Economic Growth

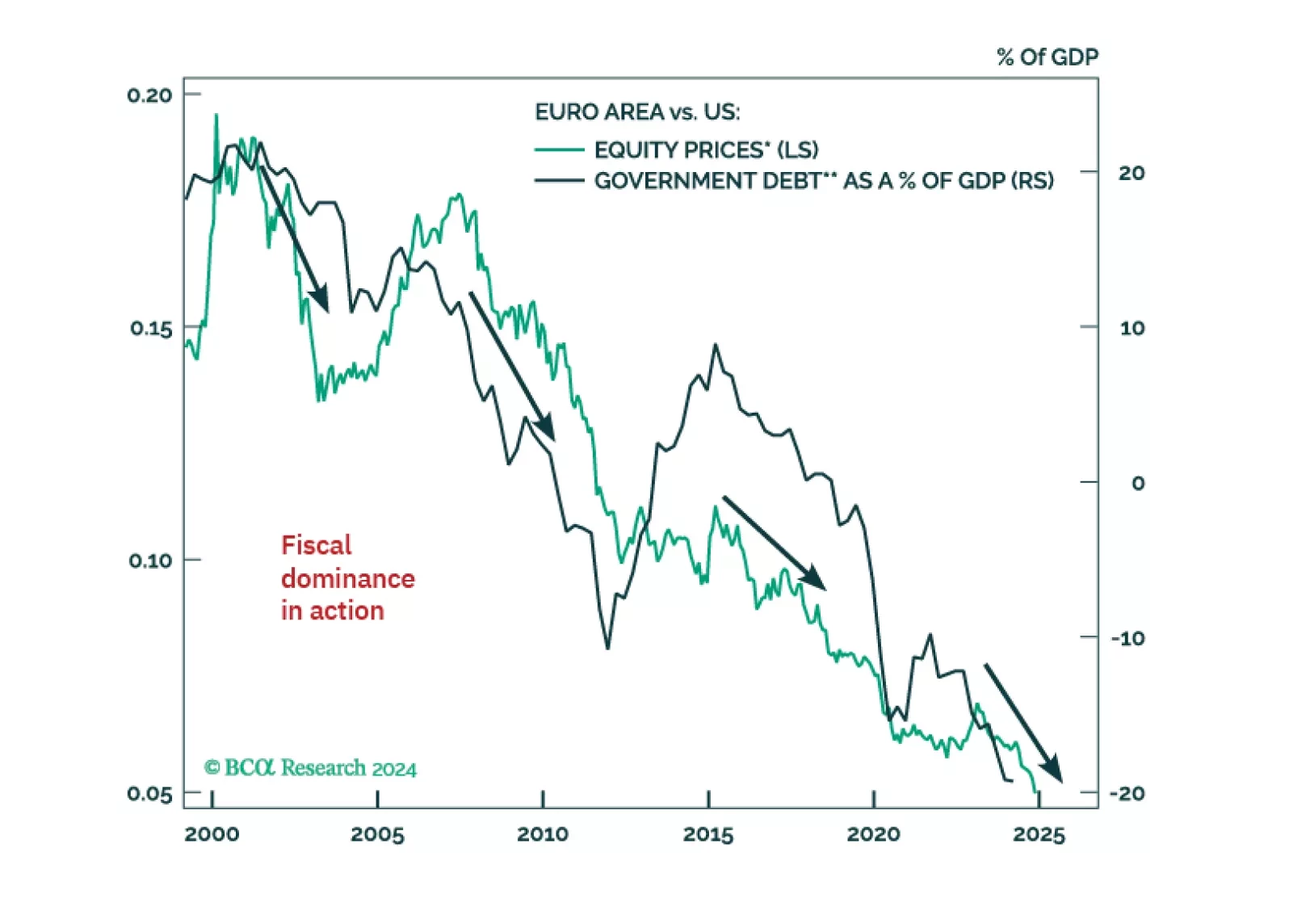

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

China’s November PMIs were mixed, and reflected very low growth. The official composite PMI was unchanged at 50.8, driven by a small uptick in manufacturing to 50.3 and a small downtick of services to 50. The Caixin manufacturing PMI jumped to 51.5 from…

The November ISM Manufacturing index beat expectations, increasing to 48.4 from 46.5 in October. The improvement was partly driven by the new orders component, which increased to 50.4 from 47.1. Price pressures moderated. The underlying details of…

The November Tokyo CPI beat expectations, with headline inflation accelerating to 2.6% y/y from 1.8%. The core (ex. fresh food) and “core core” (ex. fresh food and energy) measures also reaccelerated to 2.2% and 1.9%, respectively. The Tokyo CPI provides…

Our 2025 Outlook was just published. We revisit this year’s calls and discuss what we think is ahead for the global economy and markets for the next 12 months and beyond. The recent US election has significantly shifted our economic and market outlook. A…

President-elect Trump jolted markets Monday night by declaring that tariffs will be implemented on imports from Mexico, Canada, and China. The US dollar strengthened while stocks fell, as did Treasury yields. Equities, however, recovered on Tuesday, as a…

The November Ifo Business Climate index for Germany missed expectations, falling to 85.7 from 86.5 in October. Both subcomponents decreased, with the Current Assessment sliding 1.4 points to 84.3 and Expectations essentially flat at 87.2. The data confirm…

Canadian inflation was slightly hotter than expected in October, re-accelerating to 2.0% y/y from 1.6% in September. The BoC’s favored core measures, median and trim, re-accelerated to 2.5% and 2.6% respectively, and CPI-common rebounded to 2.2%. CPI…

Chinese activity indicators showed resilience in October, with retail sales jumping from 3.2% to 4.8% y/y. Industrial production growth was roughly unchanged at 5.3% y/y. New and used home prices keep falling, albeit at a slower pace. We would fade this…