Emerging Markets

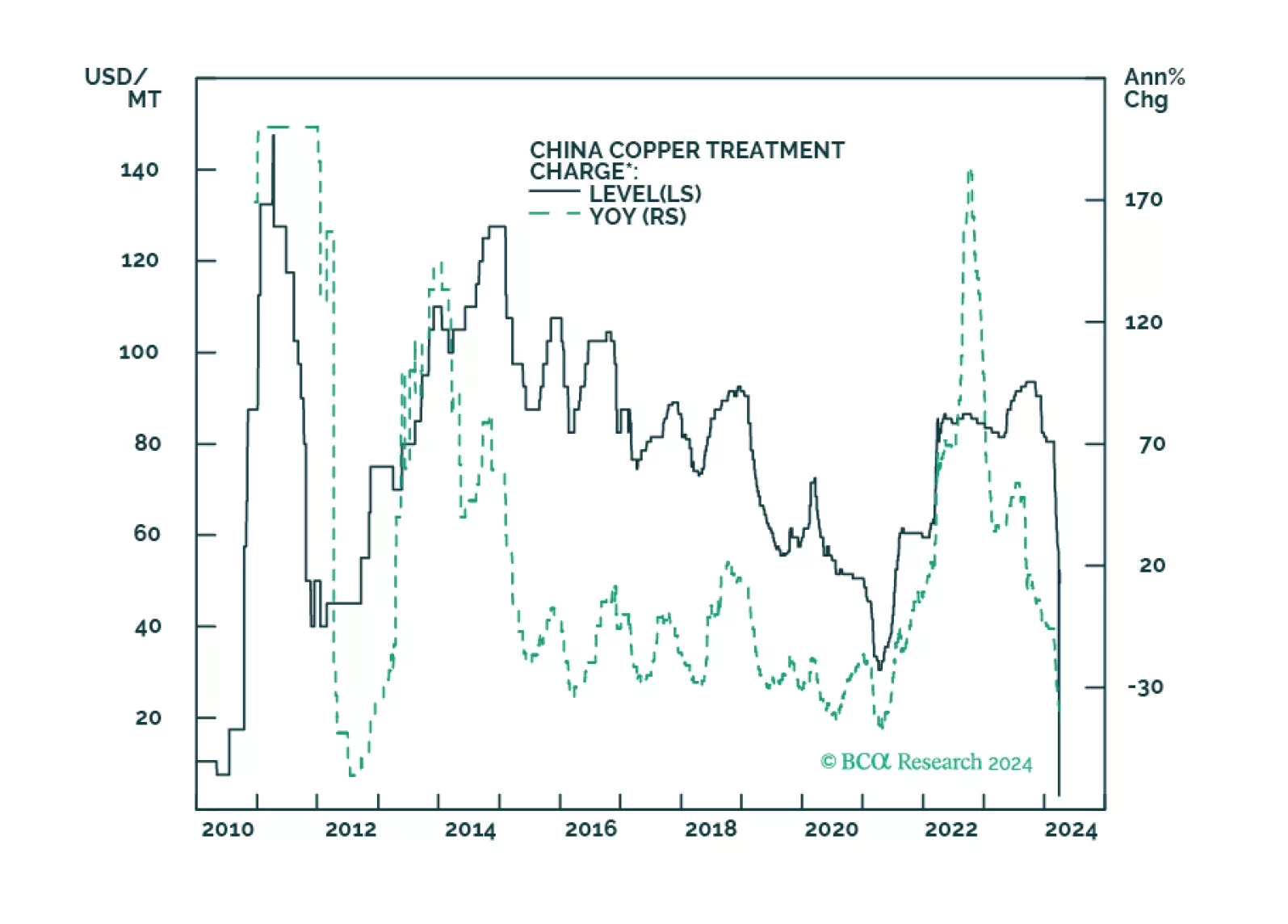

Copper markets are fast approaching a price breakout, as Chinese smelters scramble to find ore to meet increasing refined-copper demand in the wake of a global manufacturing rebound. We are holding fast to our expectation of $4.50/lb (COMEX) this year. We remain long the XME ETF to retain exposure to copper miners and refiners, and the COMT ETF to retain exposure to commodity flat price and the copper backwardation we expect.

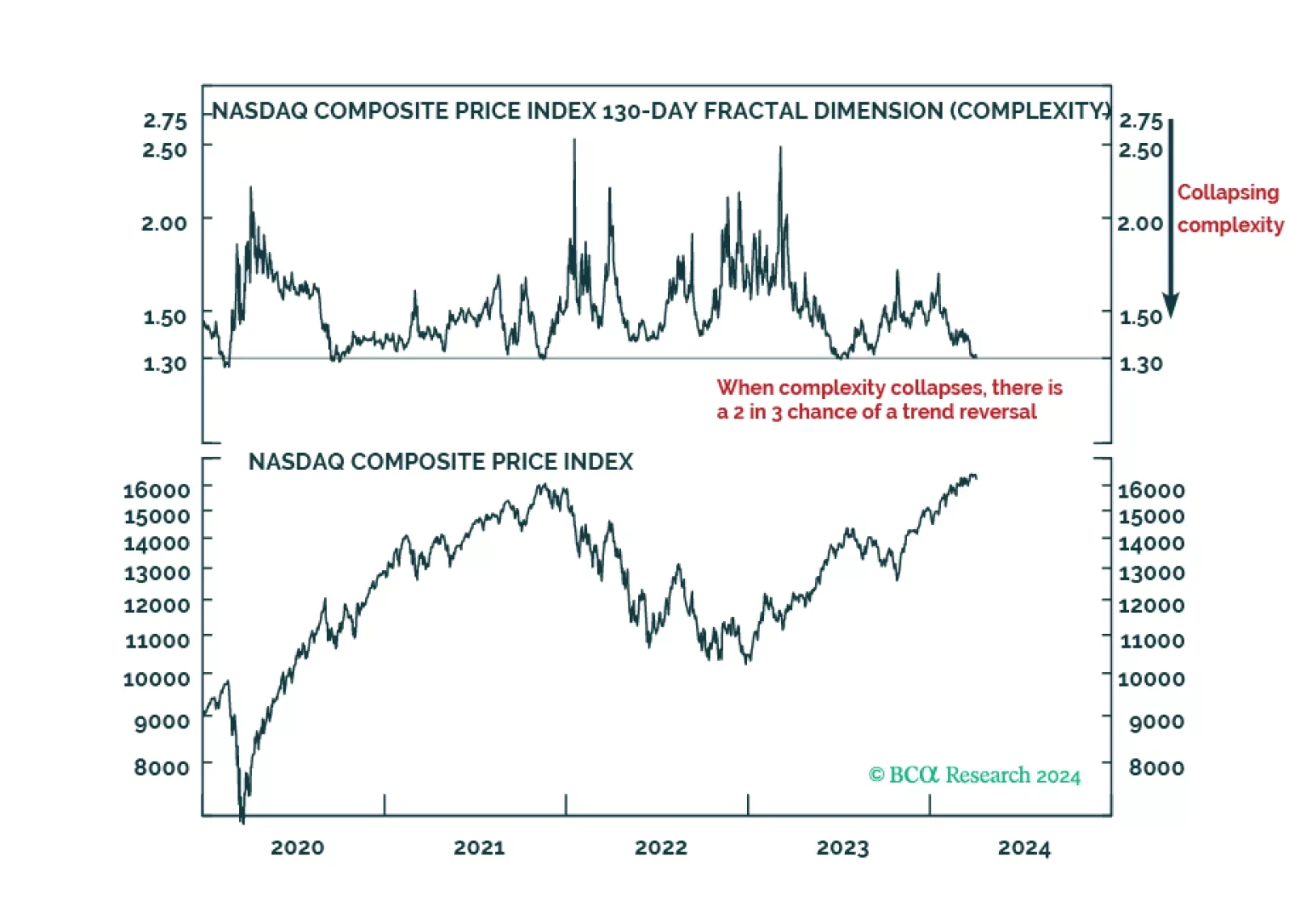

The analysis of complexity is a massive competitive advantage in investing, and from today, clients will be able to monitor the complexities of the world’s 17 major investments on our webpage in real-time.

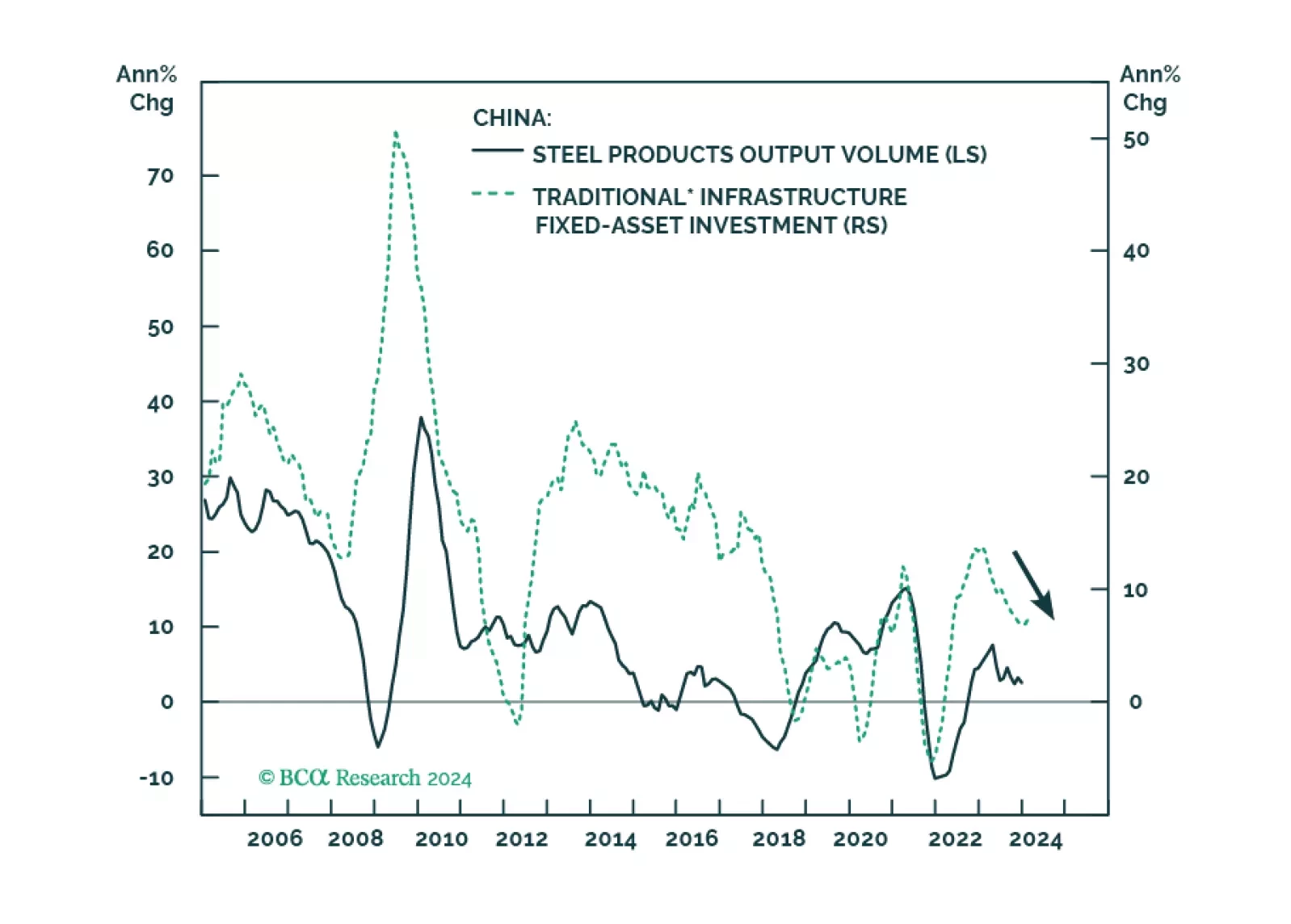

Due to funding constraints, China’s infrastructure investment nominal growth rate will likely slow from 9% in 2023 to about 6% this year. The new issuance of Special Treasury Bonds will prevent a contraction in the country’s infrastructure spending, but it will not lead to an acceleration. Stay cautious in China’s infrastructure plays in general and steel and machinery stocks in particular.

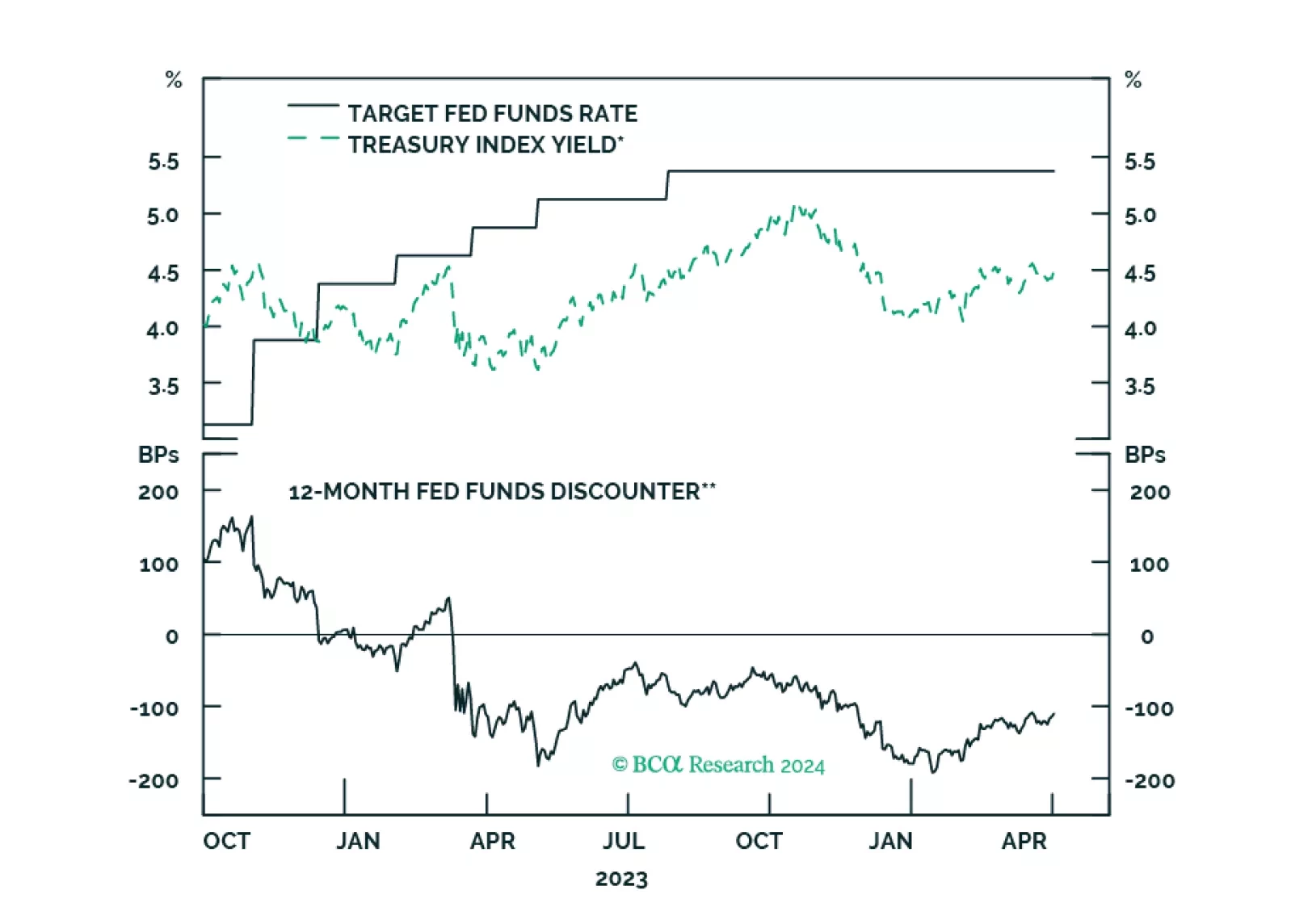

The global economy is wobbling precariously between slowing growth and reaccelerating inflation. This is unlikely to end well. Stay cautious, and hedge against both recession and inflation.

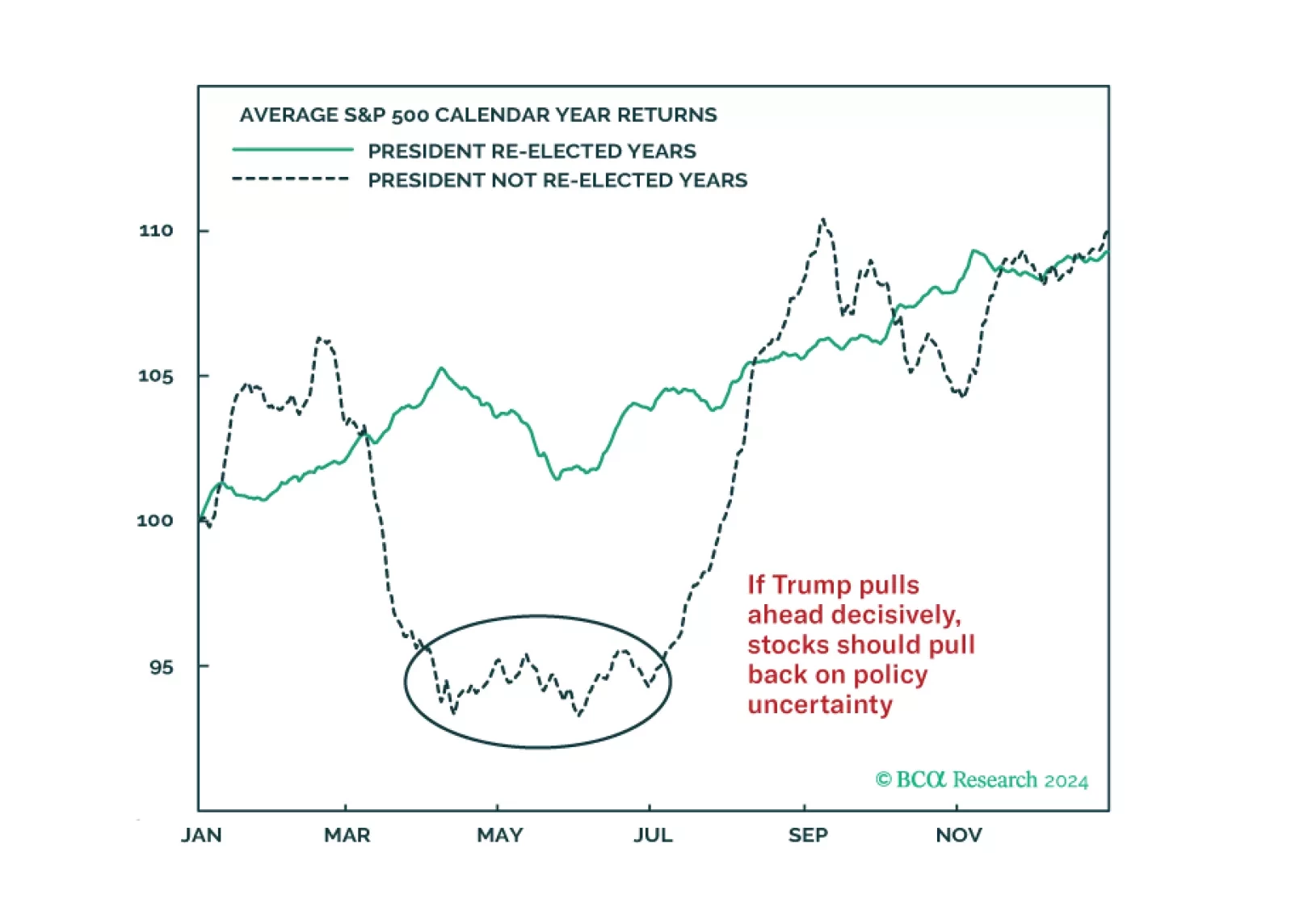

Investors around Europe and North America are concerned that the stock market is increasingly overbought and vulnerable to exogenous risks. We agree and have good reasons to fear that festering geopolitical risks and the US election season will deal negative surprises.

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.