Fixed Income

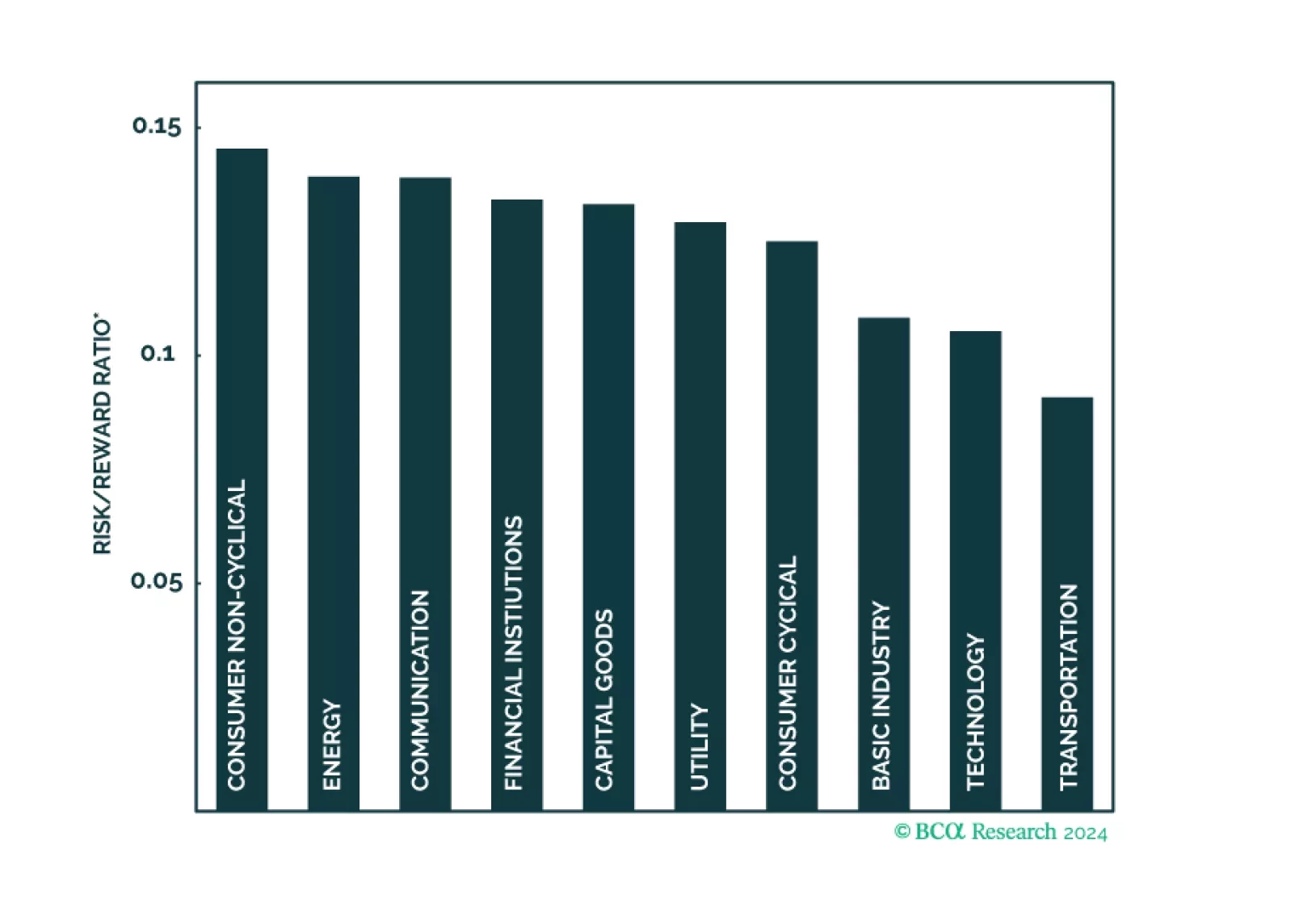

We expand our risk/reward analysis of US investment grade corporate bonds to focus on the 44 industry groups included in the Bloomberg index.

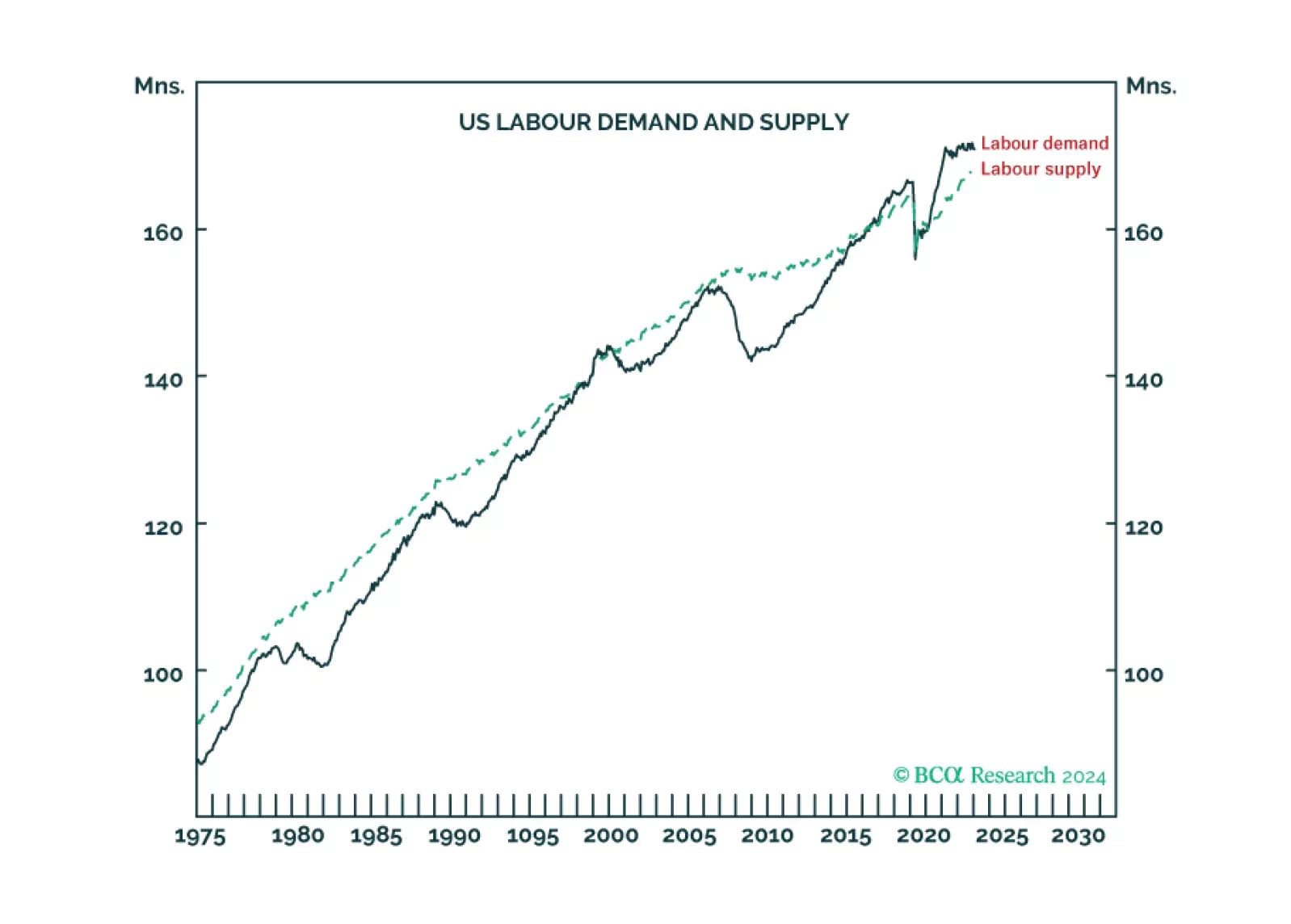

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and asset allocation. Plus: NVDA is at a consolidation point.

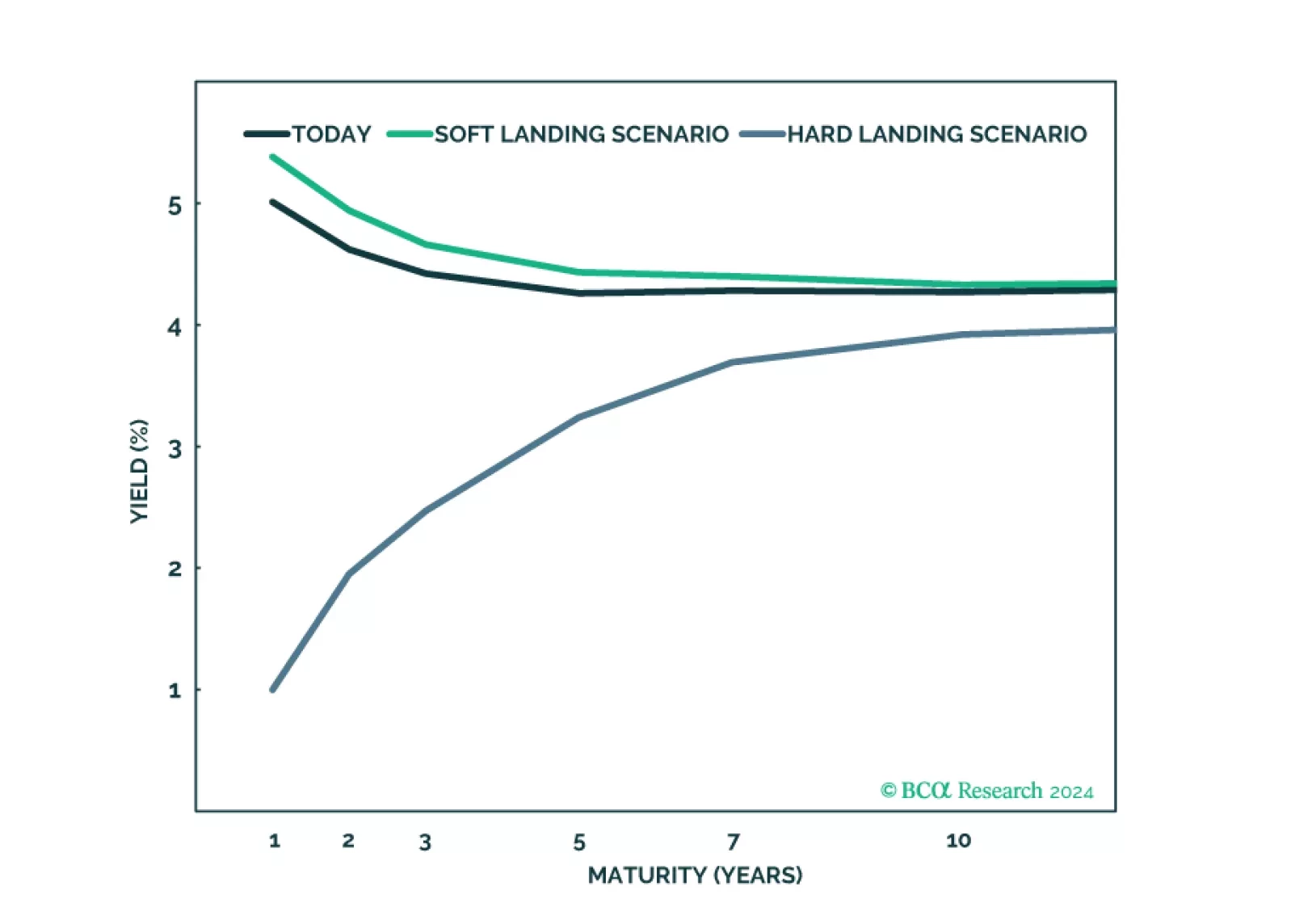

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

In this Insight, we continue our series of reports outlining investment frameworks for inflation-linked bonds in the developed markets, this time focusing on Japan. Our Japanese Inflation-Linked Golden Rule suggests that investors should overweight Japanese inflation-linked bonds versus nominal JGBs on a strategic (6-12 month) investment horizon. Our new Japanese inflation models suggest that there is a material risk that Japanese inflation exceeds the current level of market-based inflation expectations over the next year.

A risk/reward ranking of the 10 major US investment grade corporate bond sectors.

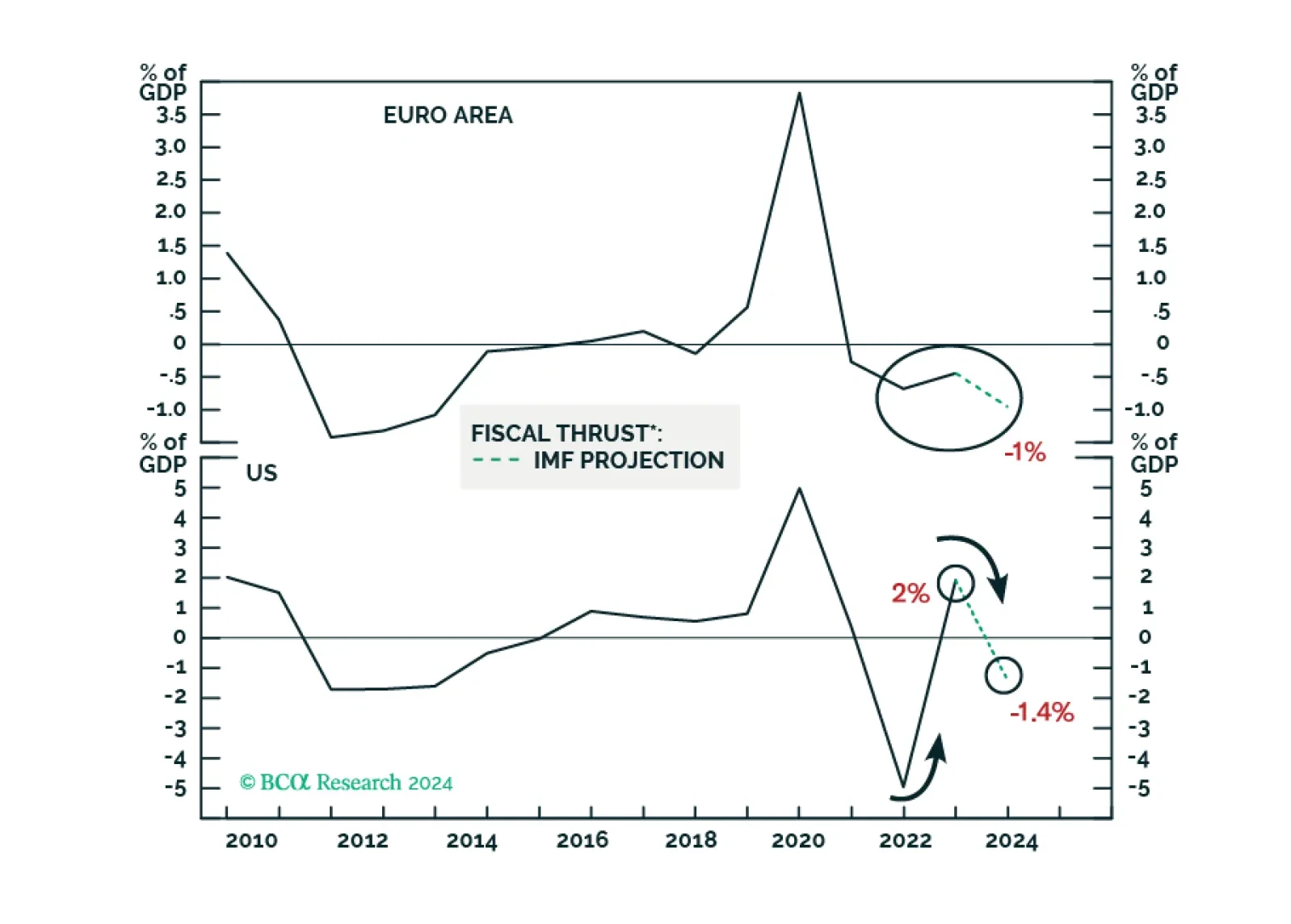

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

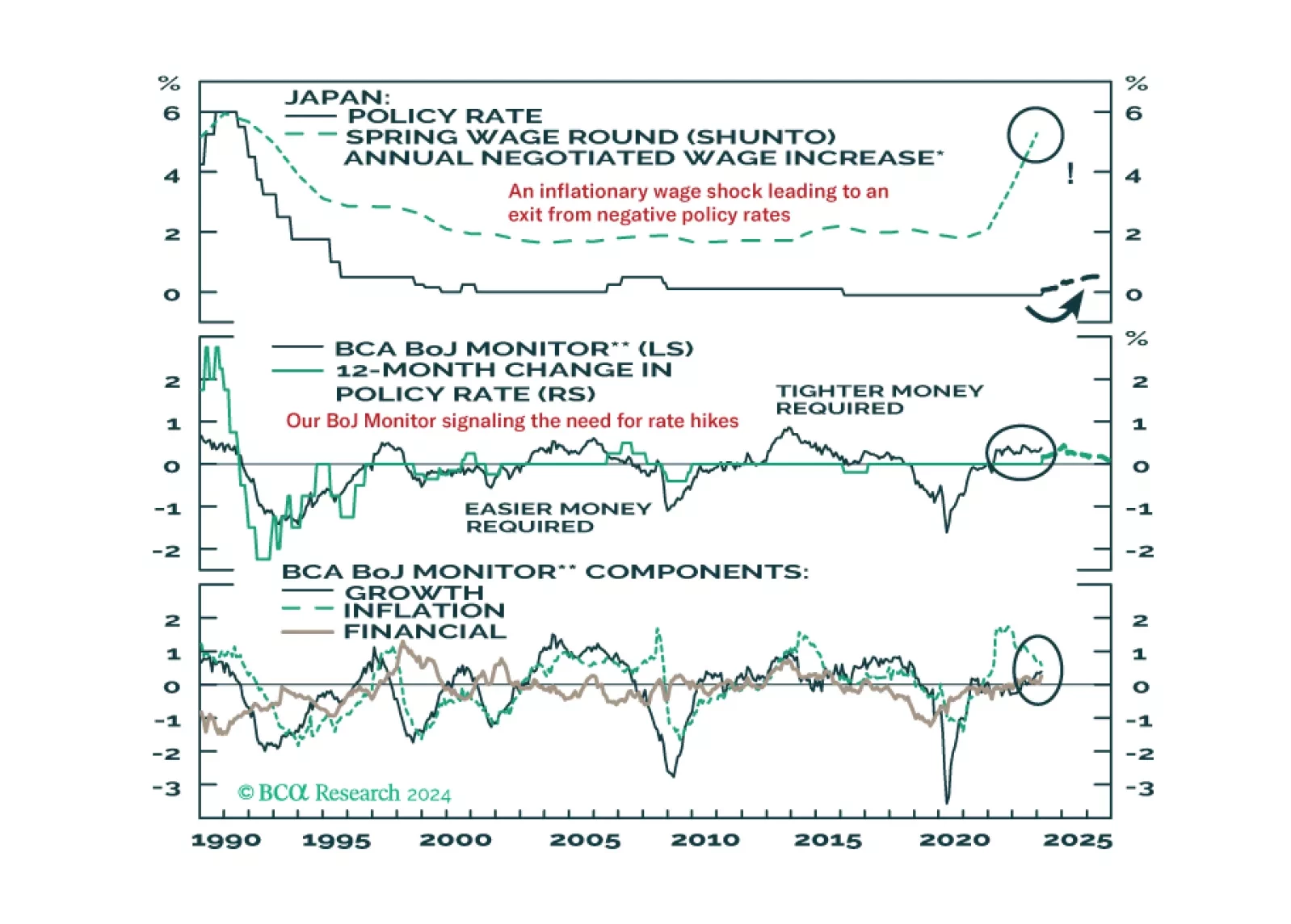

The Bank of Japan delivered a historic policy adjustment this week, ending both negative interest rates and Yield Curve Control. In this Insight, BCA’s global fixed income and currency strategists discuss the immediate implications of the move for Japanese bond yields and the yen, and the potential for additional tightening actions.