Commodities

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

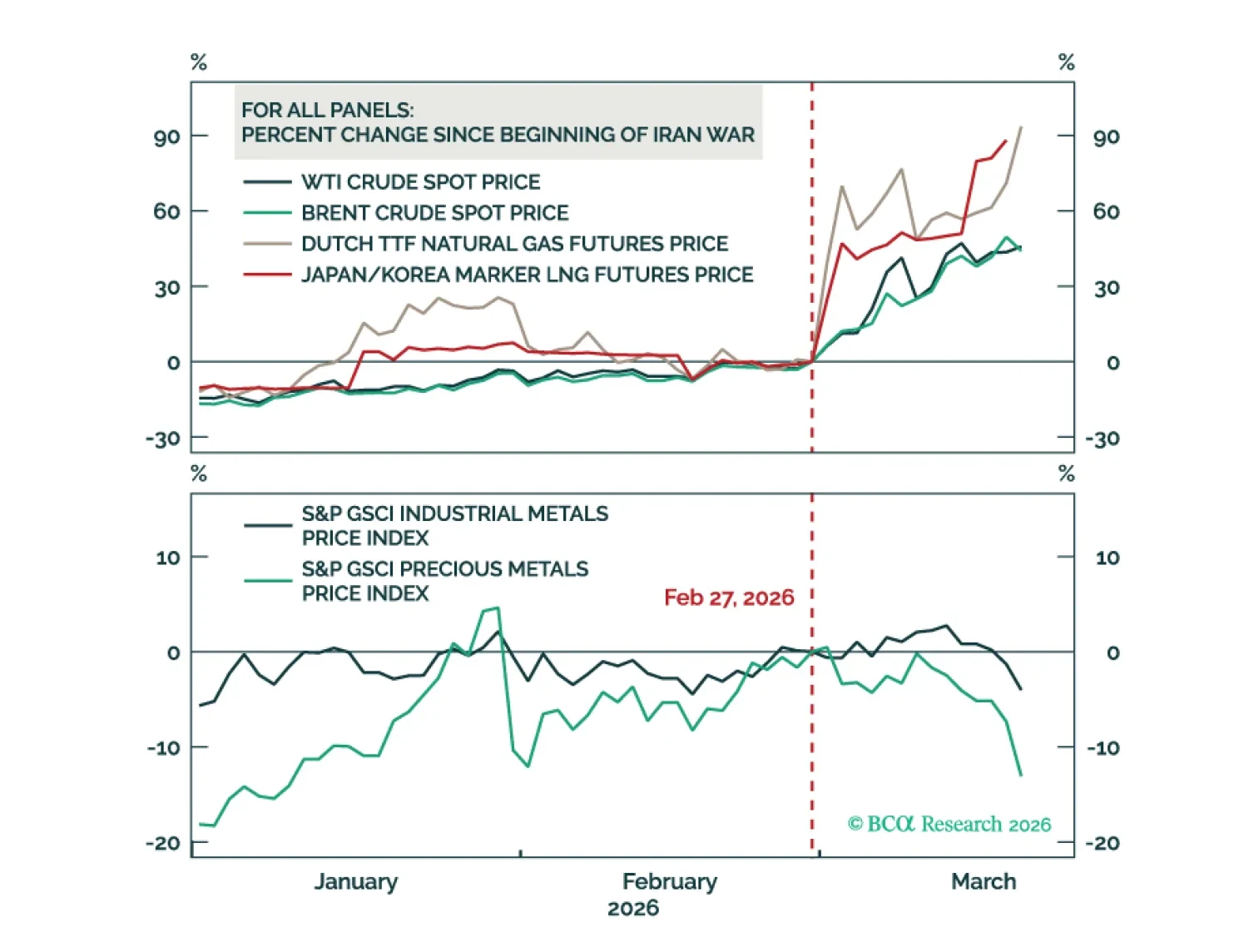

We outline a framework for the Iran war's impact on the commodity outlook in the event of a prolonged Strait of Hormuz disruption. We break it down into three phases: (1) the Initial Shockwave, (2) the Ripple Effects, and (3) the Backwash. The first phase has largely passed, and we are now in the Ripple Effects phase.

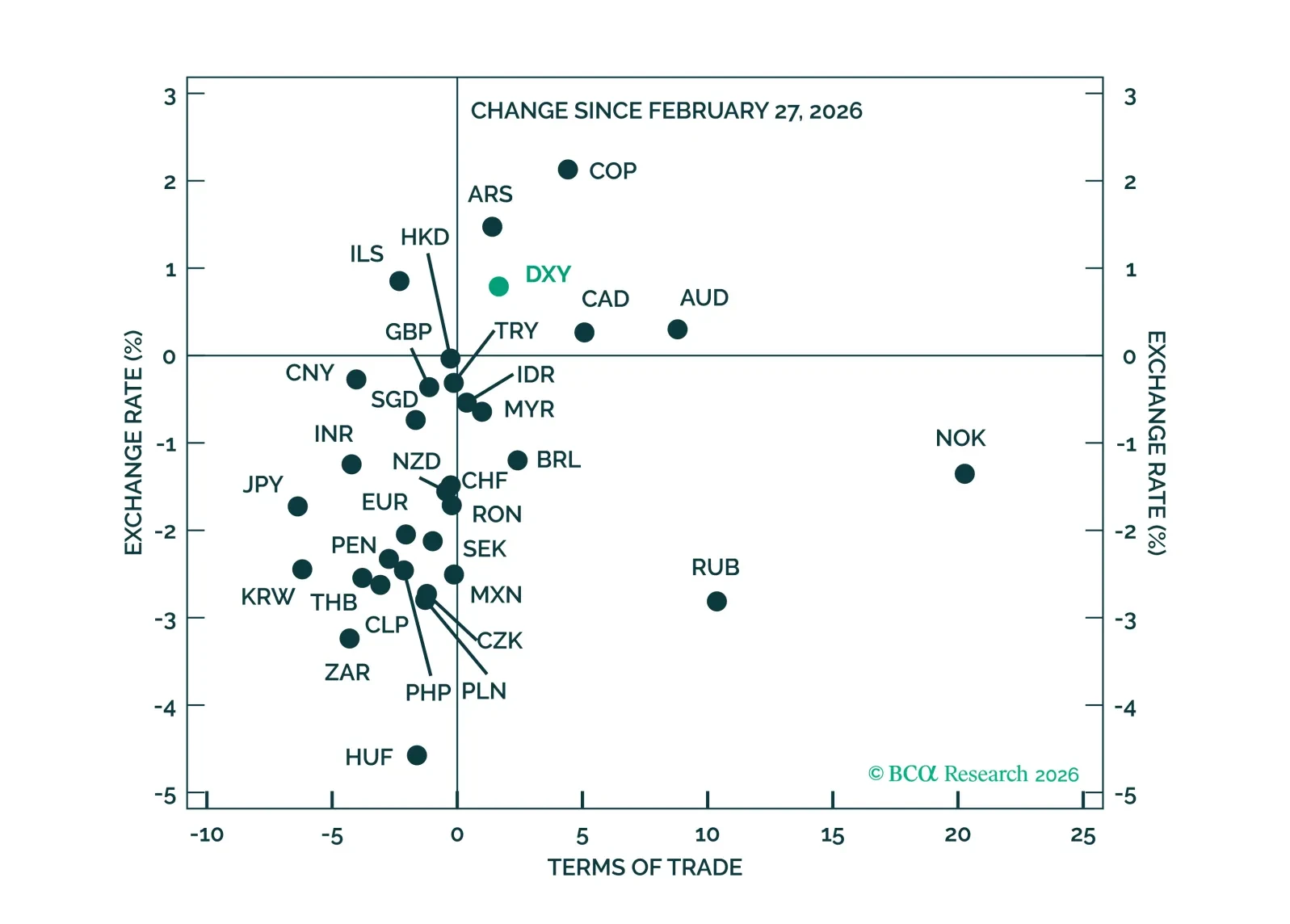

The Iran war remains a terms-of-trade shock rather than a classic flight to safety – for now. As oil risks skew higher, policy repricing and growth differentials should continue to favor a tactical rebound in the USD.

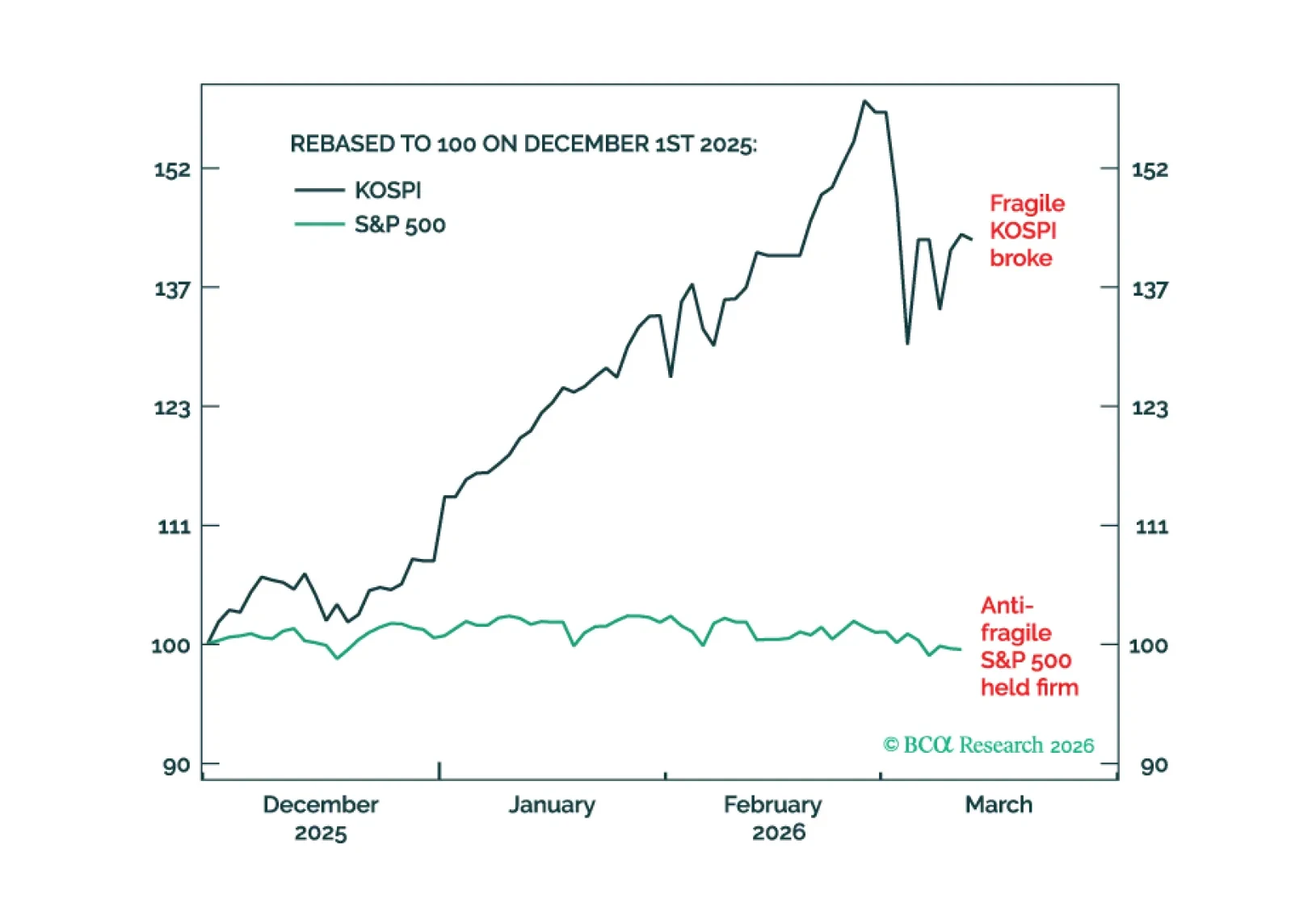

In the ongoing Middle East crisis, anti-fragile markets will remain relatively resilient while fragile markets will break. We describe how to draw the distinction. Plus, a new trade is a 50:50 combination of long USD/MXN and overweight Consumer Discretionary.

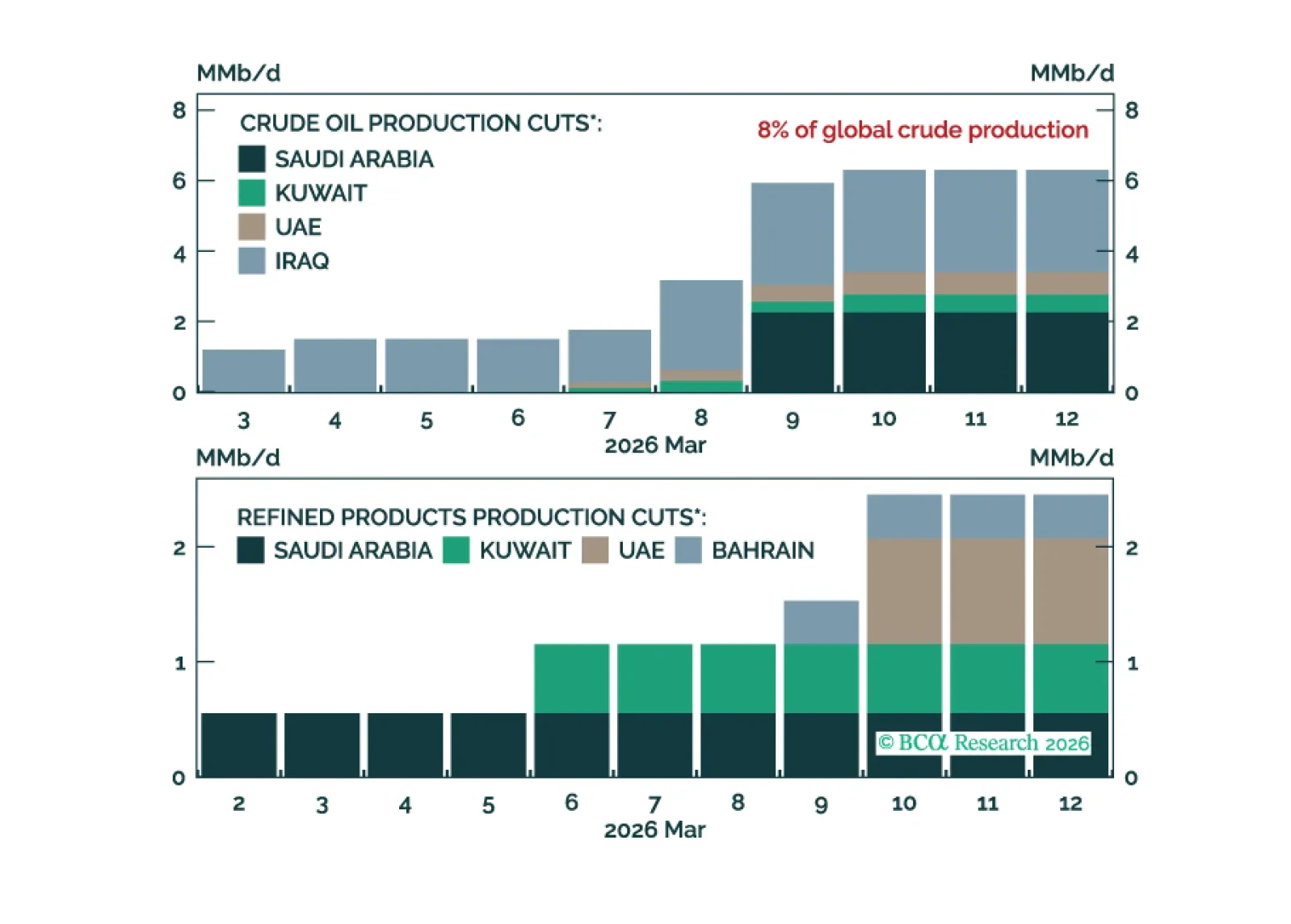

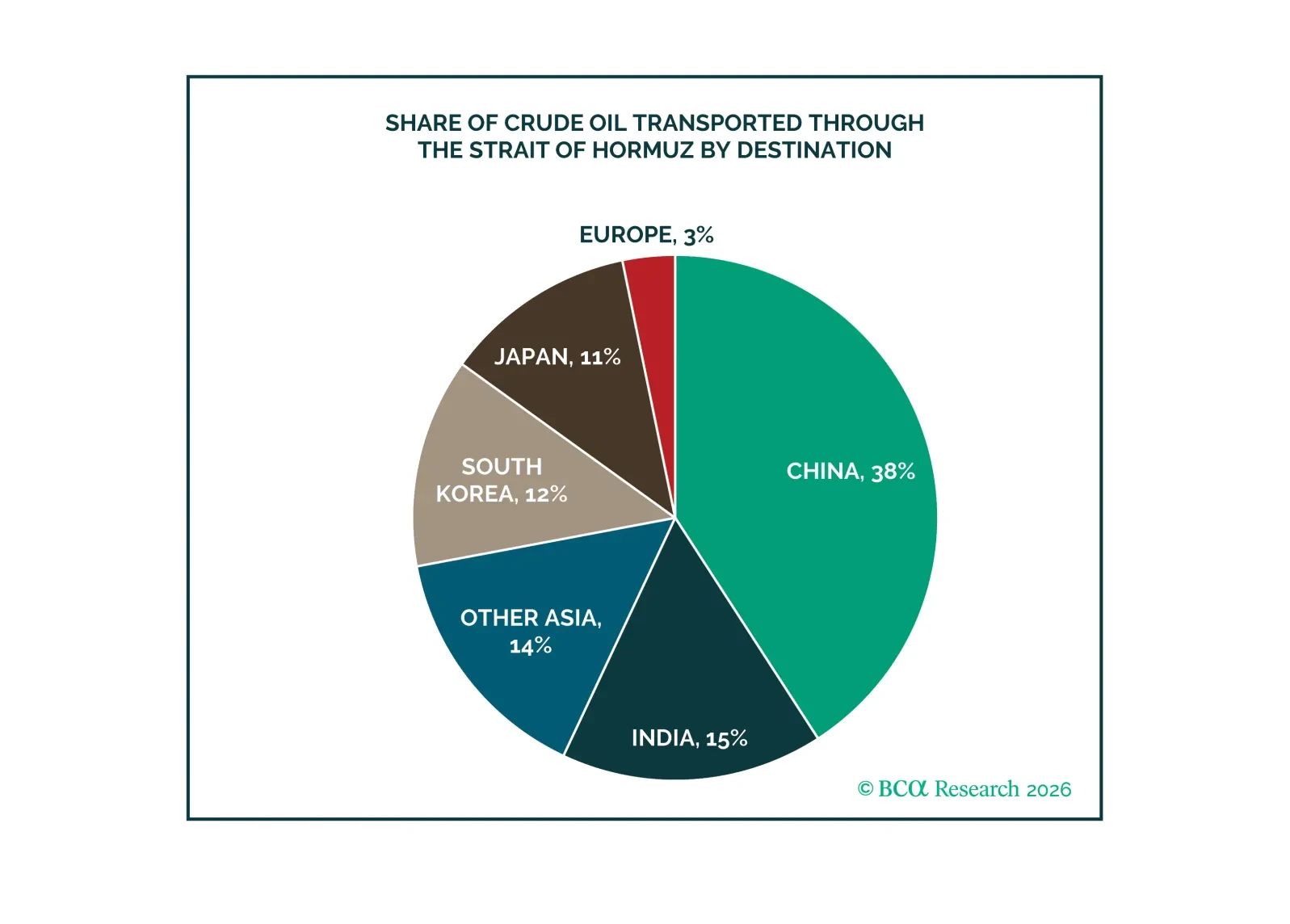

The war in Iran is disrupting global oil and LNG flows and remains a threat to regional energy infrastructure.

Energy price risks remain skewed to the upside over the near term.

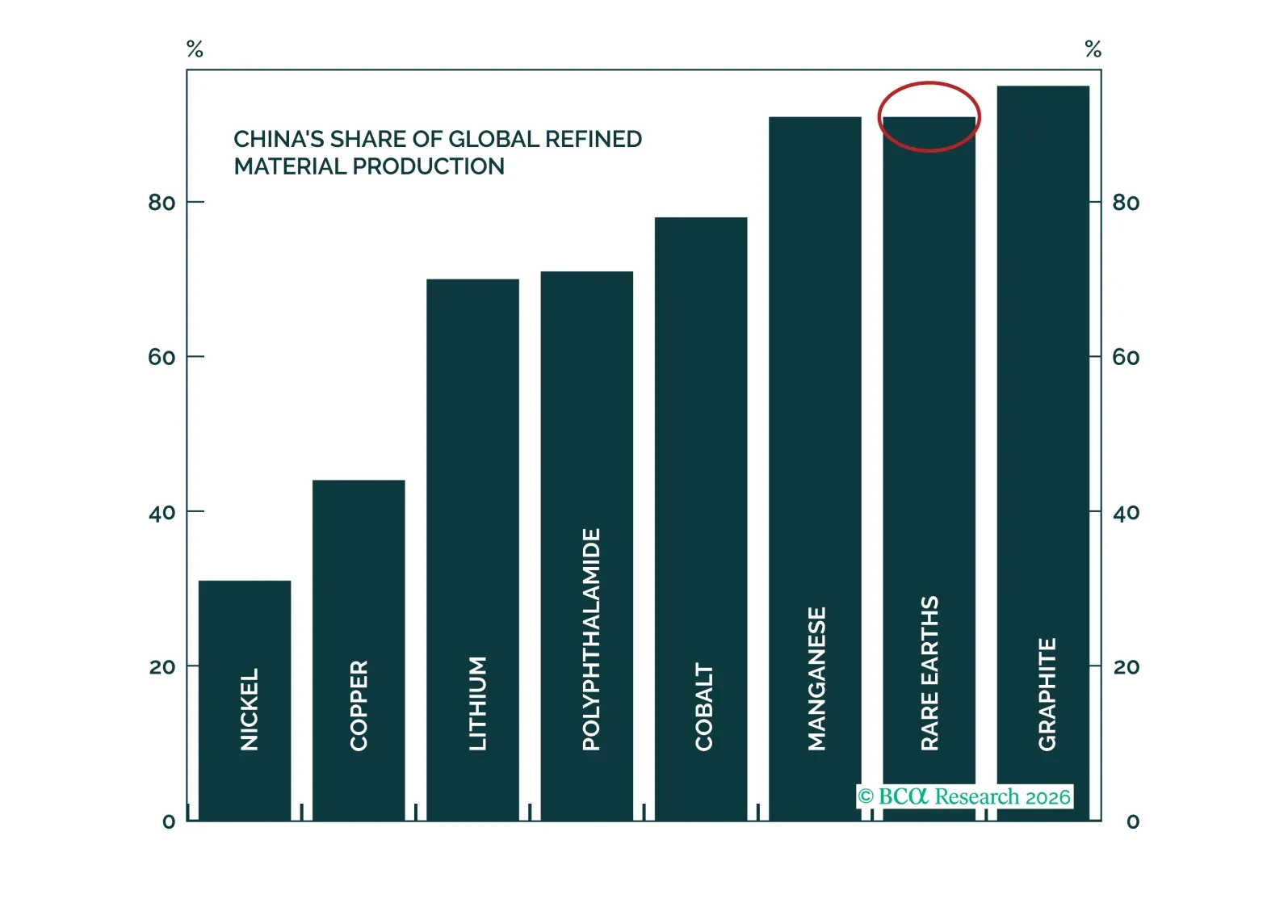

The global drive to build a resilient ex-China rare earth supply chain is accelerating. It has emerged as a strategic priority and is backed by both public and private sector investment in many countries.

In this Special Report, we argue that rare earth adjacent plays present a more attractive opportunity for investors looking to gain exposure to the rare earth capex cycle than a pure-play strategy.