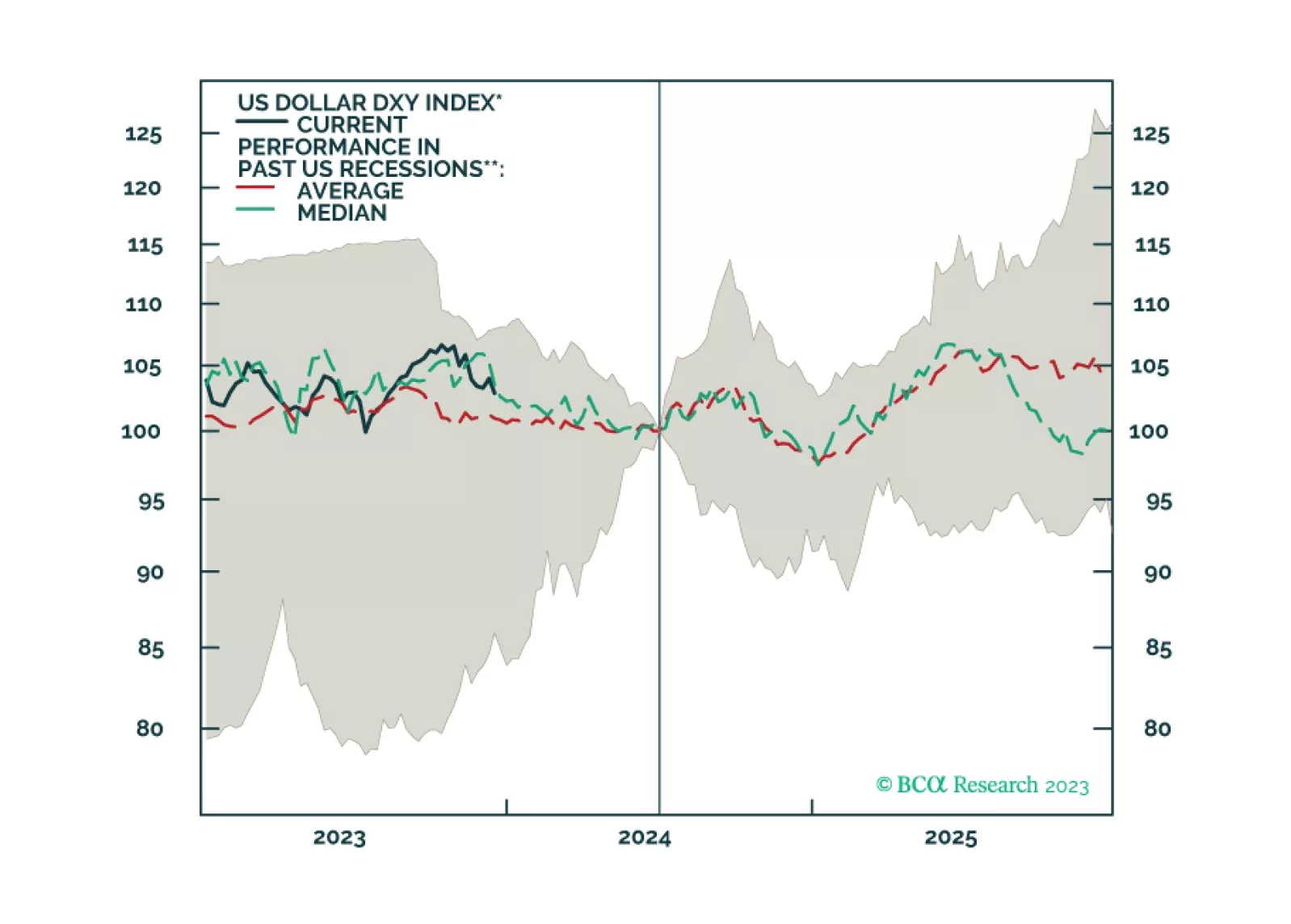

Currencies

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

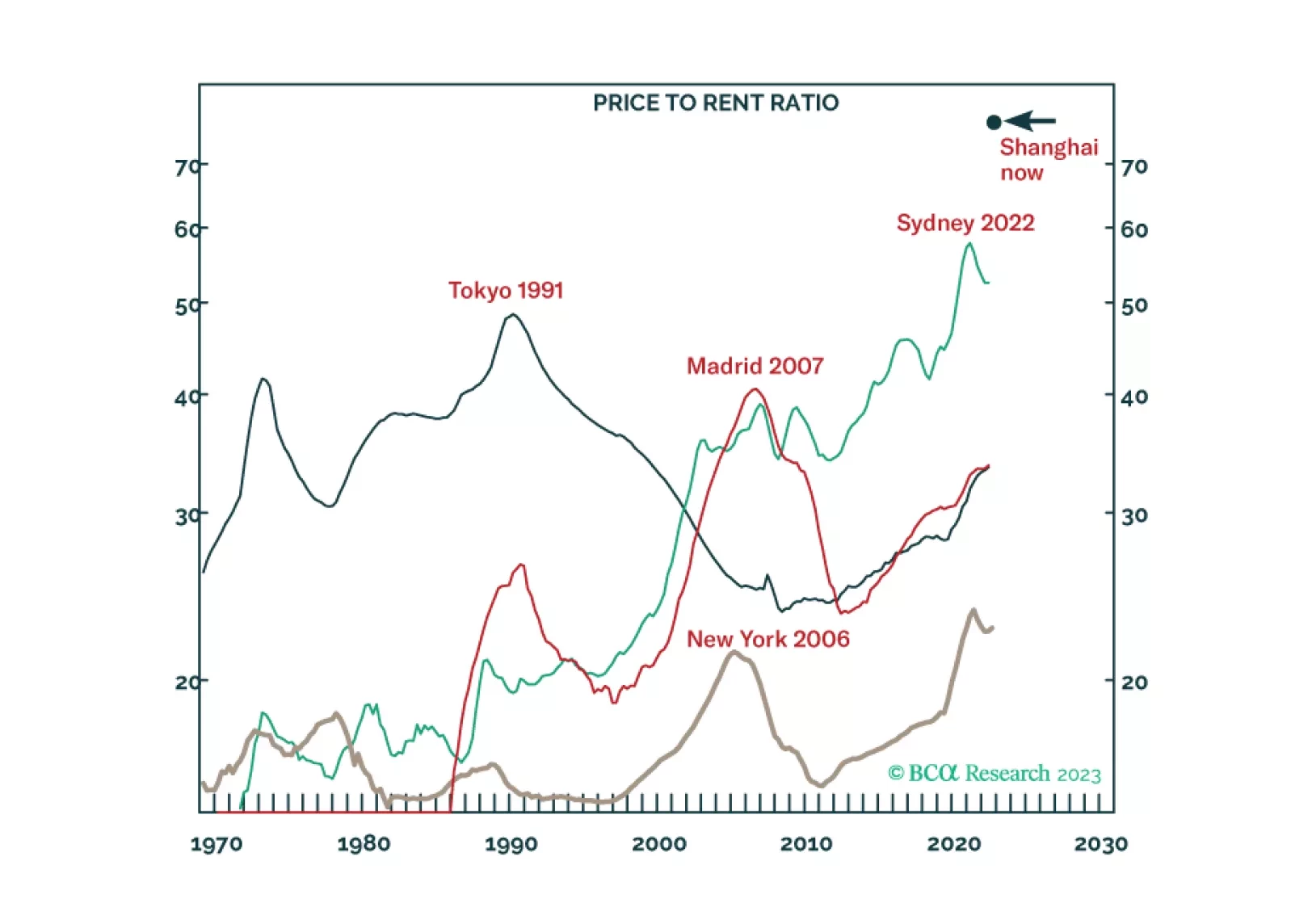

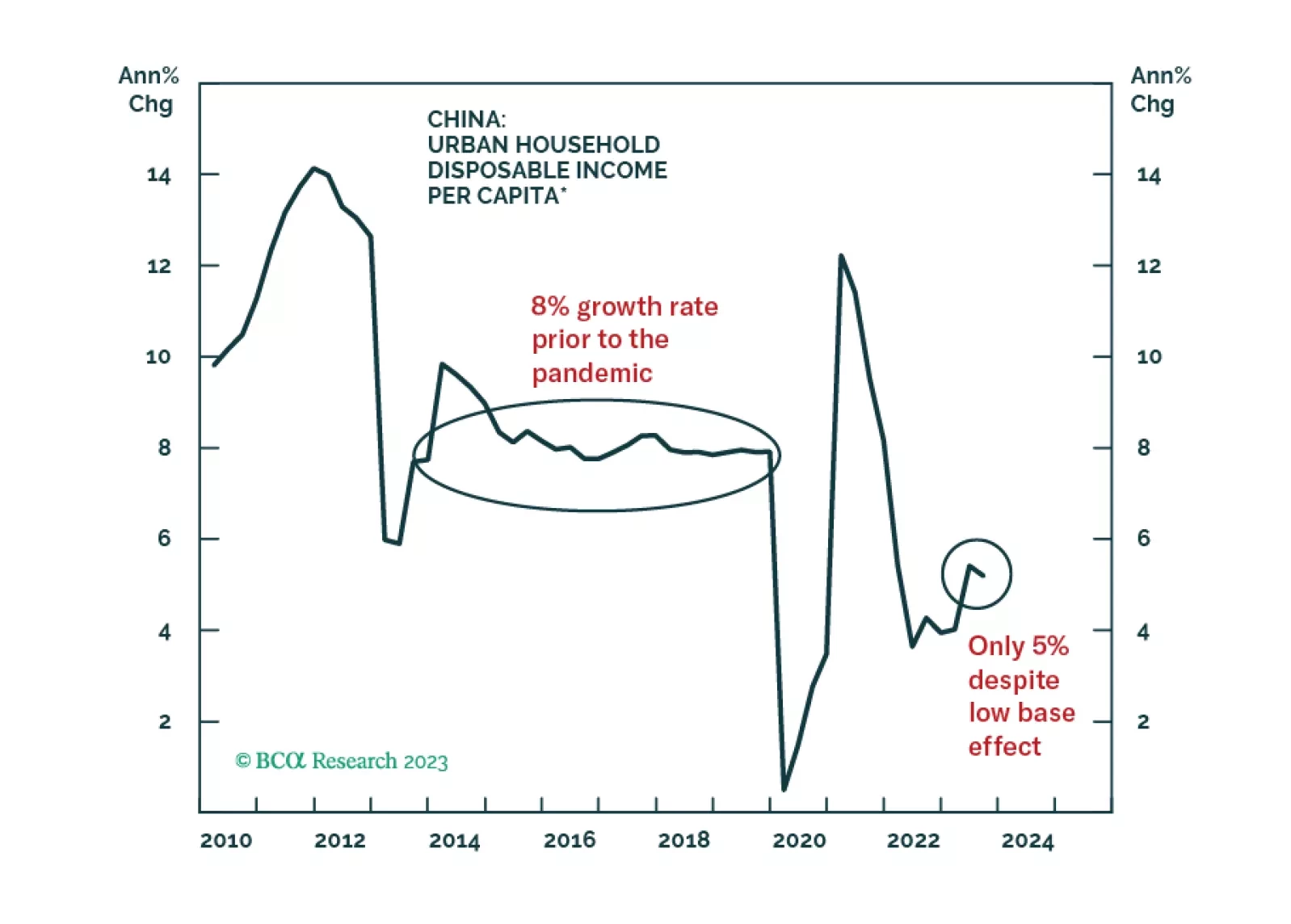

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

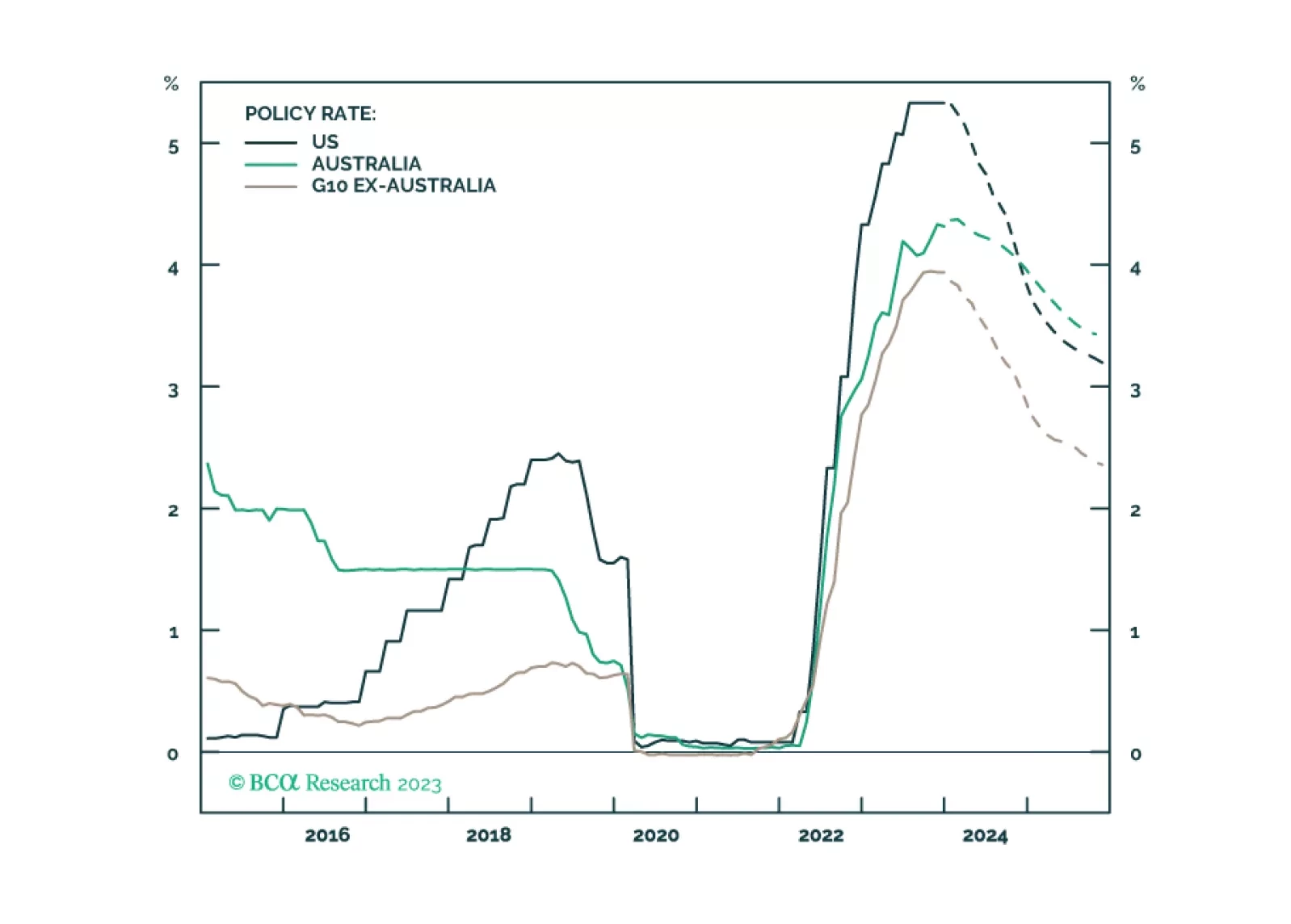

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.