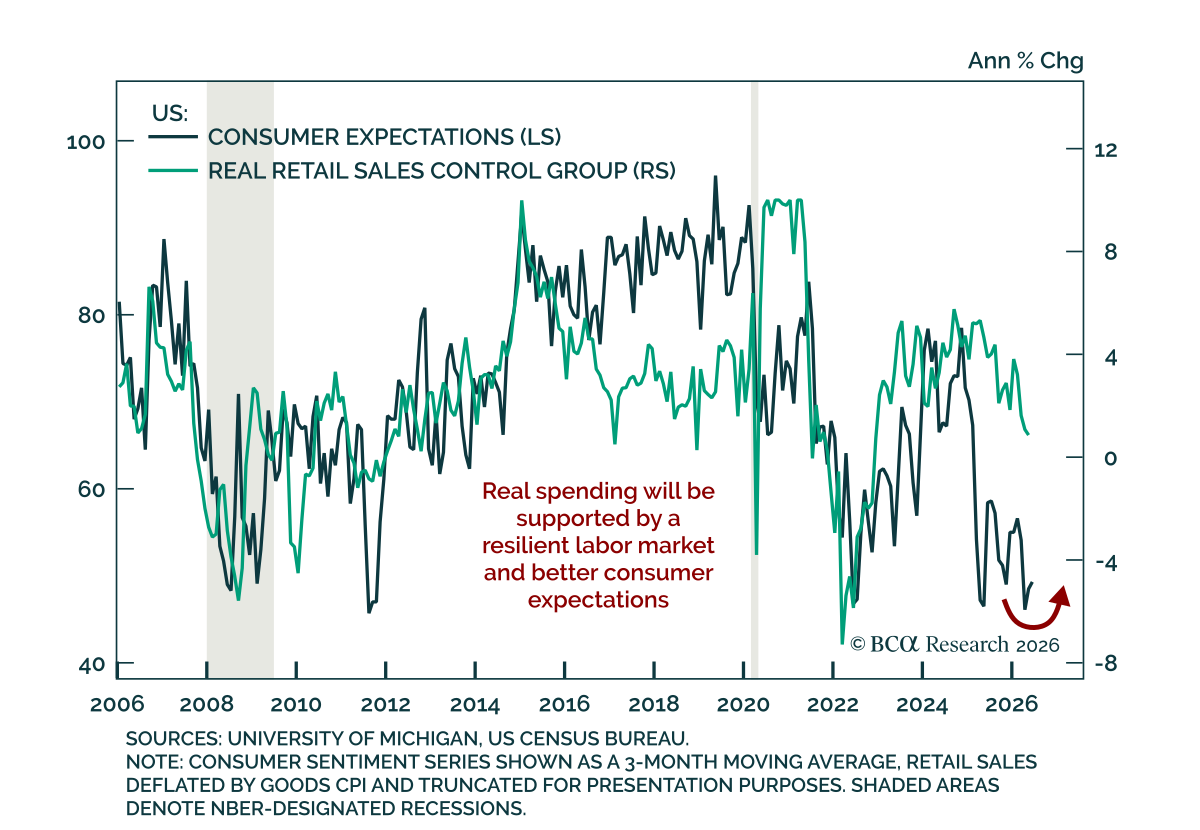

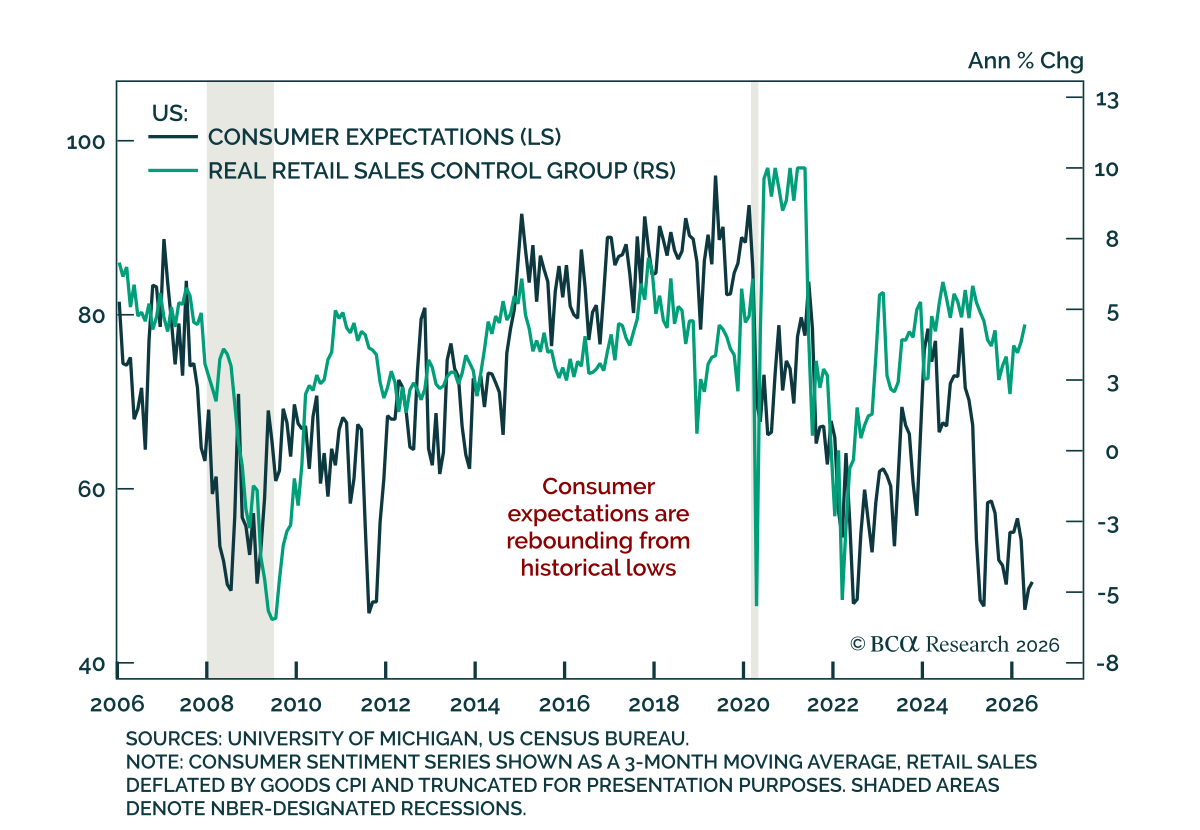

Consumer

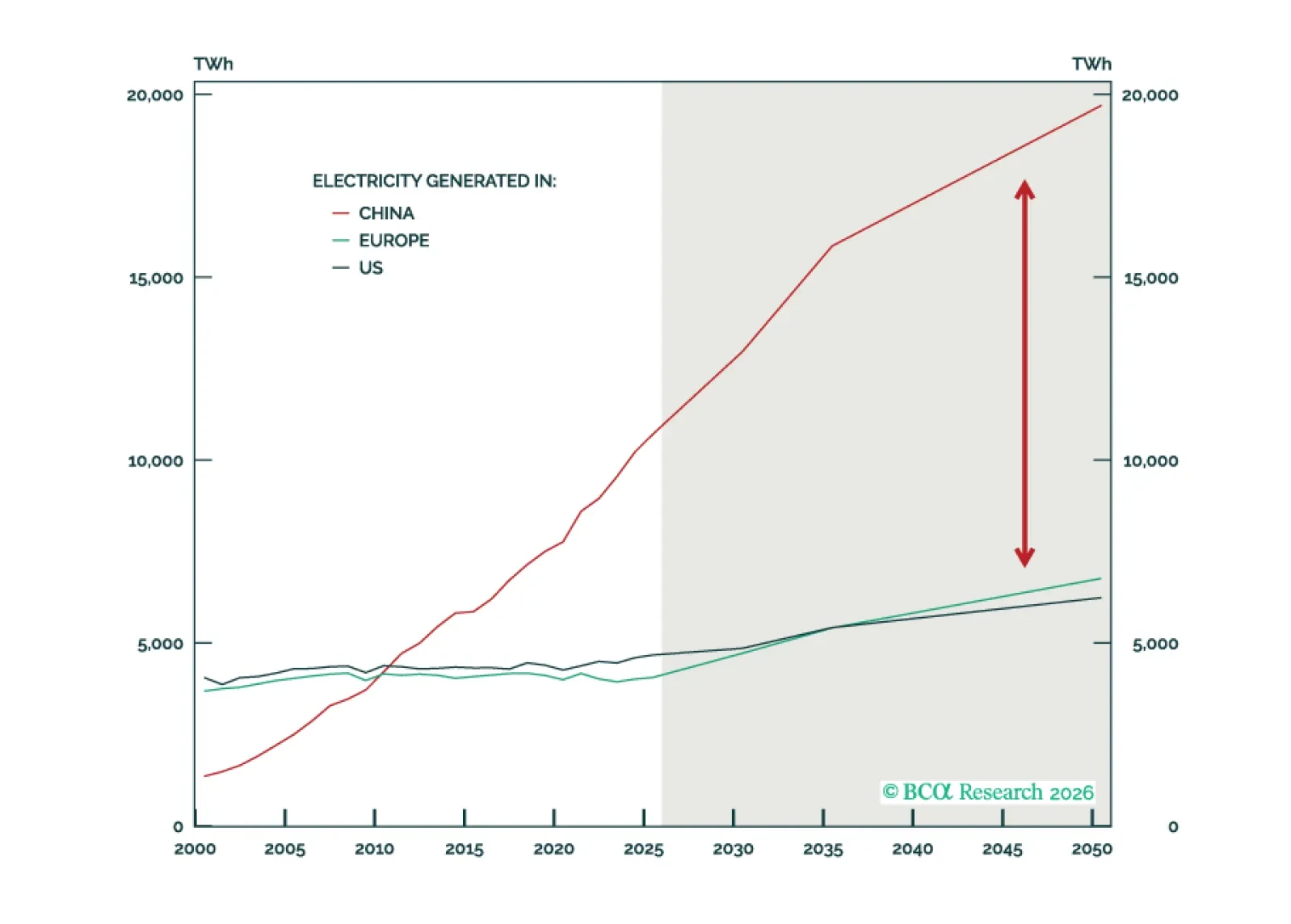

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

Section I maps how the broad distribution of wealth gains is supporting US consumption. Section II examines how countries can meet swelling electricity demand. The winners will find paths to build the infrastructure needed to power the high-tech future.

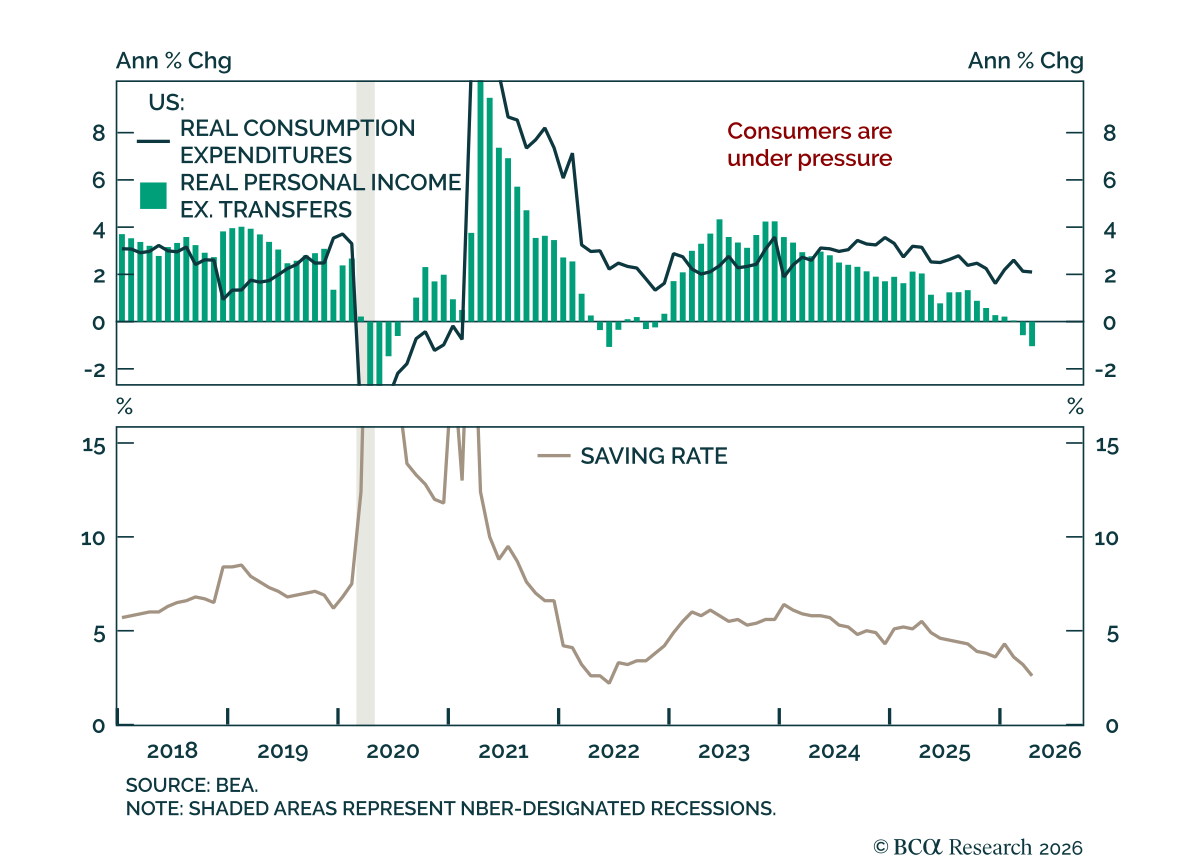

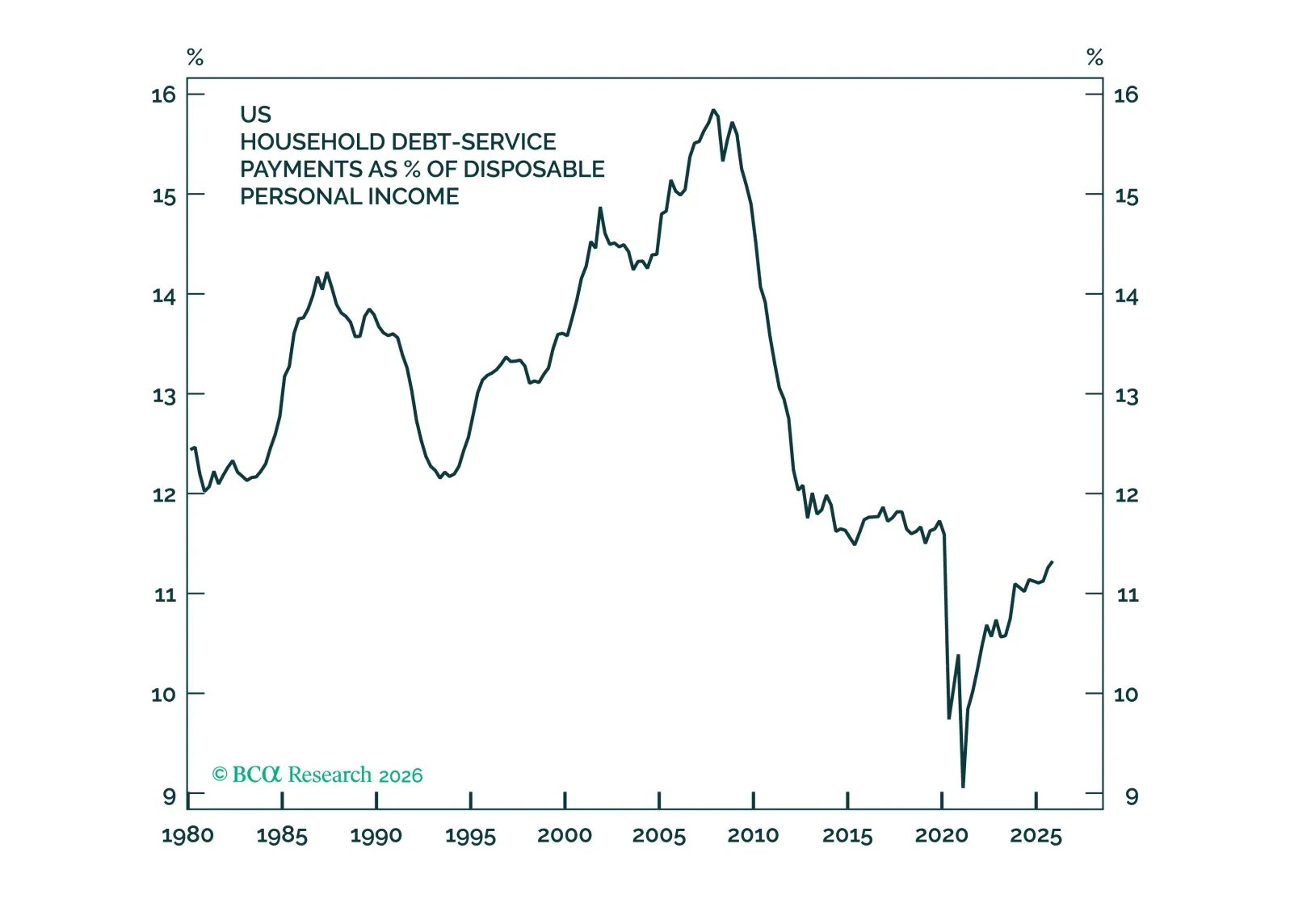

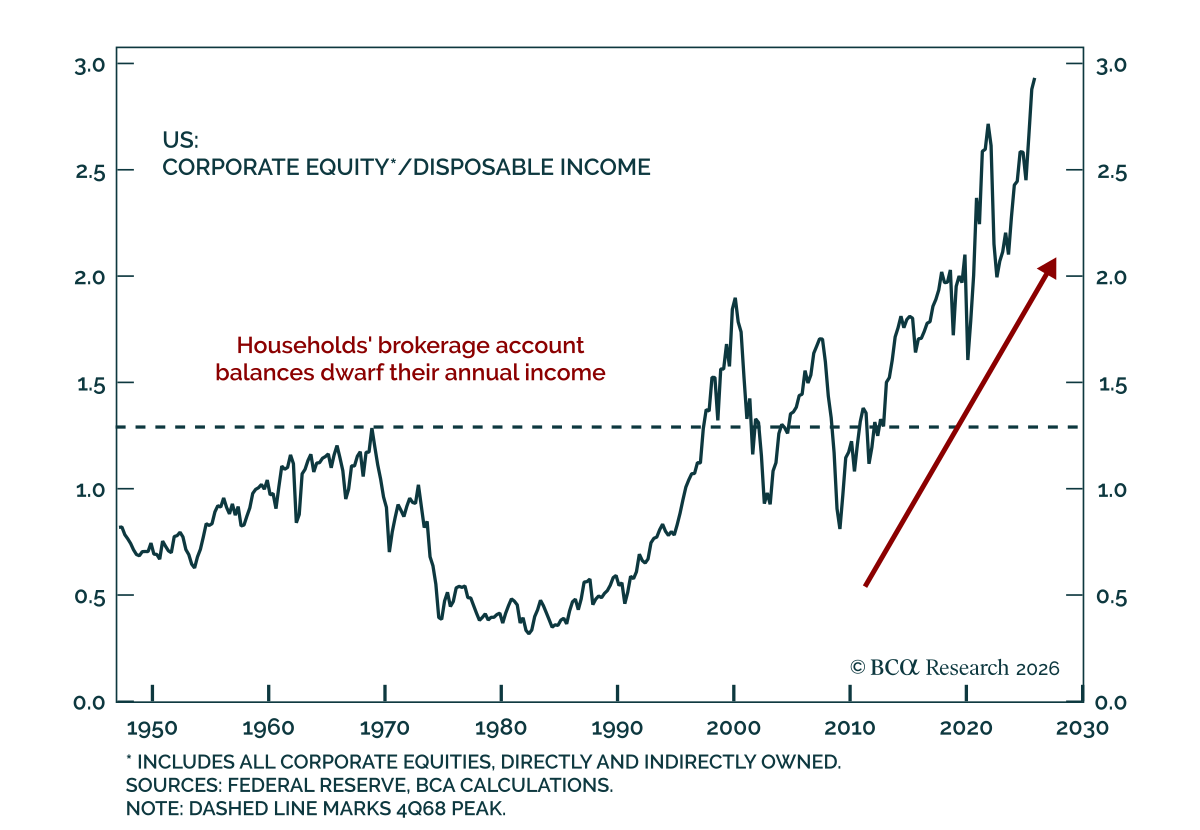

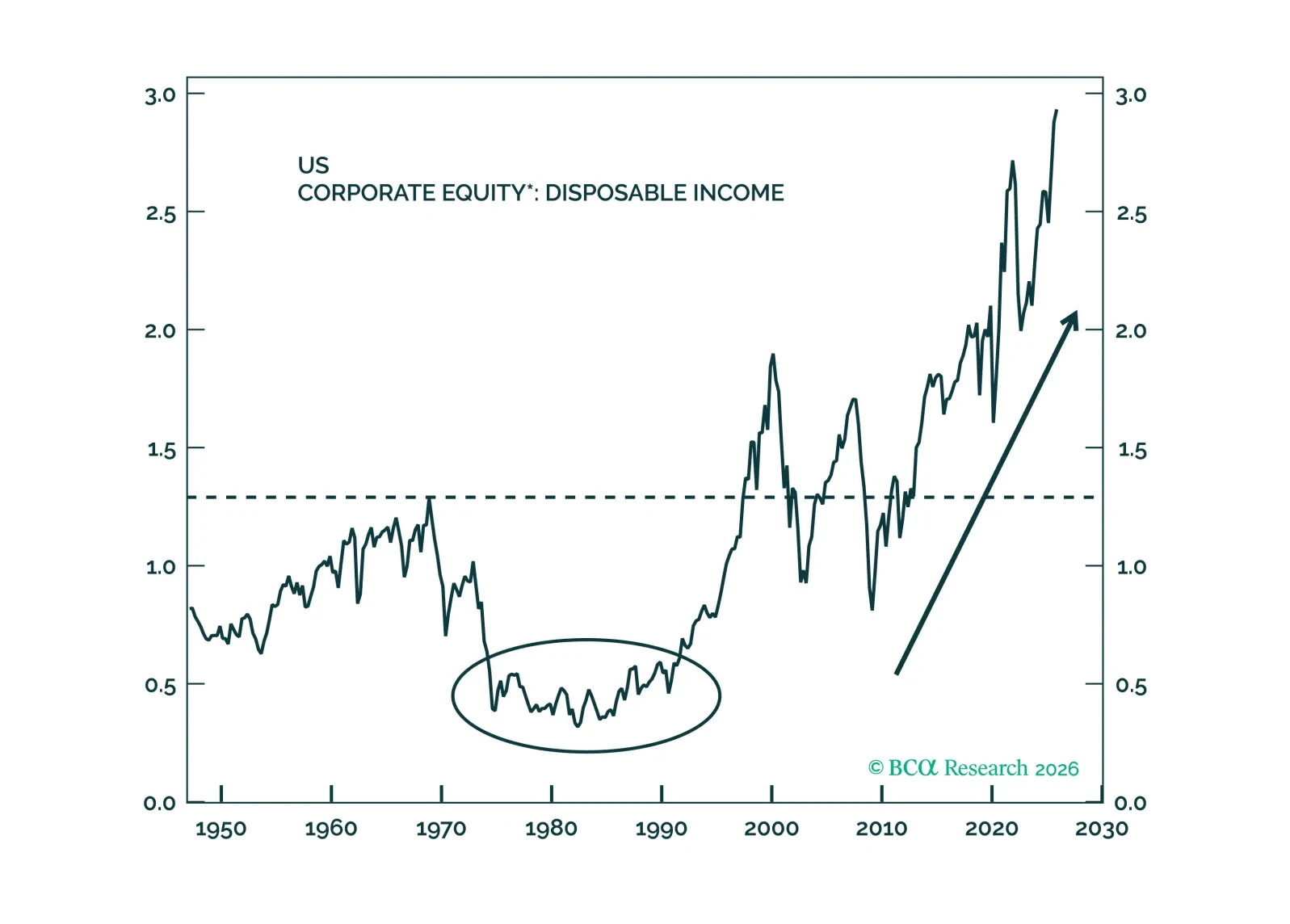

The most vulnerable households have whittled down their real debt balances while achieving significant real wealth gains. The combination has made consumption more resilient to income hiccups than in past cycles.

Although the multi-decade surge in the value of households’ equity holdings has made US activity more vulnerable to a stock selloff, the latest income, spending and employment data suggest that consumption growth can carry on at a 2% inflation-adjusted pace.

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

In Section I, Doug revisits the situation in the Strait of Hormuz and its implications for growth in Europe and the US. In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.