Currencies

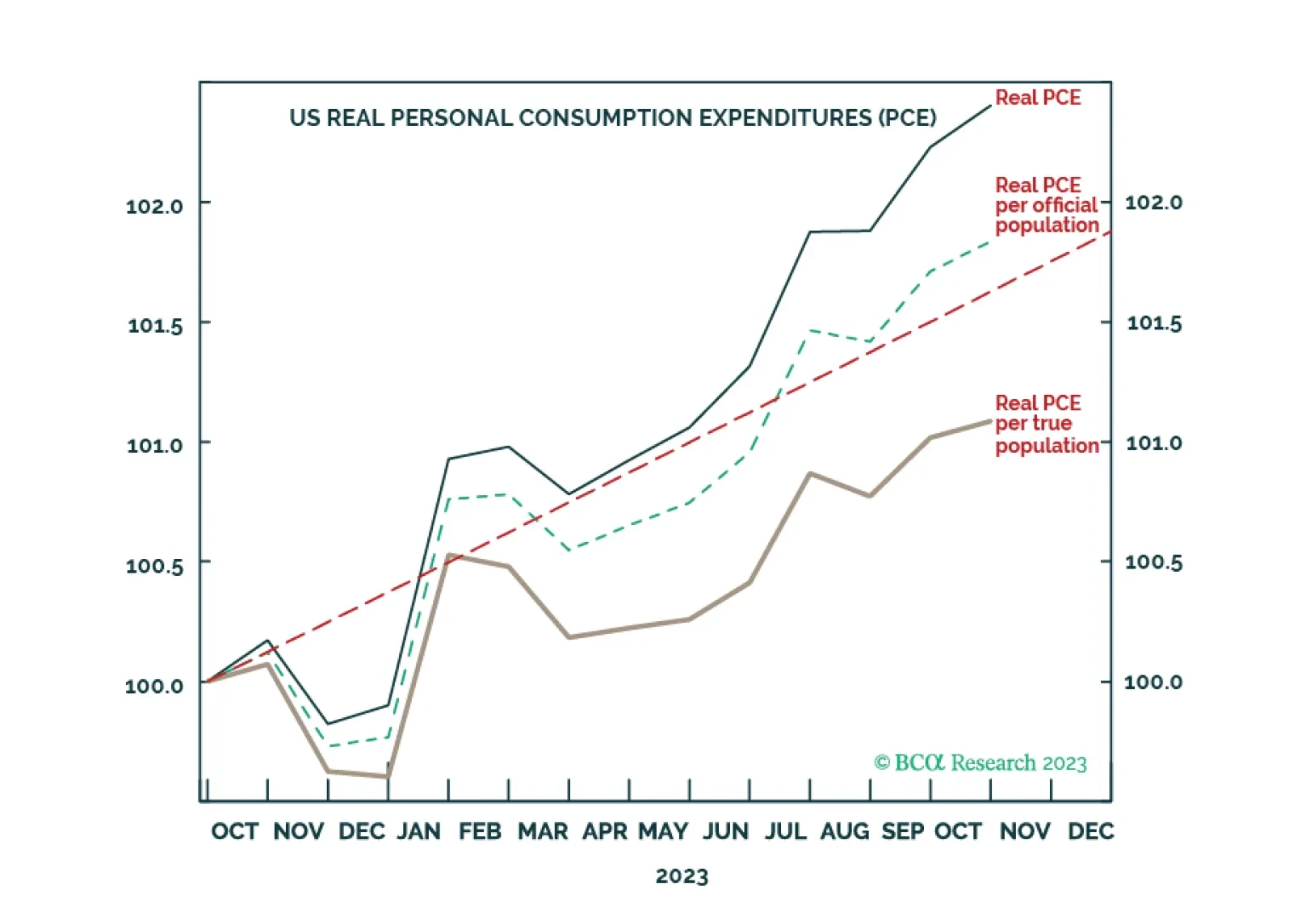

Illegal immigration into the US has skyrocketed to record levels. Correctly accounting for this, US real consumption growth on a per head basis is already fragile. Meanwhile, the real bond yield is only now approaching the pain point that typically triggers a recession. Ahead of the upcoming US jobs report, we point out what it would take for the Joshi rule real-time US recession indicator to breach its event horizon. And how to position in stocks and bonds, both tactically and cyclically. Plus: potential turning points in Biotech and Genome, ADBE, and Taiwan versus China.

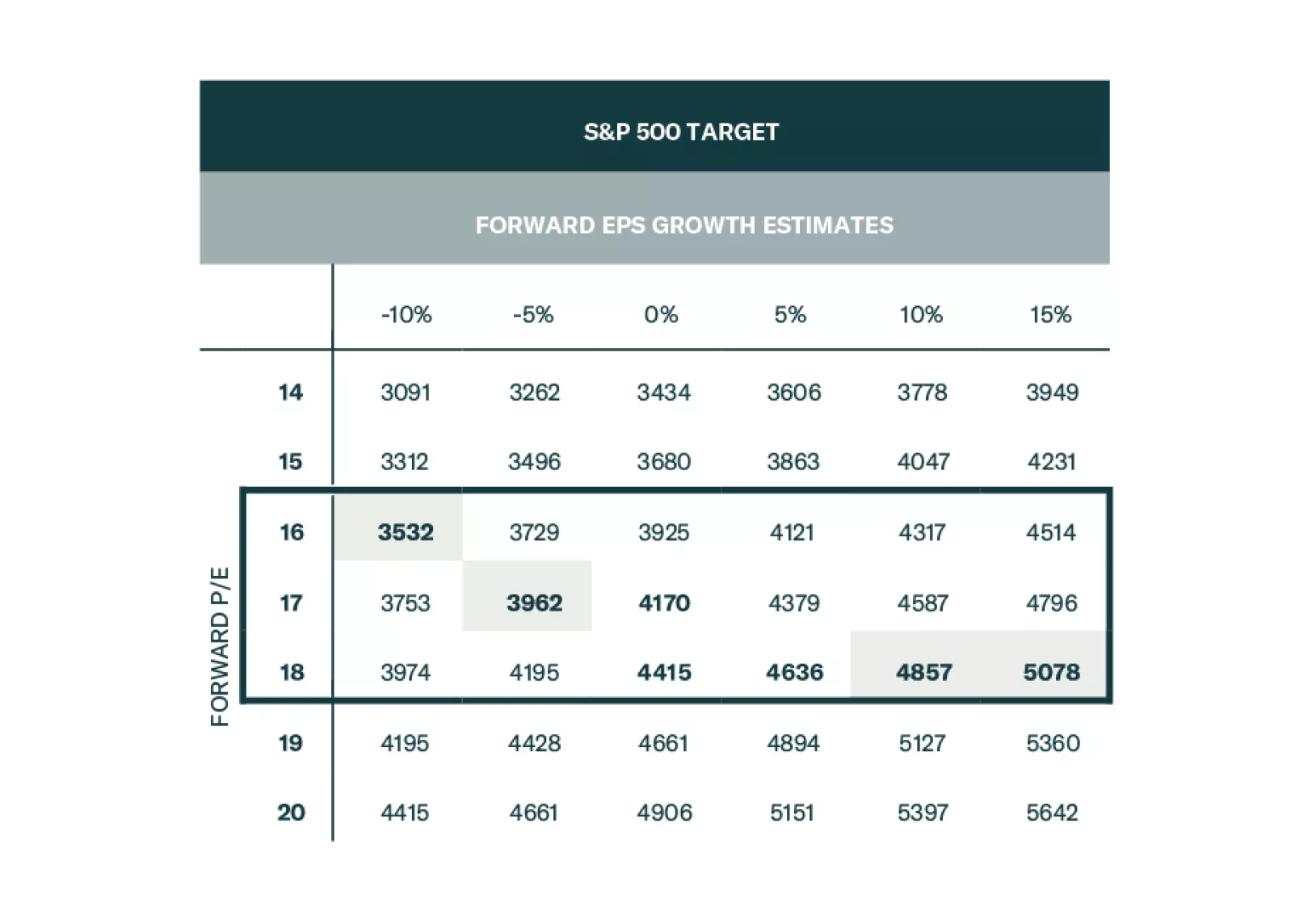

We expect the US economy to slow and potentially downshift into a recession sometime in 2024, as tighter monetary policy weighs on consumers and businesses. In addition, (geo)political tensions may increase market volatility. The risk/return for US equities is unfavorable. We recommend that our clients reduce portfolio beta and increase allocations to defensives and quality growth.

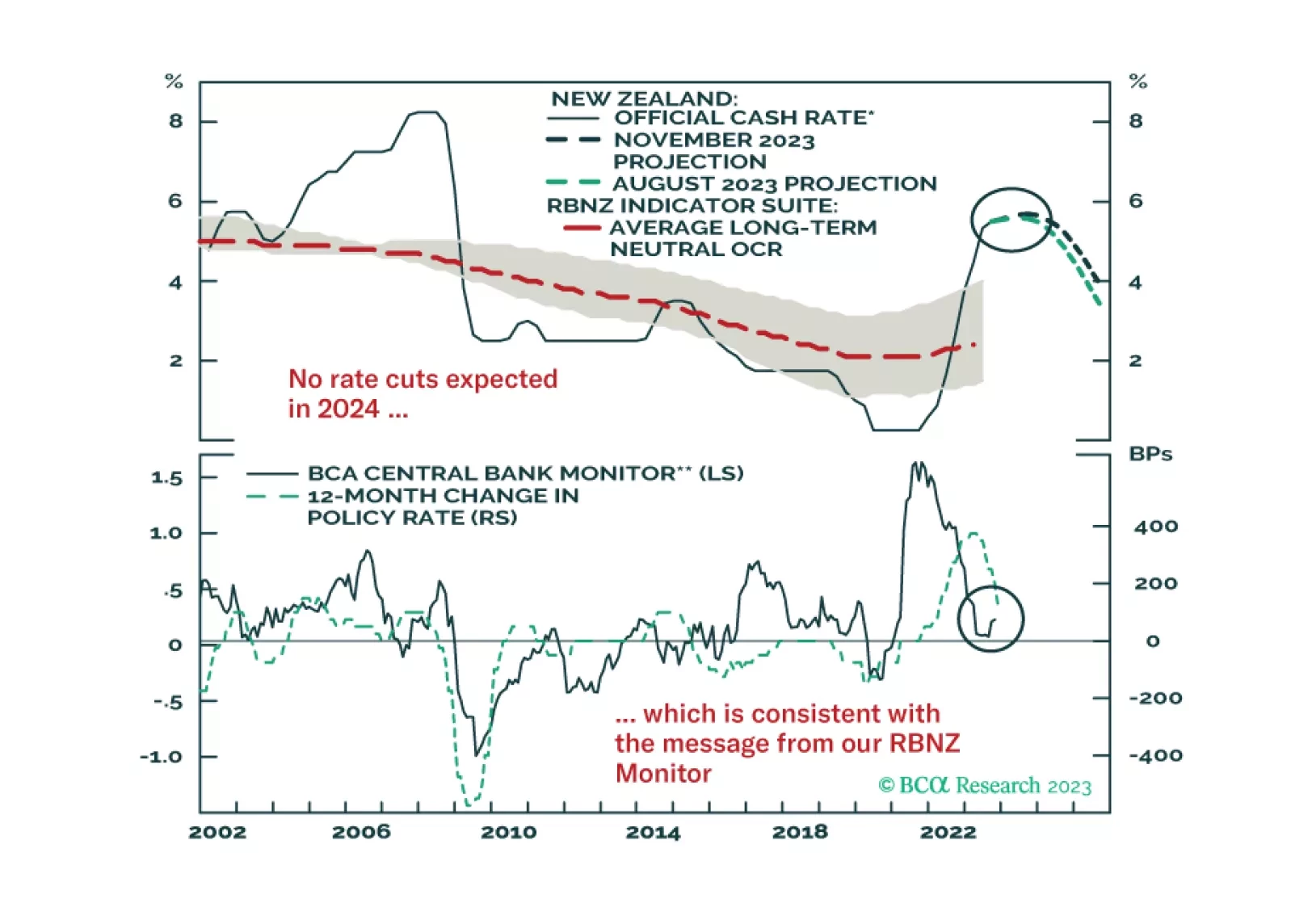

In this Insight, we discuss the outlook for monetary policy in New Zealand after this week’s RBNZ policy meeting, and introduce related fixed income and currency trade ideas.

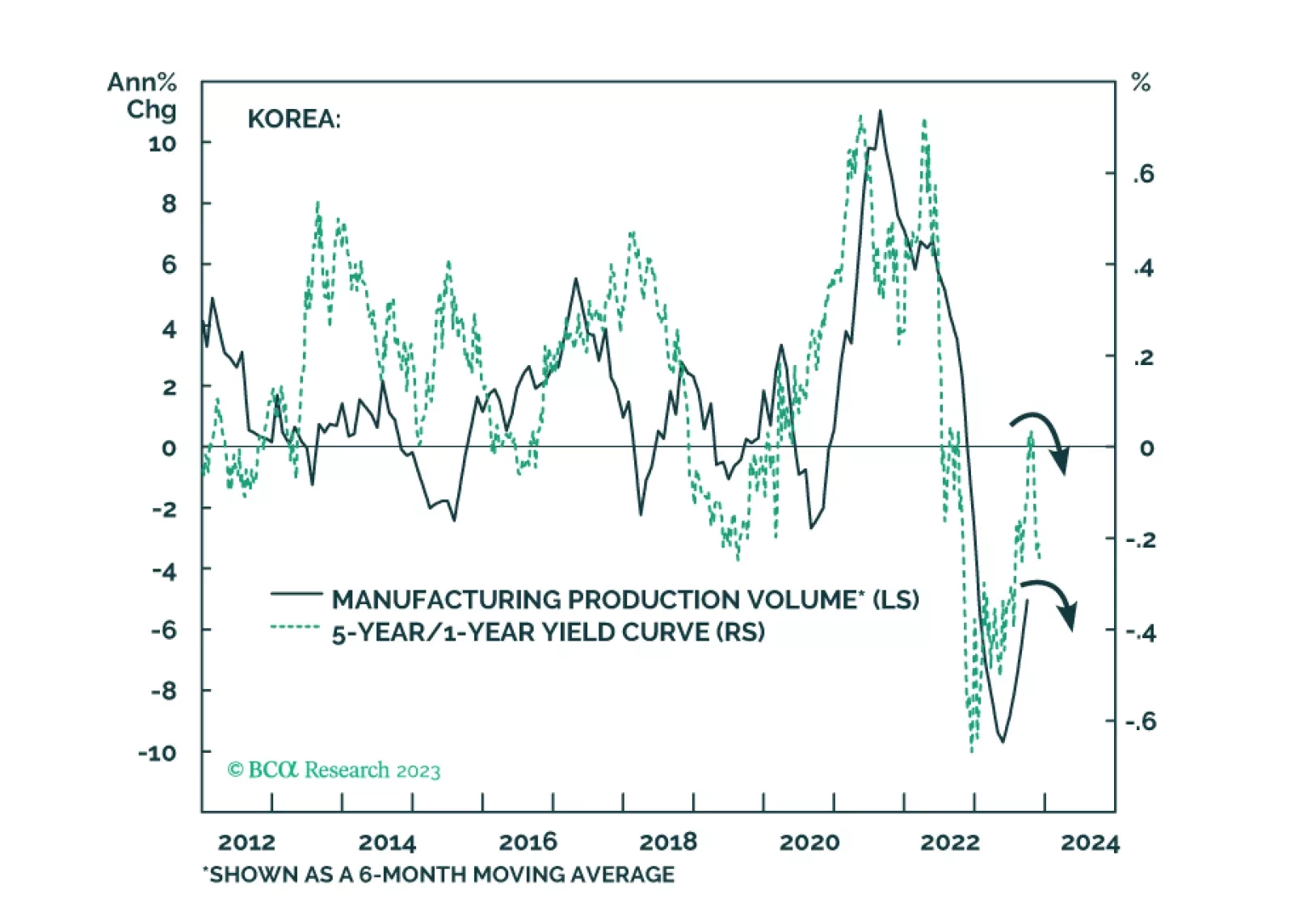

The recent increase in Korean exports will likely prove to be a mid-cycle rebound within a cyclical downtrend. Korea’s households and enterprises are among the most indebted globally, and their debt service ratio is among the highest in the world. Korea’s 10-year bond yields have peaked. We discuss opportunities in Korean stocks as well as in fixed income and currency markets.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

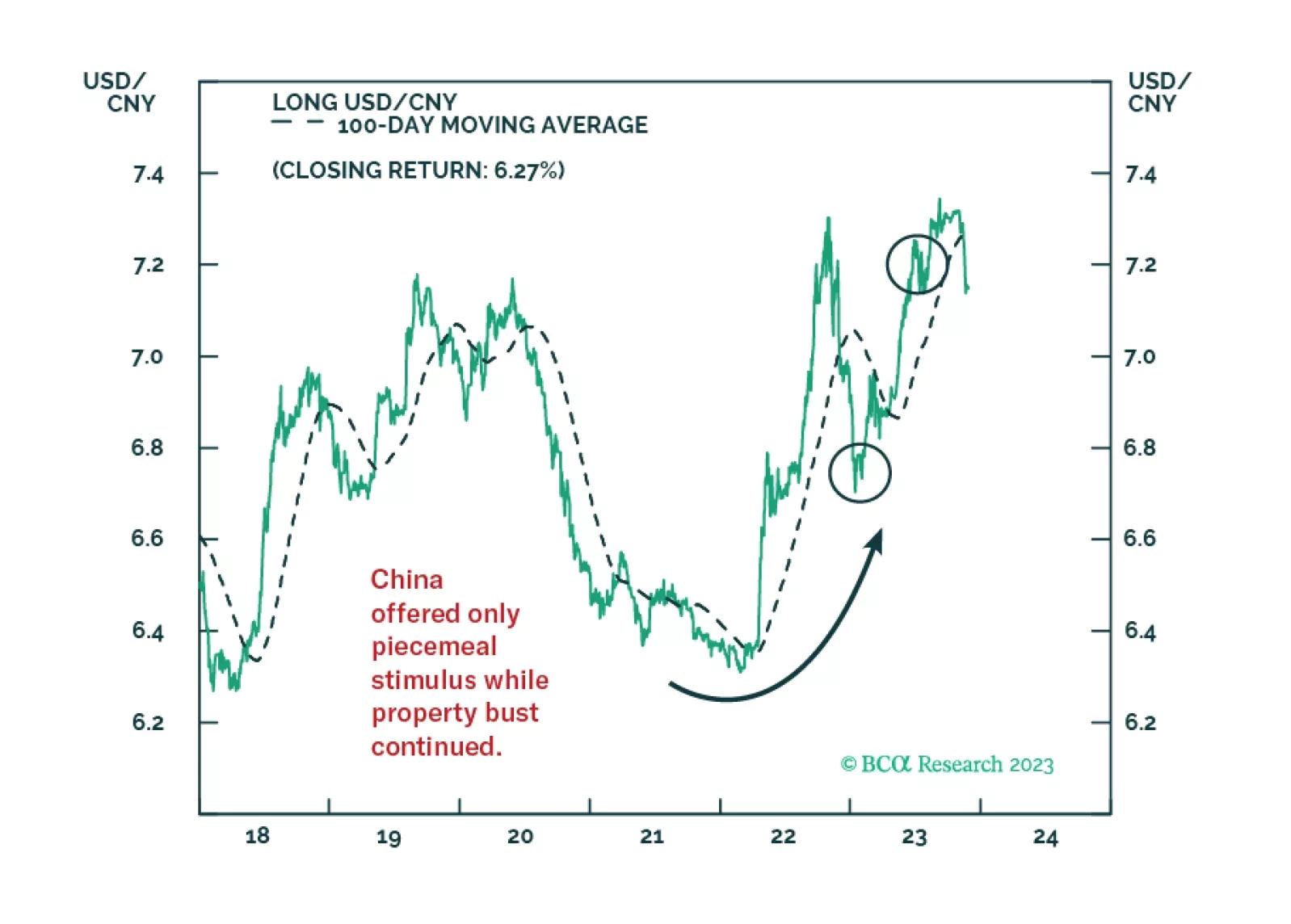

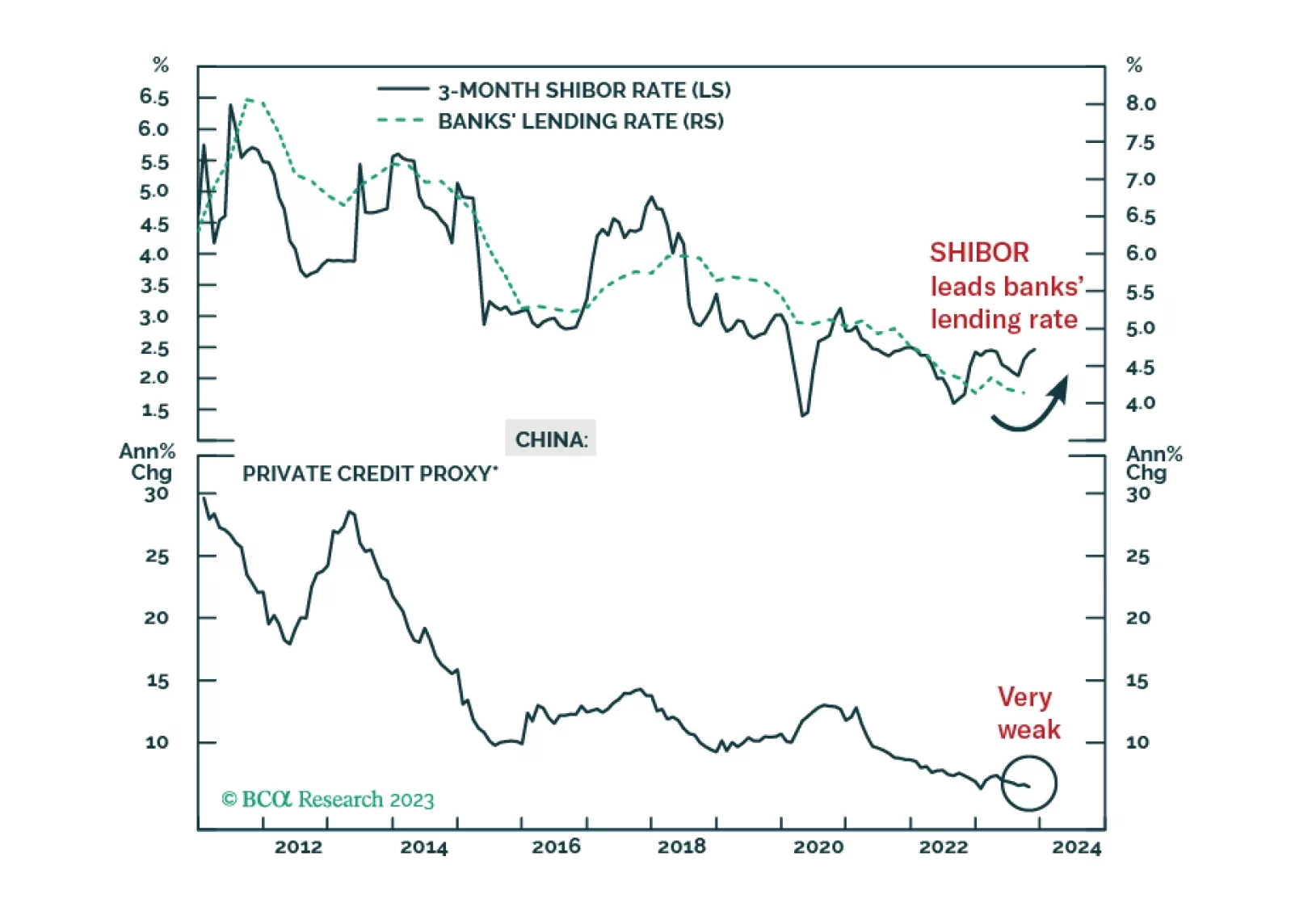

A cyclical recovery in China’s economy is still not imminent. The PBoC has tightened interbank liquidity to stabilize the exchange rate since late August. This does not bode well for the real economy. The uptick in onshore bond yields and the RMB’s appreciation will be transient. Equity investors should stay cautious.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

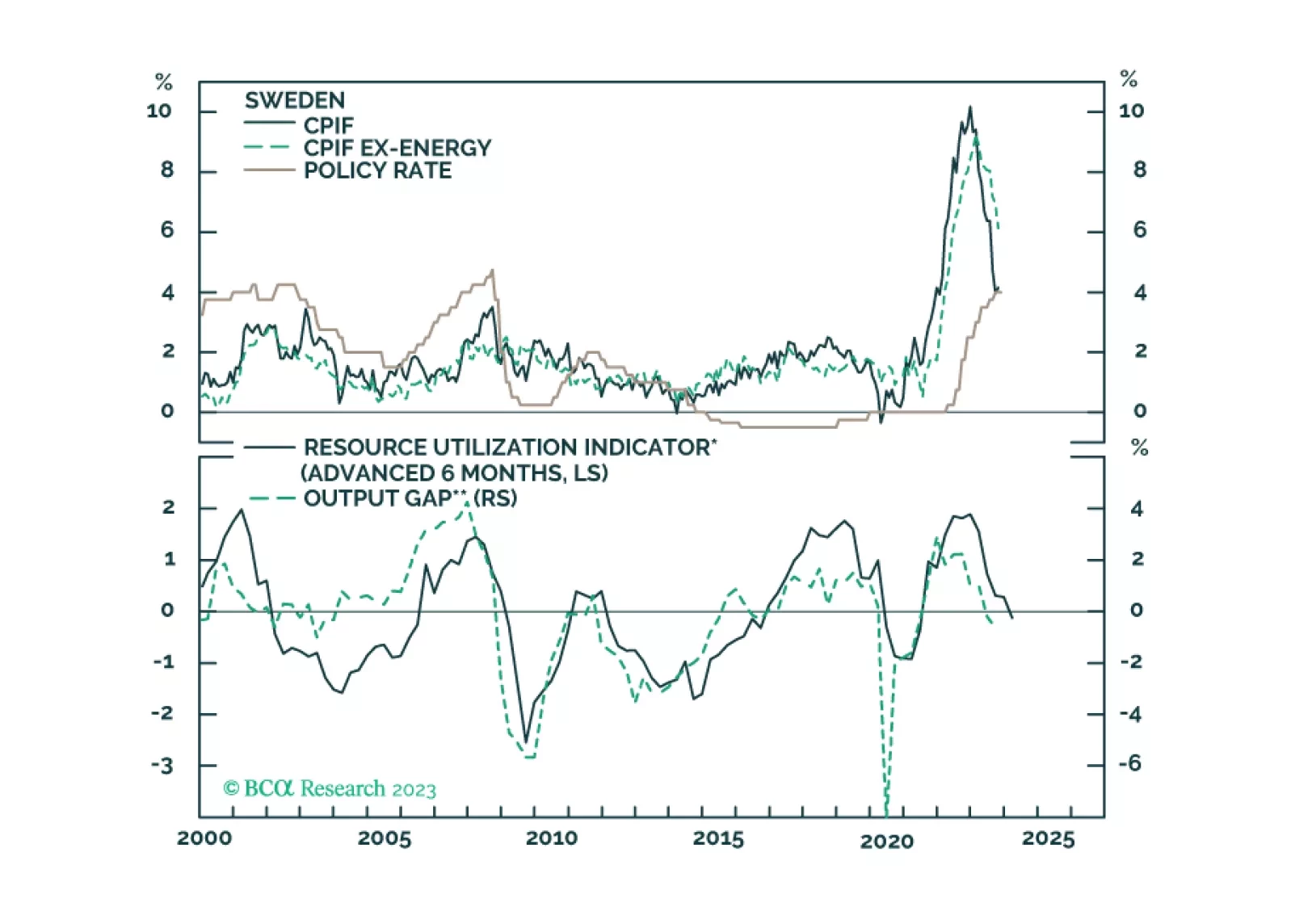

This report looks at the prospects for the Swedish krona, following the pause by the Riksbank.