Commodities

In Section I, Doug compares projected S&P 500 earnings and current capex to past cycles at the same stage of their expansions while also exploring the K-shaped bifurcation in business investment. In Section II, Mathieu argues that Australia and Canada are unloved, undervalued, and on the cusp of a structural re-rating. Long-term investors who wait for the catalysts to become obvious will miss the entry point.

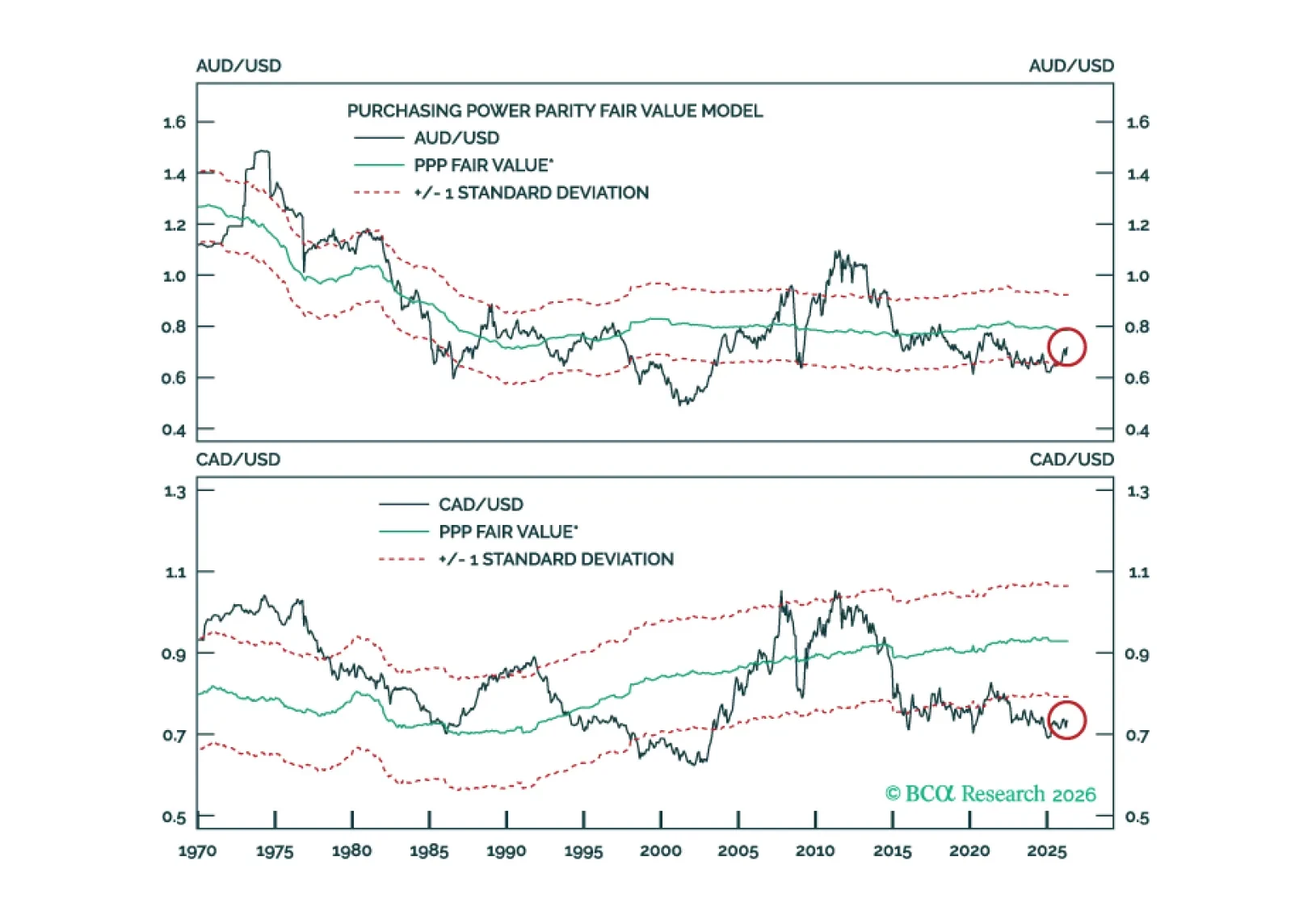

This Special Report argues that Australia and Canada are unloved, undervalued, and on the cusp of a structural re-rating. Long-term investors who wait for the catalysts to become obvious will miss the entry point.

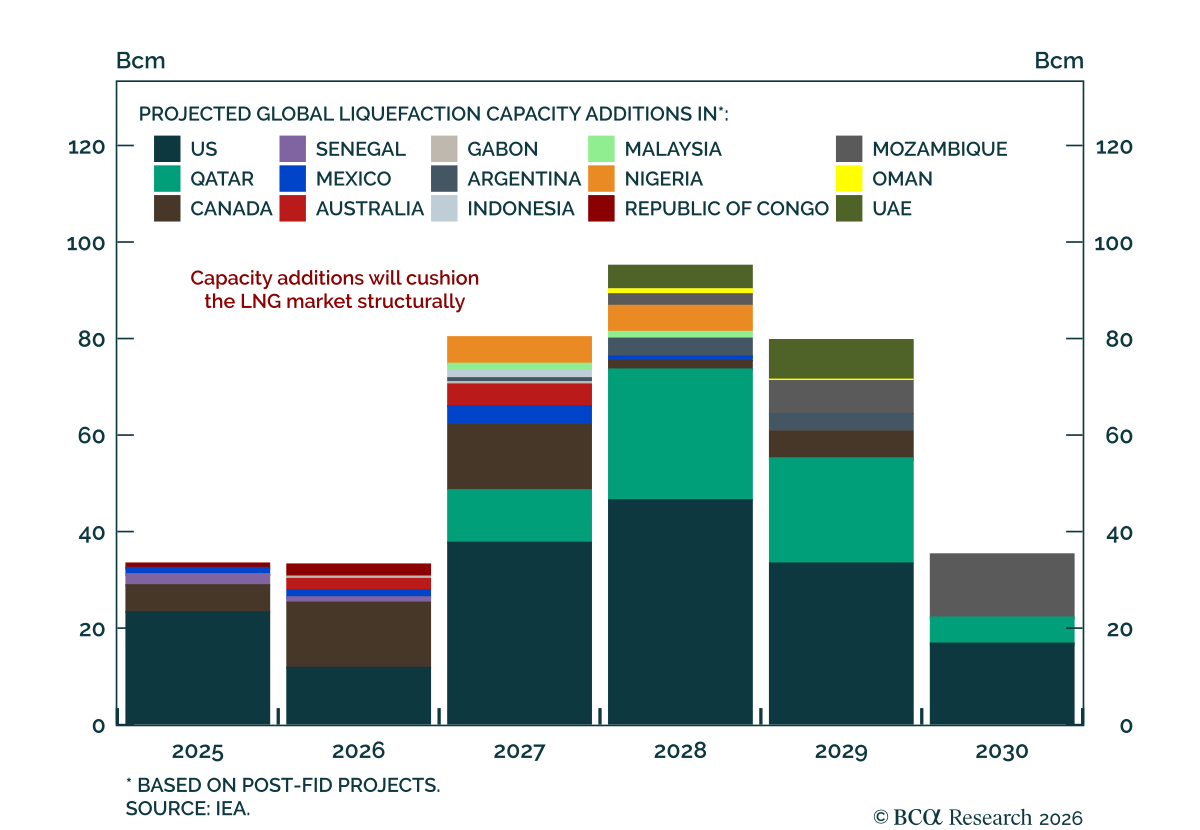

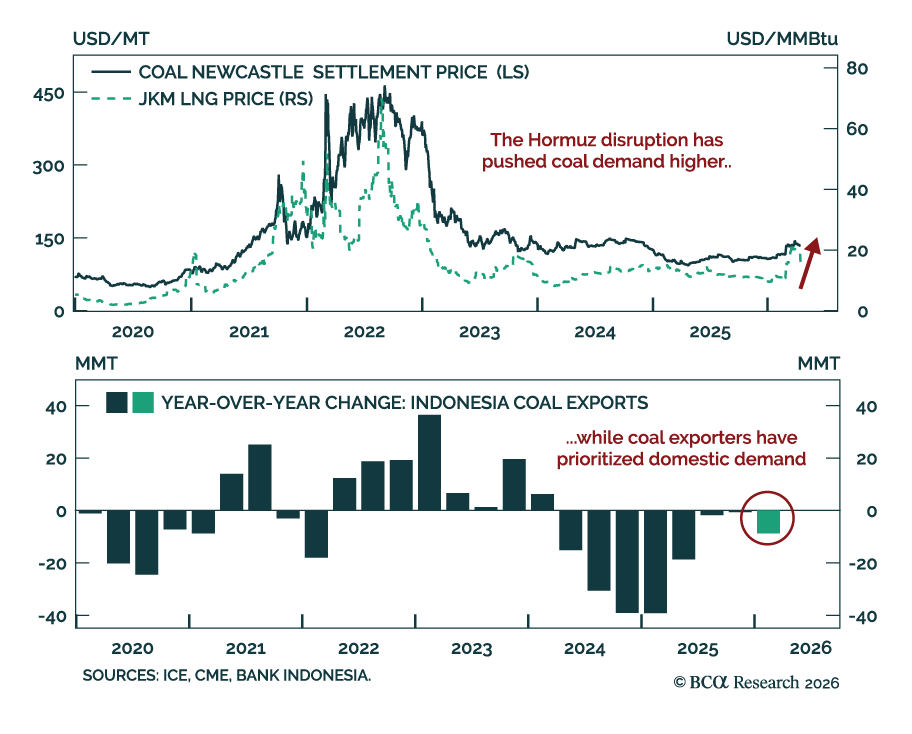

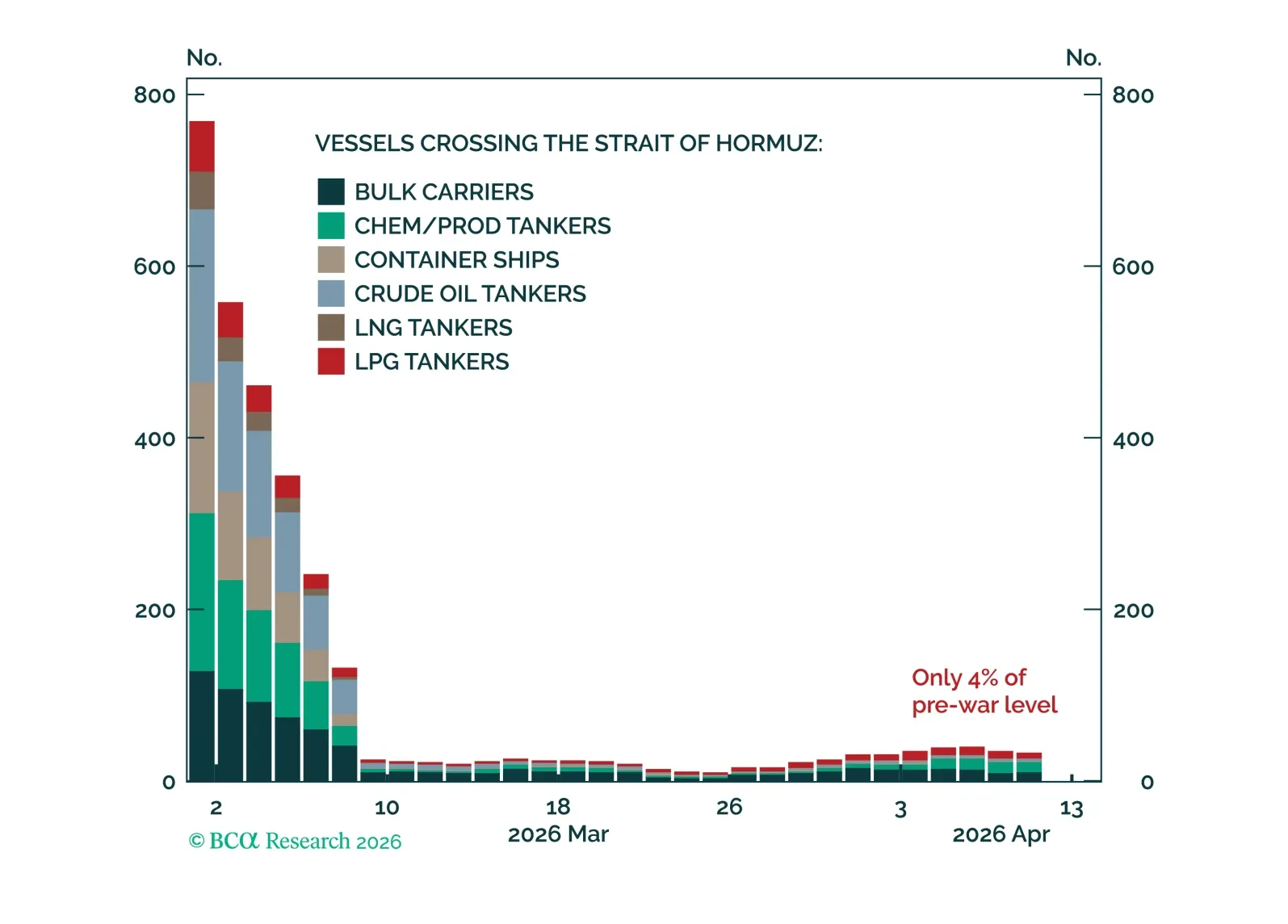

The Iran war has damaged LNG production capacity and halted tanker flows through the Strait of Hormuz. We assess the conflict's impact on LNG markets over cyclical and structural horizons.

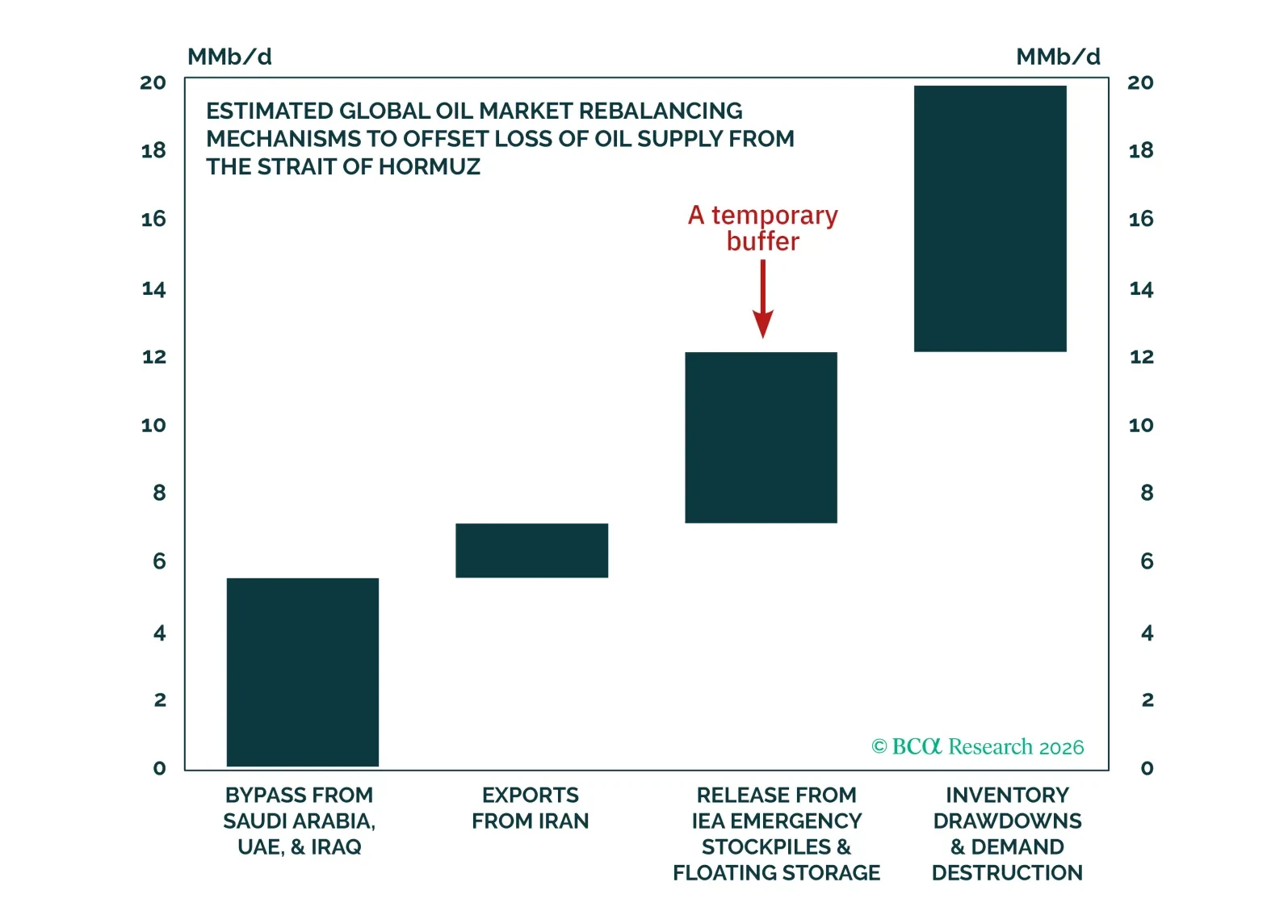

In this report, we deviate from our base case and instead assume that there is an immediate improvement in Hormuz traffic. This exercise allows us to explore how the global oil supply shortfall could eventually be offset if the right conditions are in place.

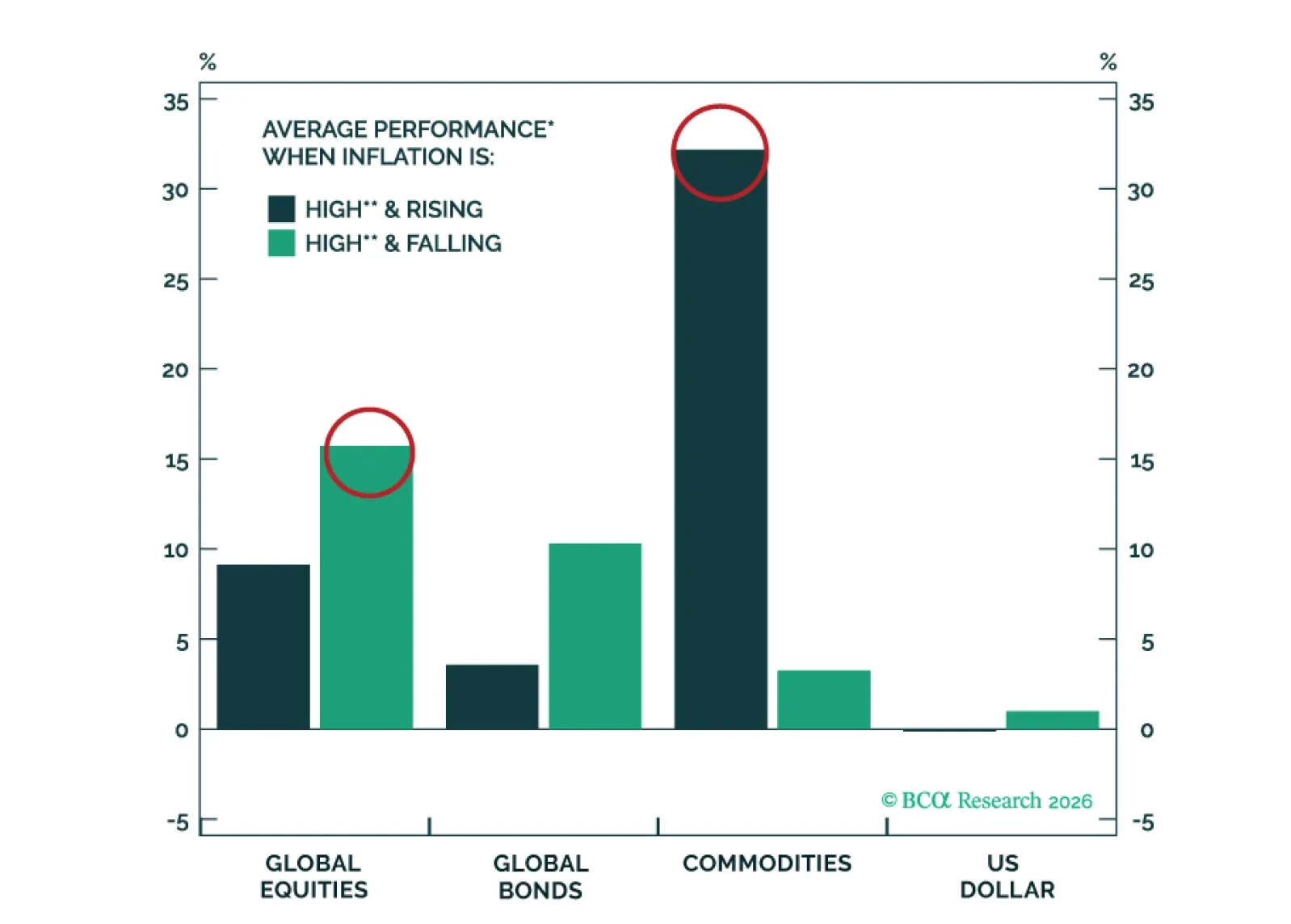

The Iran war provides a timely motivation for examining how the main financial asset classes and commodity sectors perform across different inflation regimes and during periods of elevated geopolitical risk.

Over the past month, oil market participants have scrambled to fill the gap in global oil supply caused by the Strait of Hormuz’s closure. While these efforts have been impressive, the scale of the disruption means they are ultimately insufficient. Upside pressures will continue to dominate energy prices until transit through the Strait of Hormuz is restored.

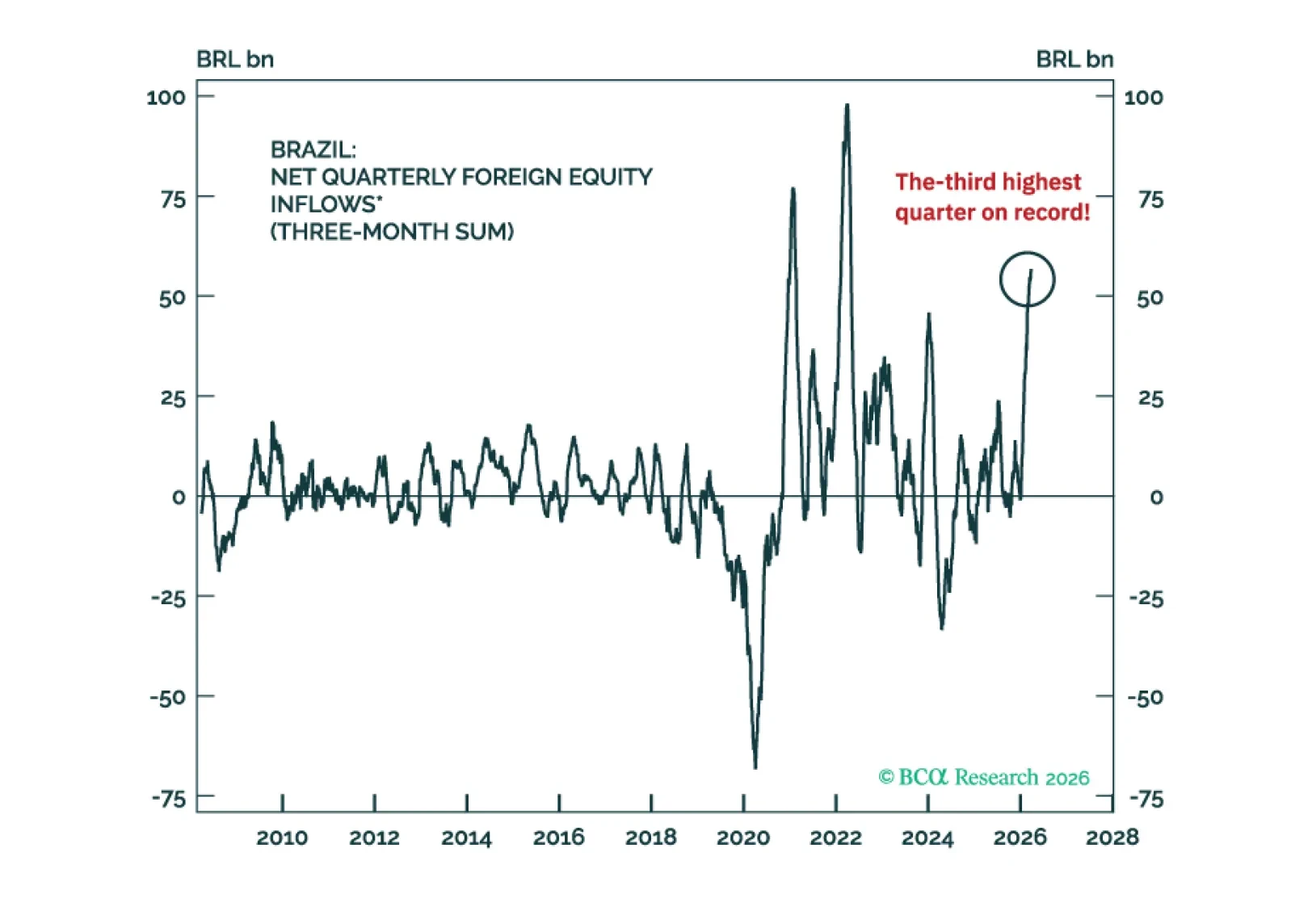

Overstretched foreign inflows into Brazilian markets will reverse, while soaring oil prices will not benefit Brazil in the near term. Avoid the country’s risk assets and the BRL, and stay underweight Brazilian equities and fixed income relative to EM. We also recommend paying 10-year Brazilian swap rates.

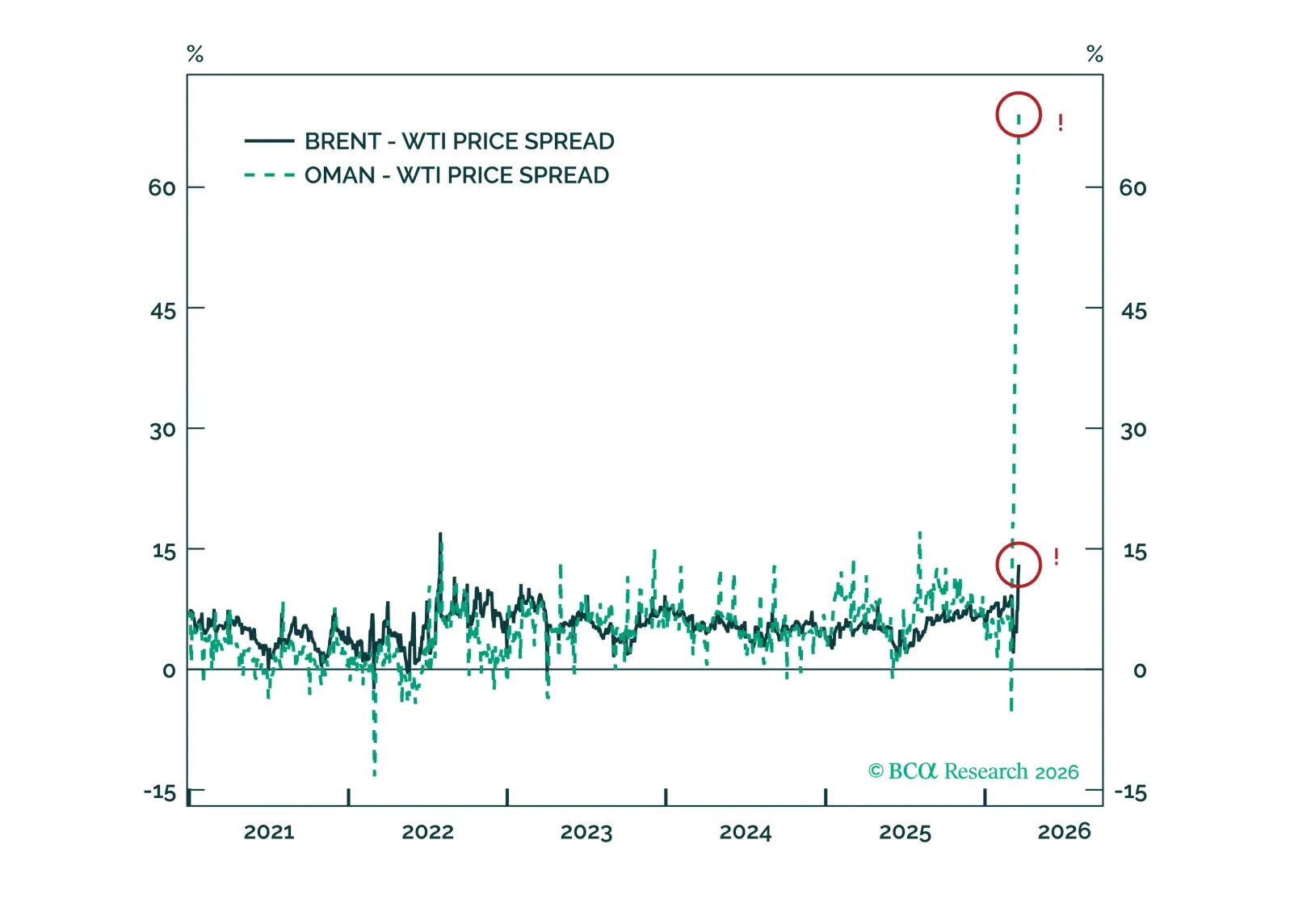

WTI is relatively calm amid the current conflict in the Middle East. Markets are too complacent on US crude relative to other international benchmarks.