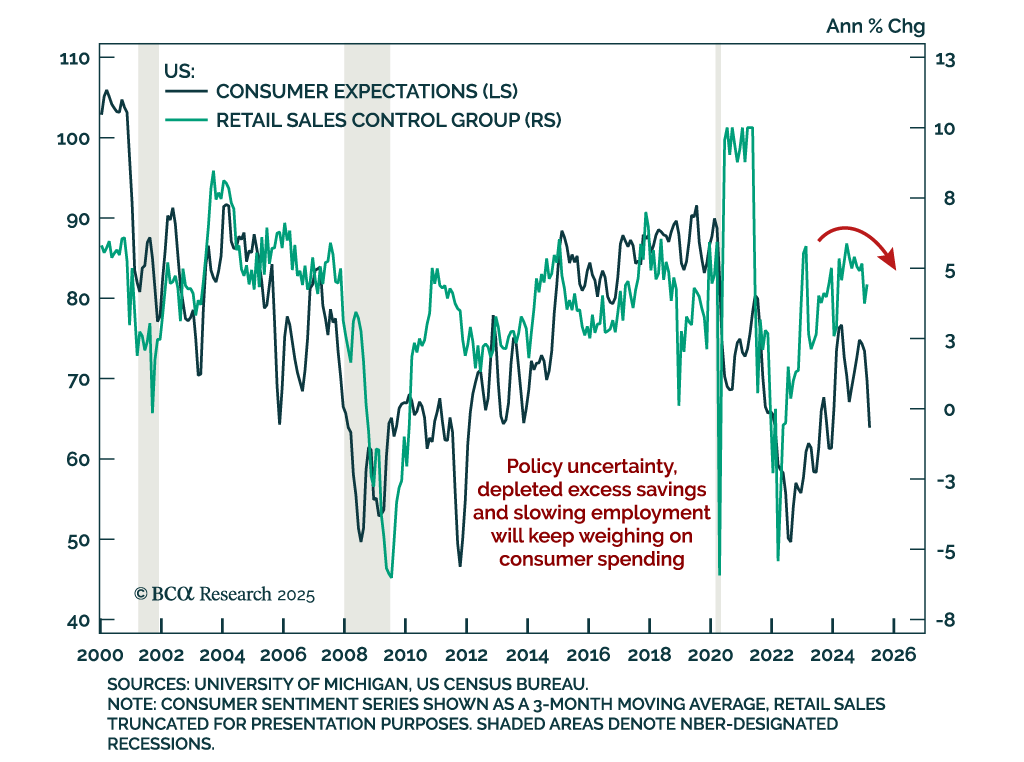

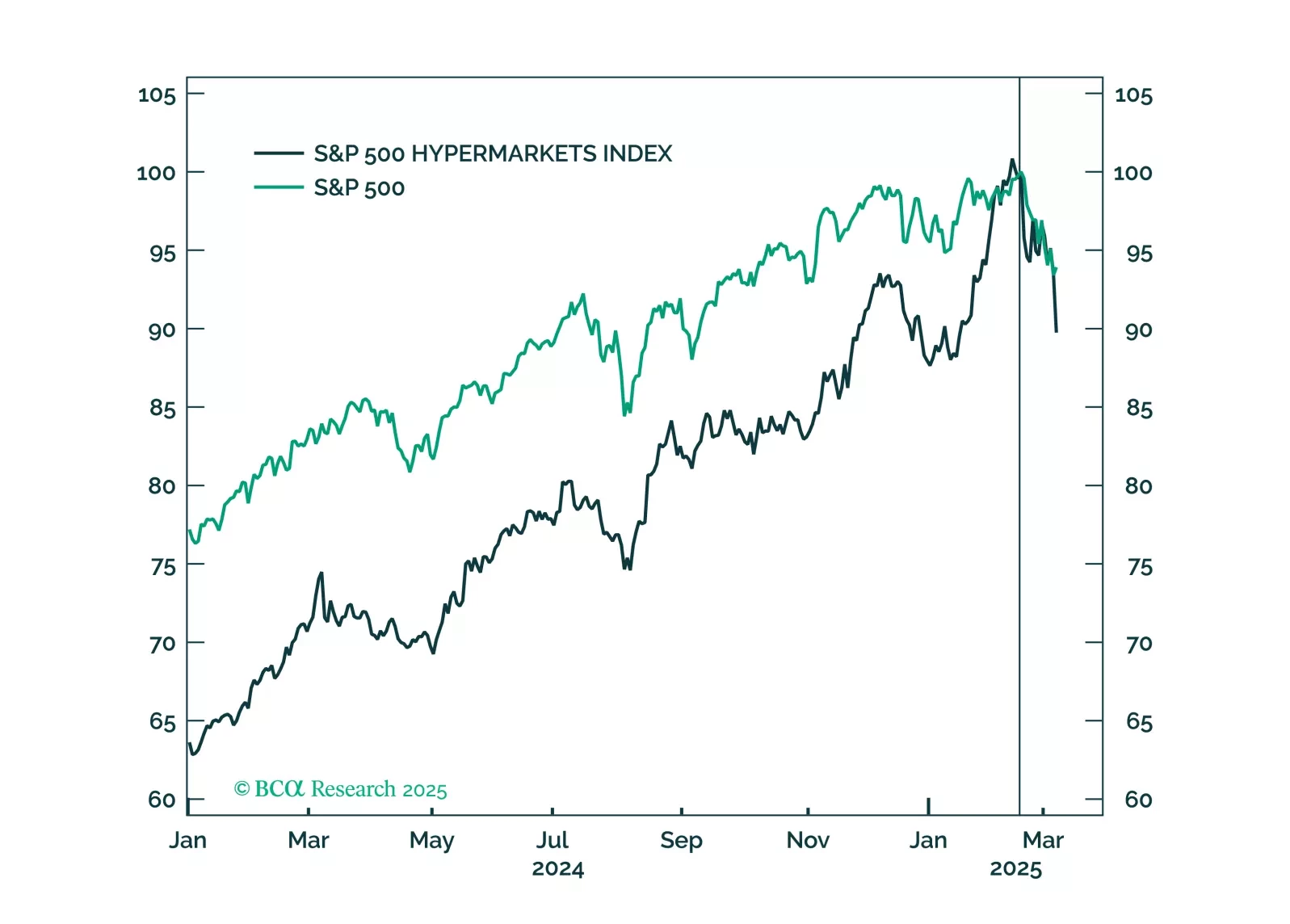

Consumer

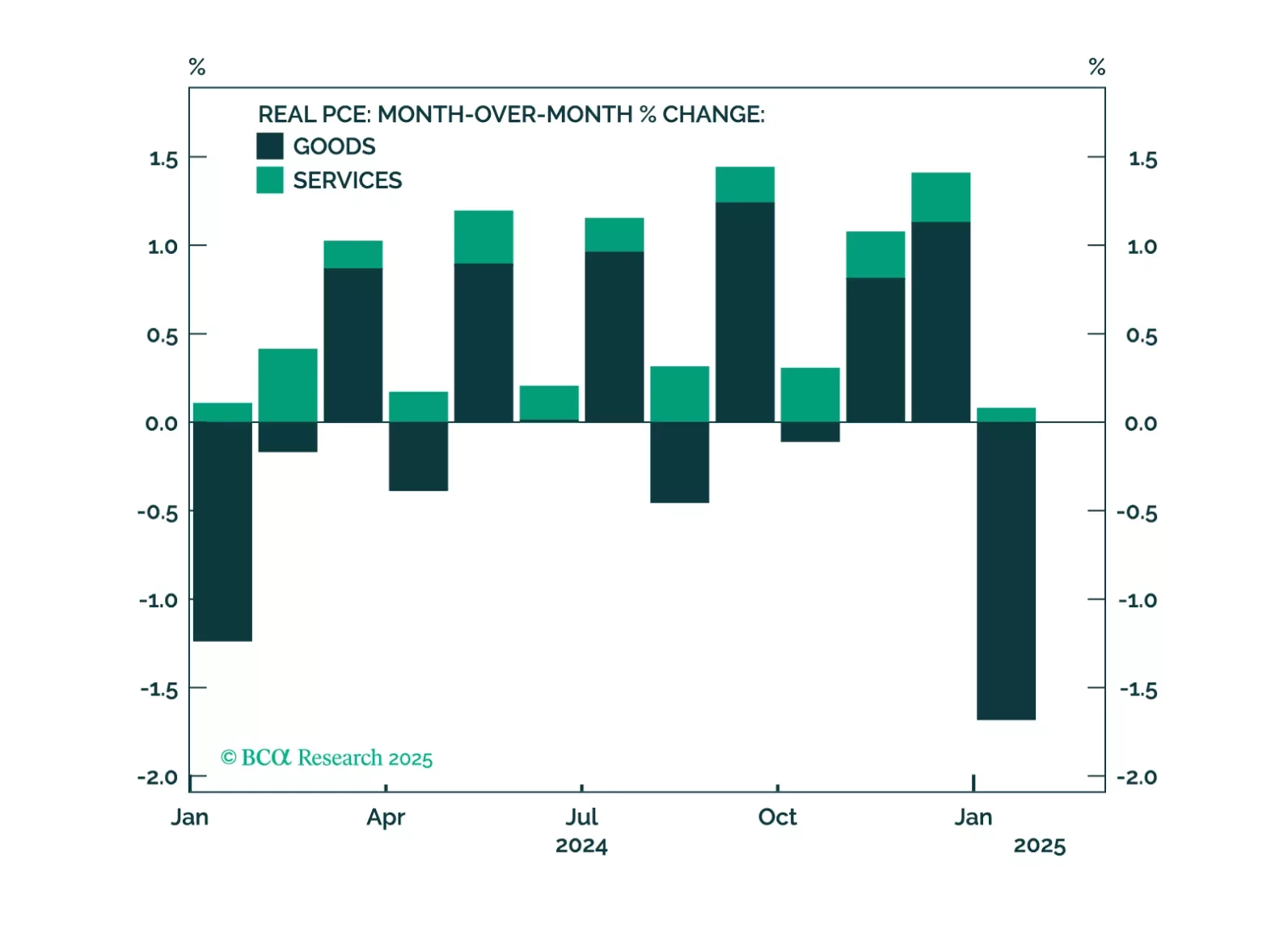

The Q4 earnings results were spectacular but are now in the rear-view mirror. Now, investors are laser-focused on tariff threats, earnings headwinds brought about by a stronger dollar, and an unhappy consumer. Our analysis of earnings commentary found that, while companies often refer to tariffs during their earnings calls, most are perplexed and still in a “wait and see” mode. A strong dollar is negative for earnings, but the recent dollar retrenchment will bring relief. Wealthy consumers are still spending, but there are early signs of stress.

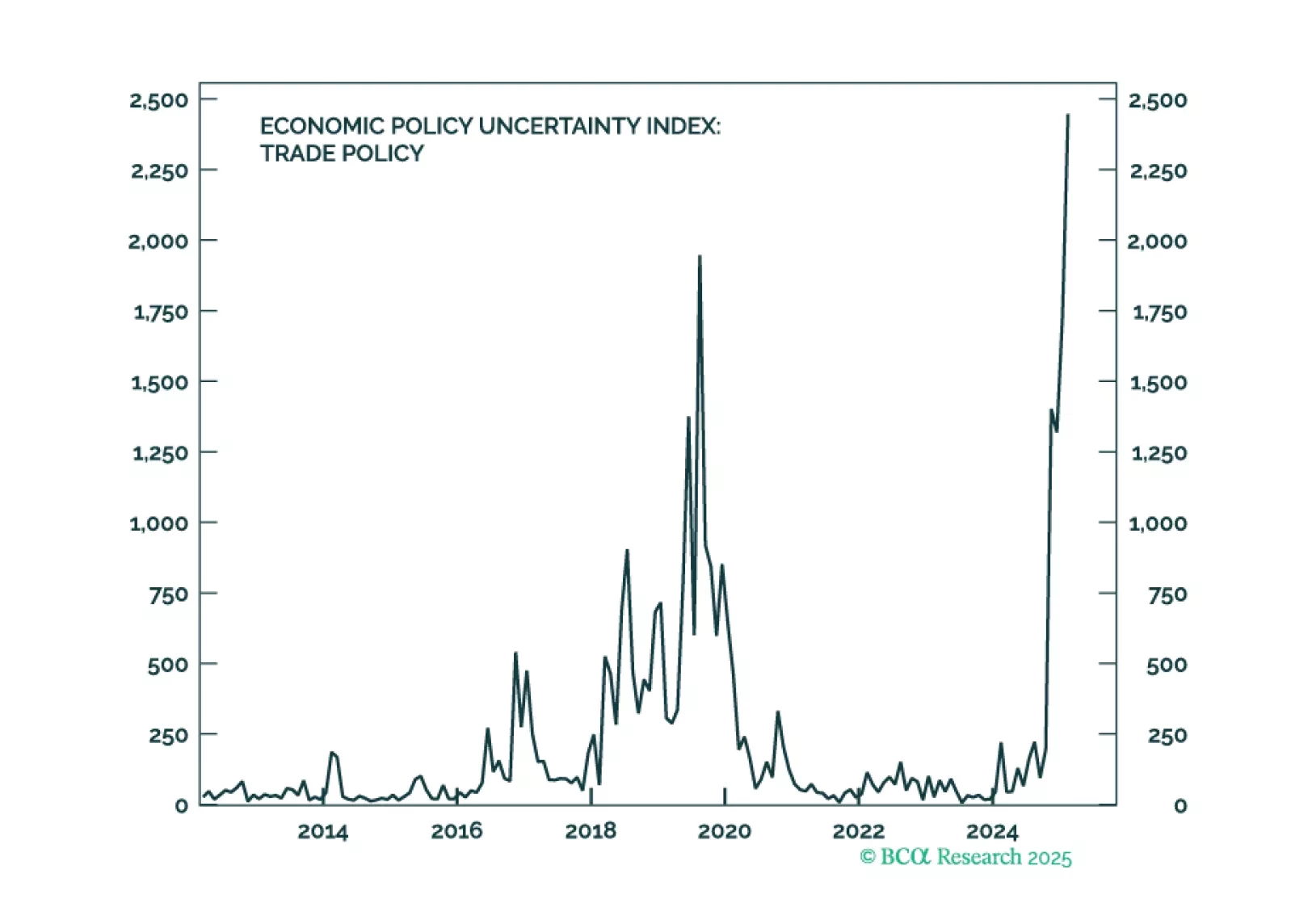

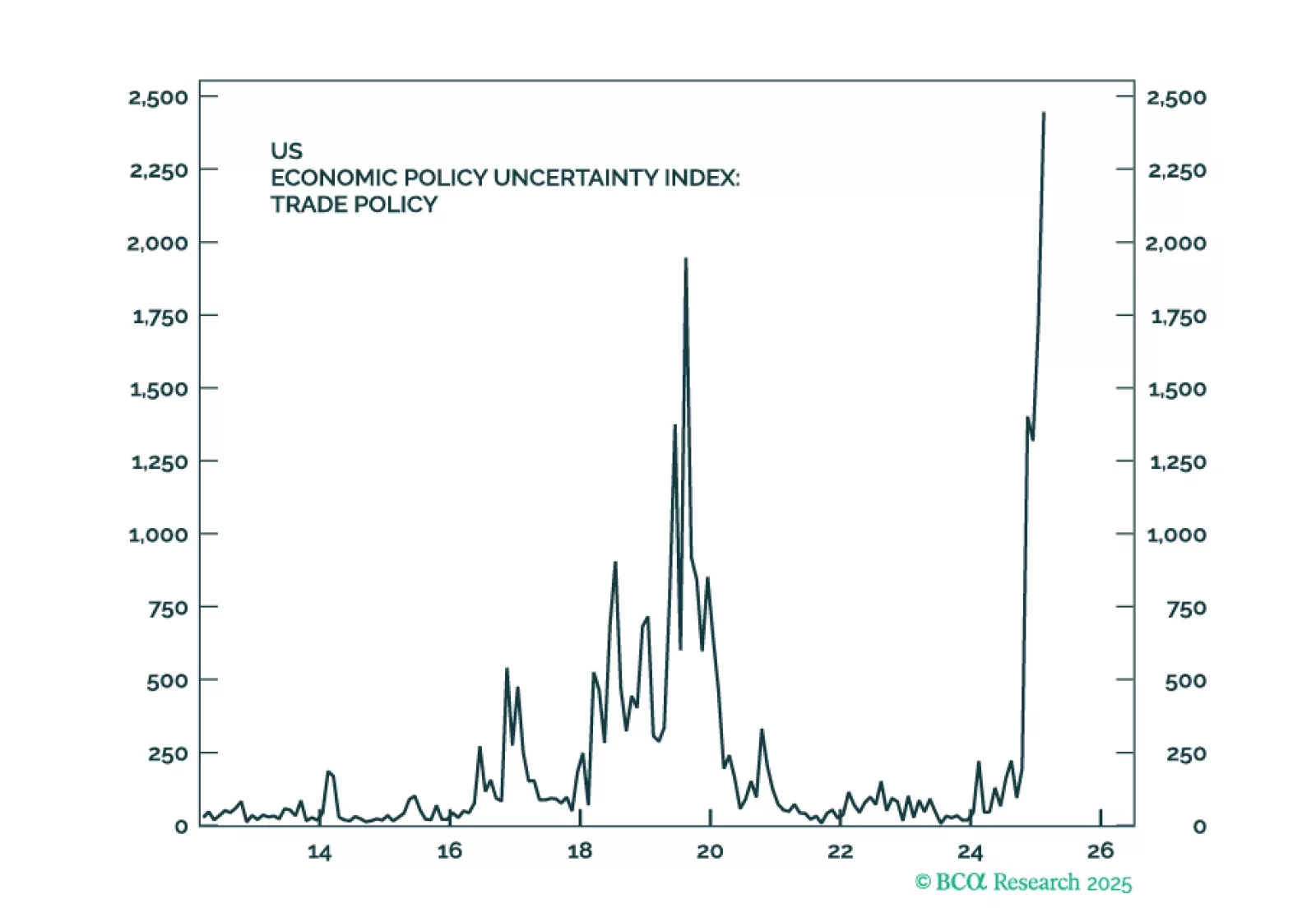

Although there may be a method to DOGE’s 100-mile-an-hour madness, we think the worries and uncertainty stoked by it and on-again, off-again tariff measures have increased the probability of a recession while bringing forward its start date. We are therefore tactically downgrading equities to underweight and upgrading fixed income and cash to overweight. Investors should pursue a defensive posture.

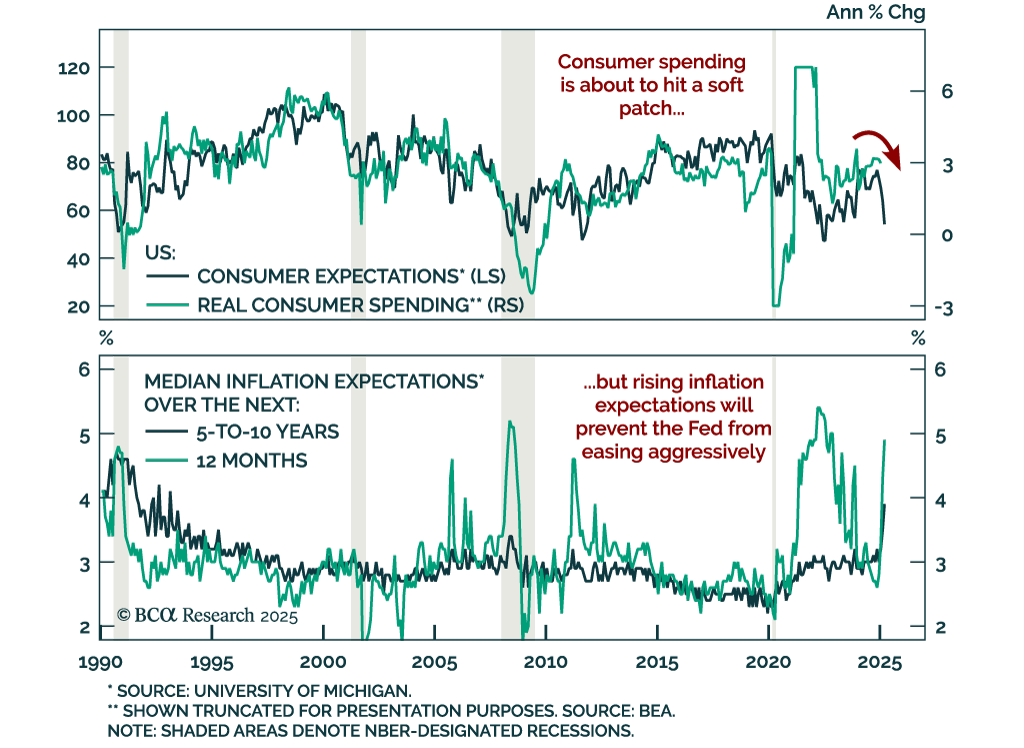

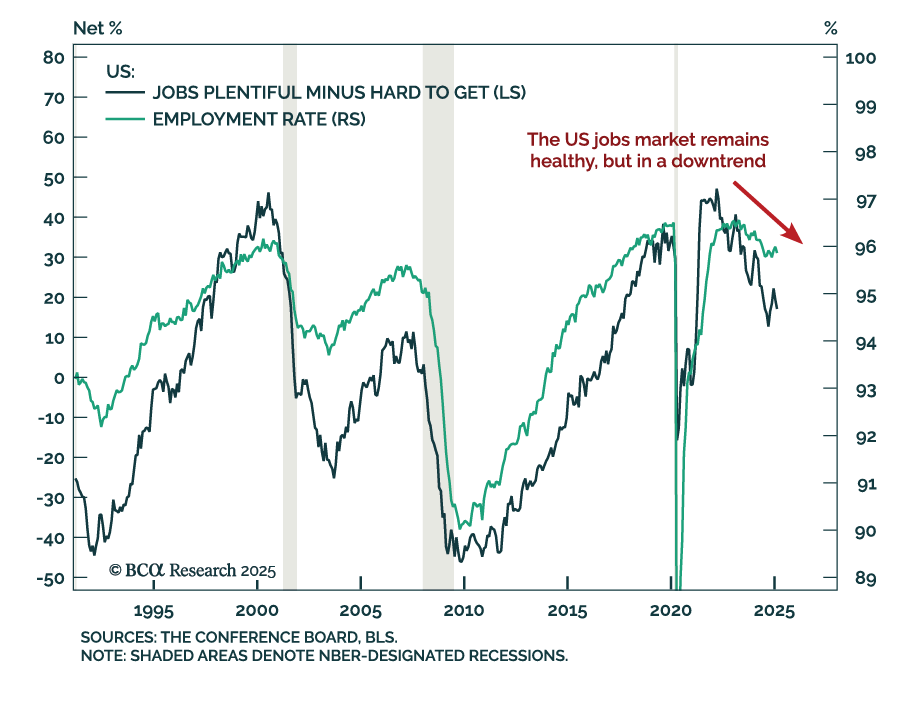

This morning’s employment report showed solid job growth, but recent consumer spending indicators are more concerning. The risk of recession starting within the next few months has increased. We suggest some important indicators for investors to track in the current environment.

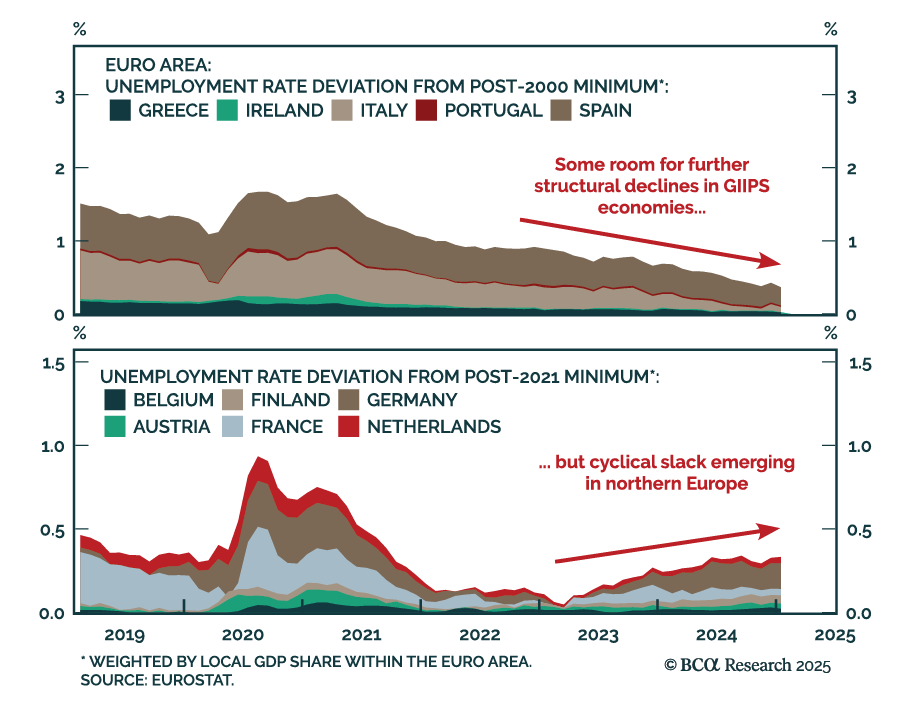

The US economy is set to enter a recession within the next few months. Stay underweight equities and overweight cash. Look to increase fixed-income duration exposure over the coming months. The euro is likely to strengthen and European stocks should outperform US stocks over the next month or so, but these trends will reverse by the middle of this year.