Economy

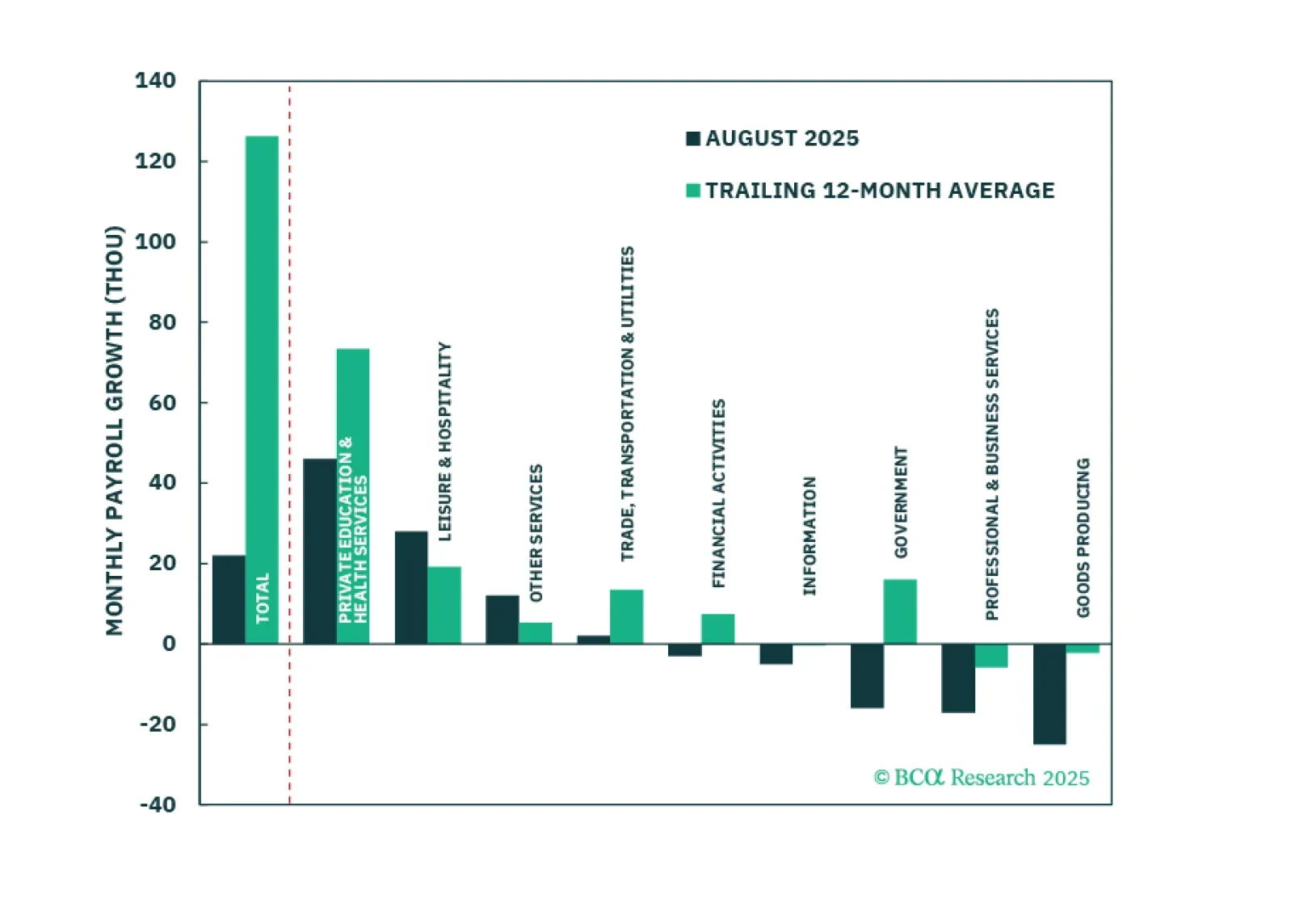

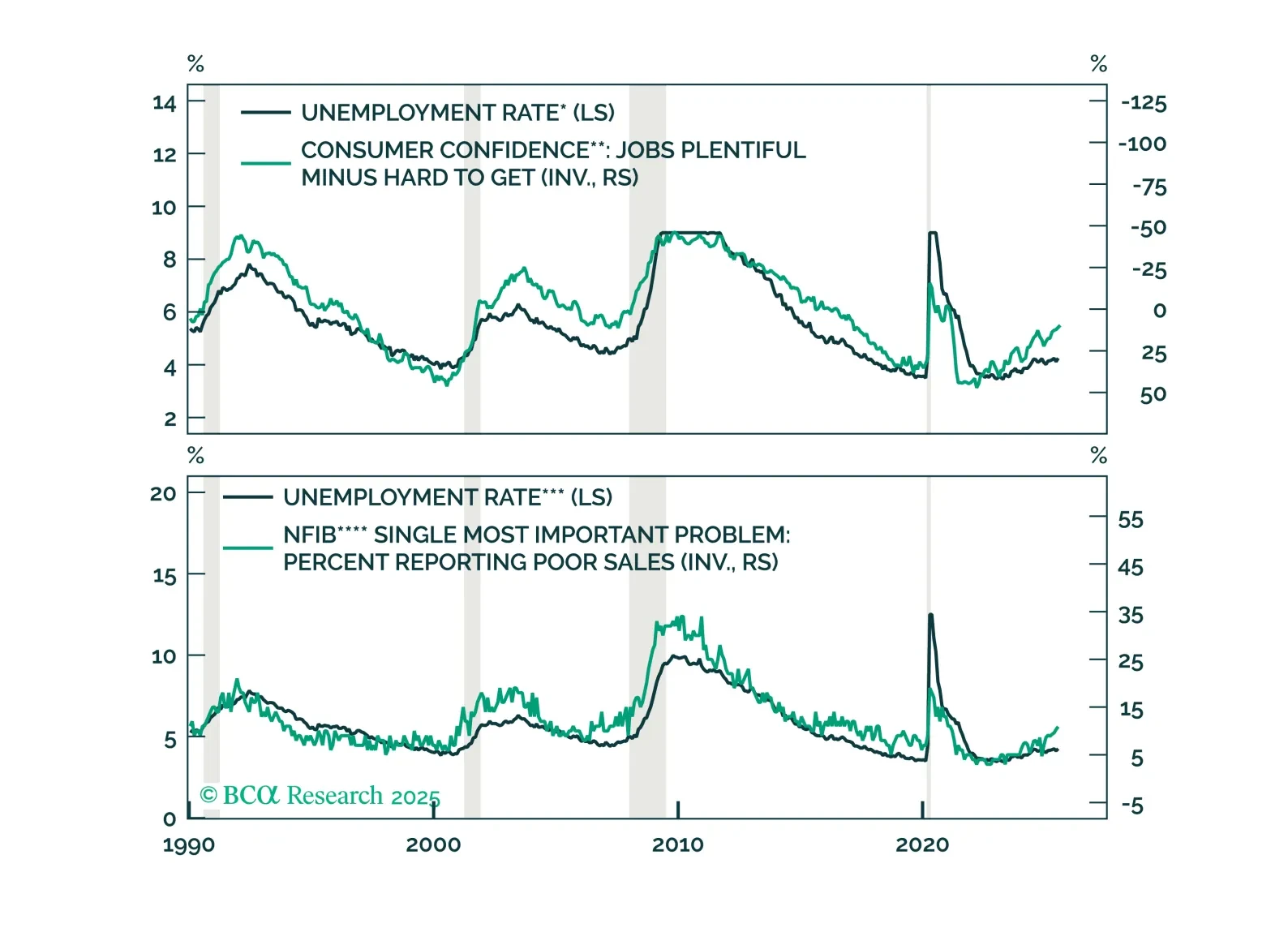

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

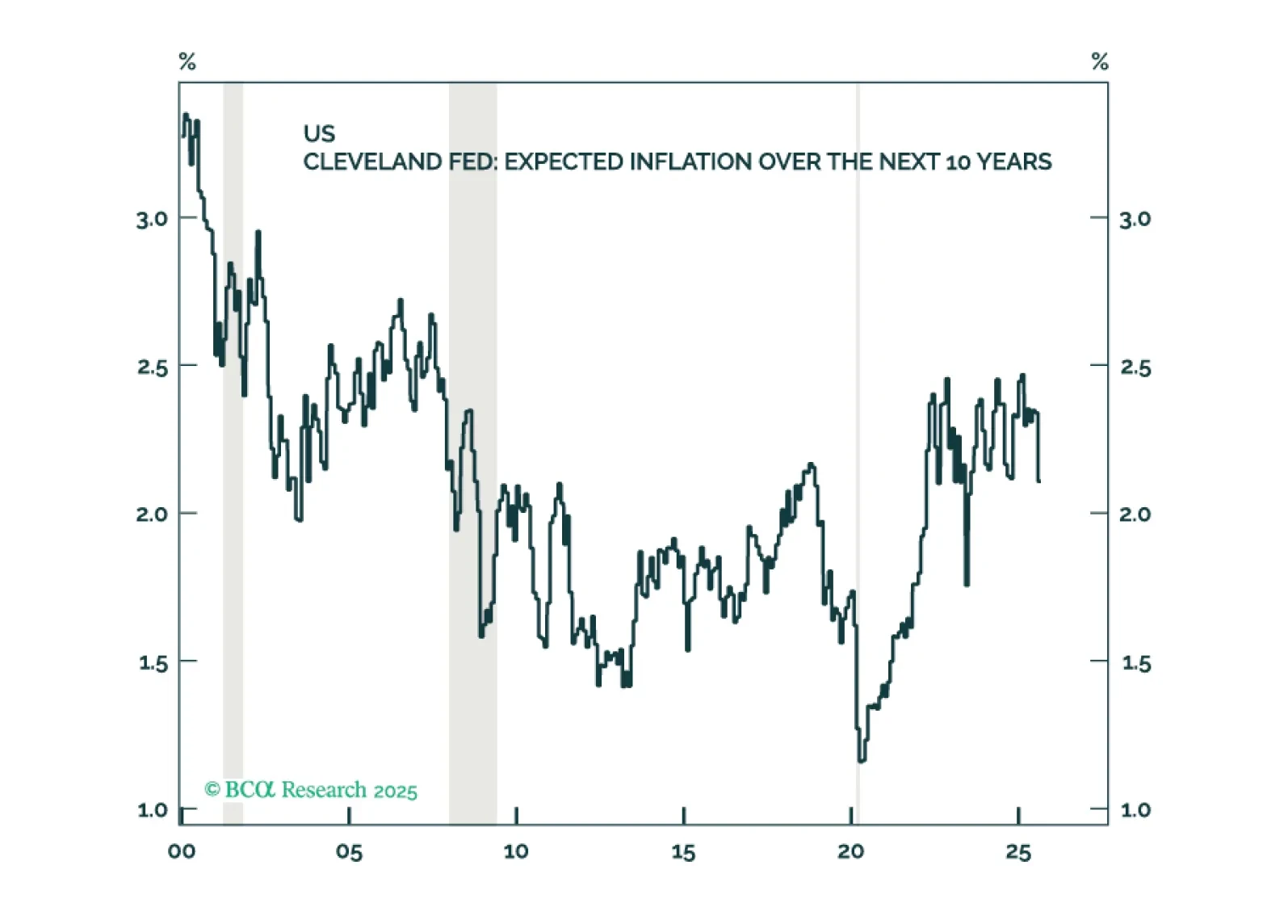

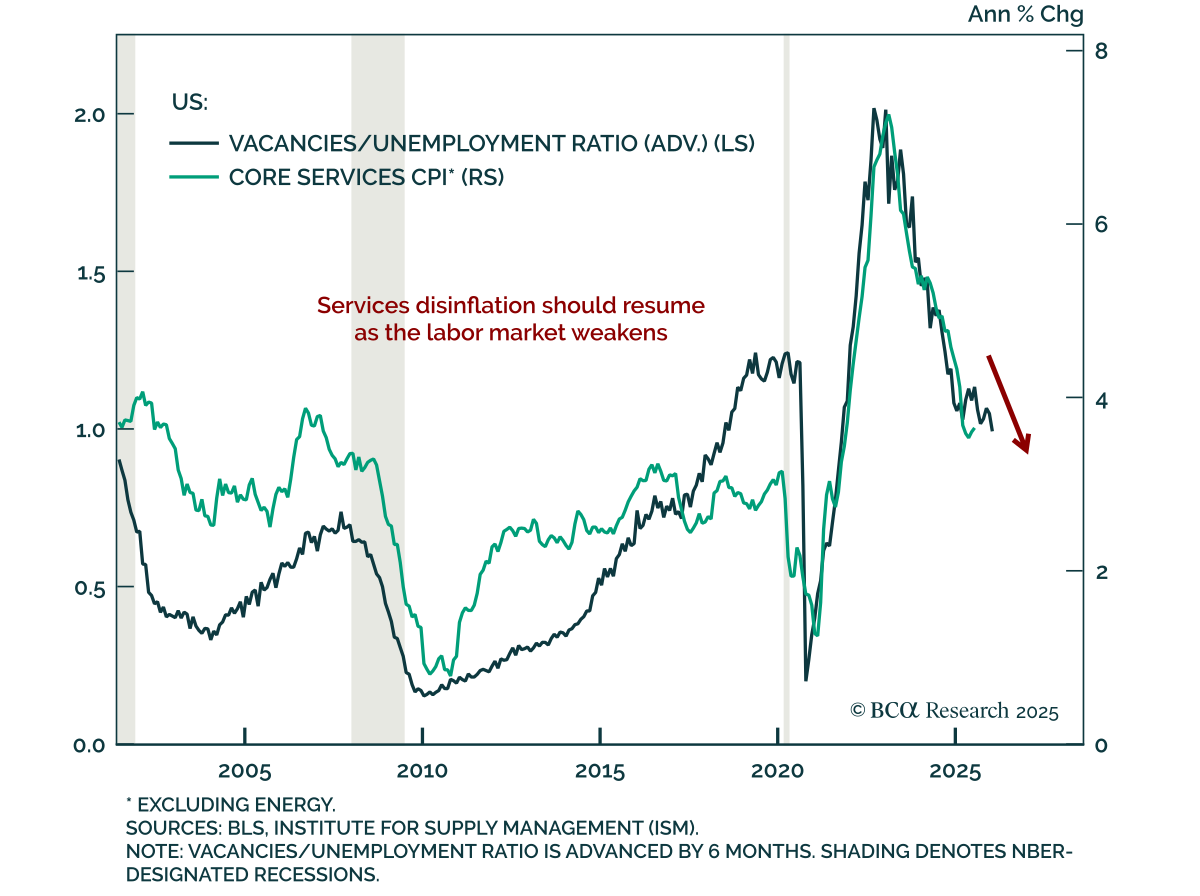

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

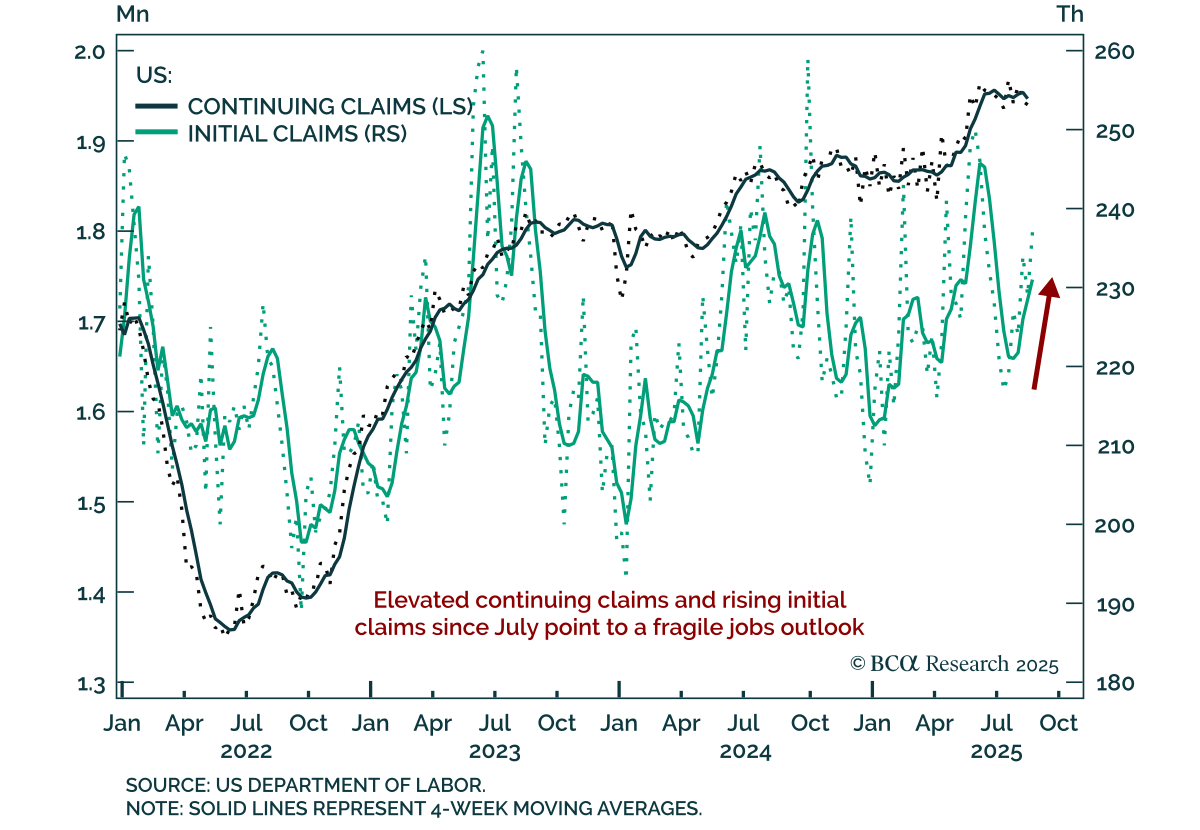

US jobless claims rose to 237k, the highest since July, underscoring fragile labor momentum. While still below the recent 250k peak, claims have been rising steadily since early July, suggesting the labor market weakness seen in the July employment…

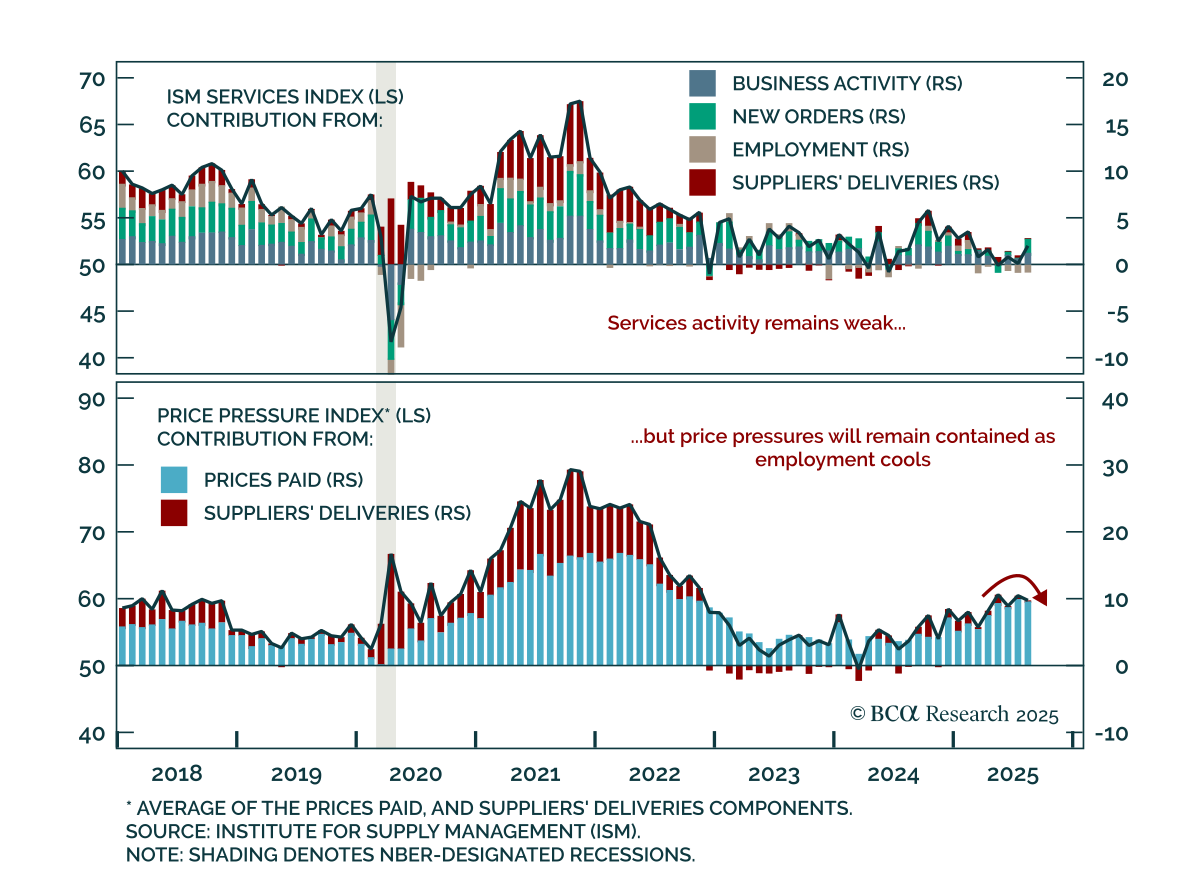

August ISM Services beat expectations, but employment weakness highlights fragile momentum. The index rose to 52.0 from 50.1, driven by business activity and new orders. However, the employment component stayed in contraction at 46.5. Inflation signals…

US job openings fell to a 10-month low in July, underscoring continued labor market weakening. Openings declined to 7.18m from 7.36m. The decline was led by non-cyclical sectors such as education and health services, which had recently been drivers of…

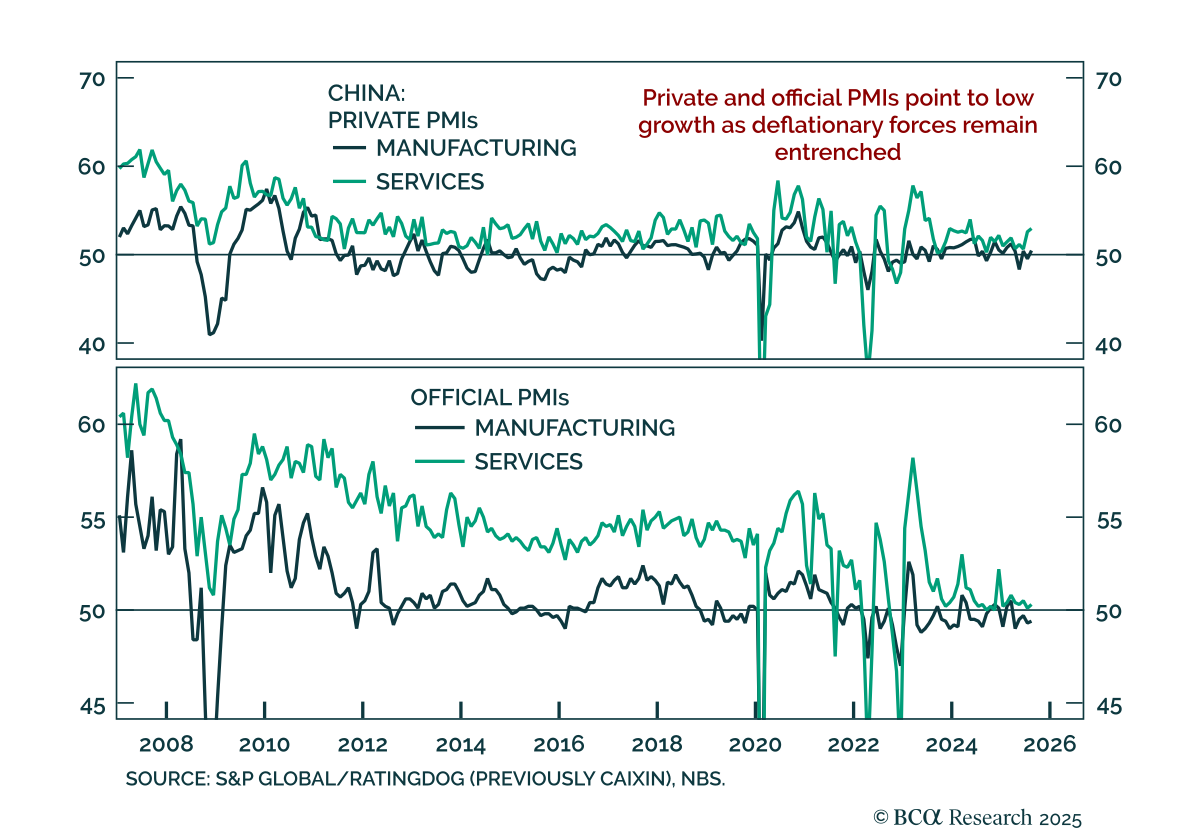

China’s August PMIs improved, but underlying data point to persistent weakness and limited momentum. The official NBS composite rose to 50.5 from 50.2, with manufacturing still in contraction at 49.4 and services edging higher to 50.3. Private PMIs showed…

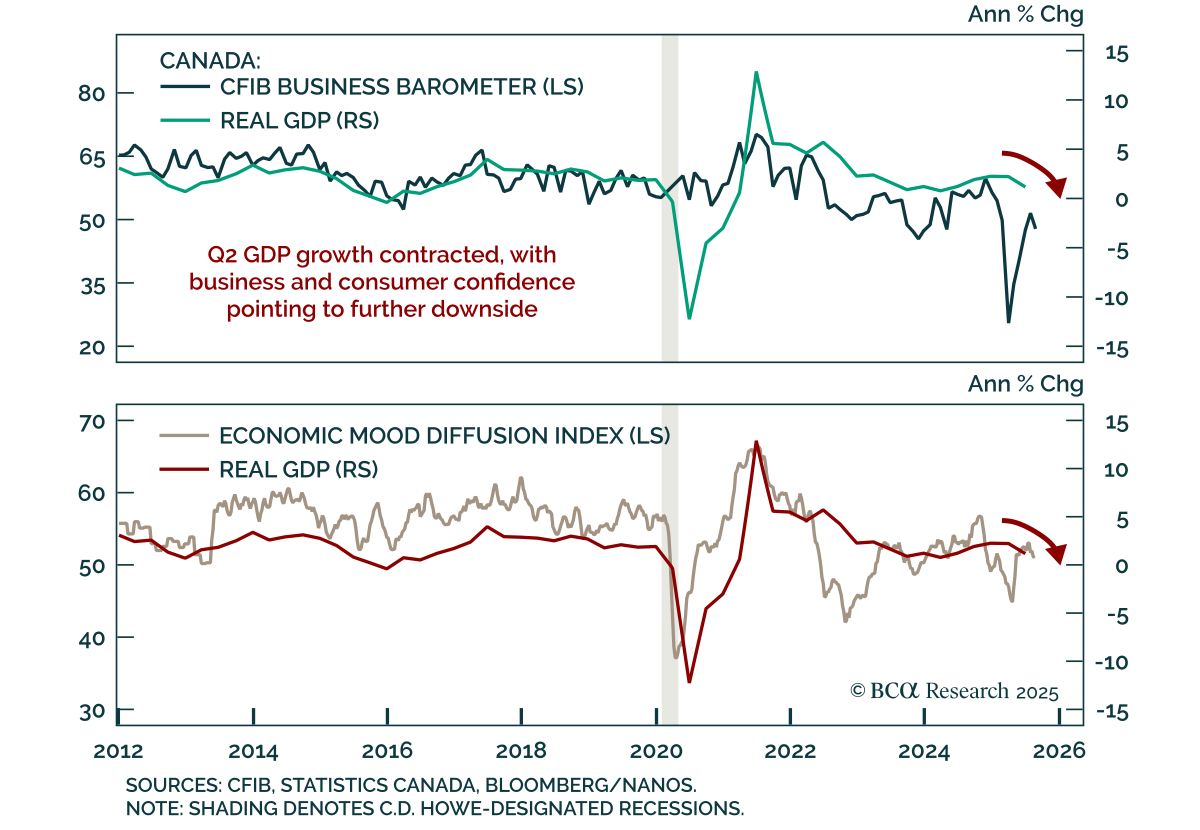

Canada’s Q2 GDP contraction underscores a fragile backdrop where growth risks will outweigh inflation, supporting further BoC easing. Real GDP contracted at an annualized 1.6% after expanding 2.2% in Q1, consistent with survey data showing weaker confidence…

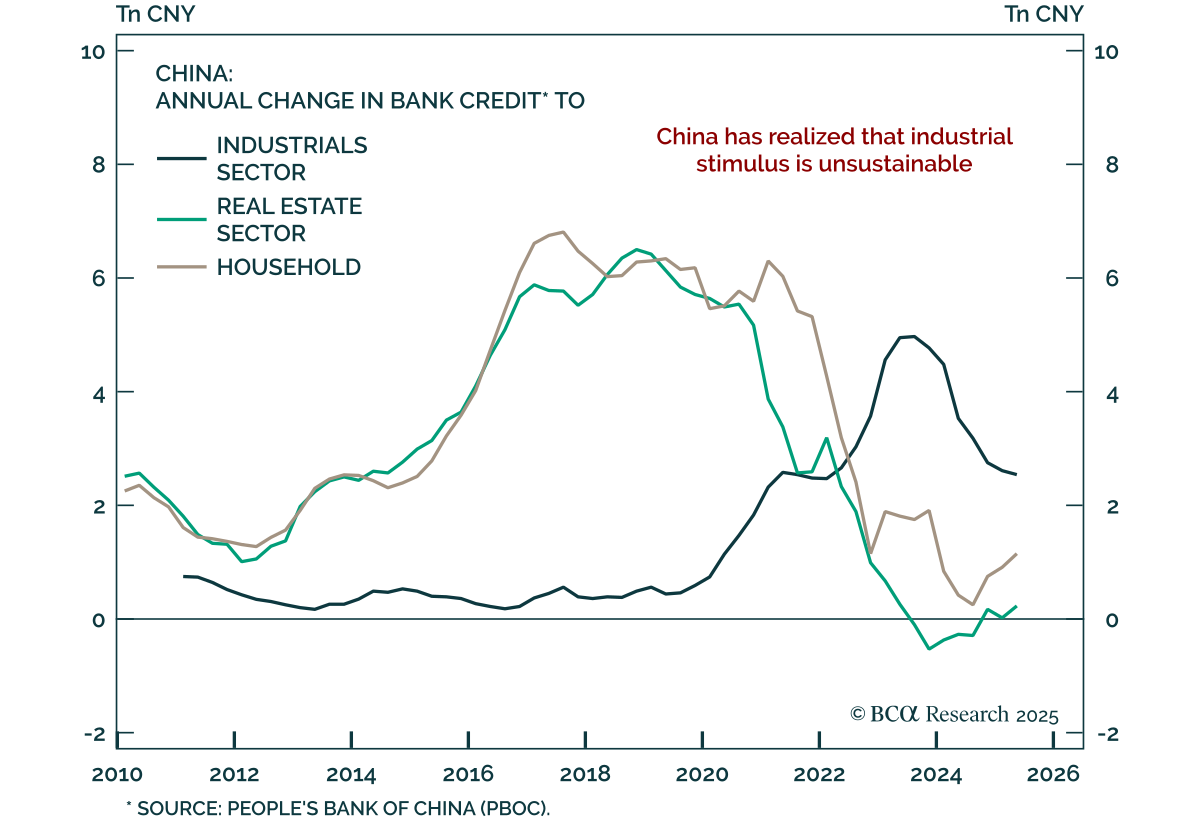

Our Global Asset Allocation strategists upgrade the Chinese yuan to overweight as global imbalances between production and consumption begin to reverse. The US continues to overconsume and underproduce, while China overproduces and underconsumes. Early signs…

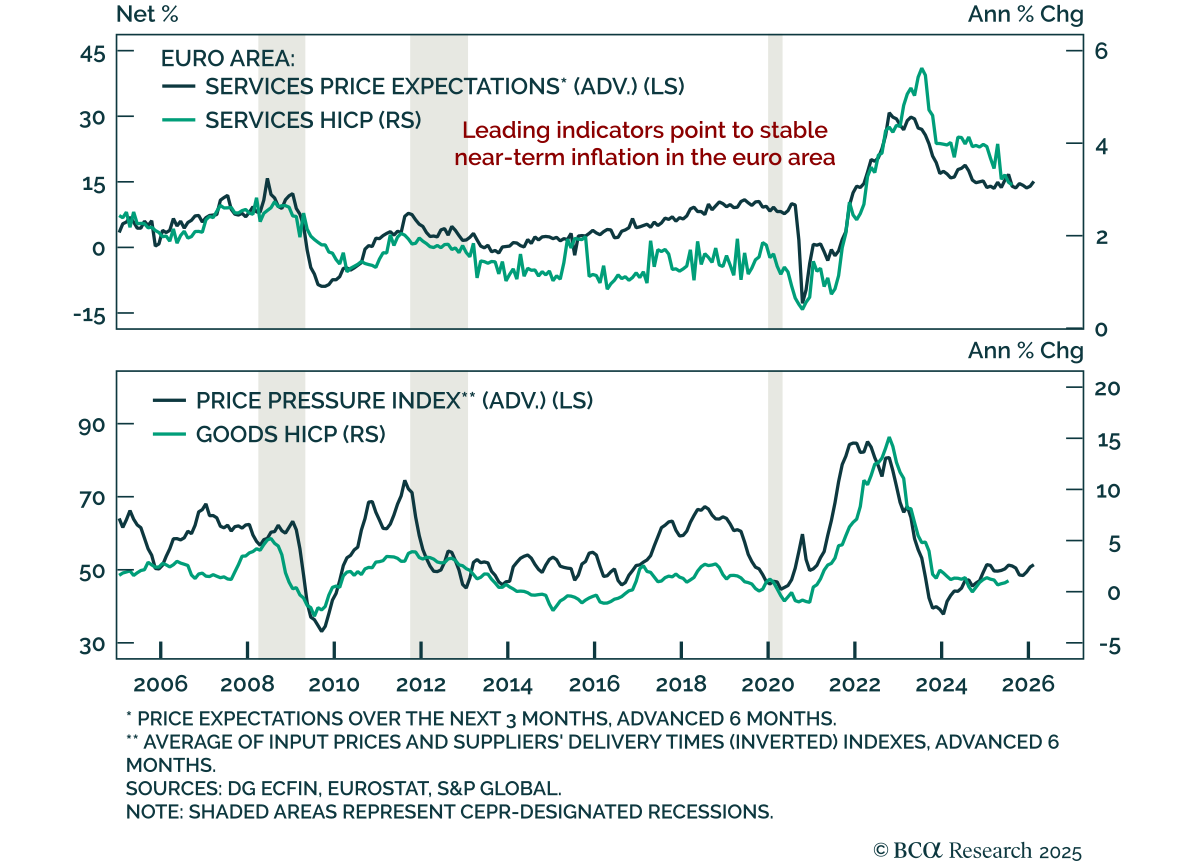

Euro area August flash HICP was slightly hotter than expected, reinforcing the case for the ECB to stay put in September. Headline inflation rose to 2.1% y/y from 2.0%, with the monthly print surprising at 0.2% m/m. Core inflation held at 2.3% y/y despite…