Financial Markets

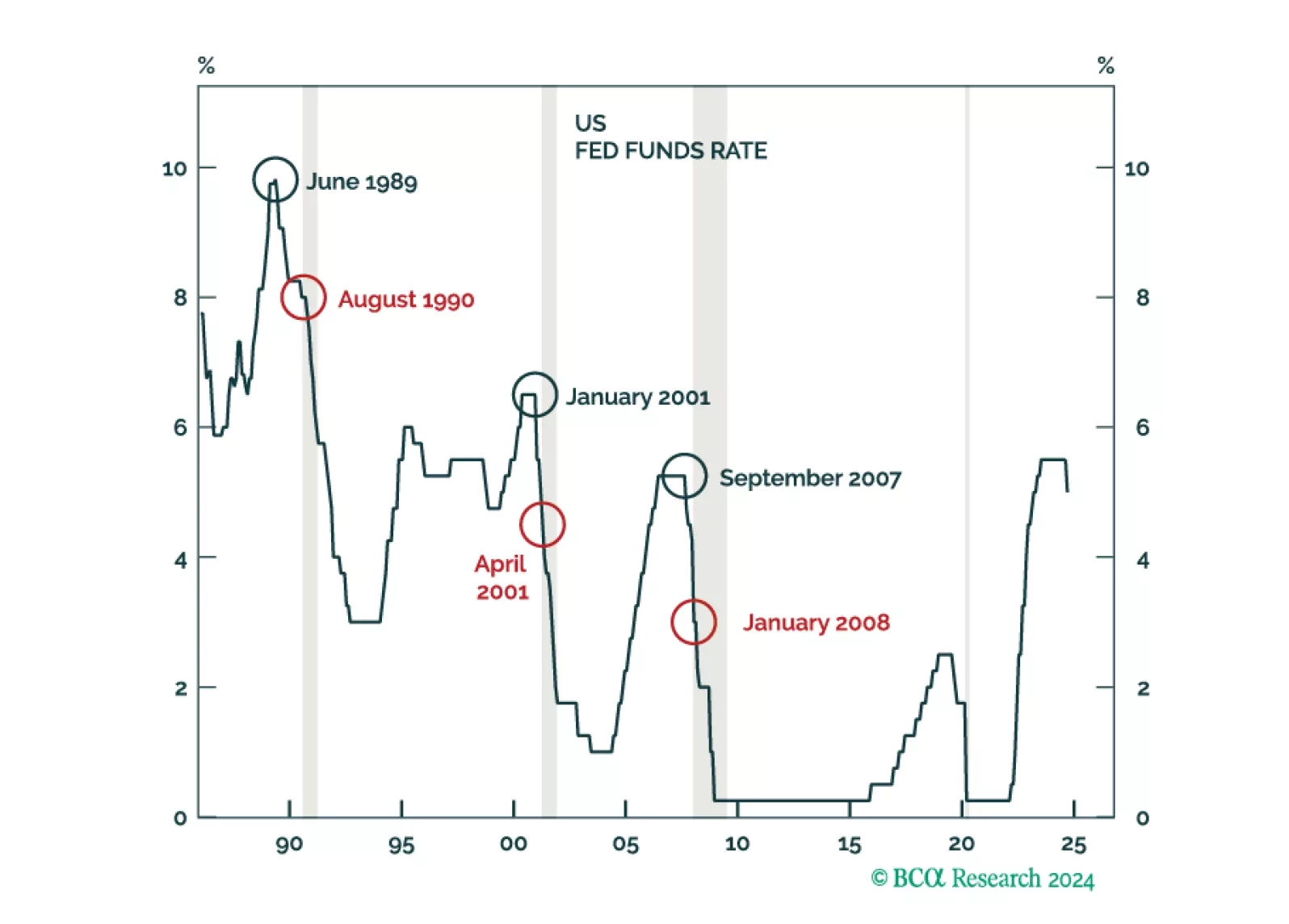

After resisting the consensus narrative in 2022 that a US recession was imminent, and then predicting an immaculate disinflation for 2023, the Global Investment Strategy team has joined the dark side and is now expecting a recession to start in the US within the next six months. Accordingly, we recommend that investors underweight stocks and overweight government bonds.

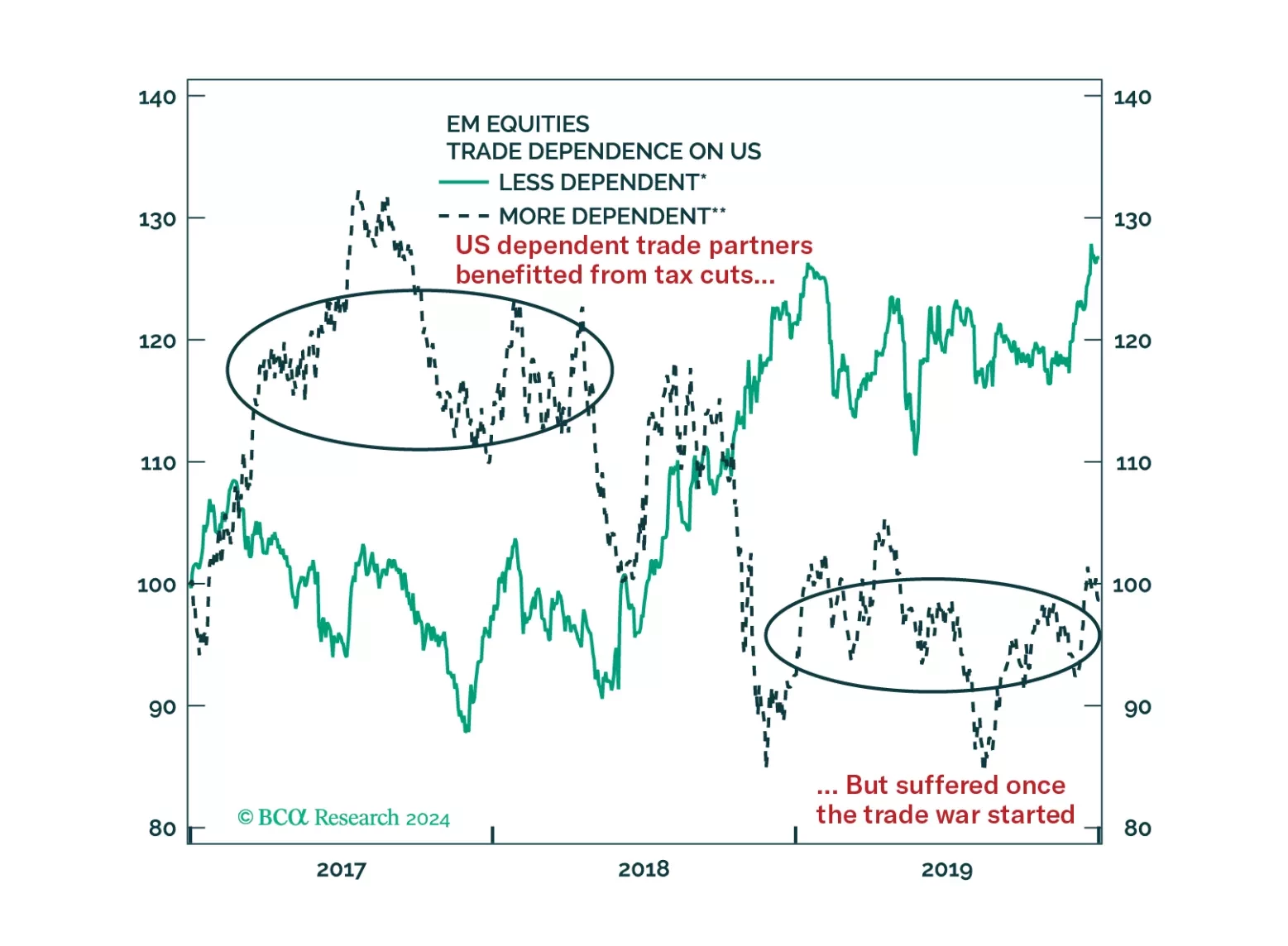

As we head into a more turbulent macroeconomic and geopolitical period, investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable region, and not so dependent on the US or China. Hence, we are introducing the Global Political Capital Index as a way to integrate these factors into a score that can help narrow down the countries with the best and worst abilities to deal with the incoming challenges.