US Midterm Election Dashboard

Real-time charts on US midterm elections: house models, macro and political fundamentals, and US political capital

Models

Our election models are based on economic and polling fundamentals. Because these variables are merely snapshots of the current political and economic environment, they must be supplemented with our outlook for the economy and the domestic and global political landscape. Therefore, the models should be used as a starting point for forecasting the midterms.

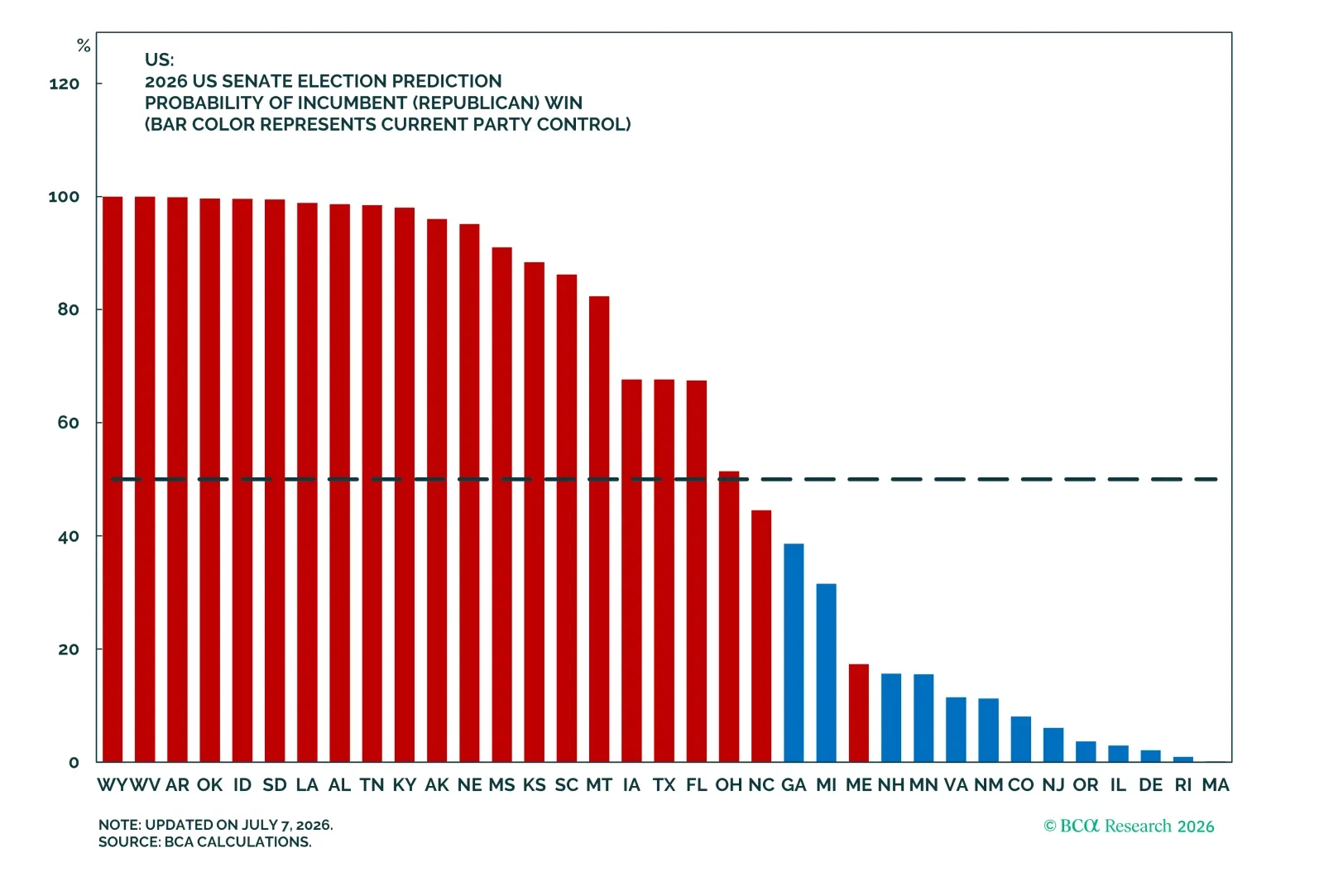

Our model predicts a narrow win for the Republicans with a 51-49 majority in the Senate, but we are skeptical.

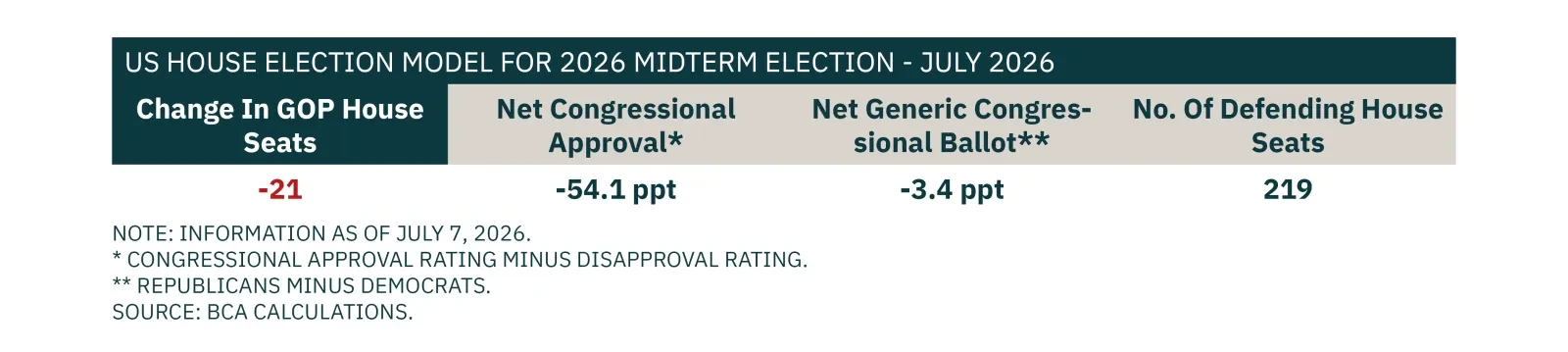

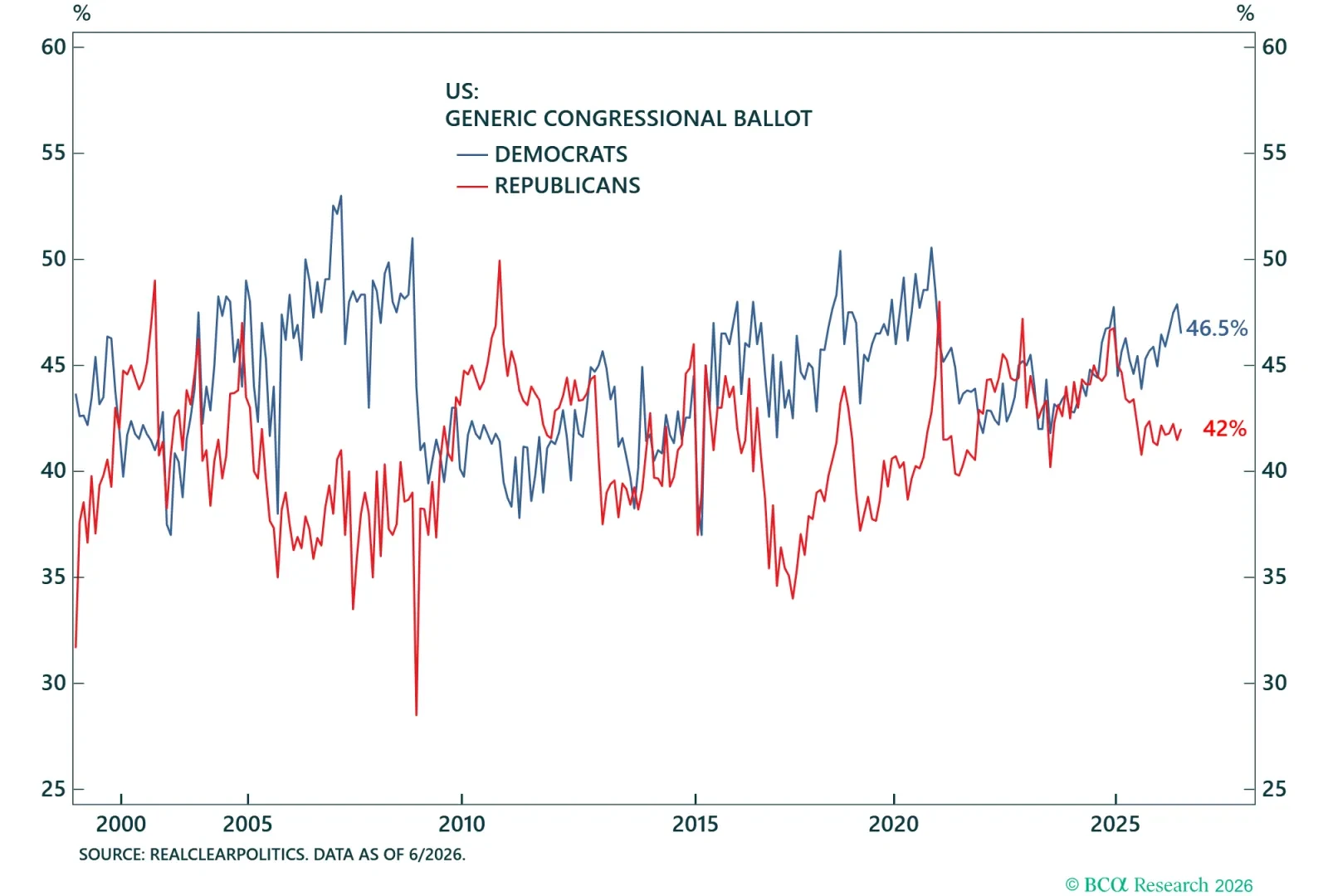

House Election Model Points To Democratic House Majority.

Historical Precedents

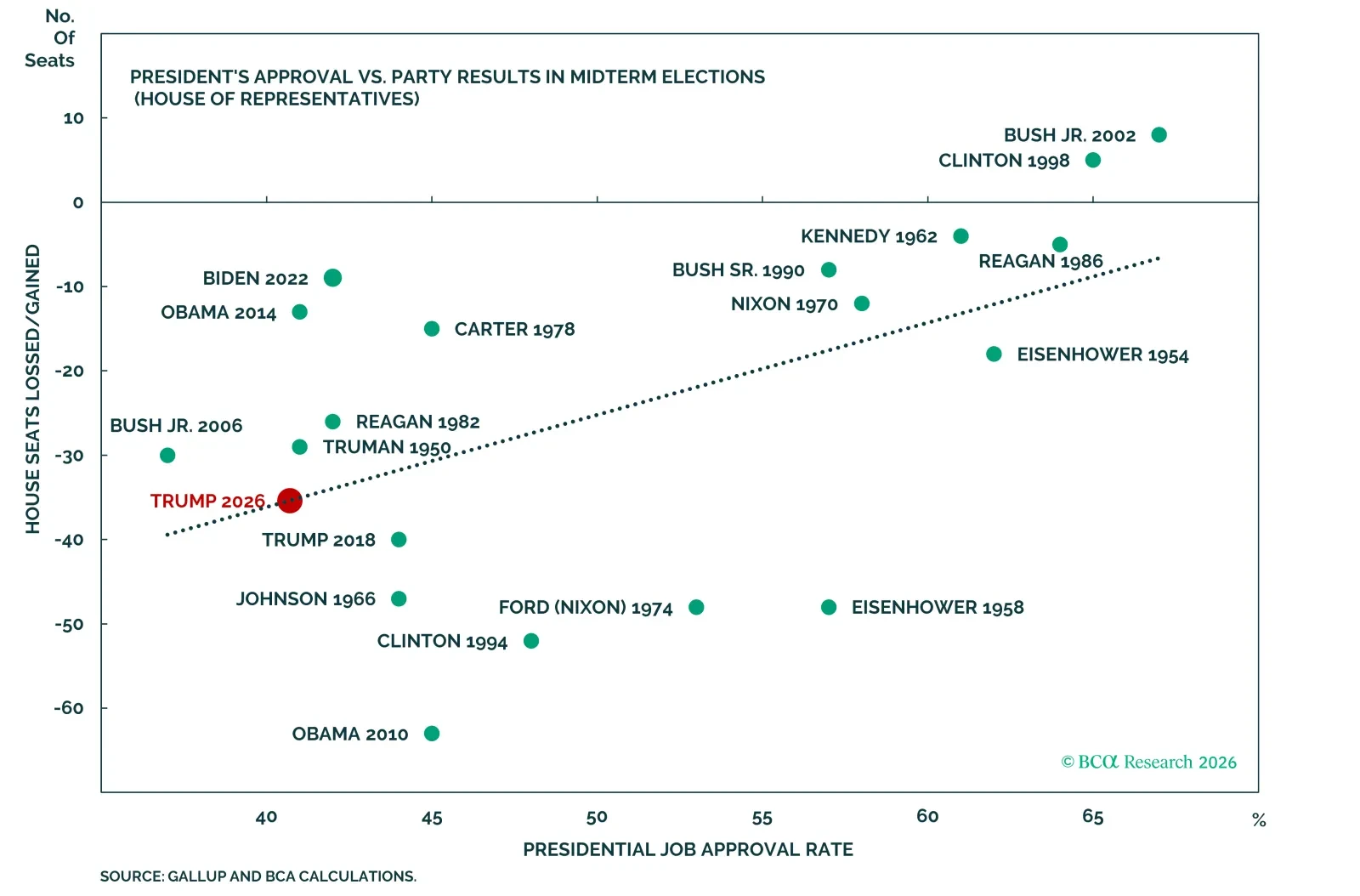

Historically, the president's party has tended to lose seats in both the House of Representatives and the Senate during midterm elections.

Unpopular presidents tend to lose more seats in the Senate during midterm elections.

Unpopular presidents tend to lose more seats in the House of Representatives during midterm elections.

Polling/Probabilities

The president's popularity is a key determinant of midterm outcomes because it influences support for his party. An unpopular president typically reduces his party's electoral prospects.

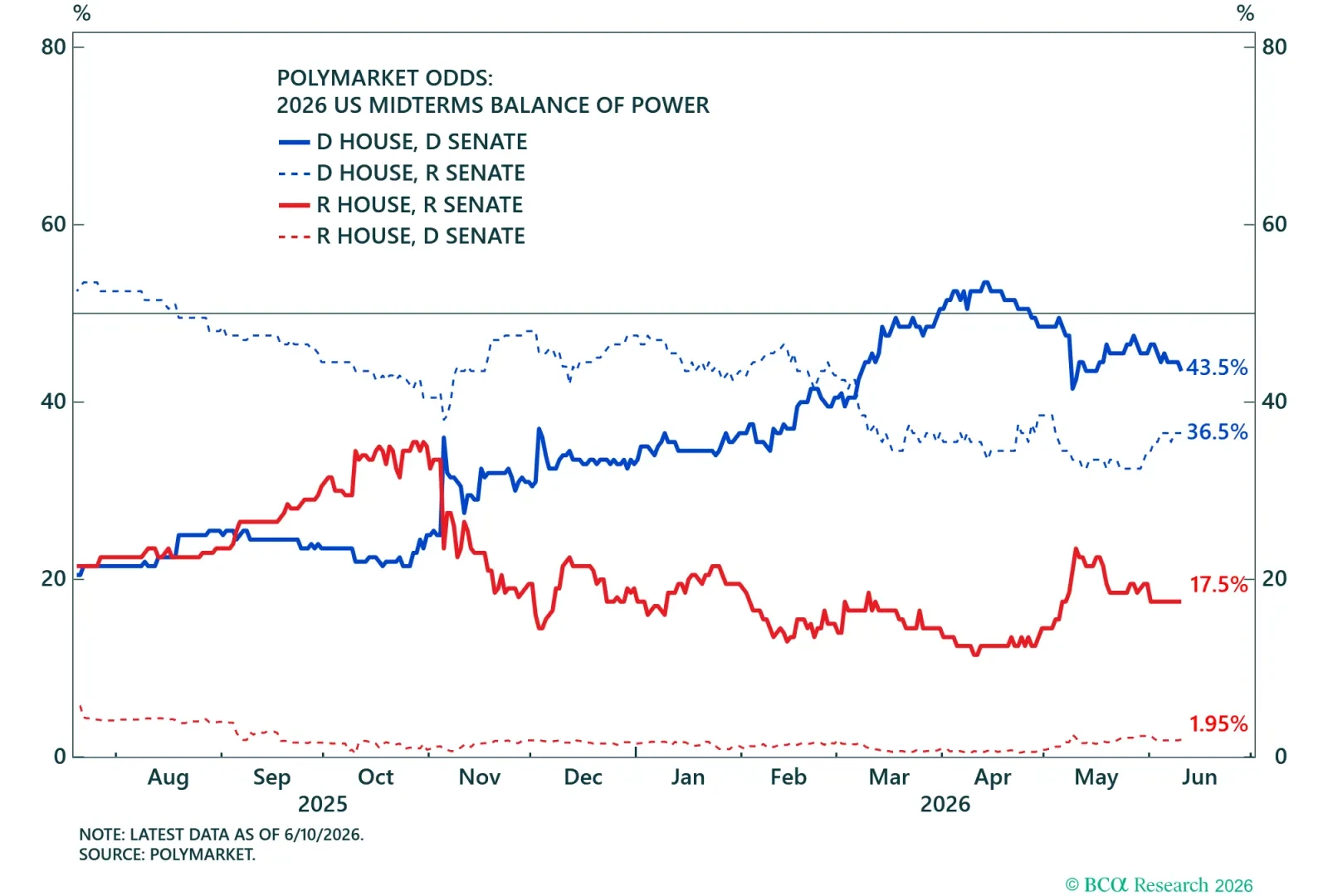

Aggregate level betting market odds on the midterm election.

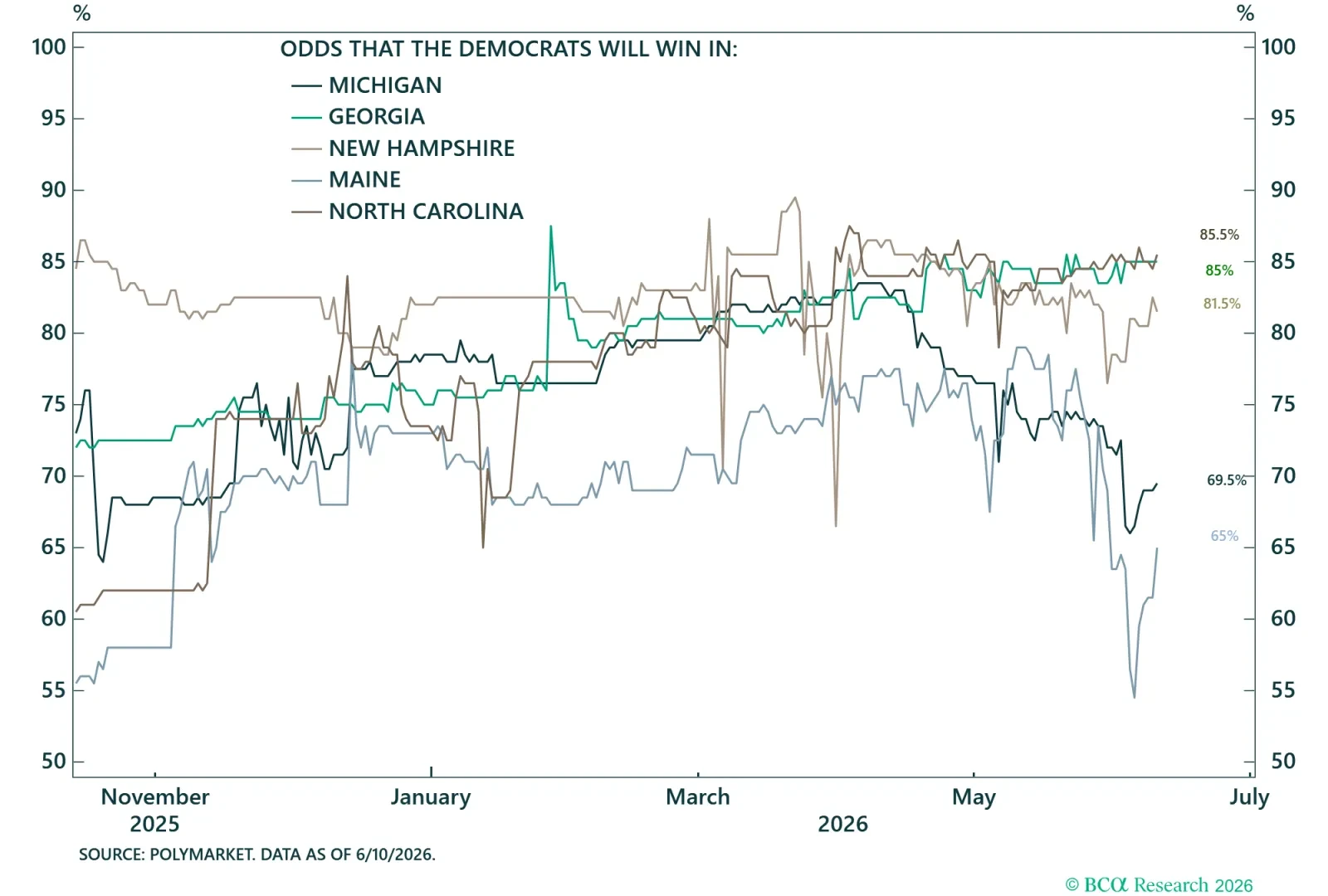

States that Democrats are likely to win.

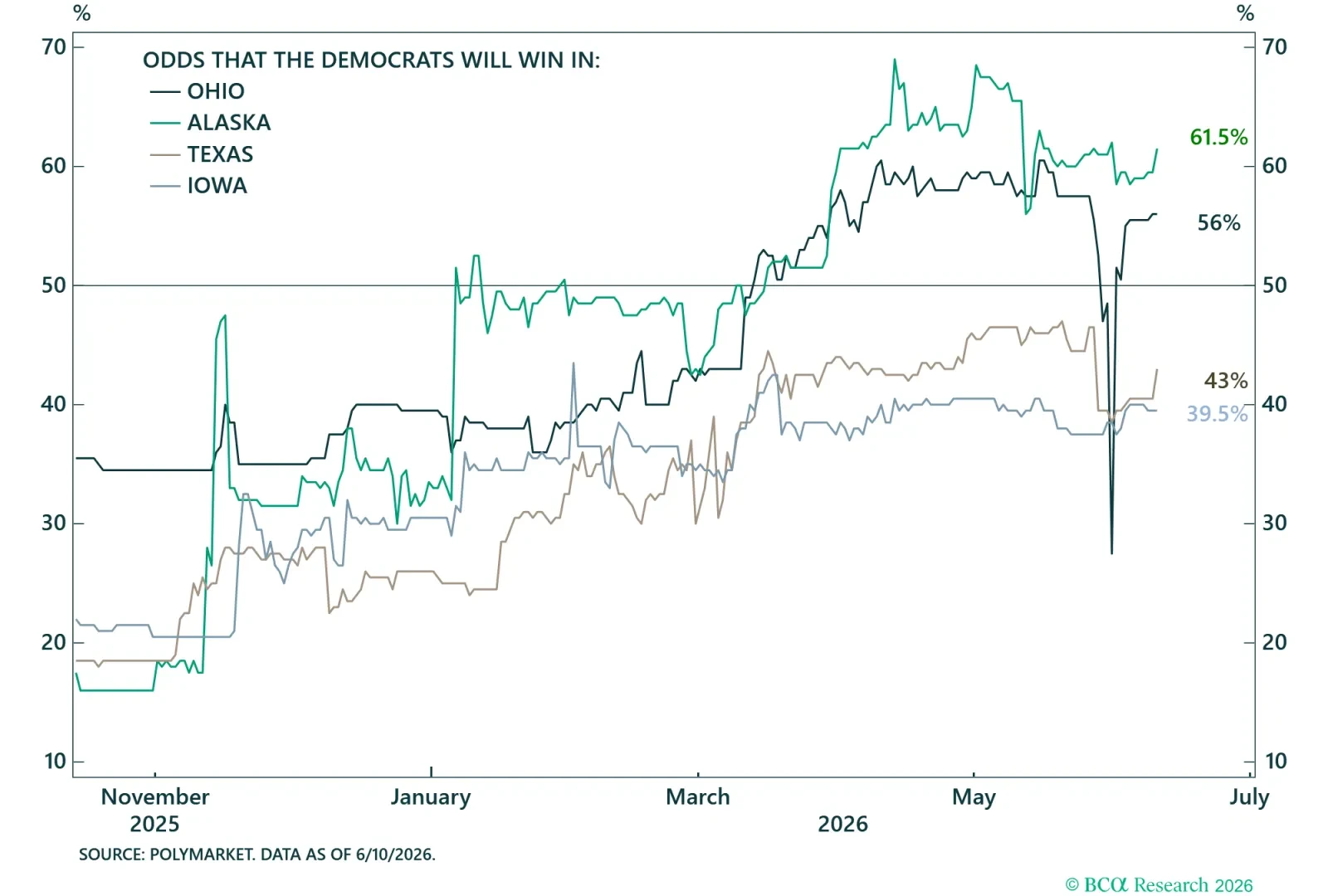

States that Democrats are marginally likely to win.

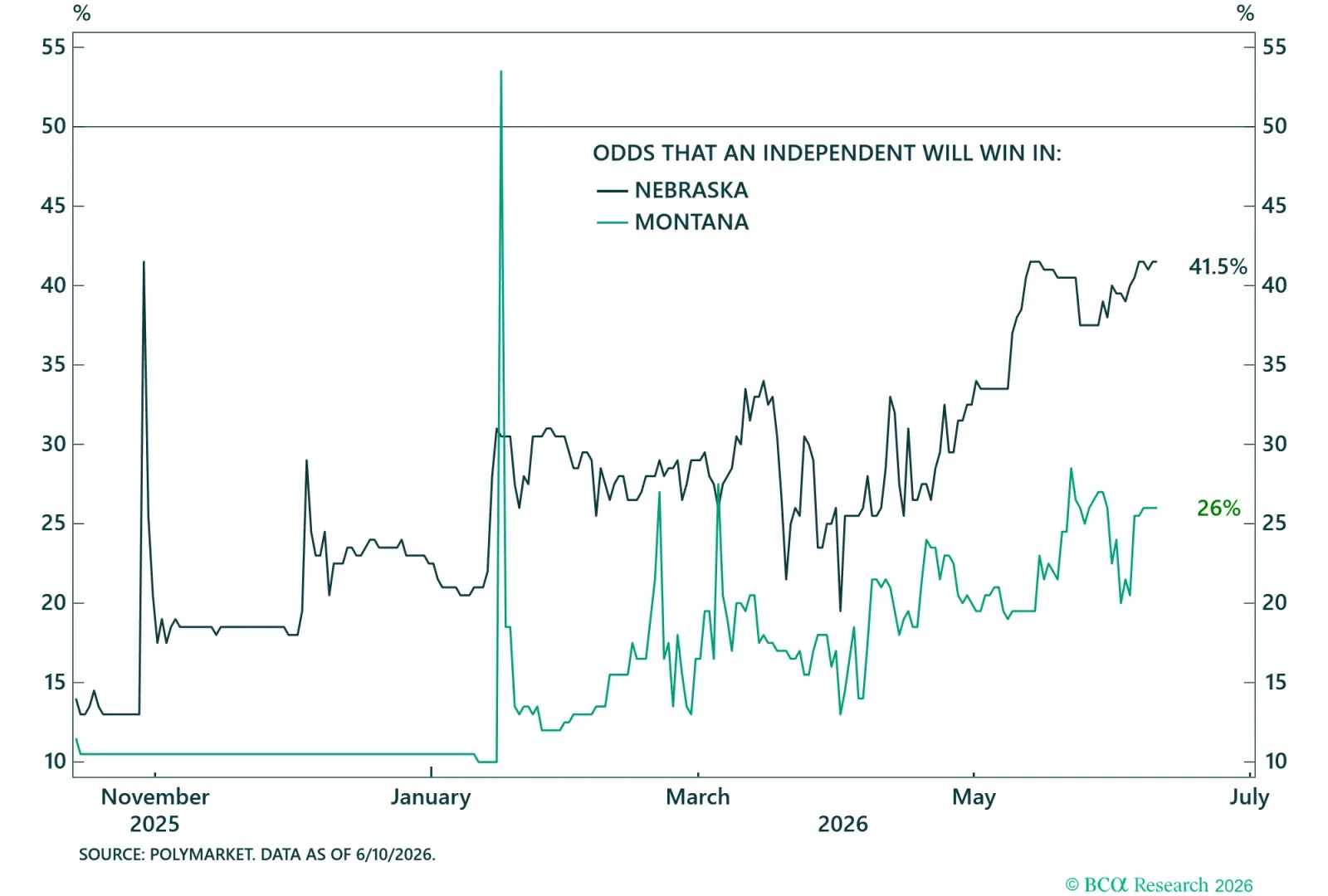

States where independent candidates are somewhat likely to win.

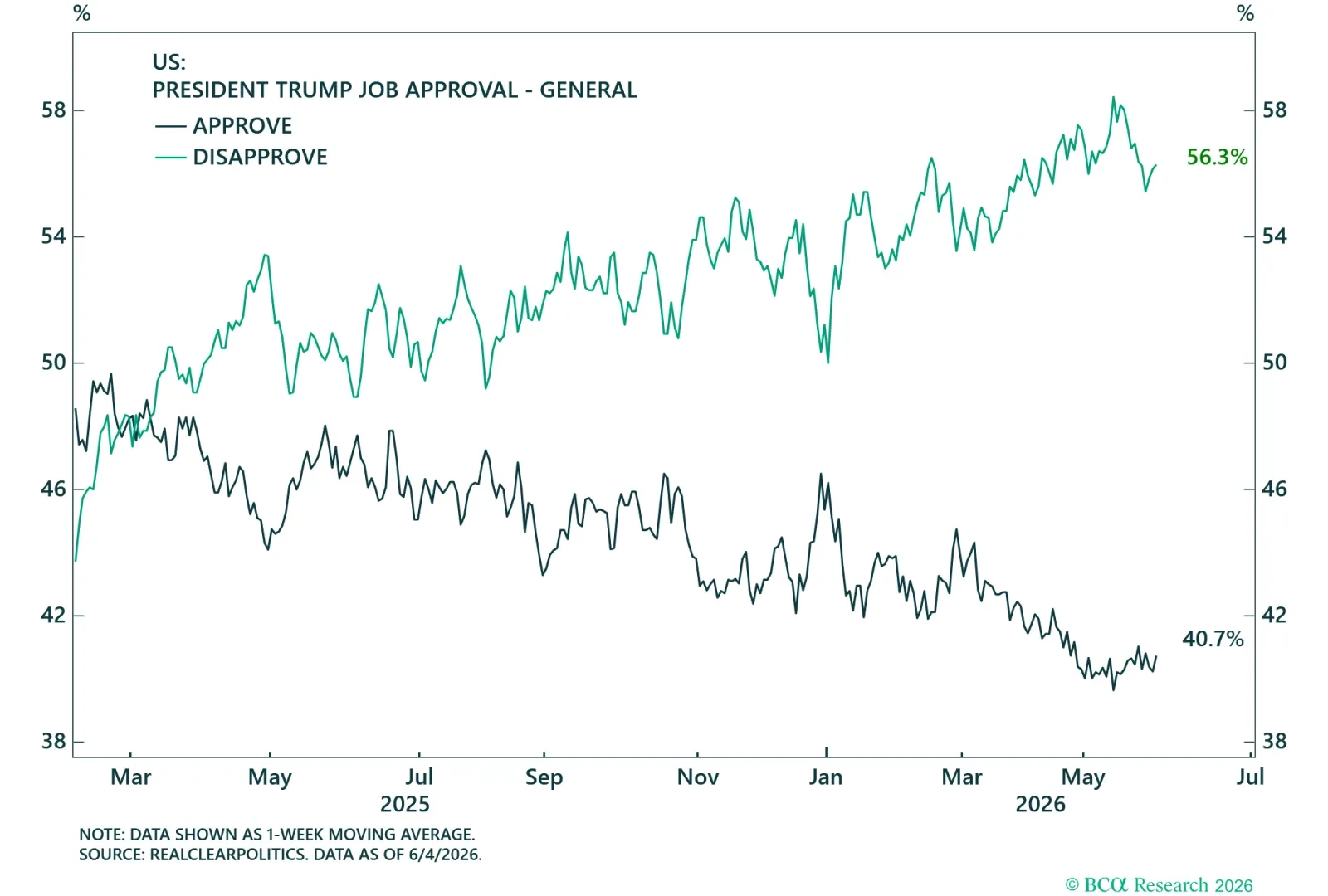

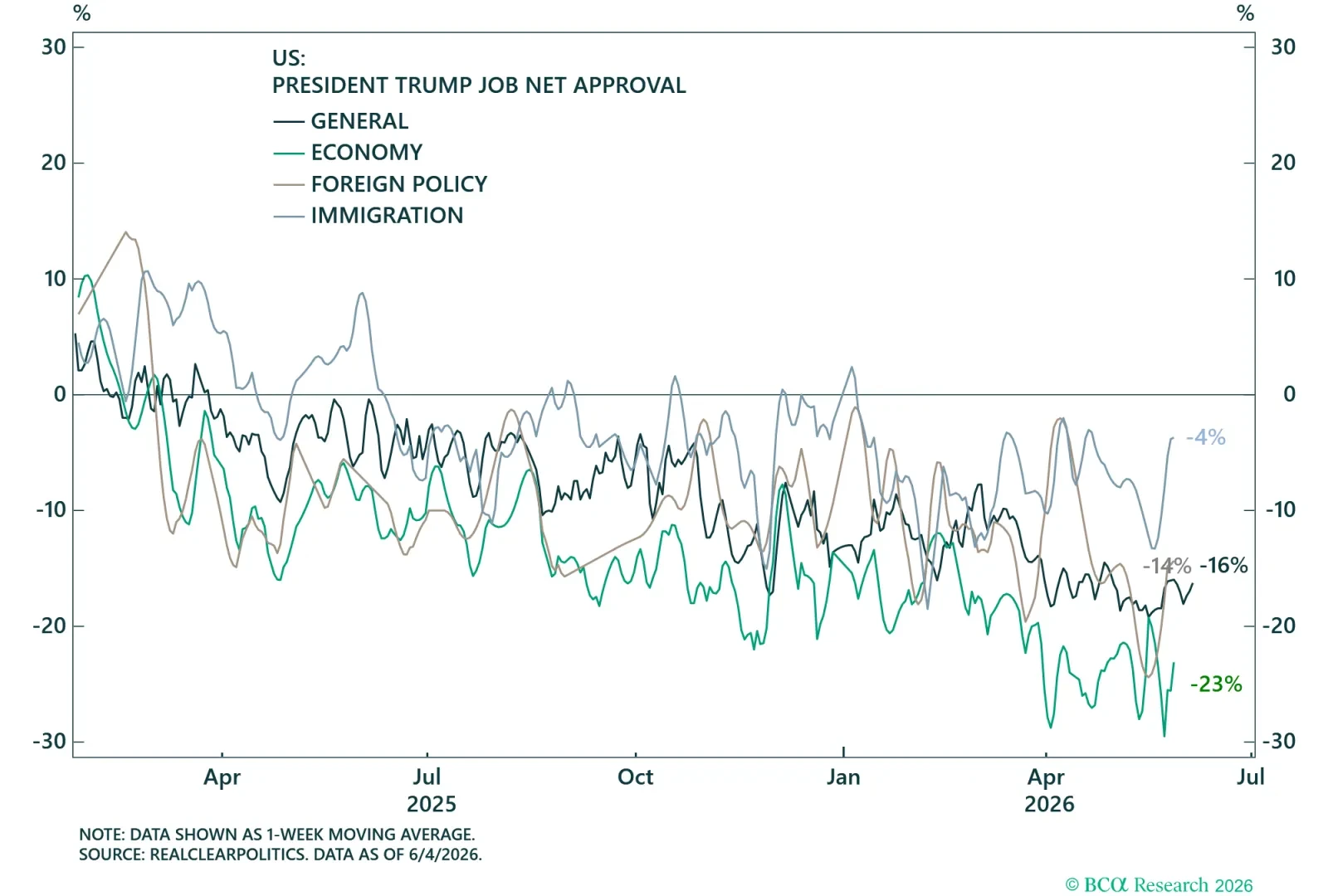

The president is not on the ballot, but his popularity will affect his party’s performance in the midterm.

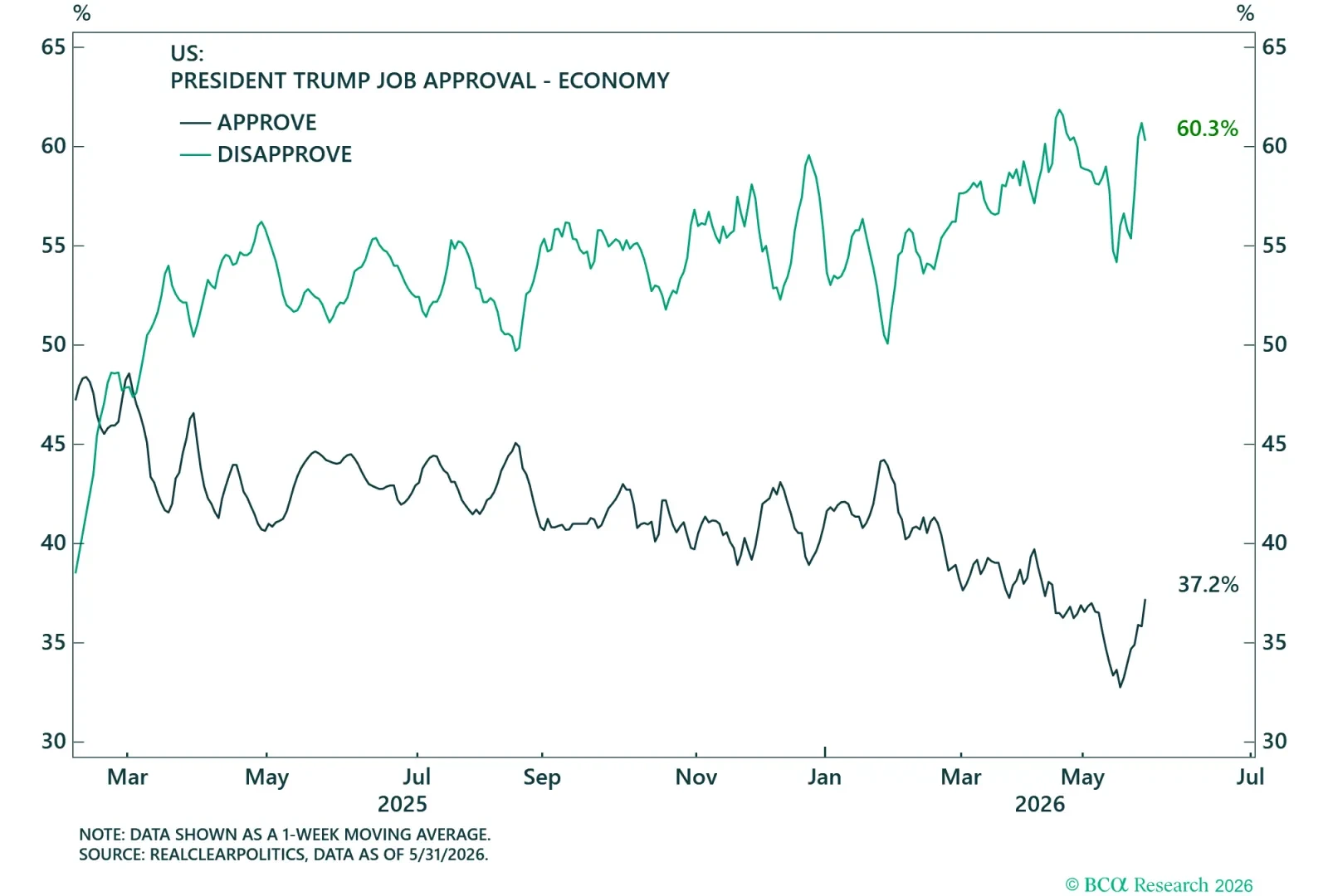

The president was elected on the premise of strengthening the economy.

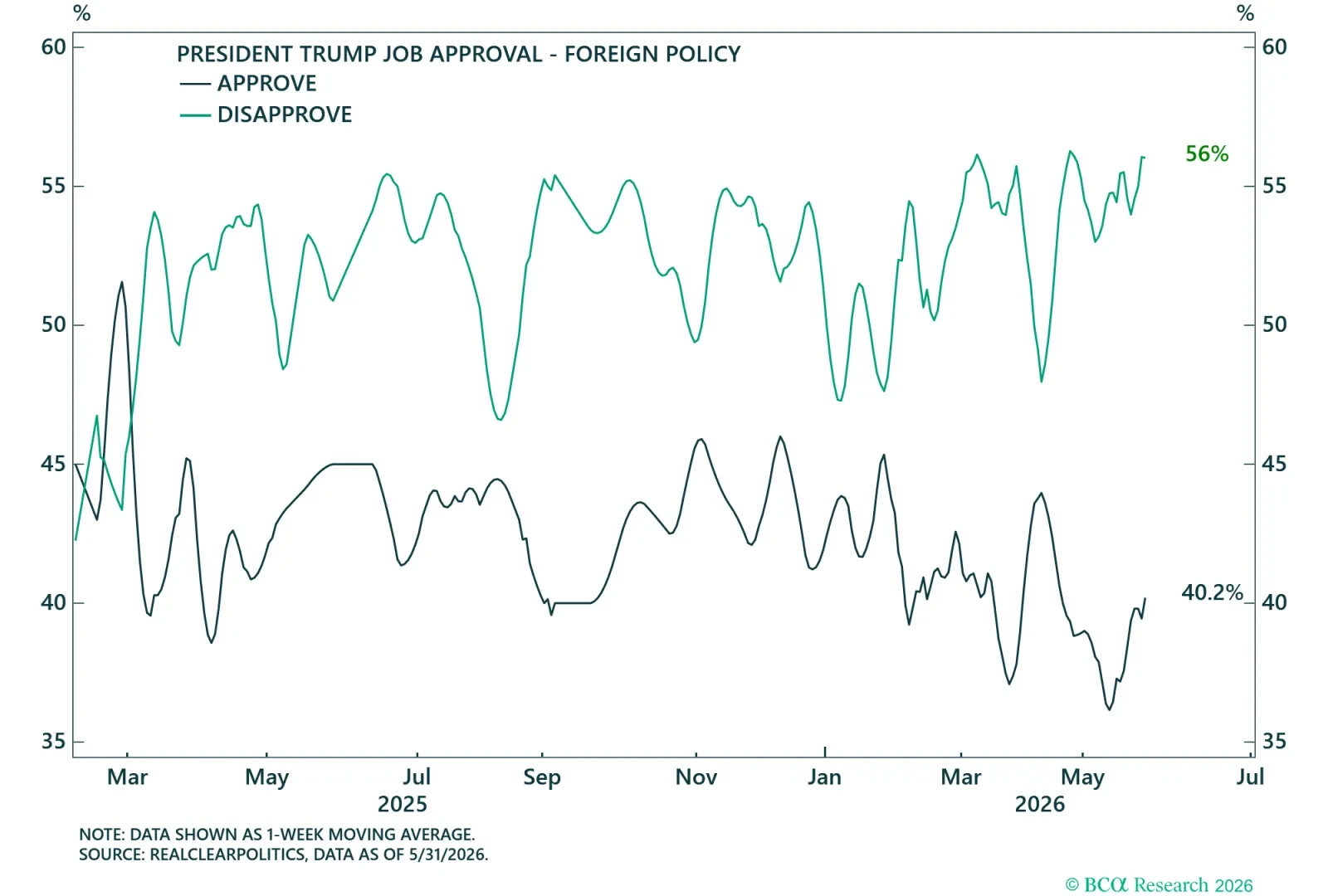

The president was elected on the premise of putting America first.

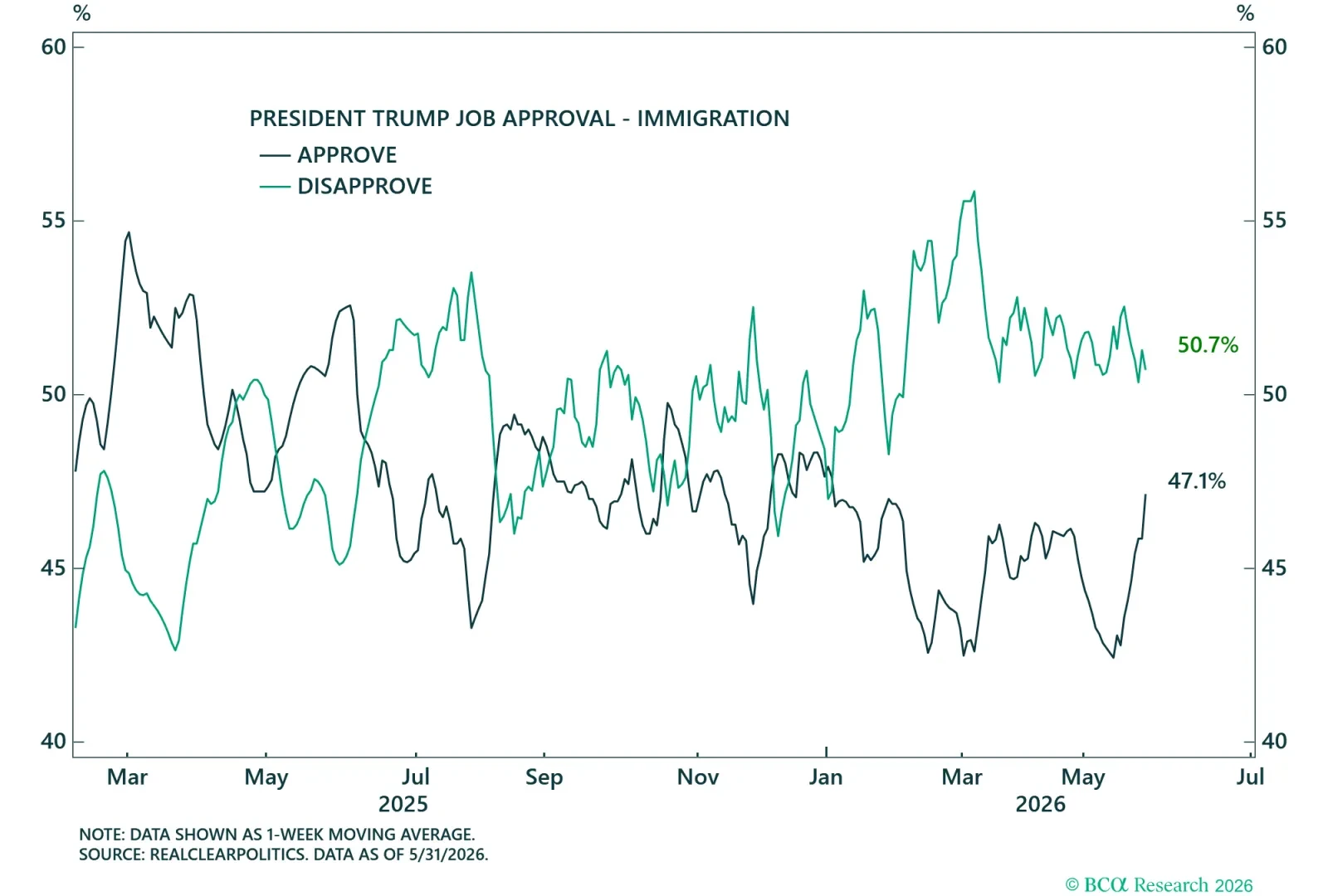

The president was elected on the premise of strengthening the border.

More voters disapprove of the president than approve across all major policies, and the trend is negative.

Generic polls on which party is favored in Congress.

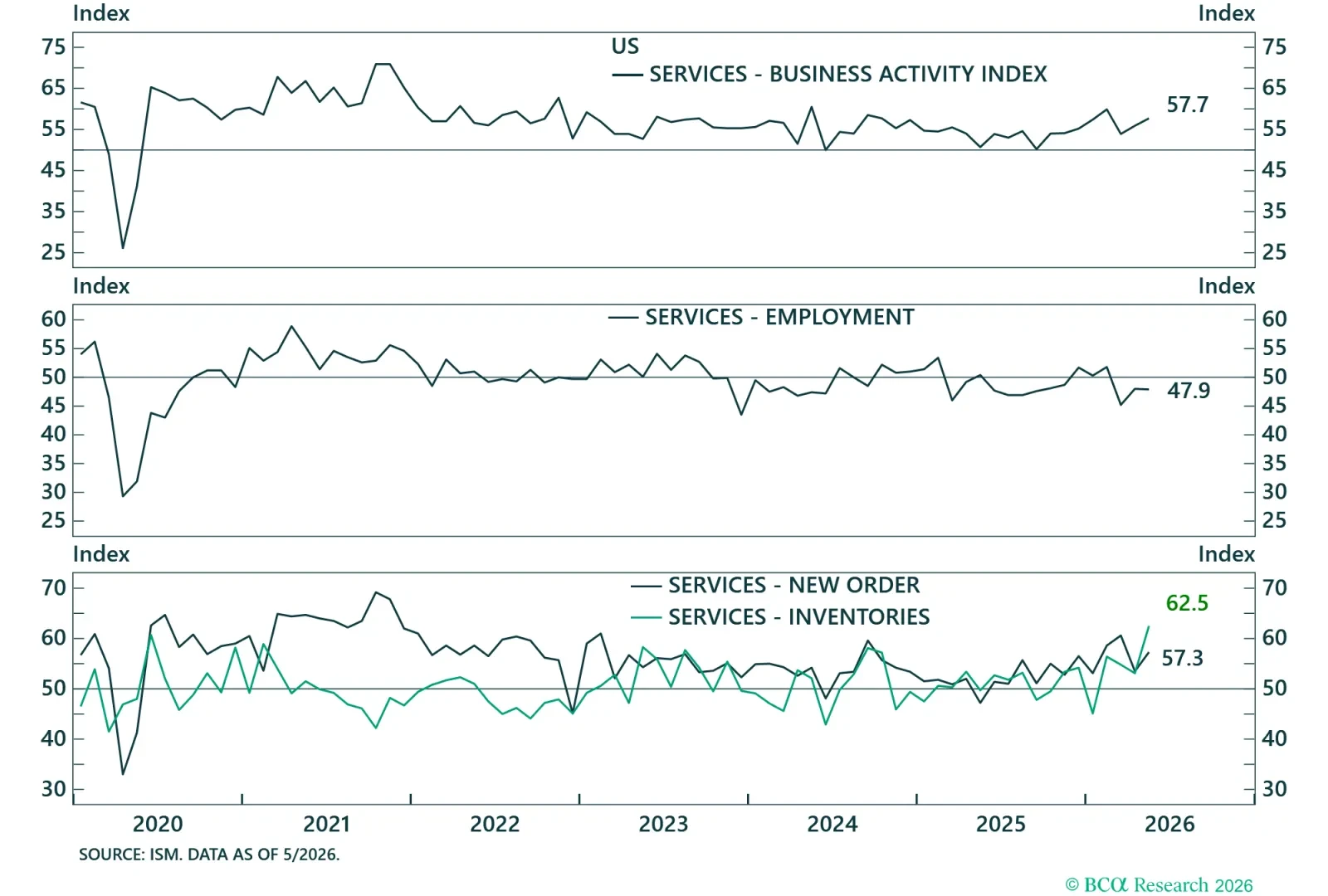

Macro Fundamentals

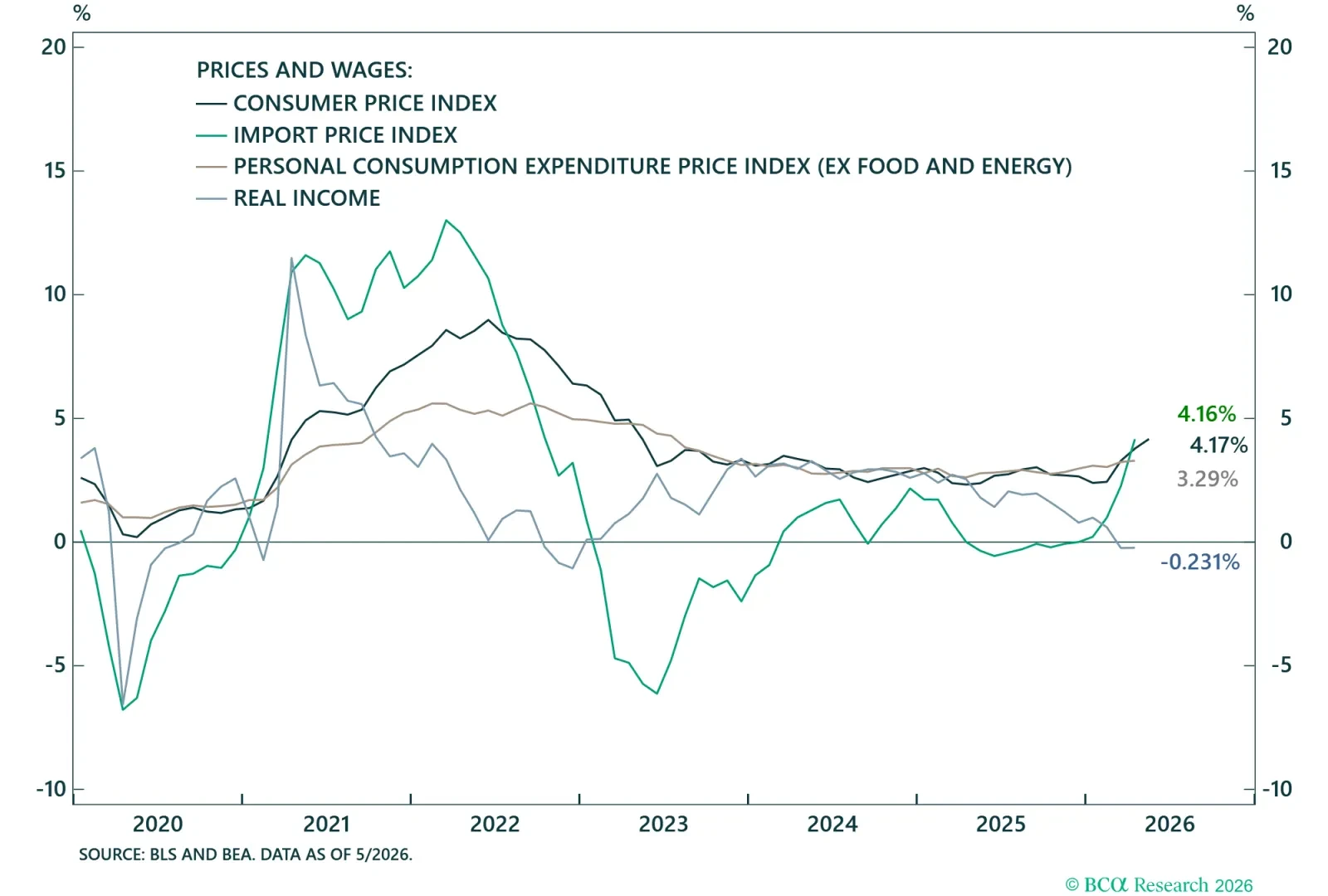

Economic conditions will influence the midterm election. Strong economic growth and rising real incomes generally improve the electoral prospects of incumbents.

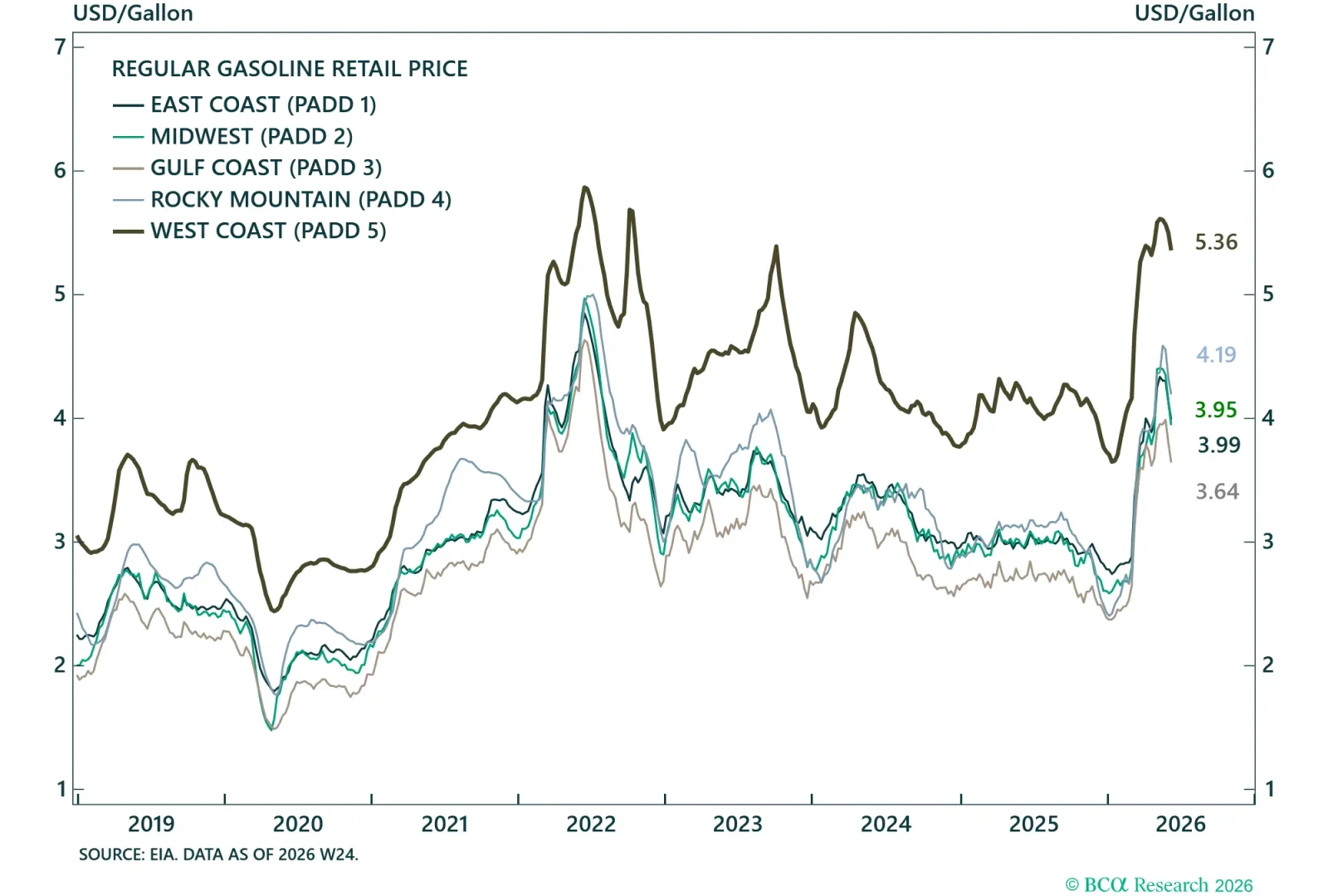

The Hormuz blockade pushed gas prices above 4 dollars per gallon for a significant swath of the country for the first time since 2022.

The trade war, and Iran and Ukraine wars, have pushed prices up.

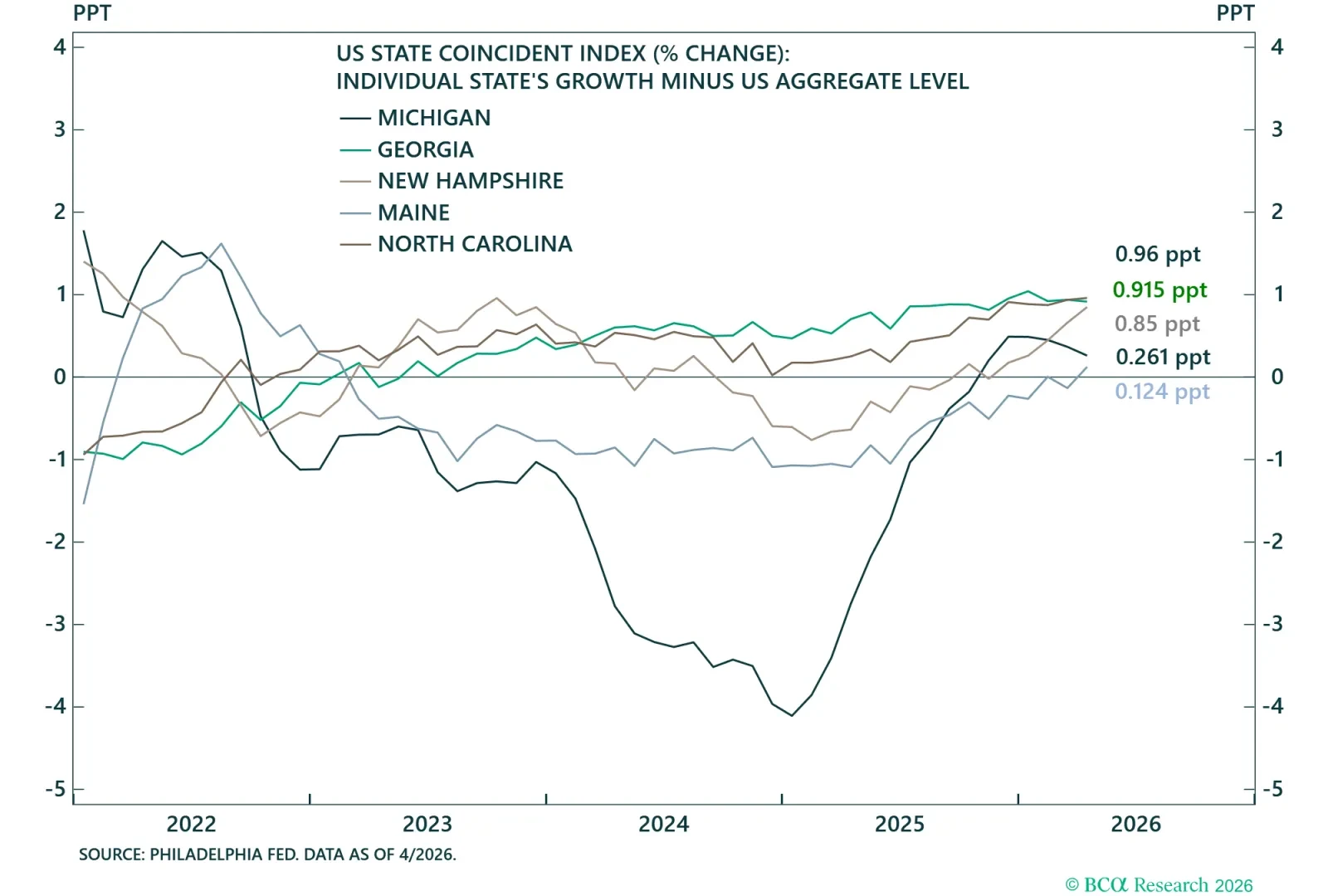

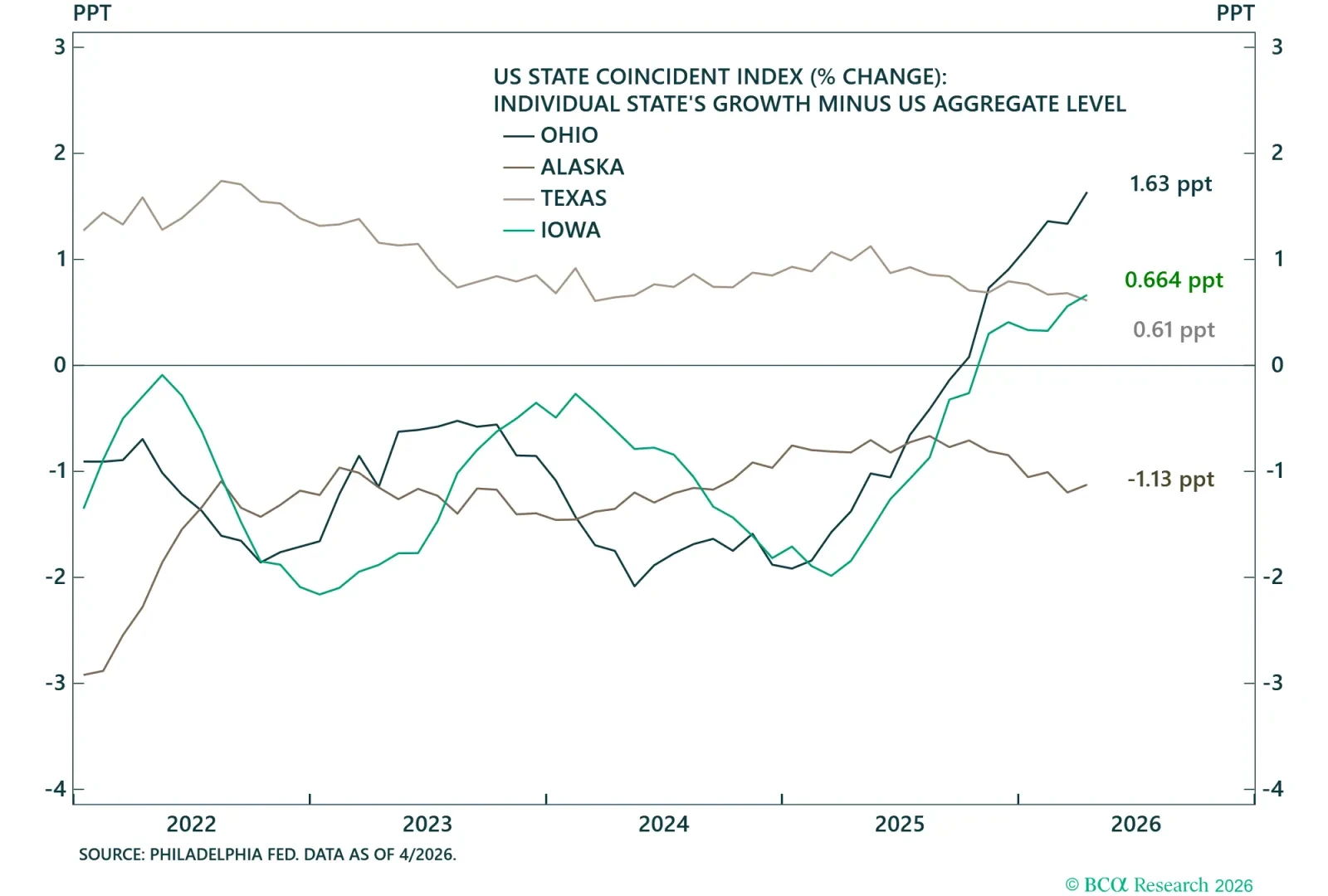

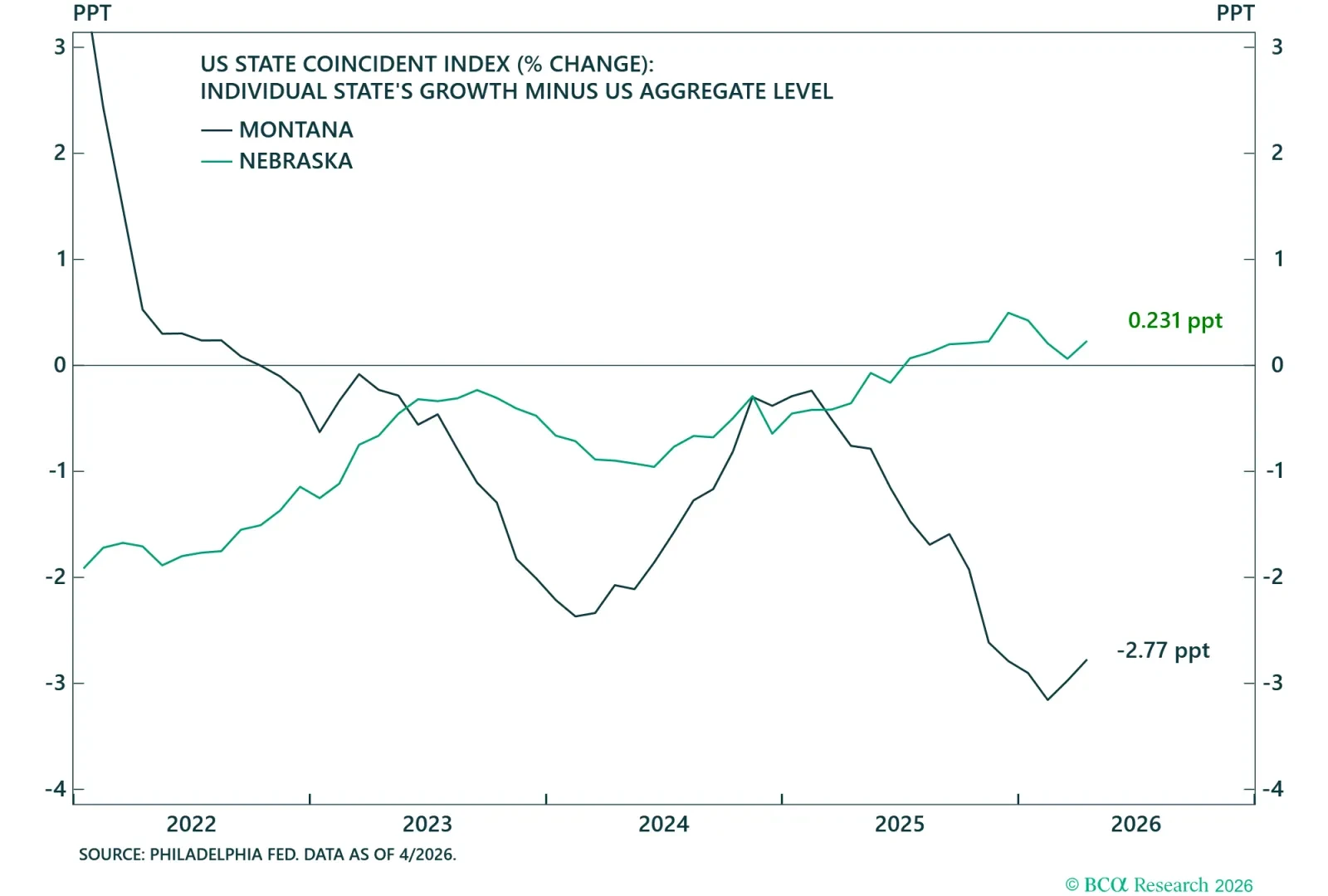

The State Coincident Index measures the economic health of a state. An increase indicates a growing state.

The State Coincident Index measures the economic health of a state. An increase indicates a growing state.

The State Coincident Index measures the economic health of a state. An increase indicates a growing state.

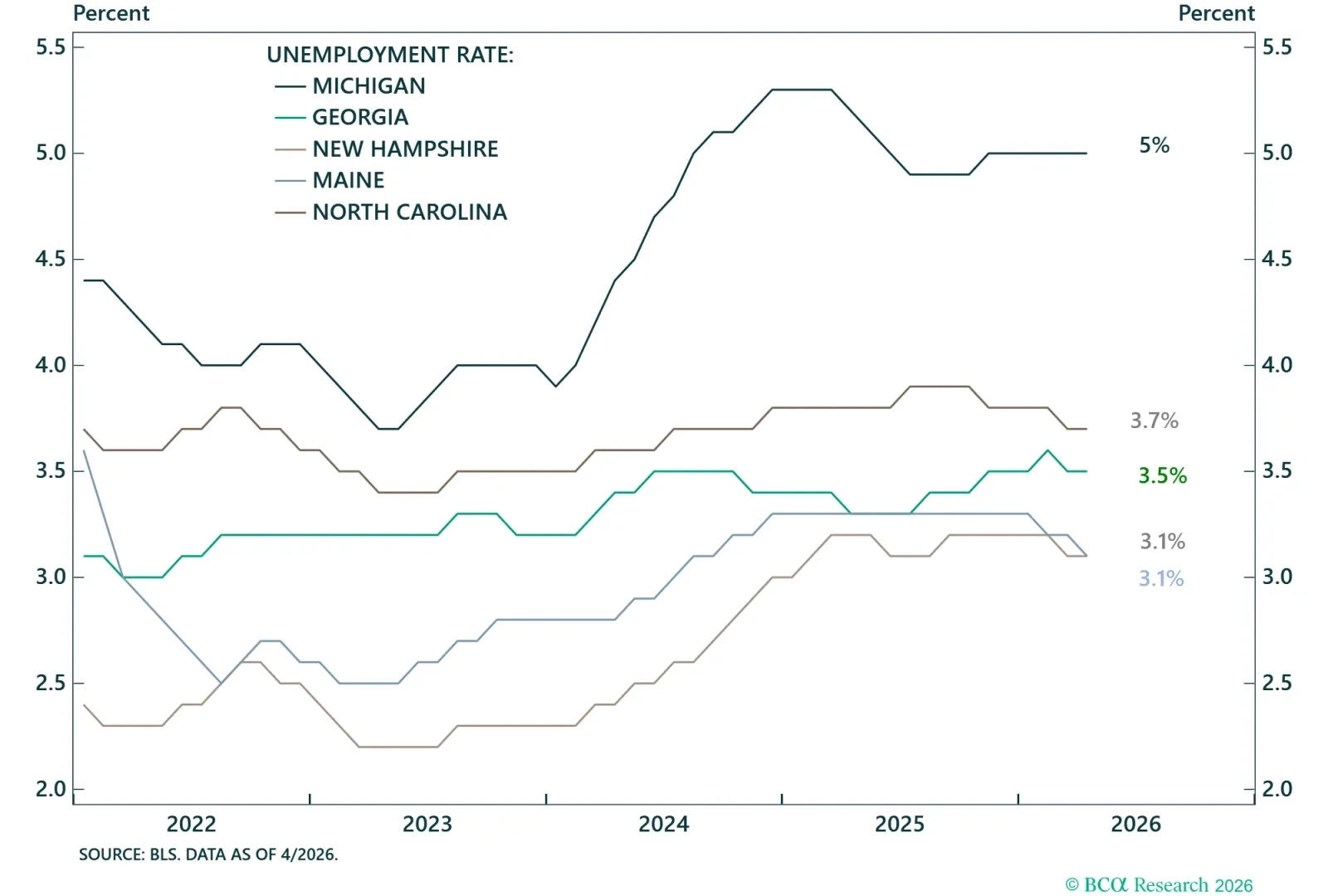

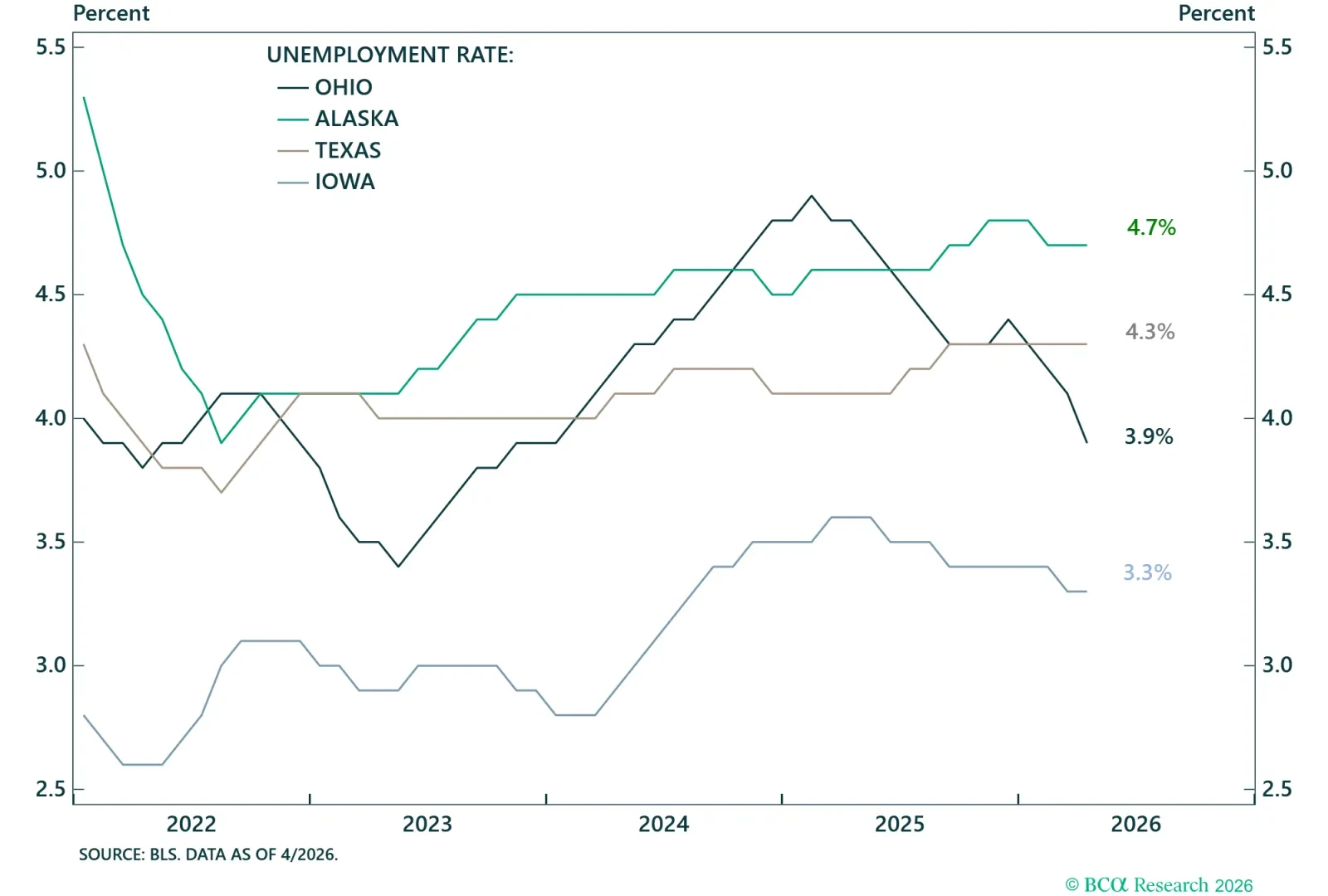

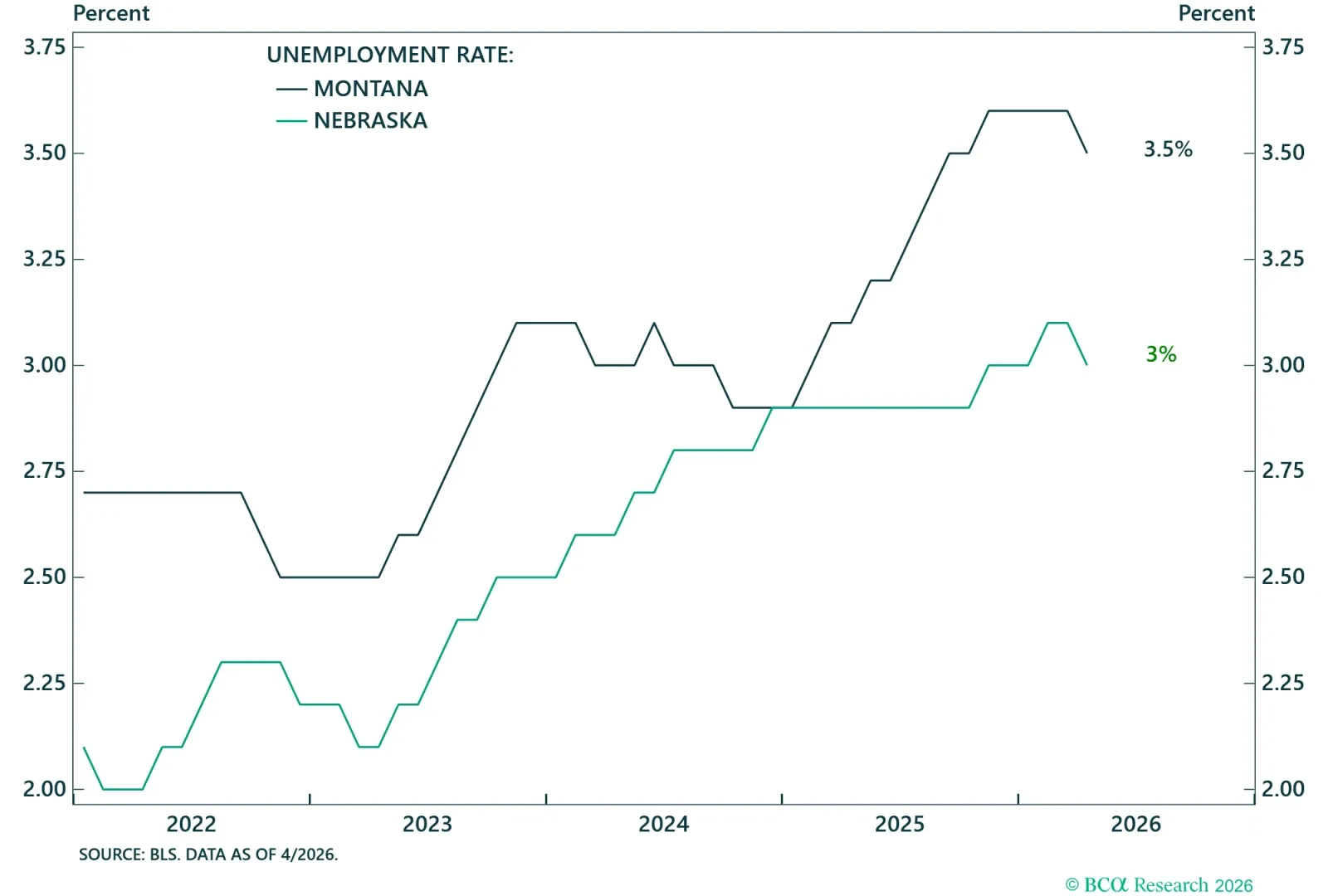

Rising unemployment in swing states could imperil Republican control of the Senate.

Rising unemployment in swing states could imperil Republican control of the Senate.

Rising unemployment in swing states could imperil Republican control of the Senate.

US Political Capital

To assess any leader’s capability, namely their ability to alter the policy setting that affects the economy and financial markets, we need to measure their political capital. Political capital encompasses both the power of leadership to effect change and the strength of checks and balances that mitigate that power. A president who oversees a growing economy will have larger political capital, while a president who oversees an economy in trouble, will have limited policy options.

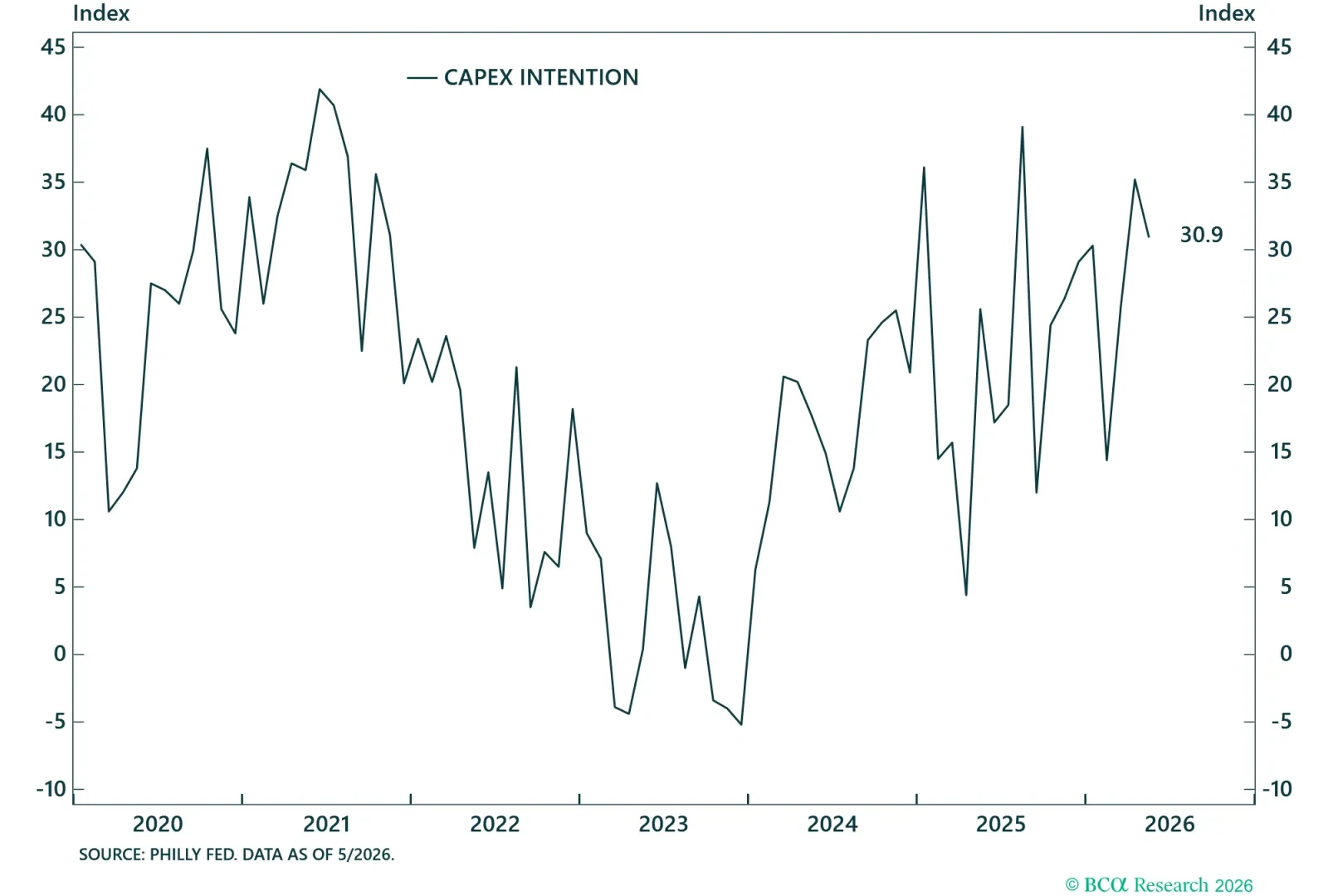

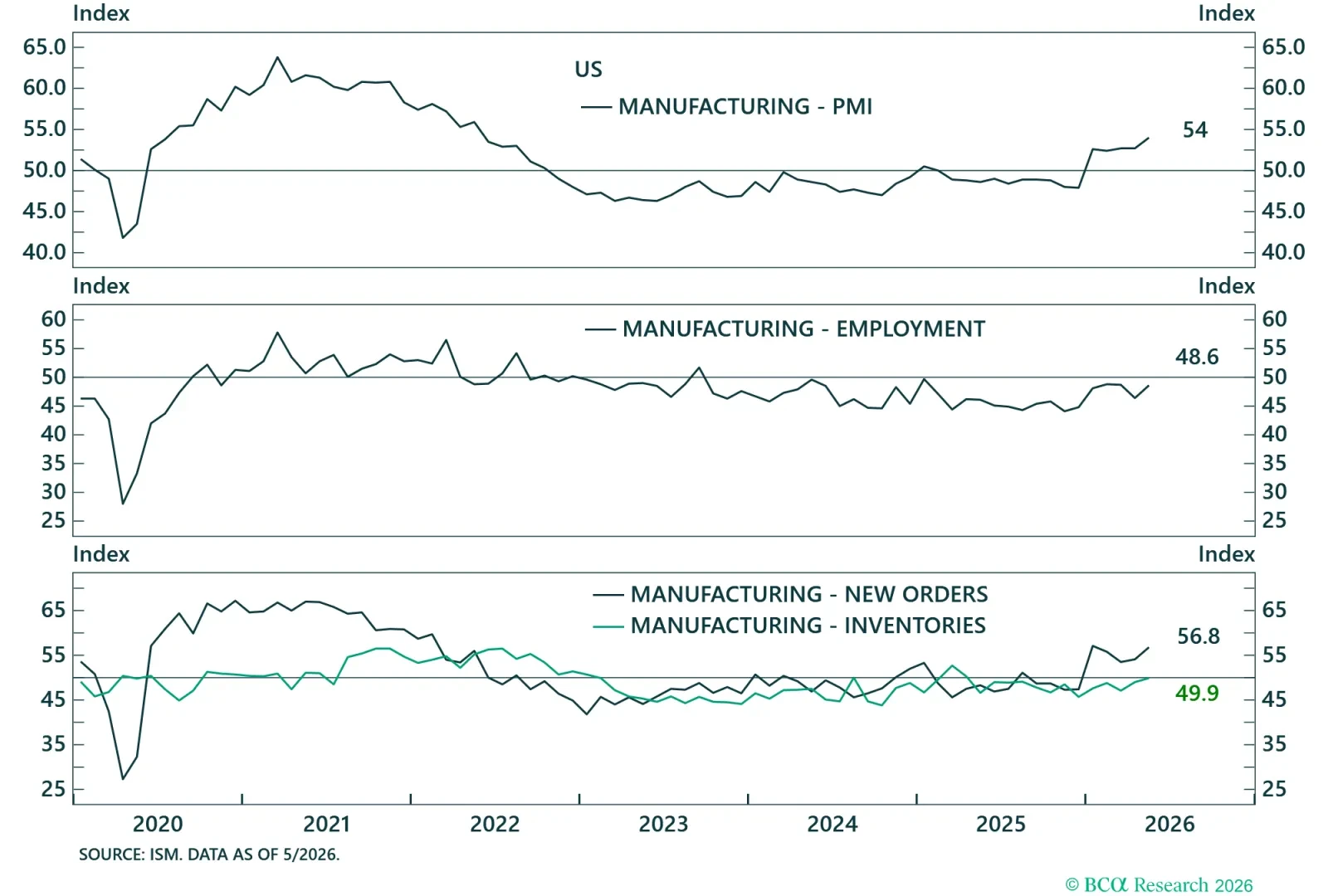

Businesses are still planning to spend on CAPEX.

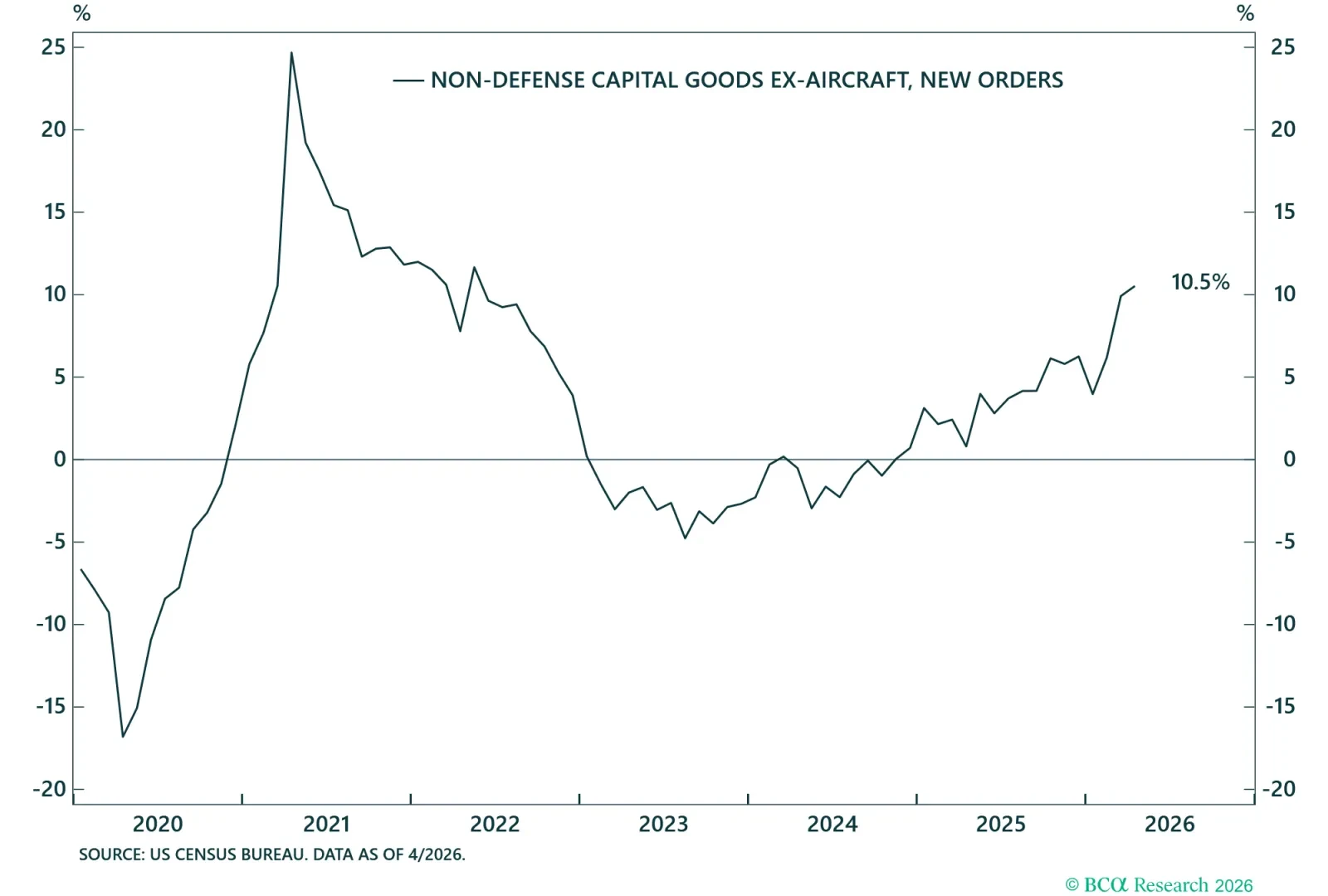

CAPEX new orders are still strong.

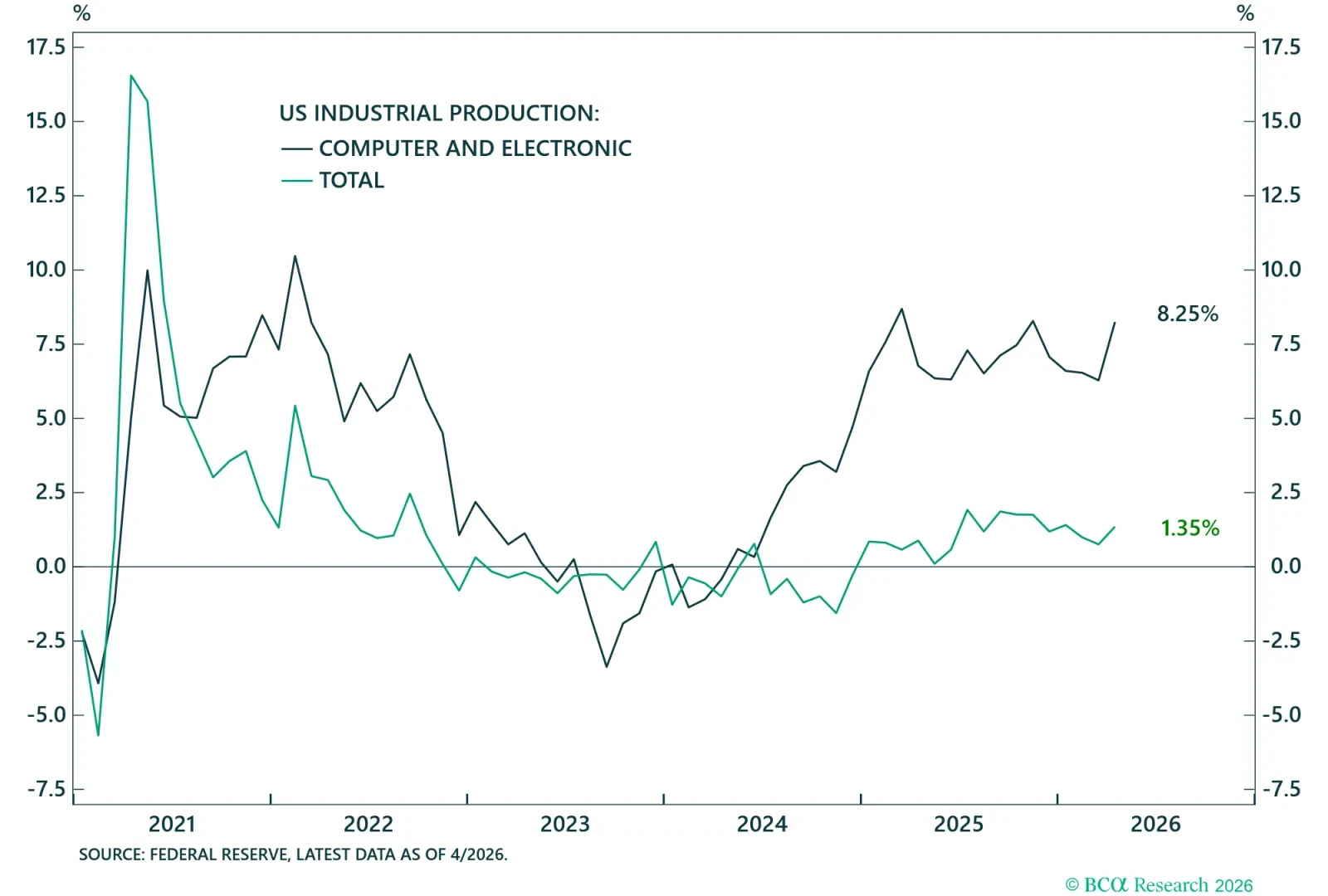

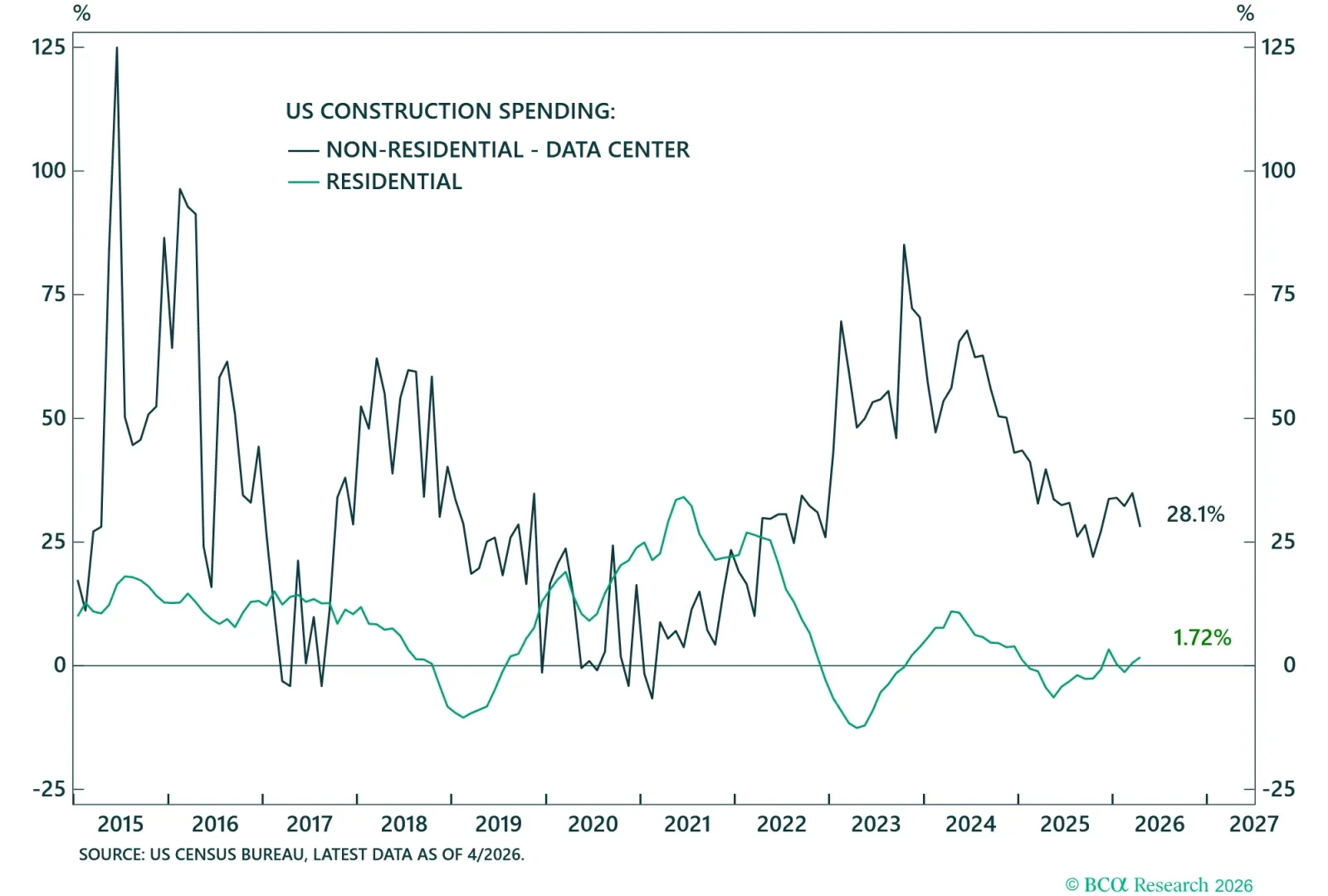

US AI-related CAPEX remains strong.

The AI-driven boom in data center construction is still strong.

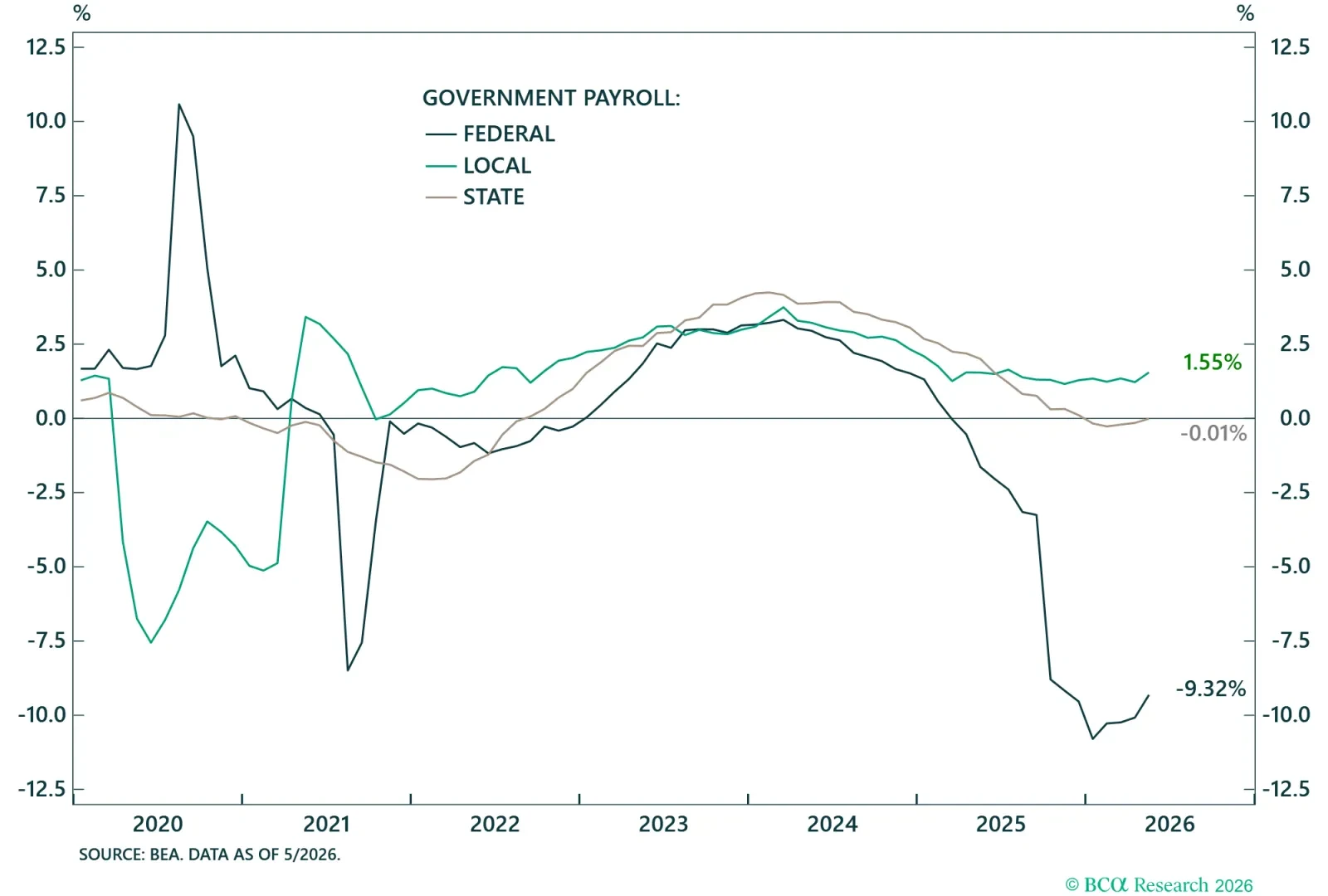

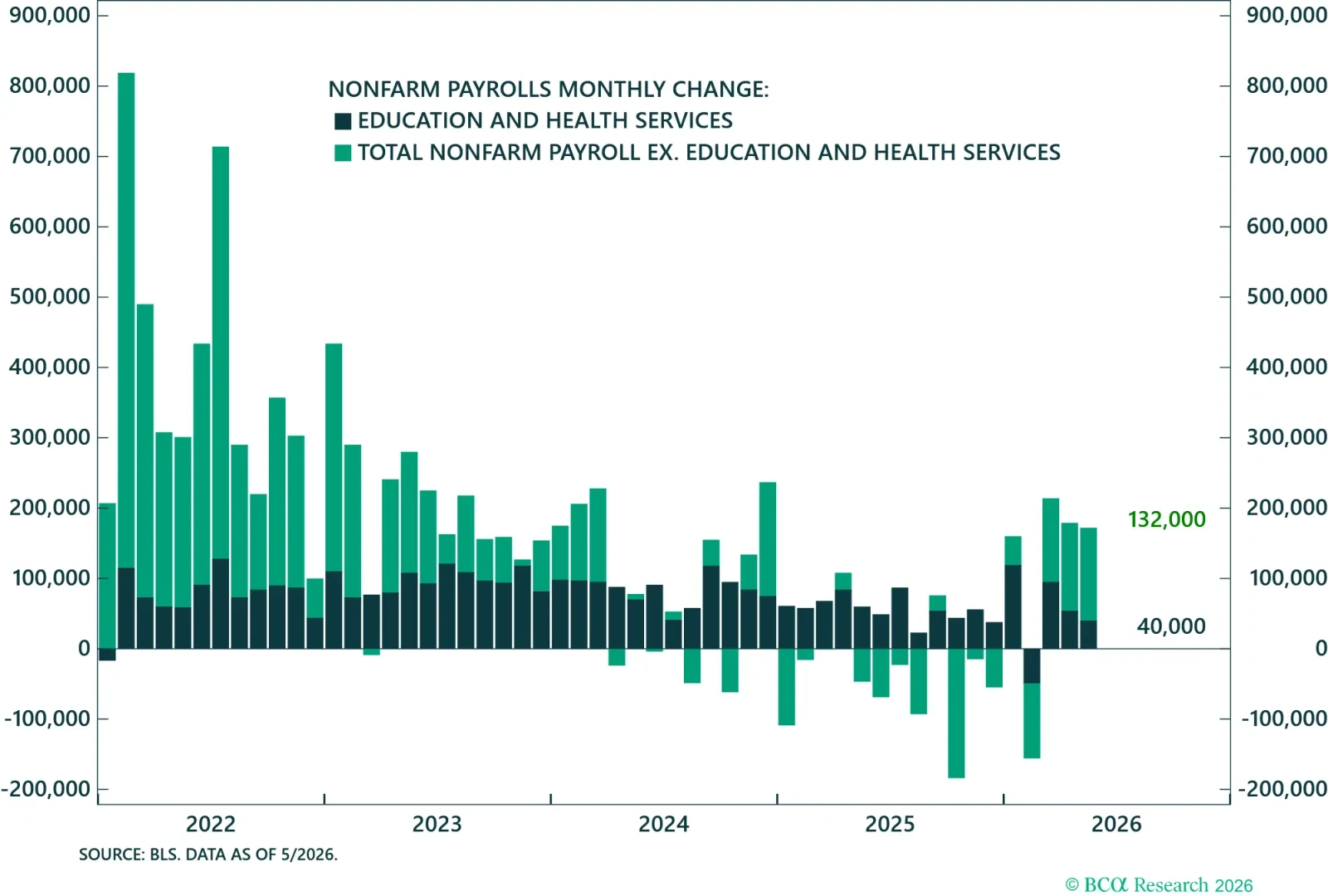

Will this cycle continue to be a jobless cycle?

Will this cycle be a jobless cycle?

Year-on-year growth of payrolls. Both federal and state governments have been shedding workers.

Transfers to households are still strong and will support consumption.

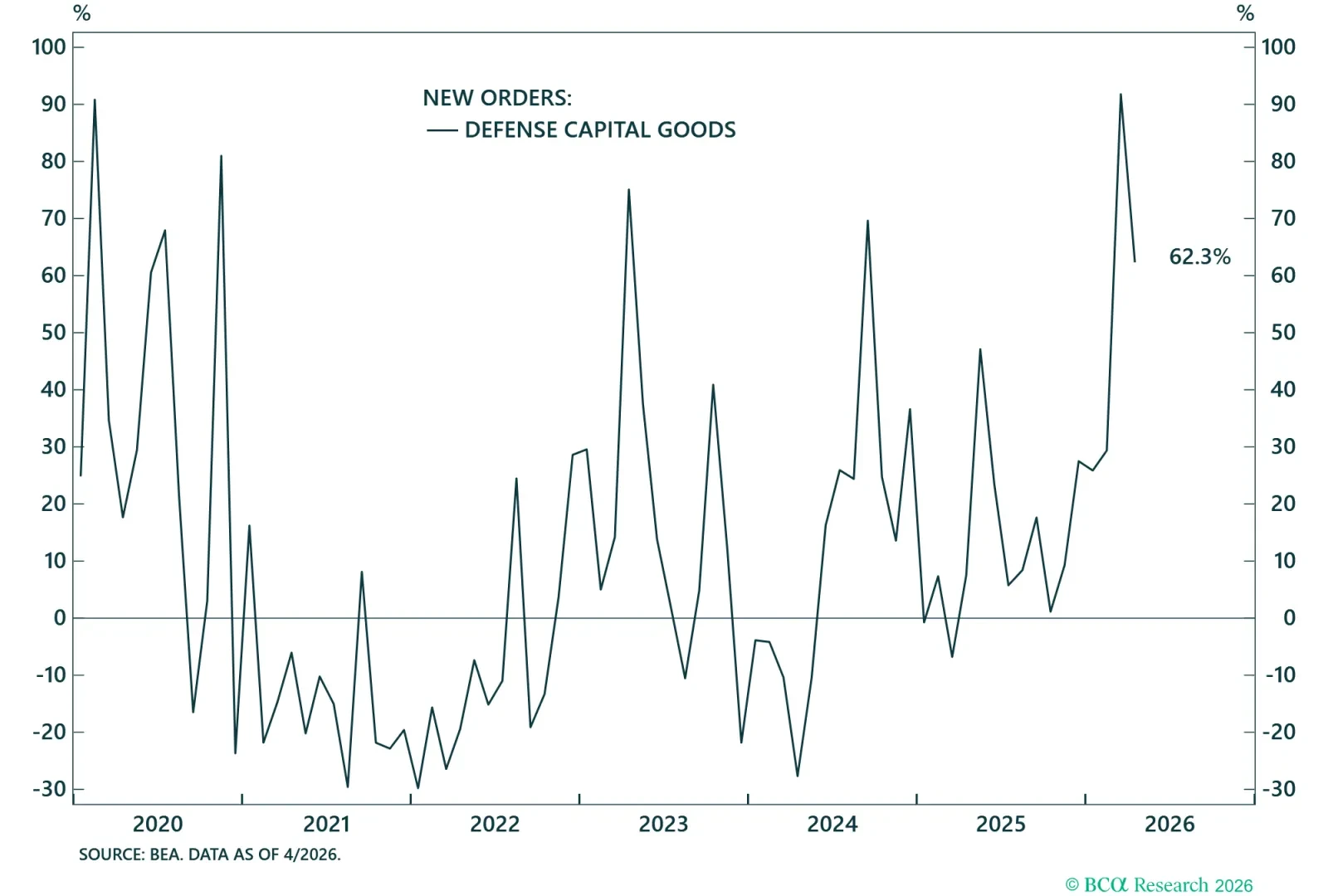

Global instability will continue to spur US defense spending.

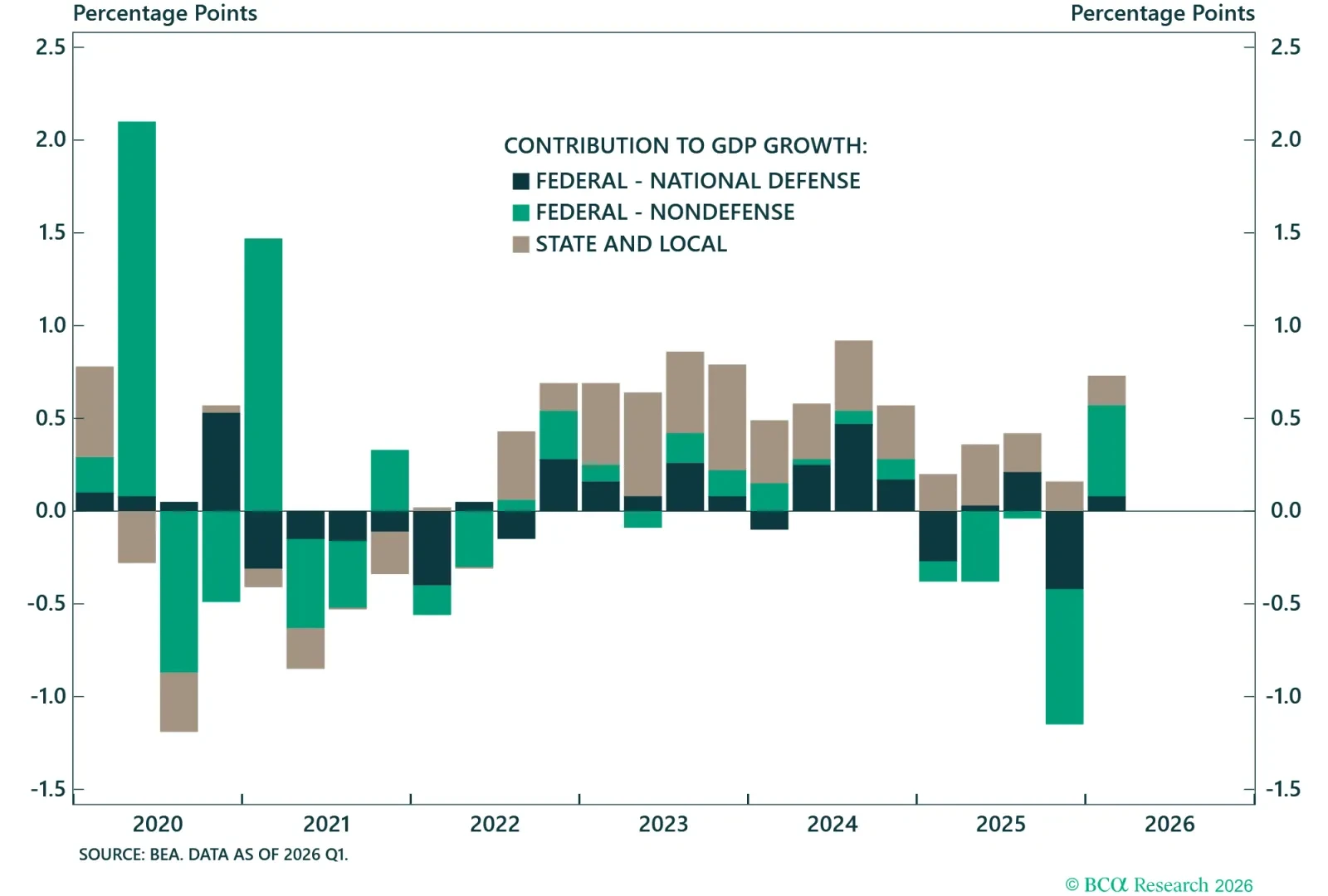

Government spending will continue to be a source of growth this year, given deficit expansion from tax cuts, tariff revenue disappointments, defense spending, and potentially a gasoline tax cut.

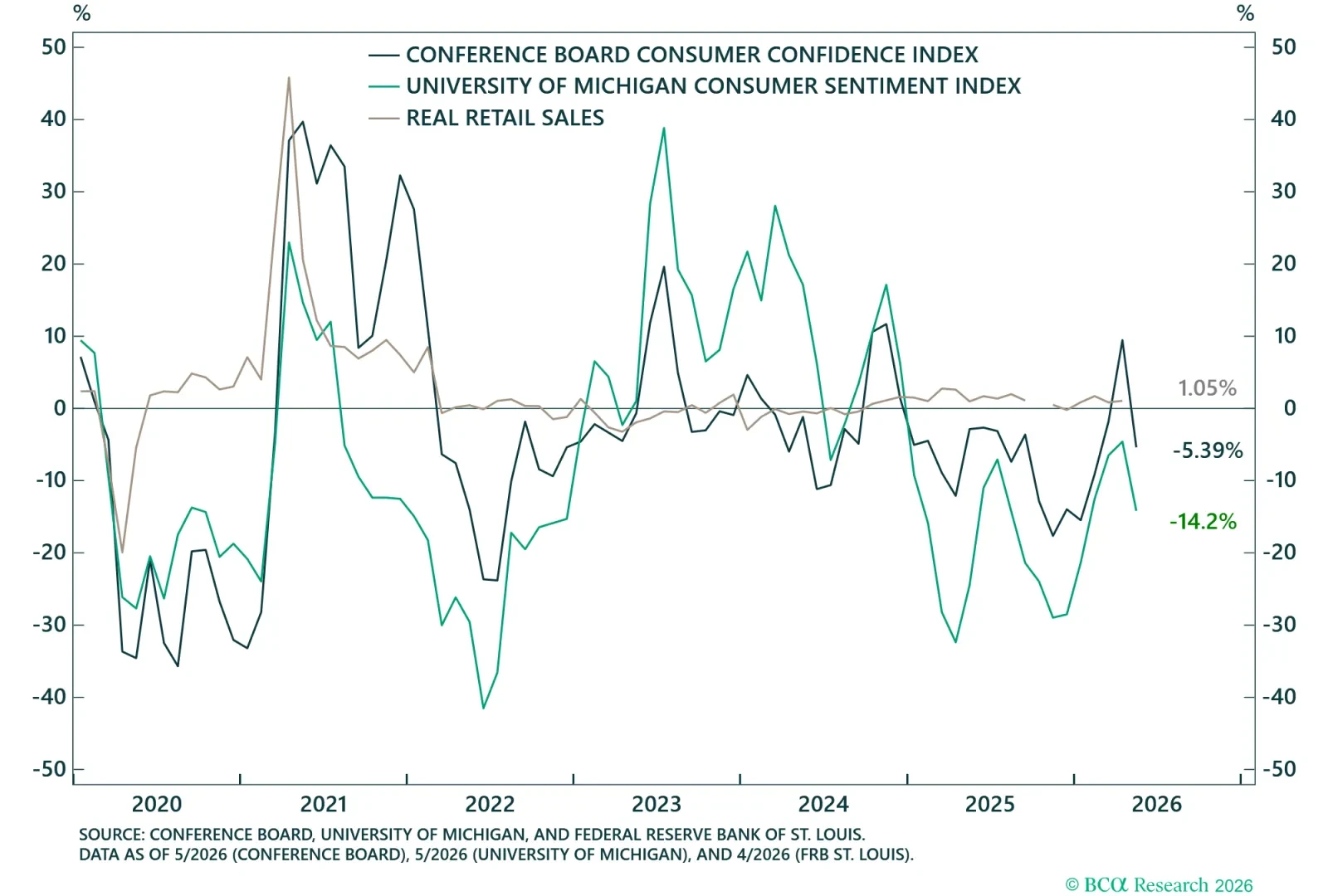

Consumers are spending despite their pessimistic outlook.

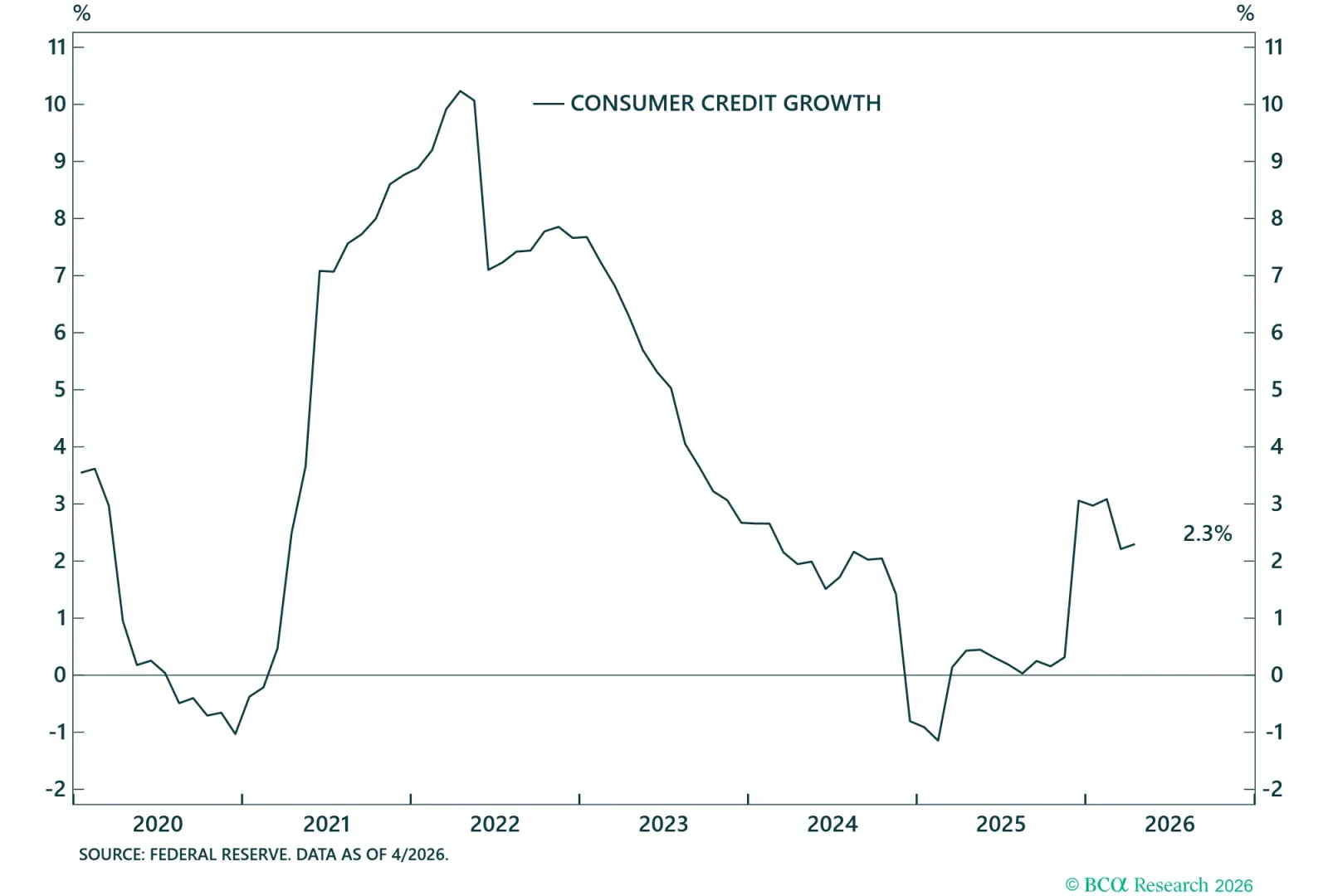

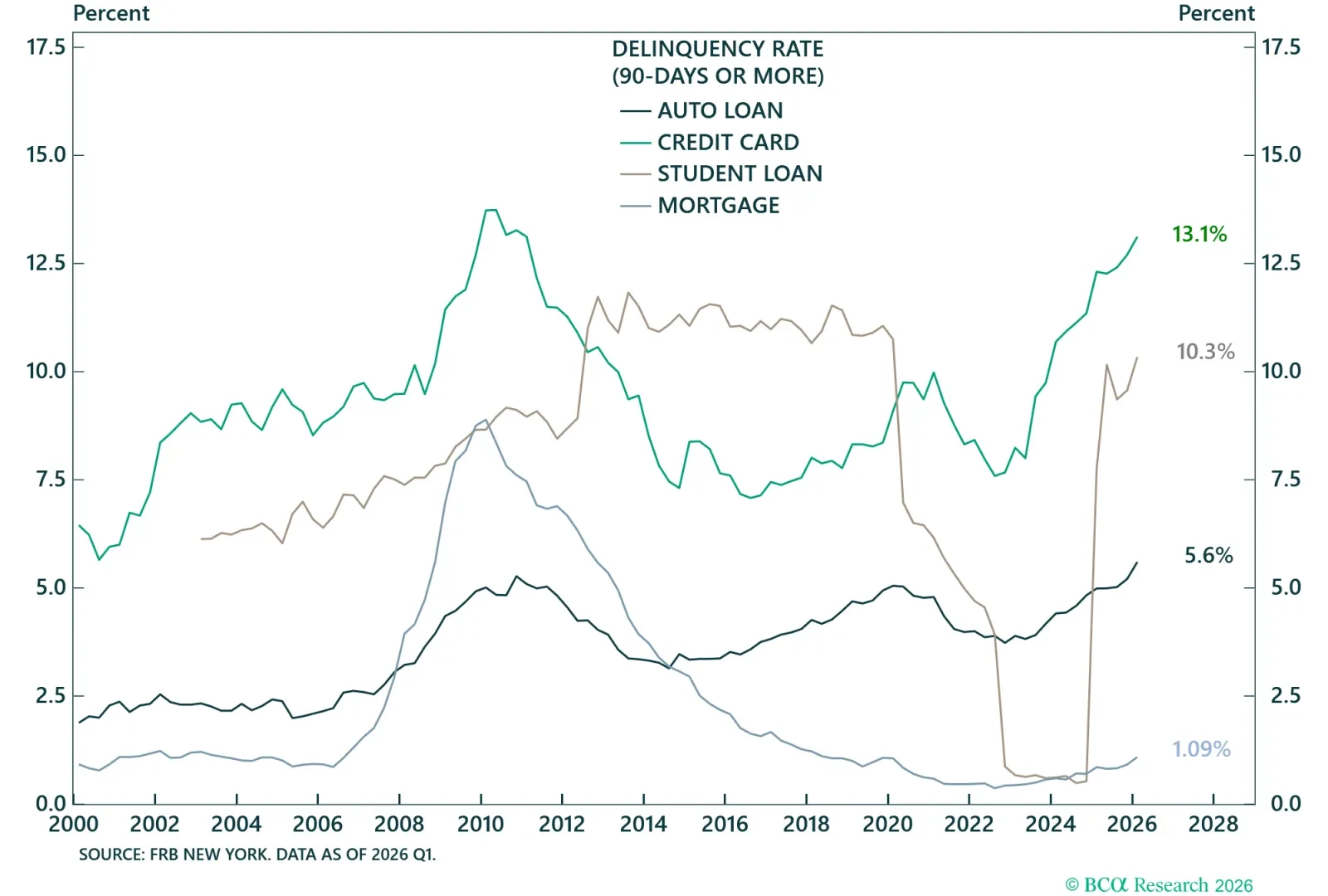

Banks are still willing to expand consumer credit, but credit growth has likely peaked. Credits are substitutes to income, when the latter is weak.

90-days and more delinquency rates of major consumer credit categories. Rising delinquency rates are a worrying sign of consumer distress.

A broad-based gain in jobs will be beneficial to the president and his party.

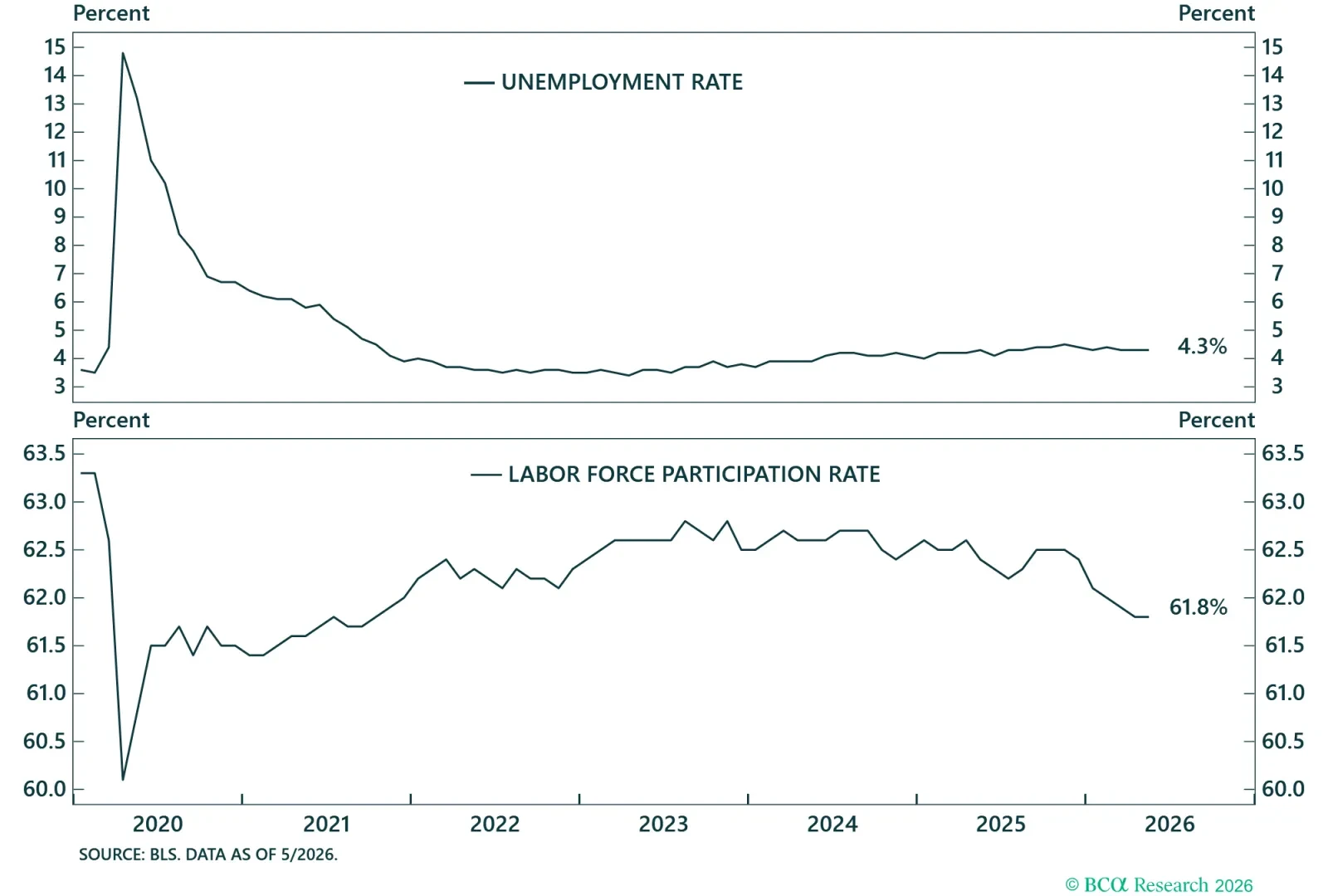

The unemployment rate is benign, but the labour force participation rate has declined, indicating a weakening labor market.

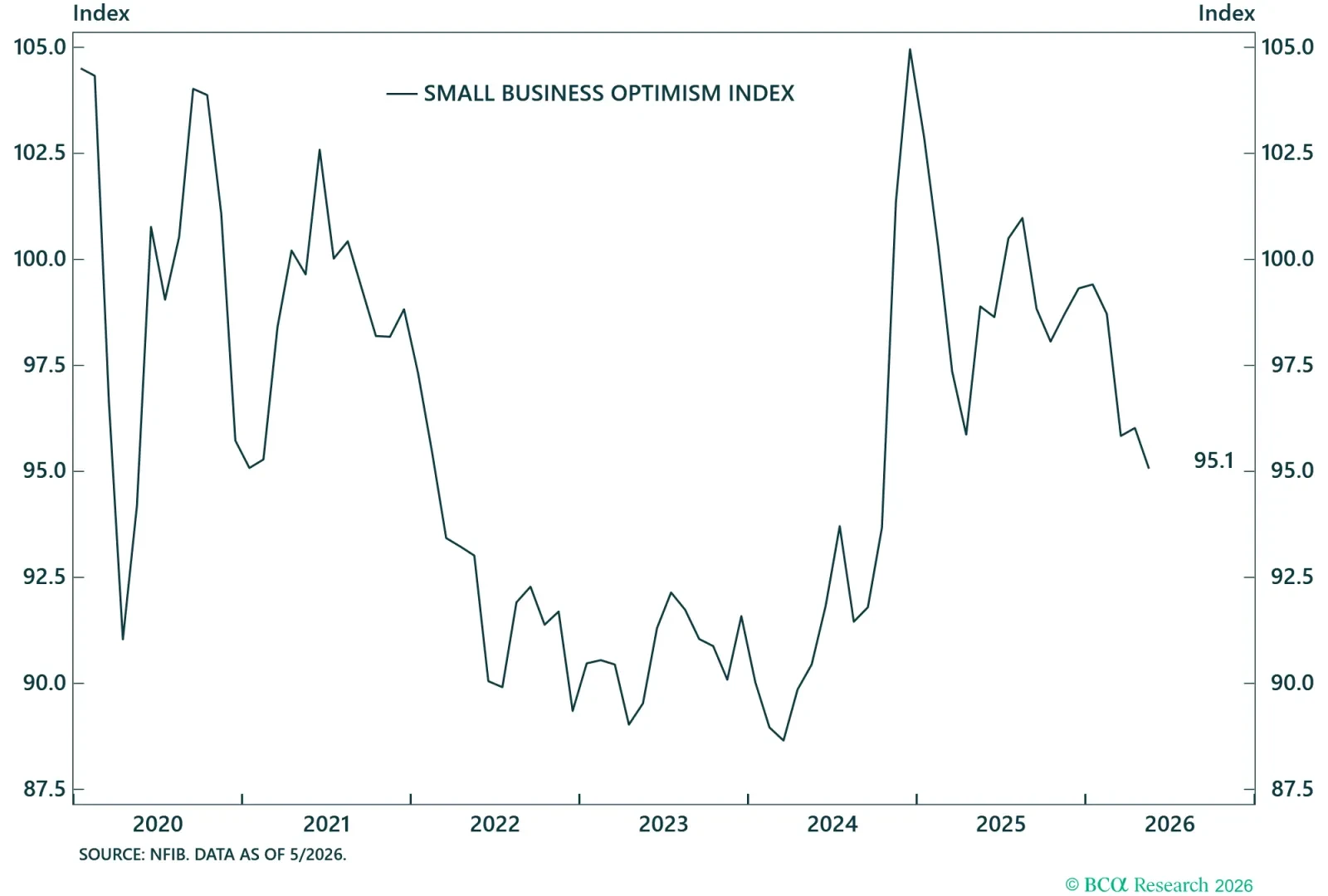

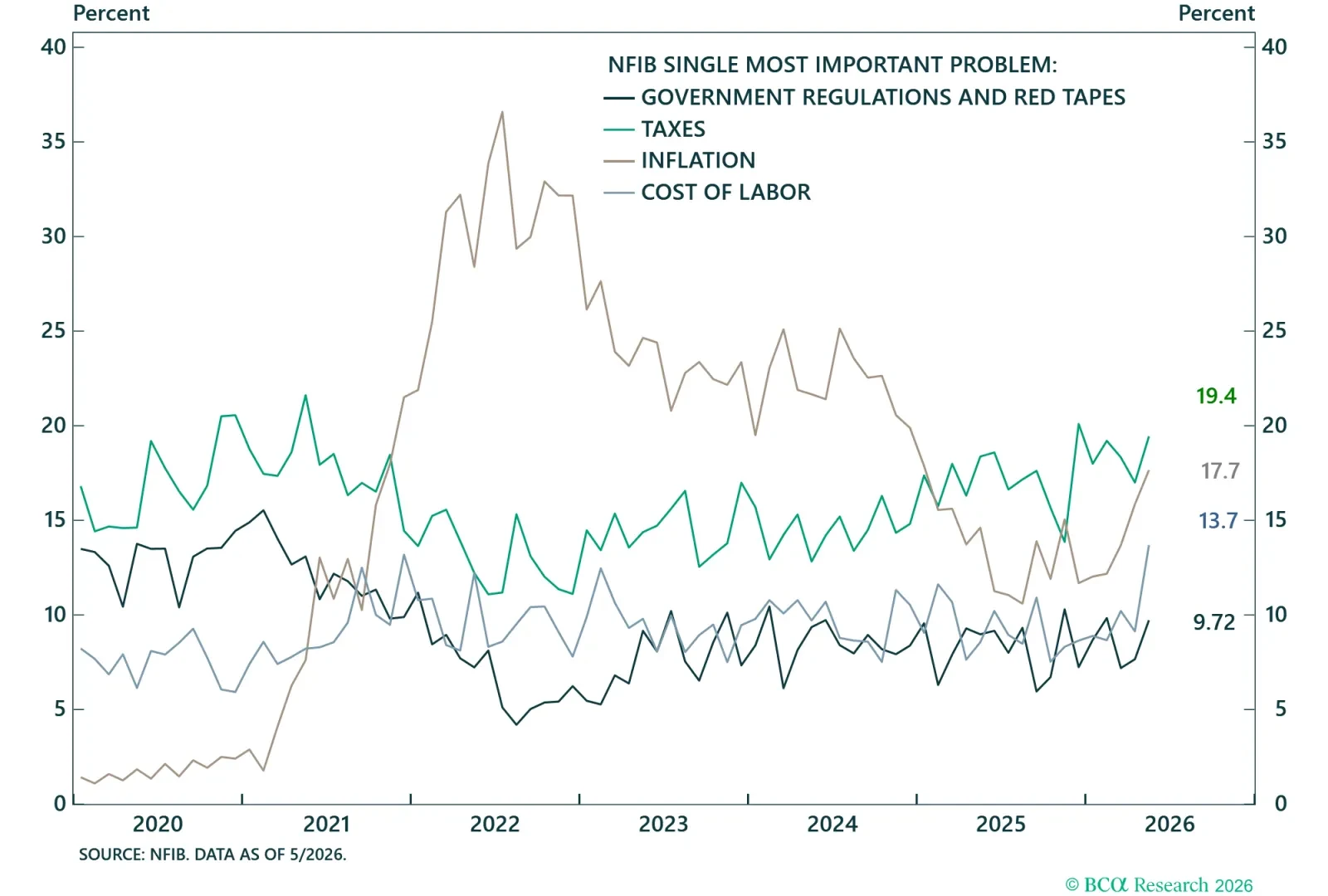

Small businesses are canaries in the coal mine. They tend to be the first to suffer from trade-related issues, or when the economy slows down.

Small businesses are an important part of the economy and a major constituent. Their biggest concerns are taxes (tariffs) and inflation.

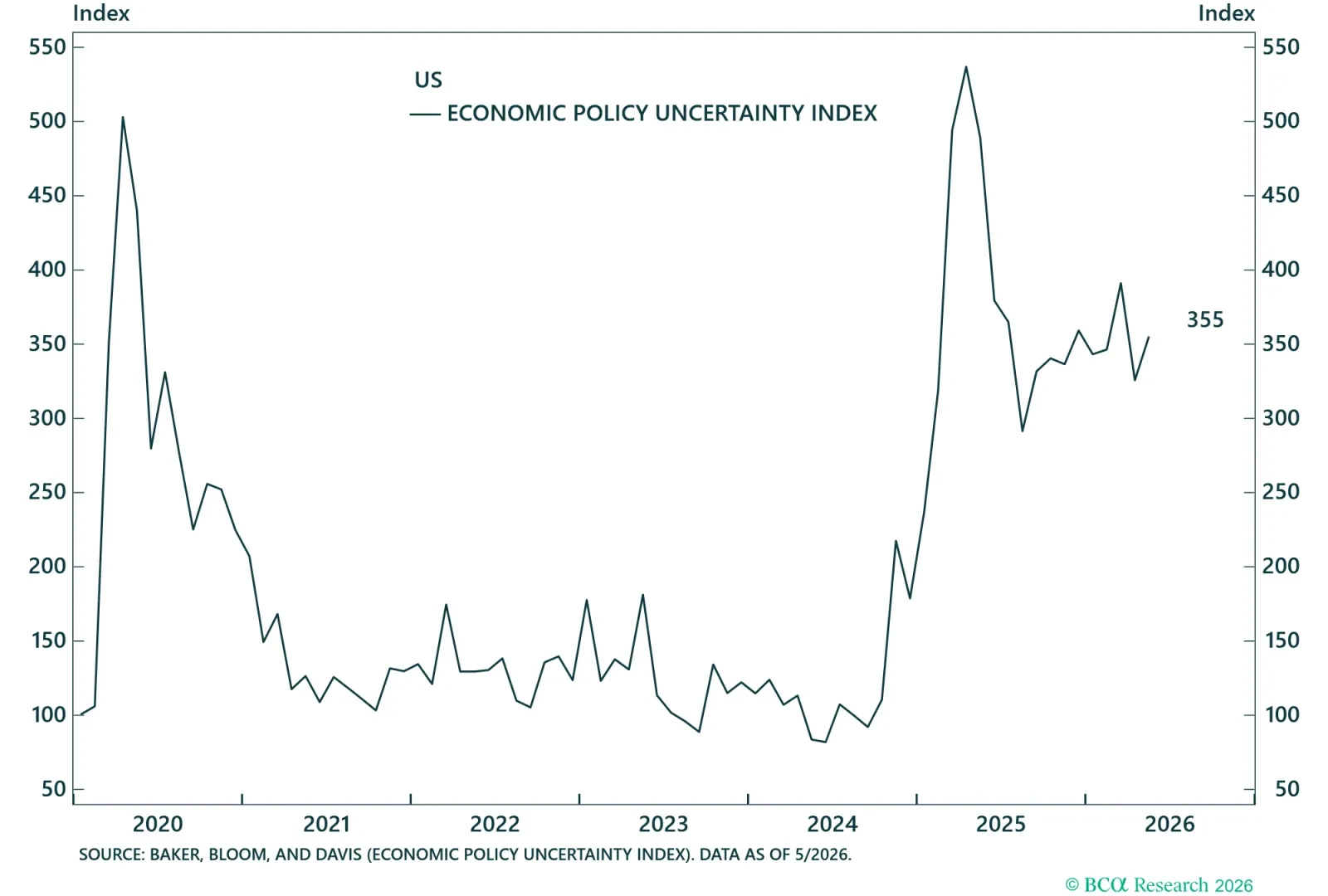

No reprieve from policy uncertainty.

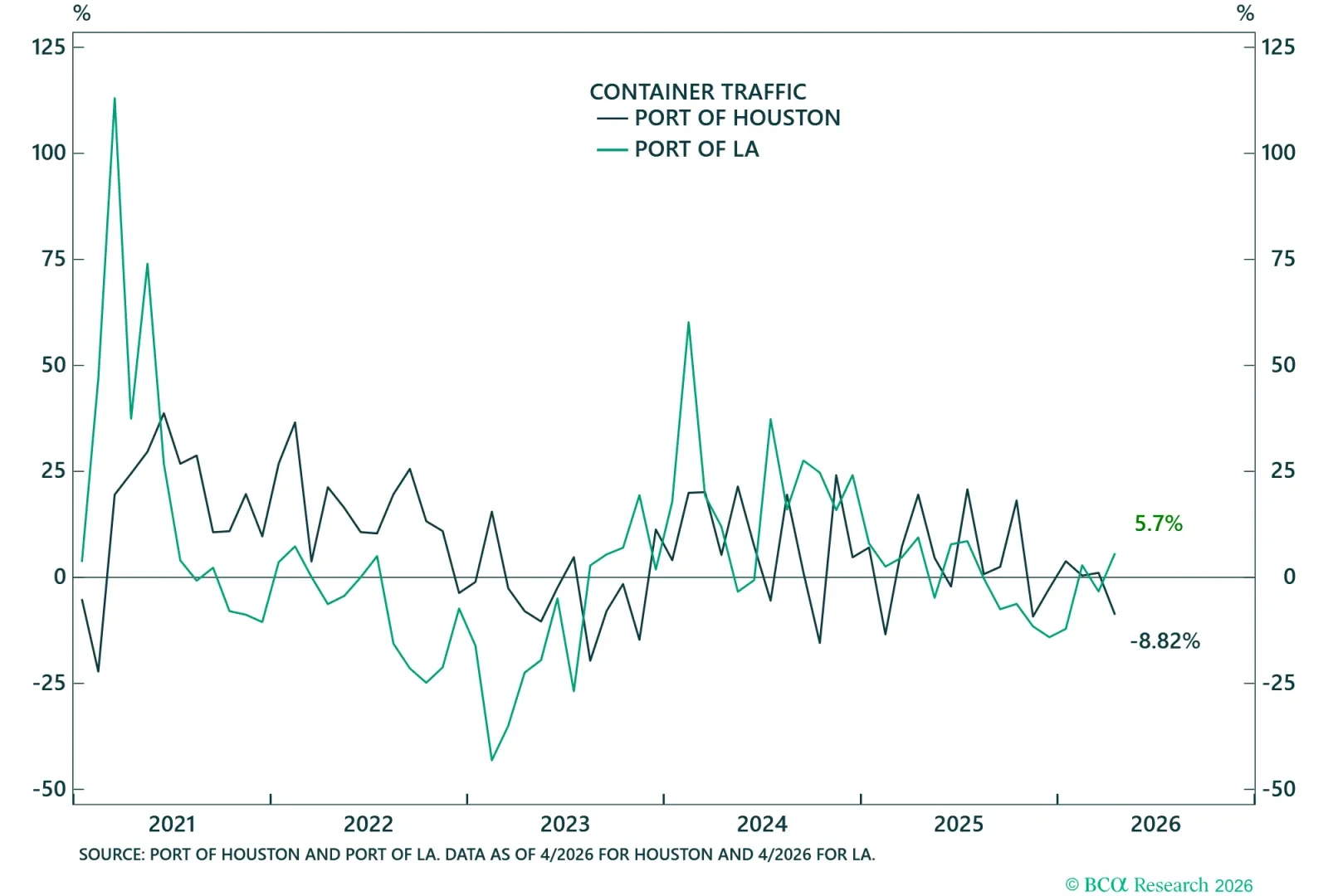

Container traffic is weak, indicating a global trade weakness.

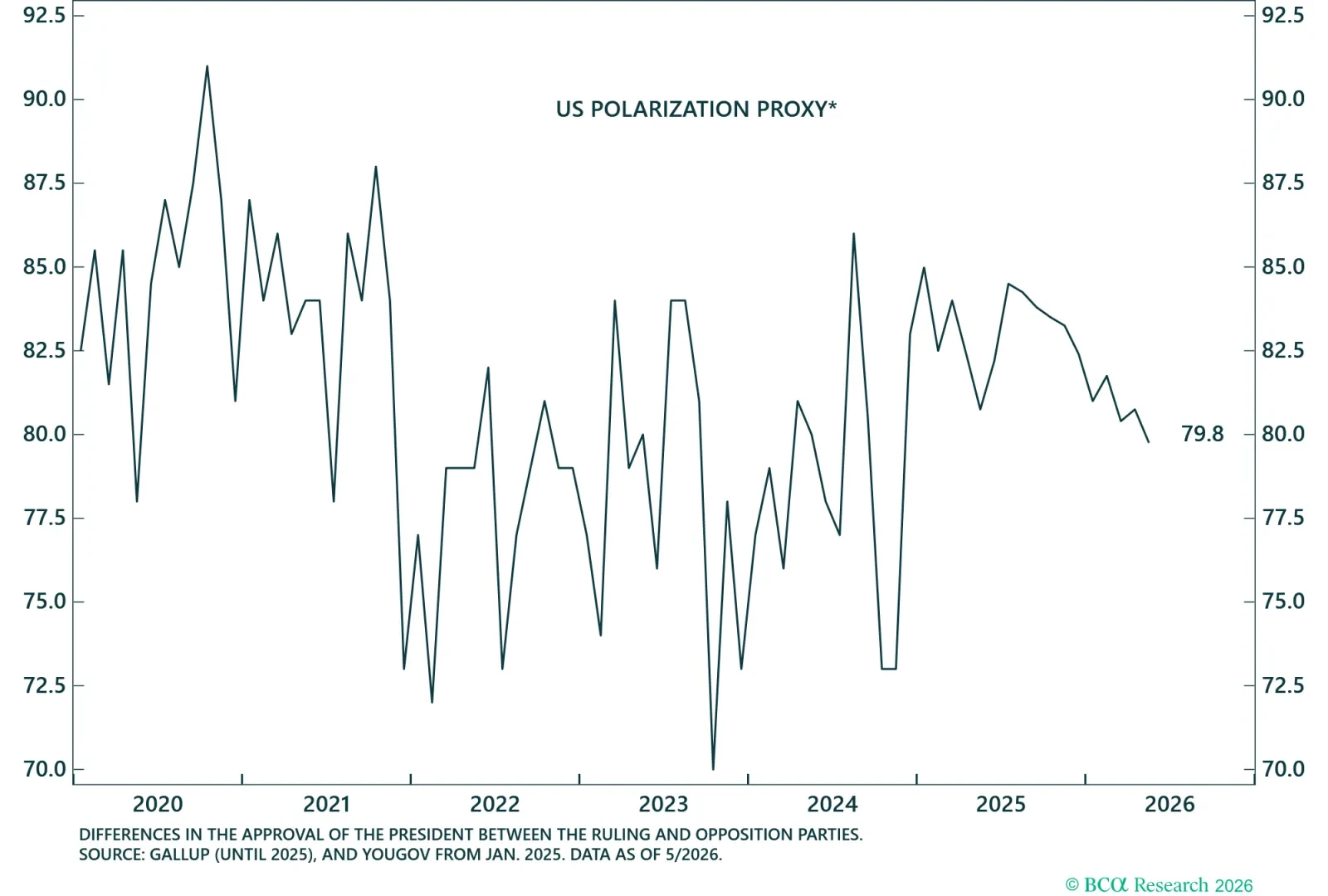

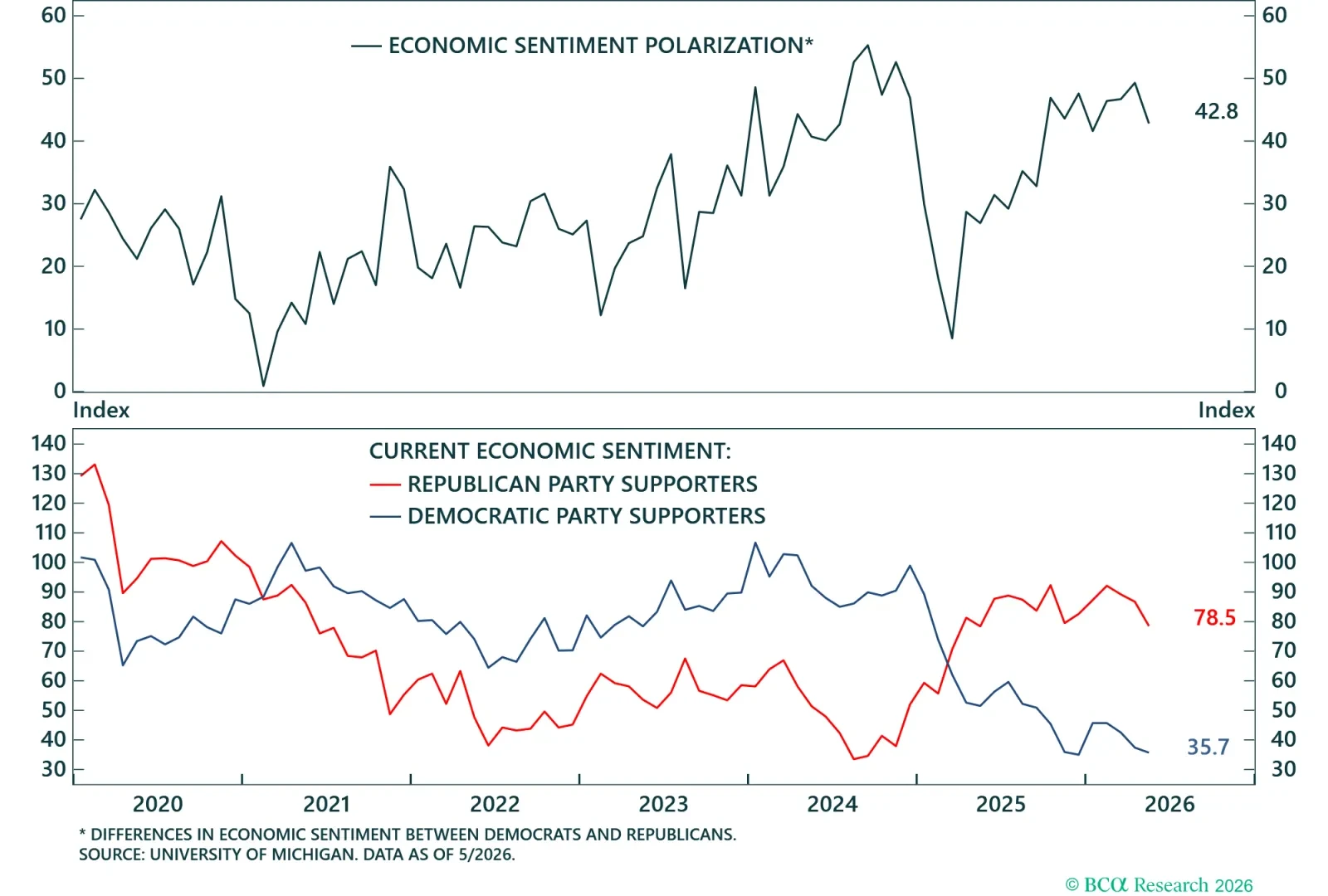

The US is at or near peak polarization, but depolarization could mean that everyone agrees in their disapproval of the current government.

Declining polarization implies rising bipartisan agreement on the poor state of the economy. Republicans’ sentiment had been declining for a few consecutive months this year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}