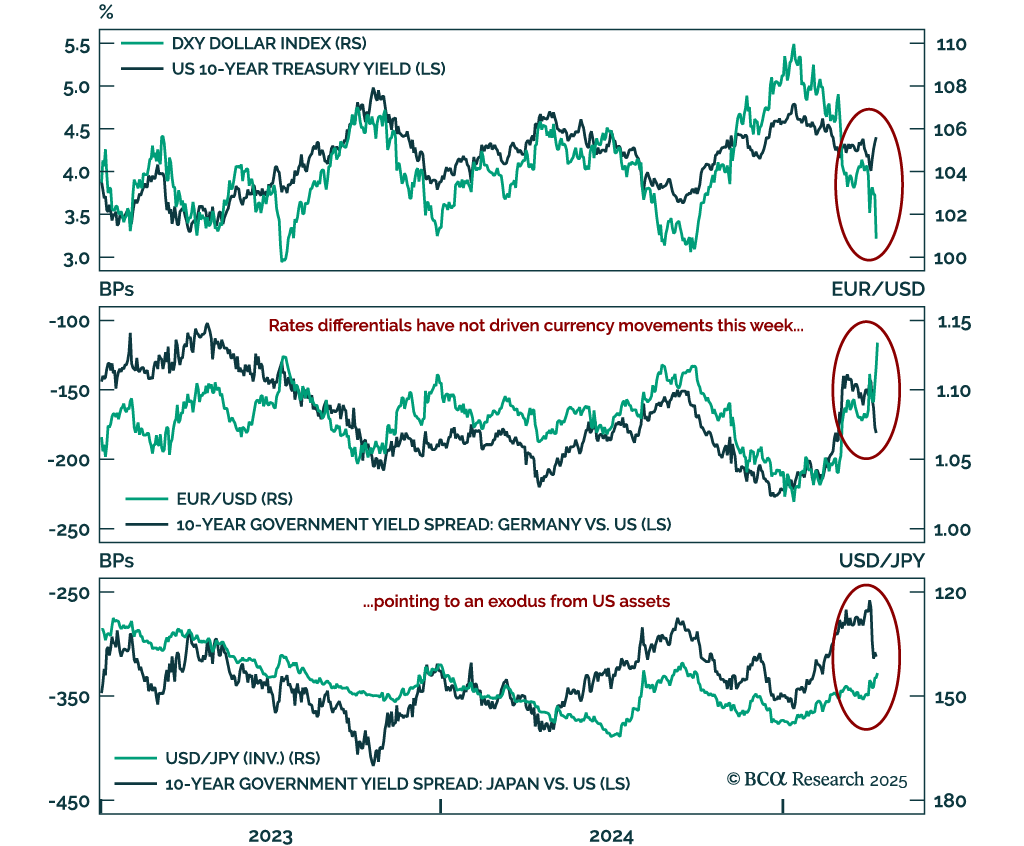

This week, we look at the sustainability of the HKD peg as the next whale to move markets, given what is happening to tariffs. After careful analysis, our bias is that it is here to stay. With the DXY dipping below 100, we are likely to see a rebound, which is actually bad news for the Hong Kong region of China, since it will tighten financial conditions. We have no new short-term trades, but if the peg broke, you want to be short HKD/JPY.

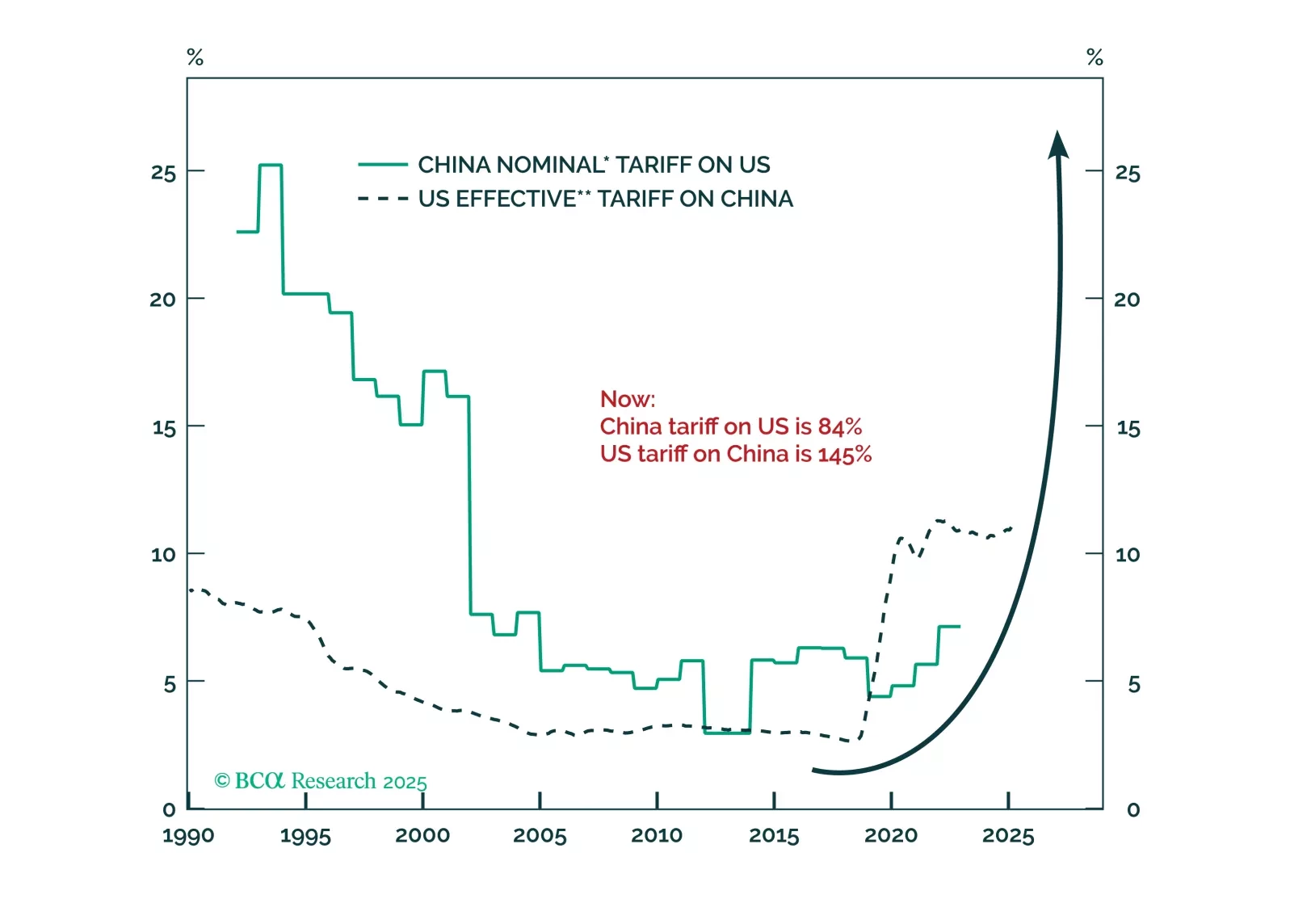

China’s aggressive retaliation against U.S. tariffs will enable President Trump to shift from punishing allies and redirect the trade war toward China. If Beijing does not react to the latest tariffs by doubling its fiscal stimulus, it indicates they are planning something different, as China will encounter economic destabilization. The likelihood of a hybrid military pressure on Taiwan will rise.

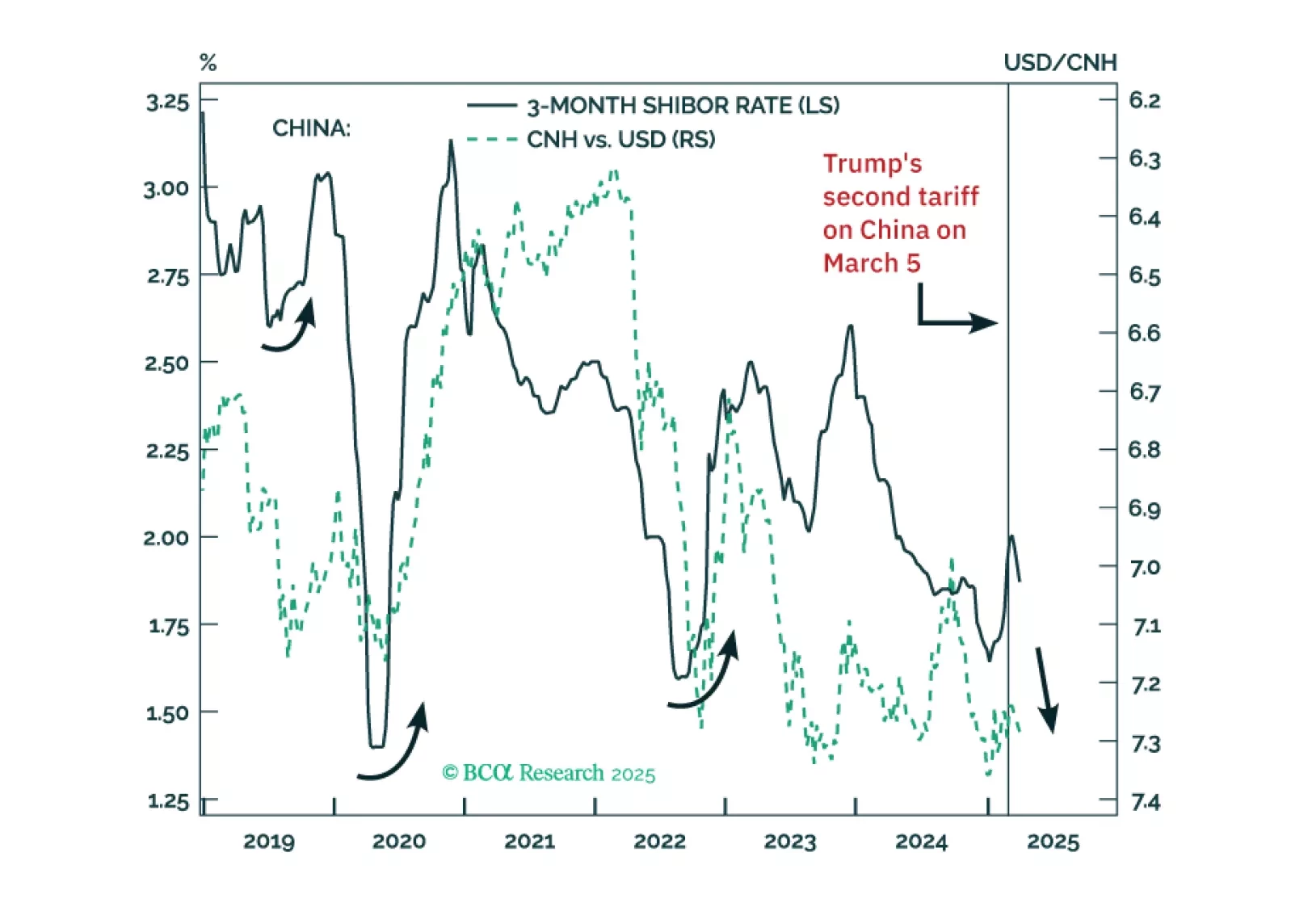

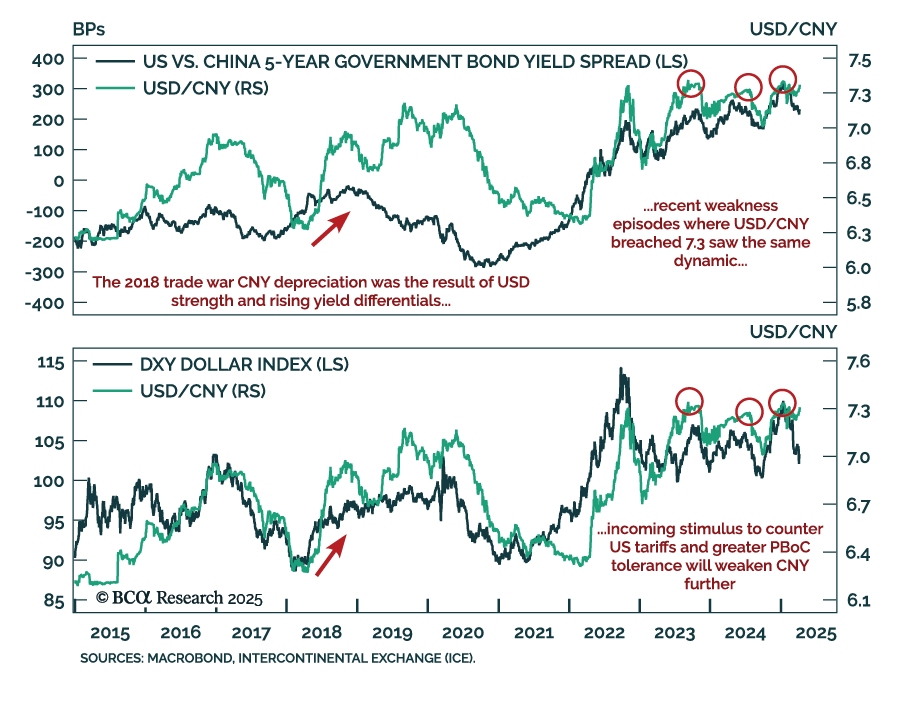

We believe Beijing views these US trade actions as nothing short of a declaration of economic war, not just a trade dispute. The US-China confrontation is set to escalate from here. Chinese authorities will allow the yuan to depreciate materially. Go short CNH against the US dollar. For EM and Asian equity portfolios, we are downgrading Chinese investable/offshore stocks from neutral to underweight.

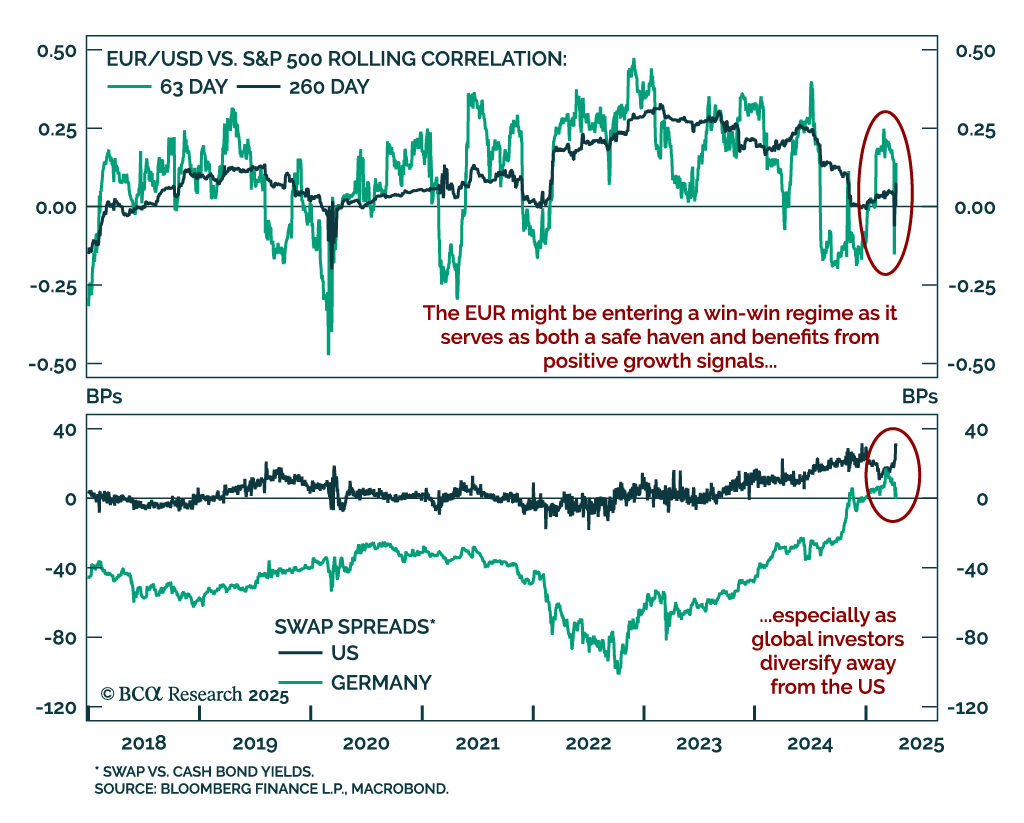

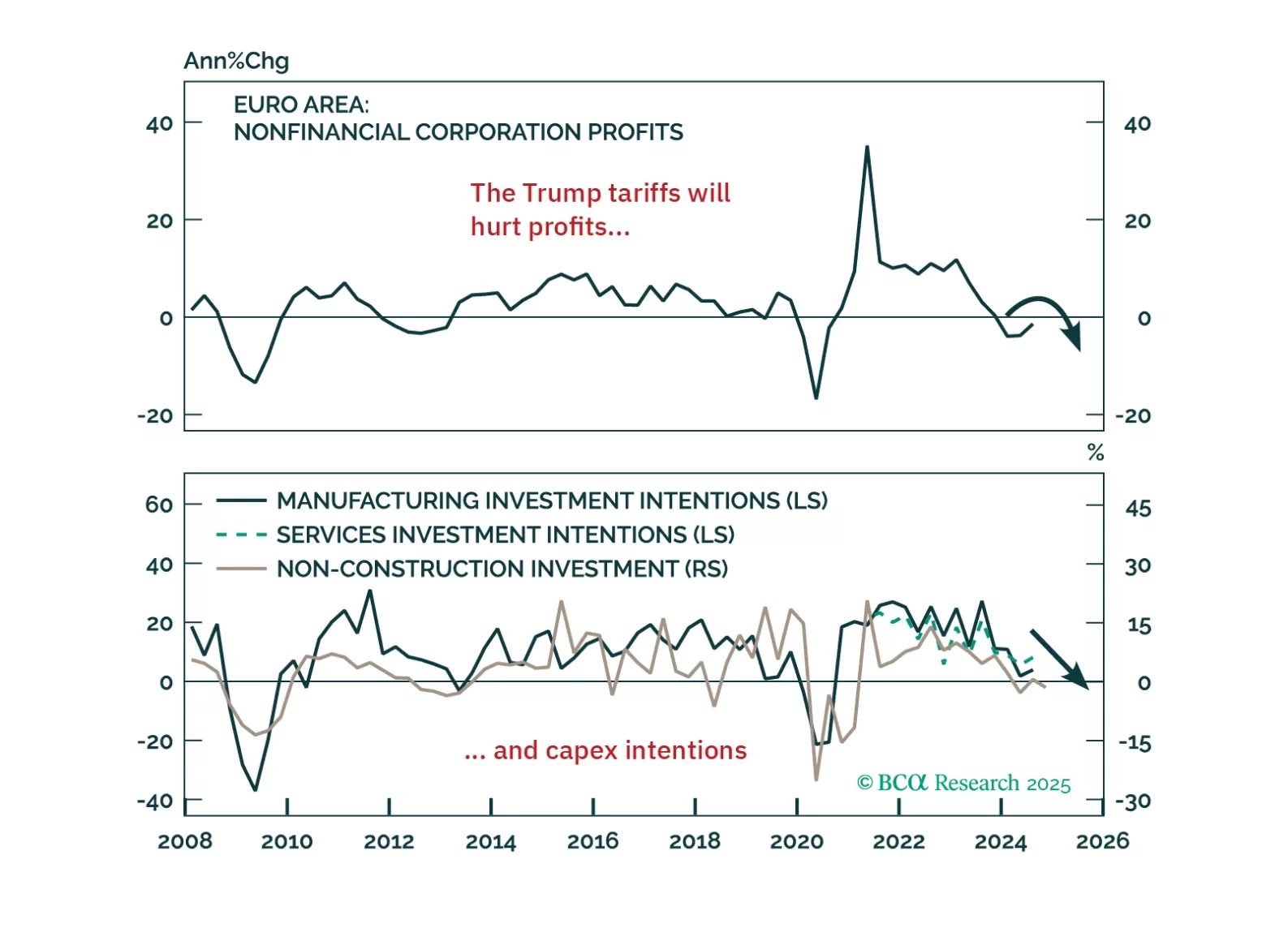

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

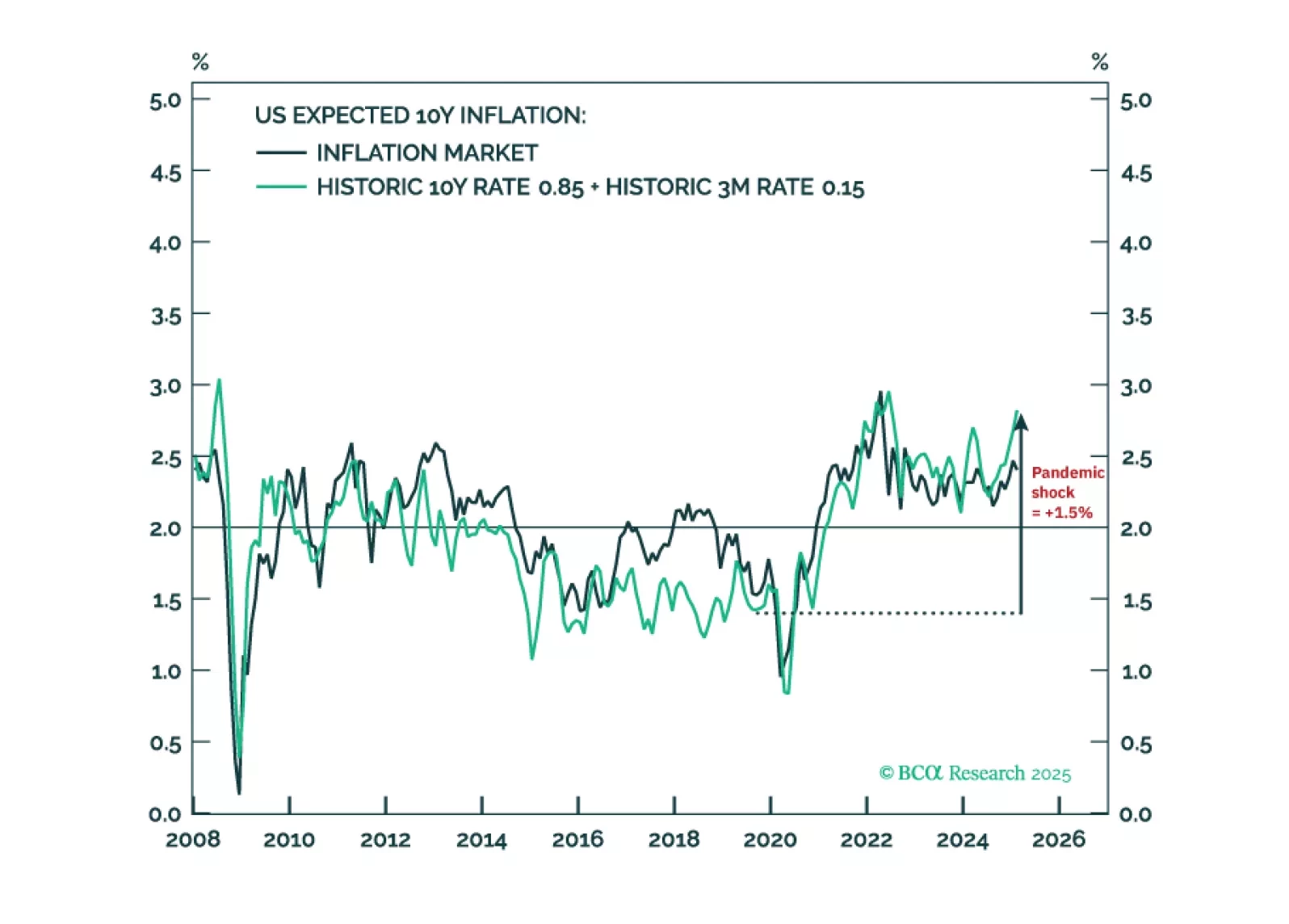

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.