Commodities & Energy Sector

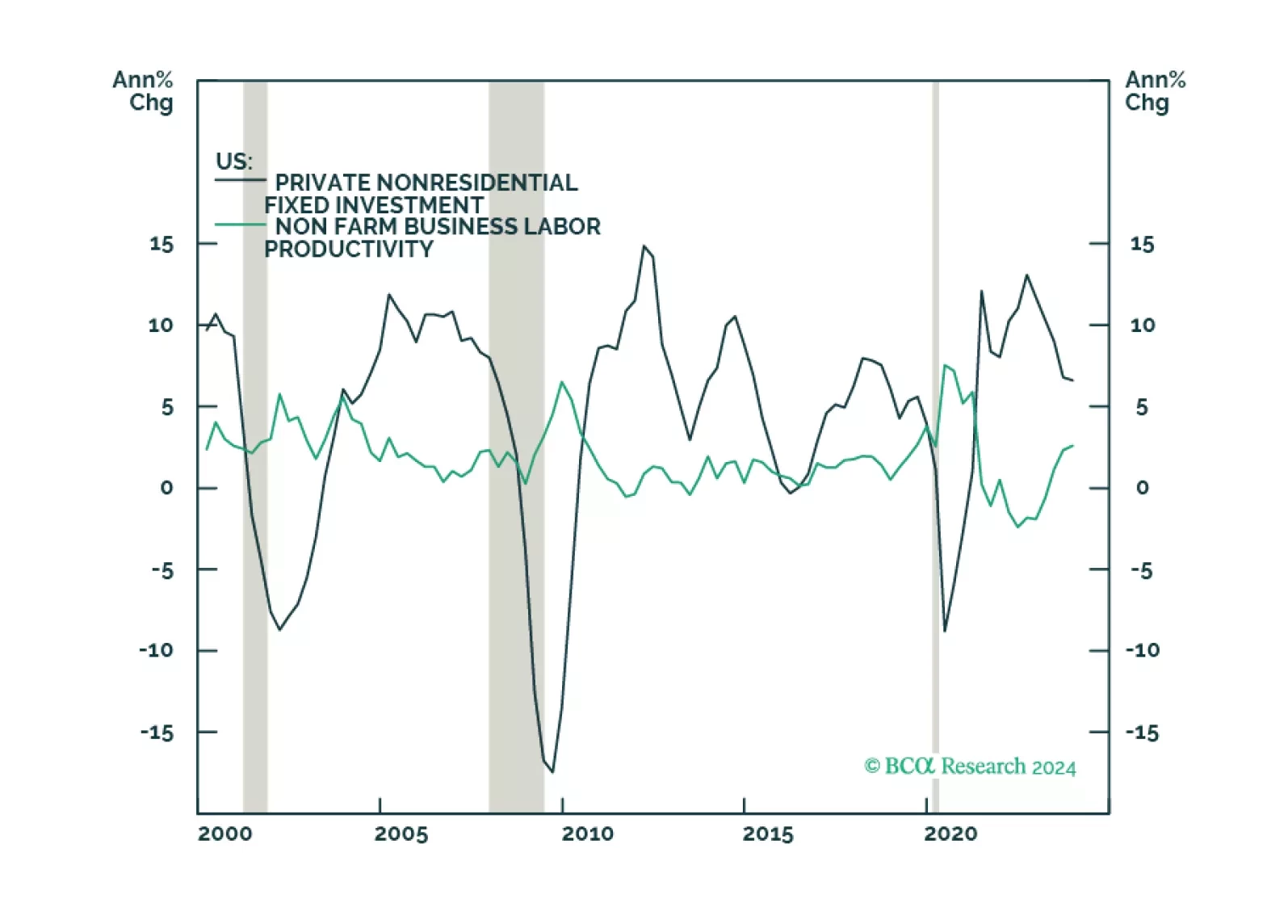

Inflationary pressures this year will remain subdued as labor-productivity growth – driven by strong capex and R+D spending – continues. This will make the Fed more confident in beginning its policy-rate-cutting cycle in June, and will keep gold well bid. We are raising our gold target to $2,300/oz. We continue to expect no recession this year.

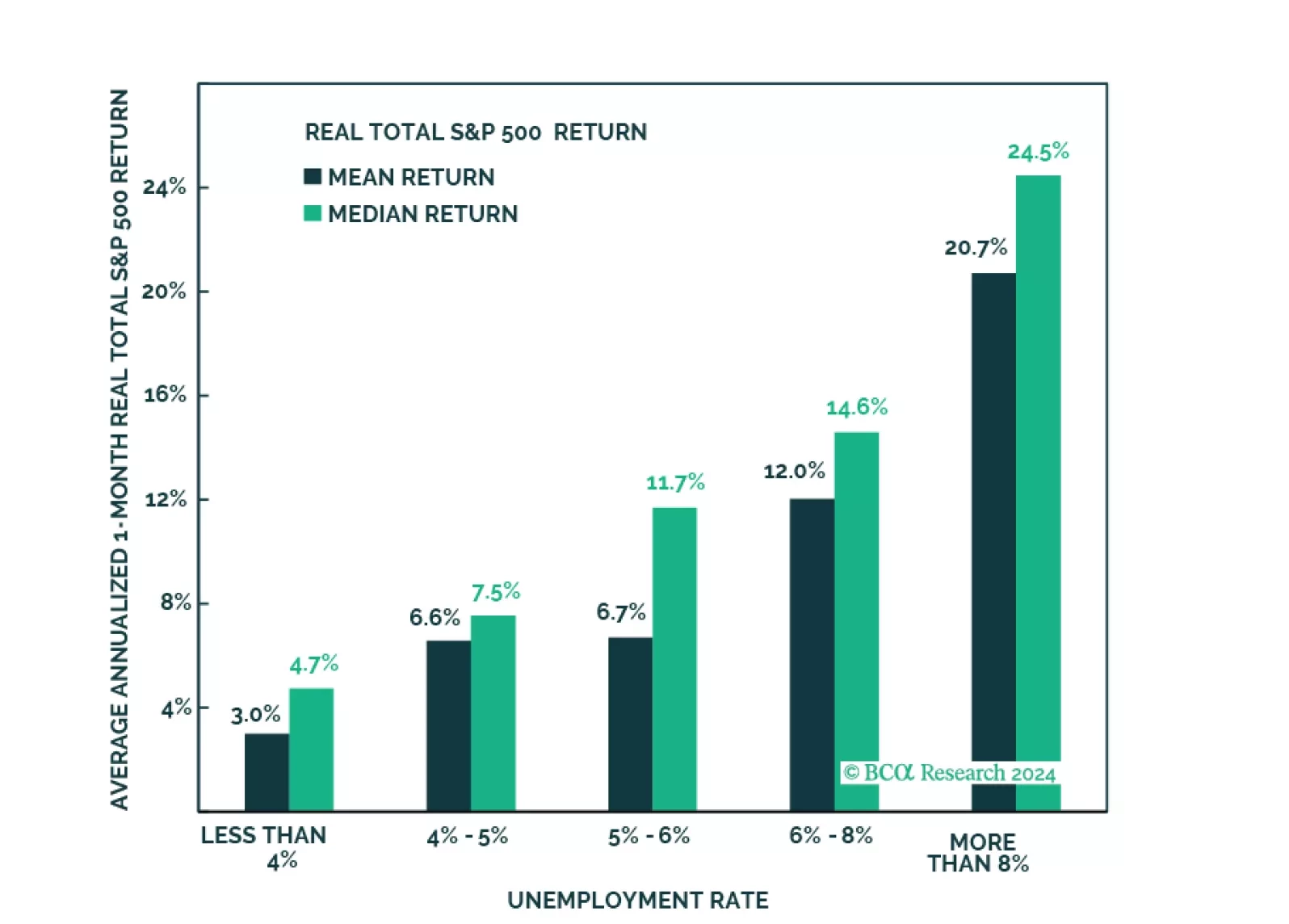

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

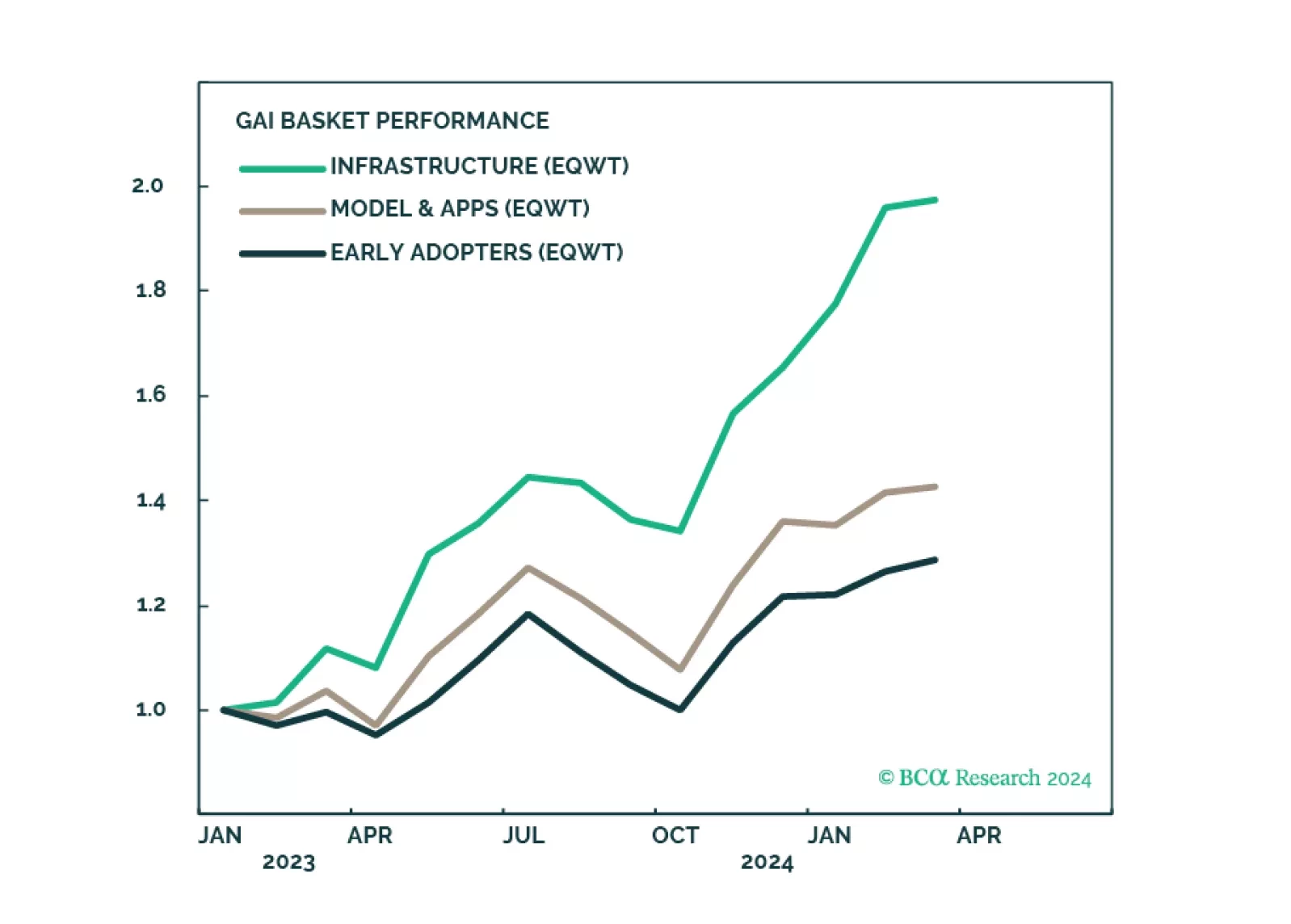

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

We expect oil-demand growth to increase this year – to 1.7mm b/d from 1.4mm b/d (0.30% of total demand) – and anticipate tighter supply at the margin. Our balances estimates are unchanged, leaving our Brent price forecasts for 2024 and ’25 at $95/bbl and $105/bbl. We expect the US to deploy warships if Venezuela makes a move on Guyanese territory in a bid to grab deep-water oil production.

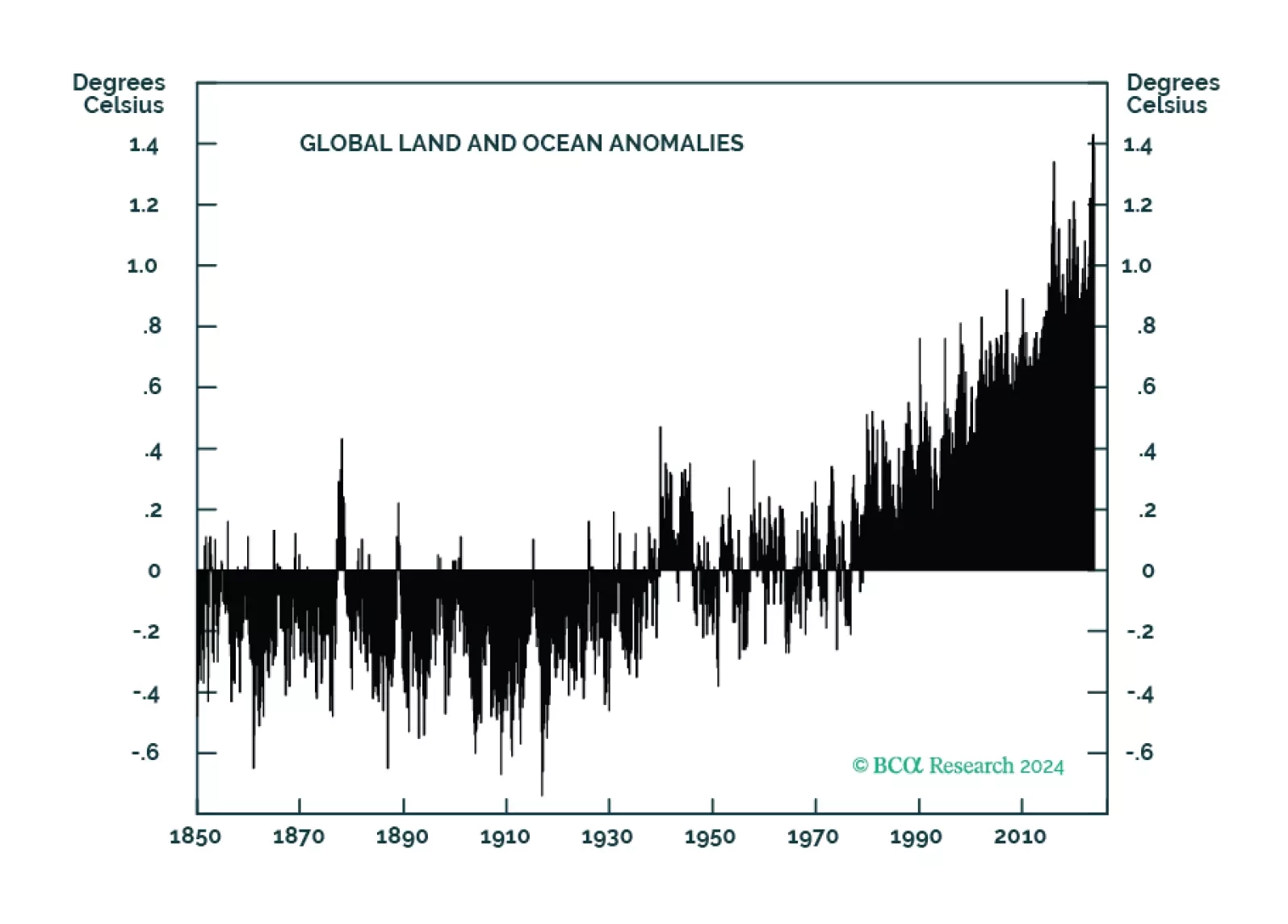

Global ag markets will become more volatile as anthropogenically induced climate change continues to degrade farmland. This will make price signals emanating from these markets less efficient in terms of processing supply-demand fundamentals. All else equal, food prices likely move higher, which will contribute to inflationary biases in the medium-to-long run. Investors will continue to seek out farmland investments as a way to diversify portfolio risk and raise absolute returns.

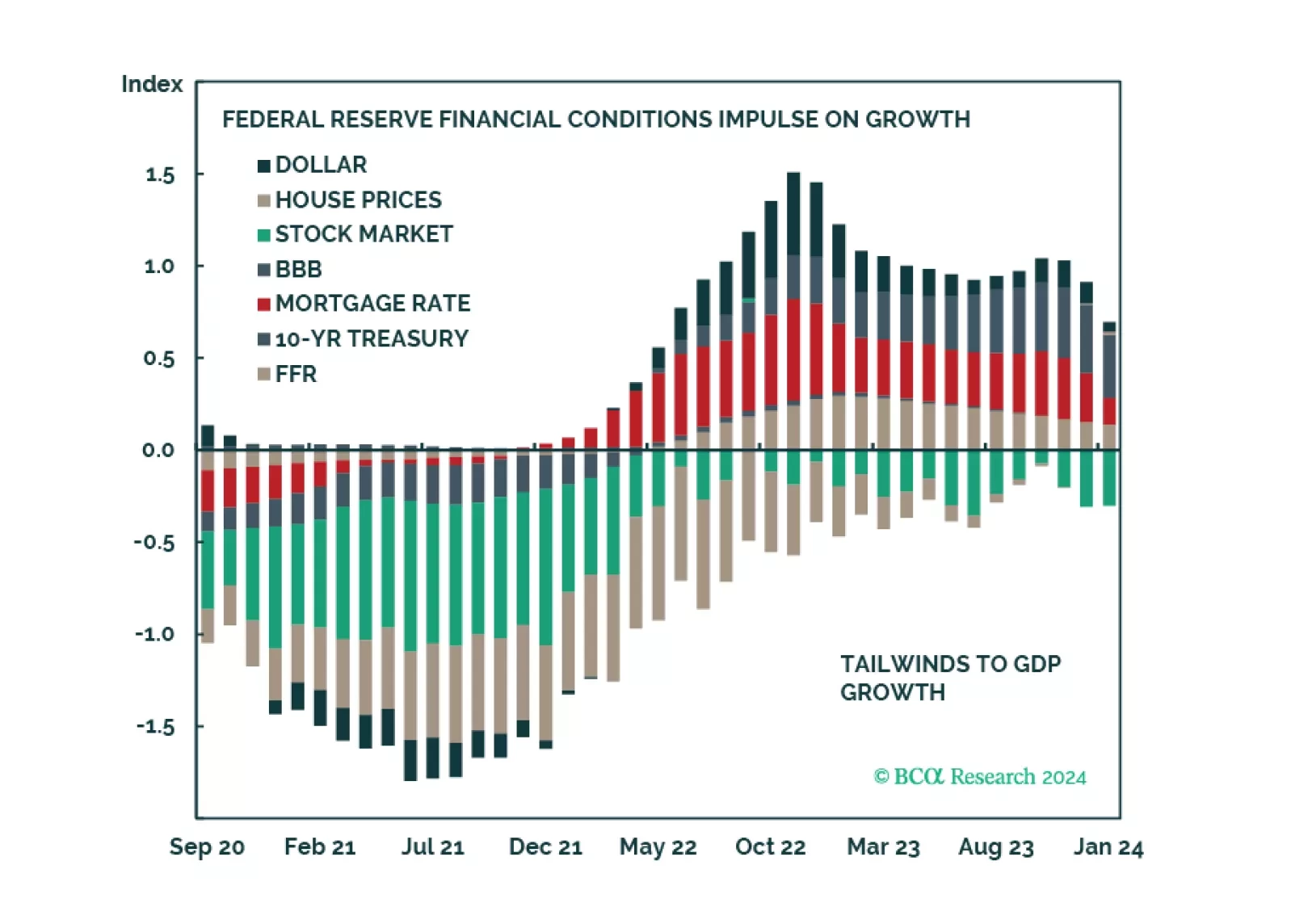

Clients are increasingly more positive about the US economy, but there are no signs of exuberance. The rally could continue as the majority is not fully invested. Financial conditions have already eased, and the Fed is unlikely to surprise on the upside but will deliver a promised cut this summer. CRE is a still pain point of the US economy. We are not bearish, but after a fast and furious rally, markets are fragile.