US Election

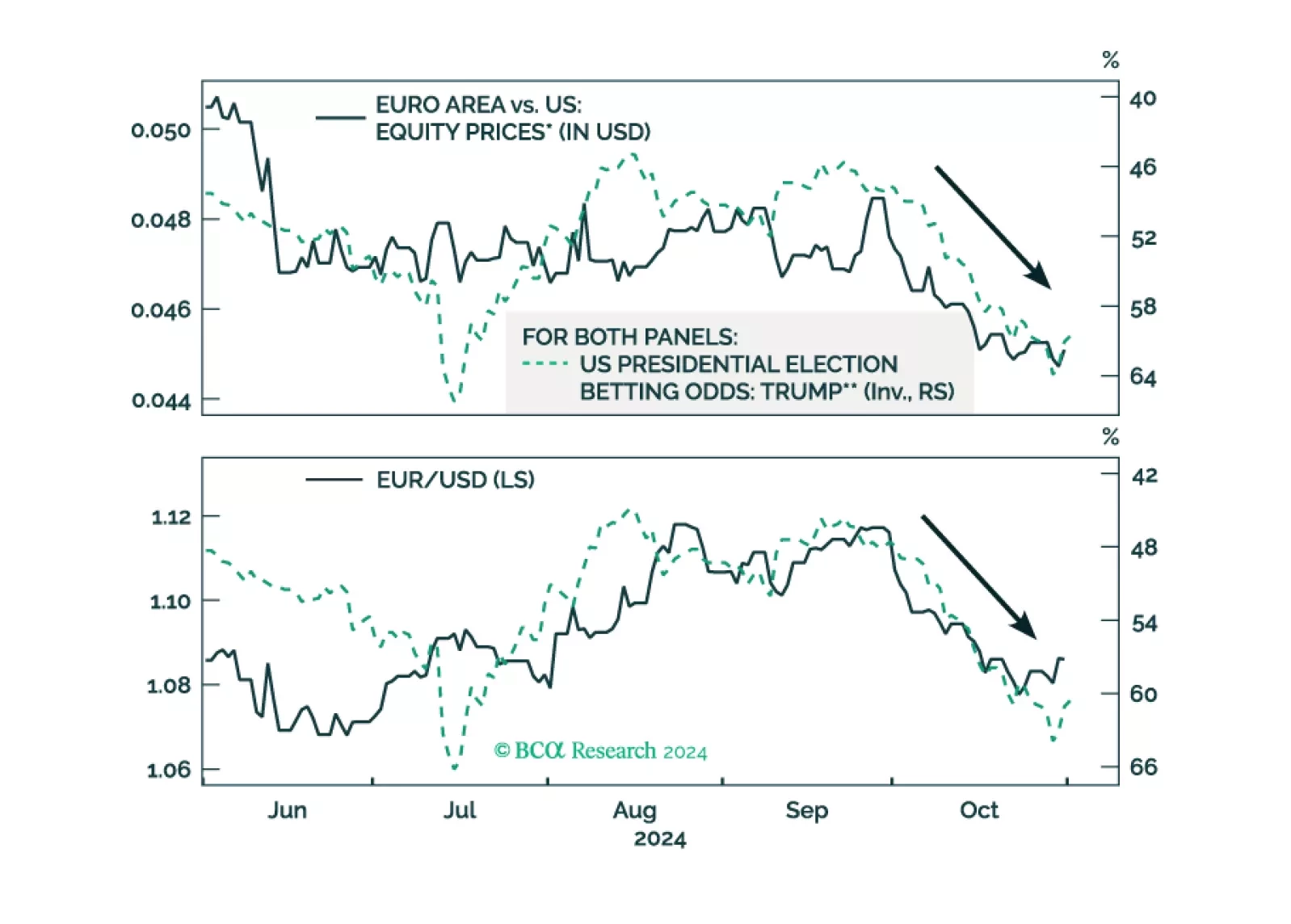

As the odds of a Trump victory rise, European assets underperform US ones. What would be the immediate impact of a Trump victory on European stocks?

EM credit markets have recently defied the selloffs in EM equities, currencies, local currency bonds, and commodity prices. Such a decoupling is unusual. Resilient US growth and Fed easing are not sufficient to justify very low EM credit spreads.

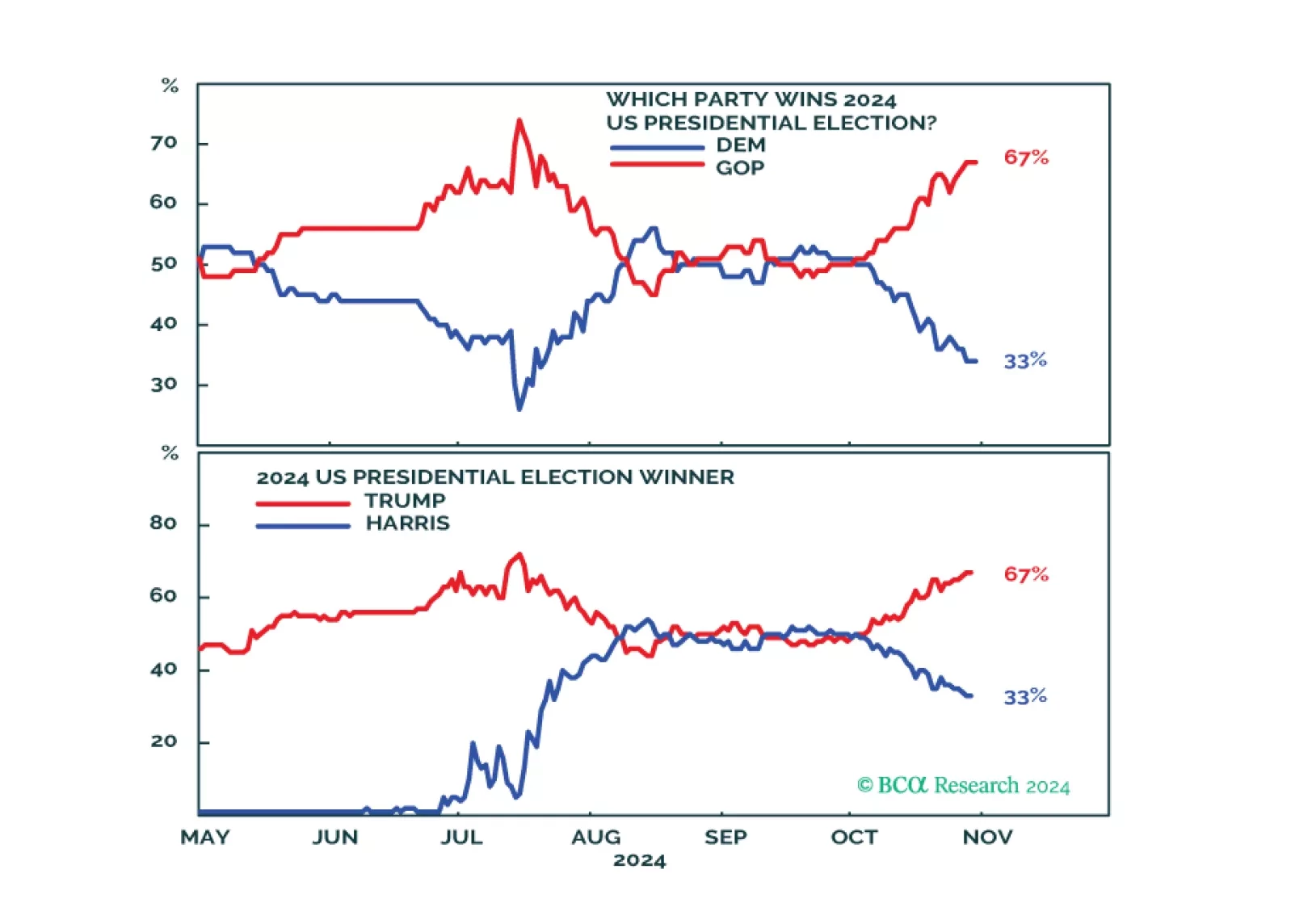

Trump may be favored, but Harris is now underrated. The Senate is highly likely to go Republican – Harris would be gridlocked if she pulled off a victory. If Trump wins it will be a full sweep. Expect volatility in the short term.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

Trump may be slightly favored for the White House but the US election is still extremely close. Odds of a contested or contingent election are rising, which should cause stock market volatility. A Republican sweep should cause more volatility. Democratic gridlock is next most likely but benign for stocks in the short run.

A Donald Trump victory would send bond yields higher during the next few weeks, but yields will fall in 2025 no matter the election outcome.

As the odds of a Trump victory increase, there are indications that the “Trump trade” has commenced in global financial markets, with negative short-term implications for EM. In short, the US dollar will strengthen, and US bond yields will rise in the lead-up to and after the election if Trump wins. In response, EM countries’ currencies will depreciate, and their fixed-income and equity markets will suffer over the coming months.

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.