Consumer

Chinese new loans grew from CNY 10.2 tr to CNY 11.1tr in May, disappointing expectations of CNY 11.3tr. Year-to-date aggregate financing also came short of anticipations, growing from CNY 12.7tr to CNY 14.8tr. Notably, the contraction in M1 worsened from 1.4%…

Global consumer spending is likely to slow over the coming quarters, culminating in a major economic downturn in late 2024 or early 2025. Investors should maintain benchmark exposure to equities for now but look to turn more defensive by the end of this summer.

The Eurozone Sentix Economic index improved from -3.6 to 0.3 in June, easily surpassing expectations of a more muted improvement to -1.7. Notably, the Expectation and Current Situation subindices rose to 28-month and 13-month highs of 10 and -9, respectively.…

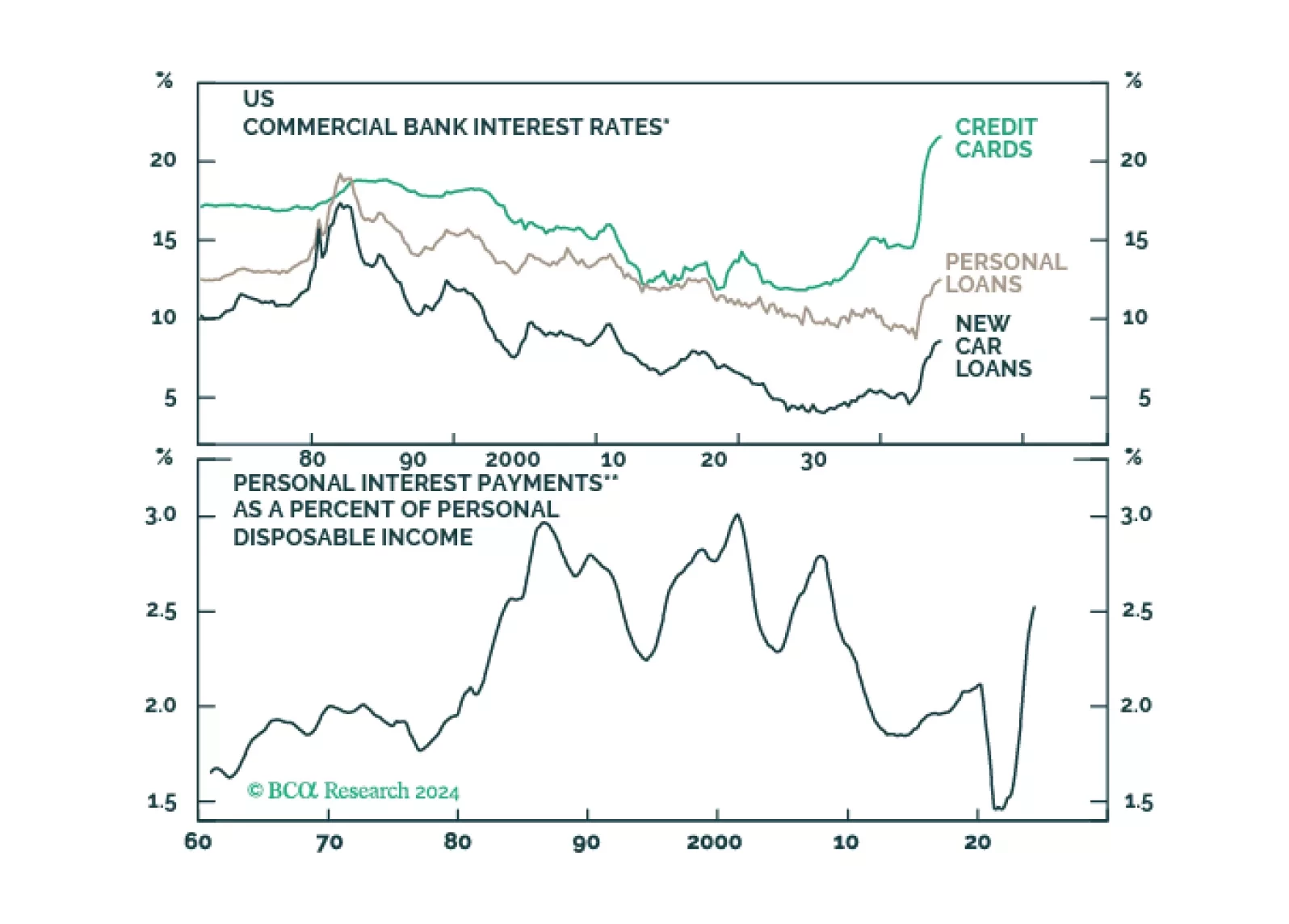

Total consumer credit rose by USD 6.4 billion in April (to USD 5,053 billion outstanding), from a USD 1.1 billion decrease in March (a large downward revision to the USD 6.3 billion rise initially reported) and significantly shy of expectations for a USD 10…

The redeployment of pandemic-era excess savings has been a significant driver of US consumption growth and helped the economy avoid a recession last year. Although pandemic-era fiscal support was less generous in China, households nevertheless accumulated CNY…

Consumption accounts for two-thirds of the US economy, and our recession view relies heavily on the deteriorating outlook for US consumers. That said, dissecting US GDP into its components reveals that consumption tends to merely stabilize during…

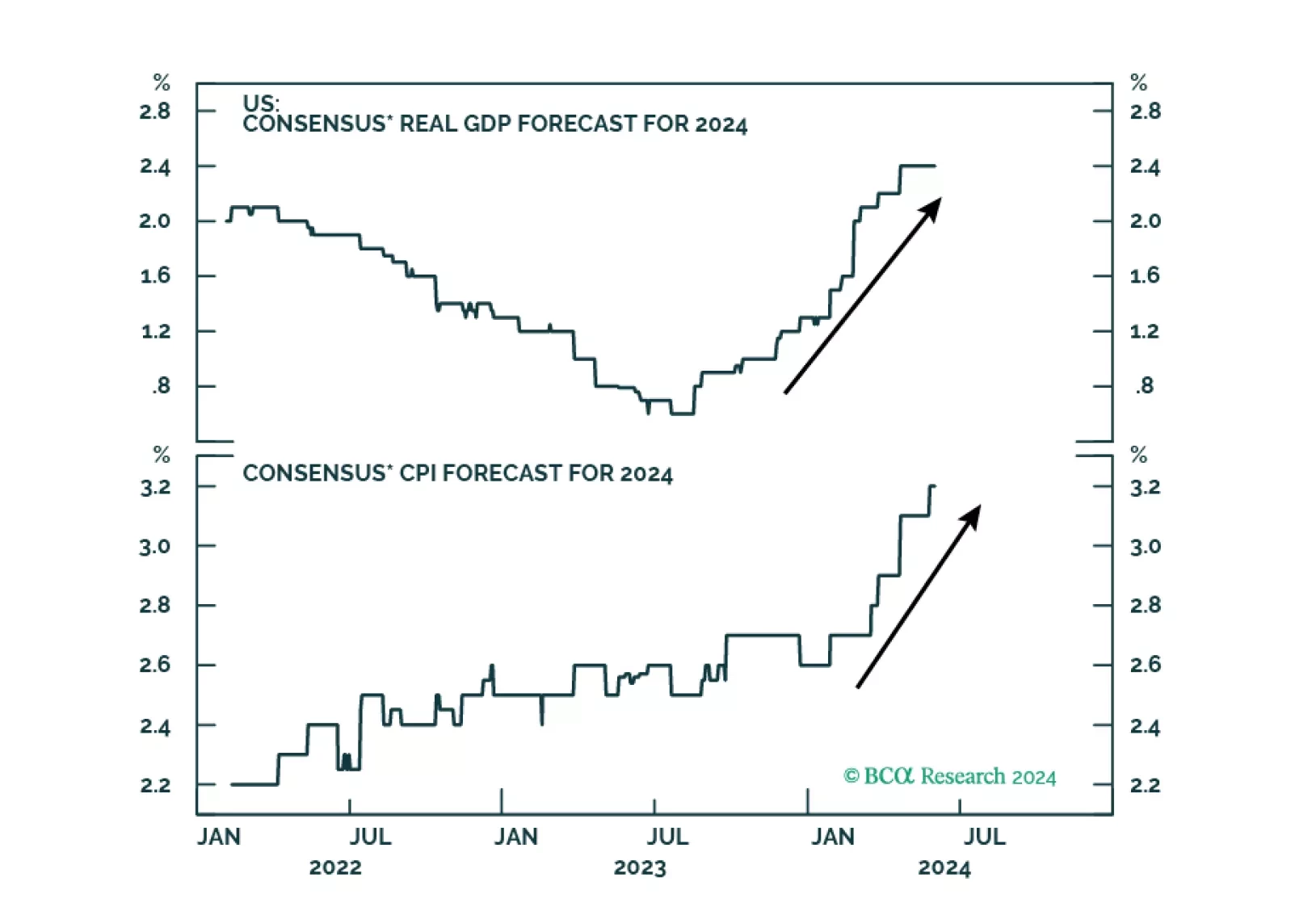

According to BCA Research’s Global Asset Allocation service, the economy has been in the “Overheating” phase of the cycle for a while, with signs of slowing growth but also stubbornly high inflation. The most likely next phase is “Recession,” though the…

According to BCA Research’s Commodity & Energy Strategy service, the oil demand forecasts from the IEA, EIA, and OPEC are too optimistic. The IEA, EIA, and OPEC all anticipate oil demand growth to slow this year following a robust post-pandemic…

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised higher. Real final sales to…