British Pound

This week, we review our currency positions, based on the latest data from G10 economies.

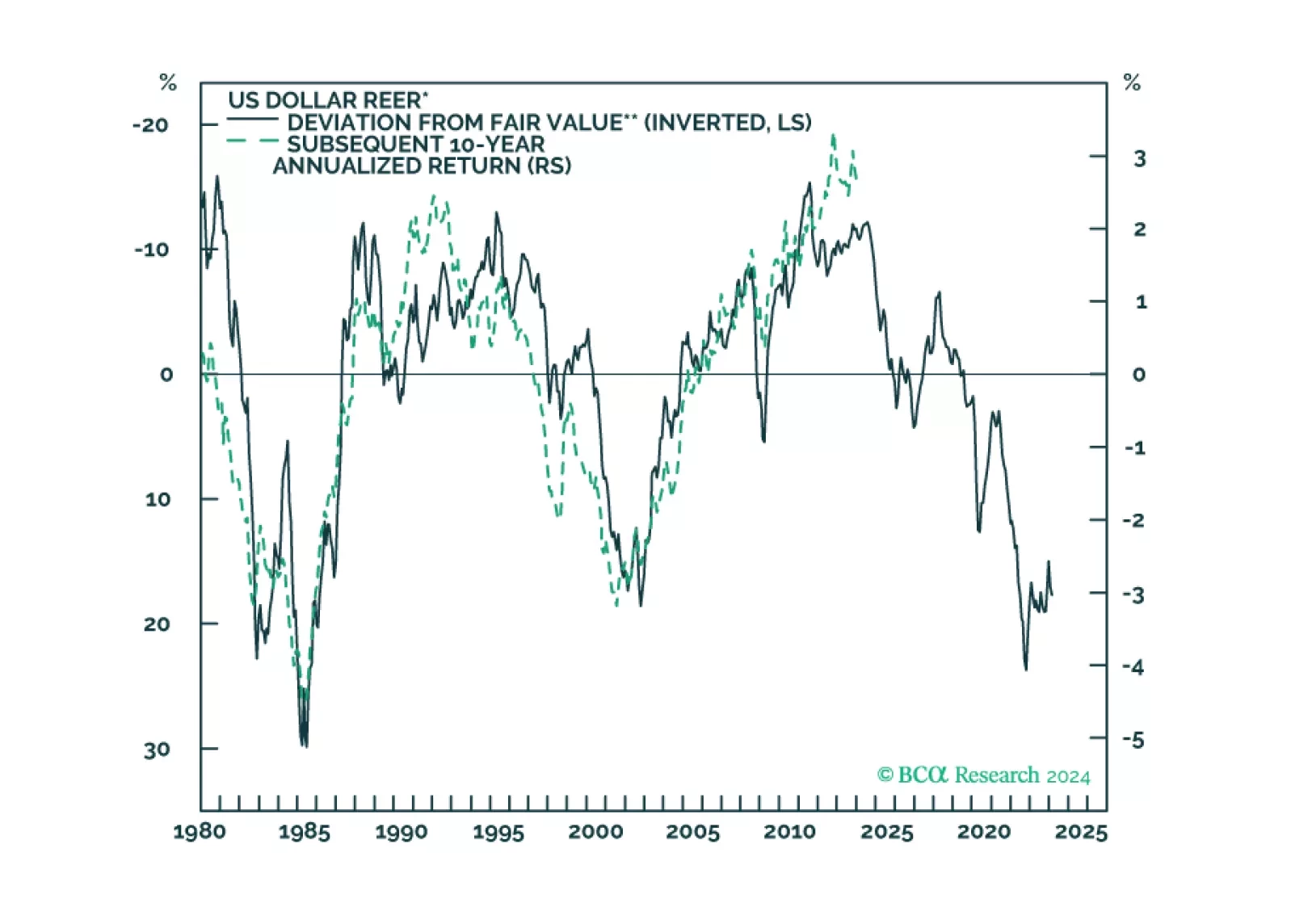

In this week’s report, we release an update to our long-term REER valuation model and expected future returns for major currencies.

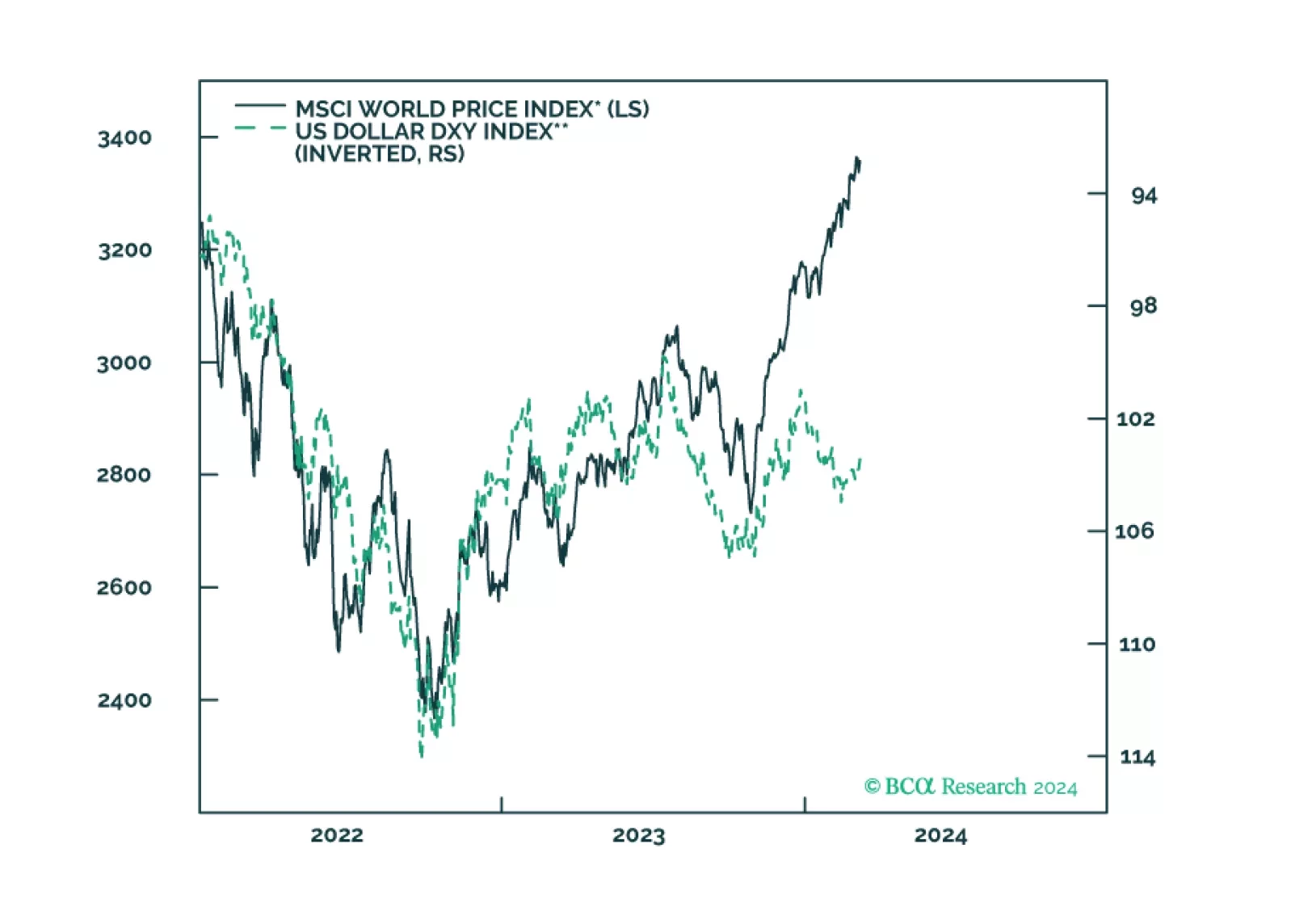

This week’s report explores factors behind the recent rise in the dollar, and whether this could continue in the next month.

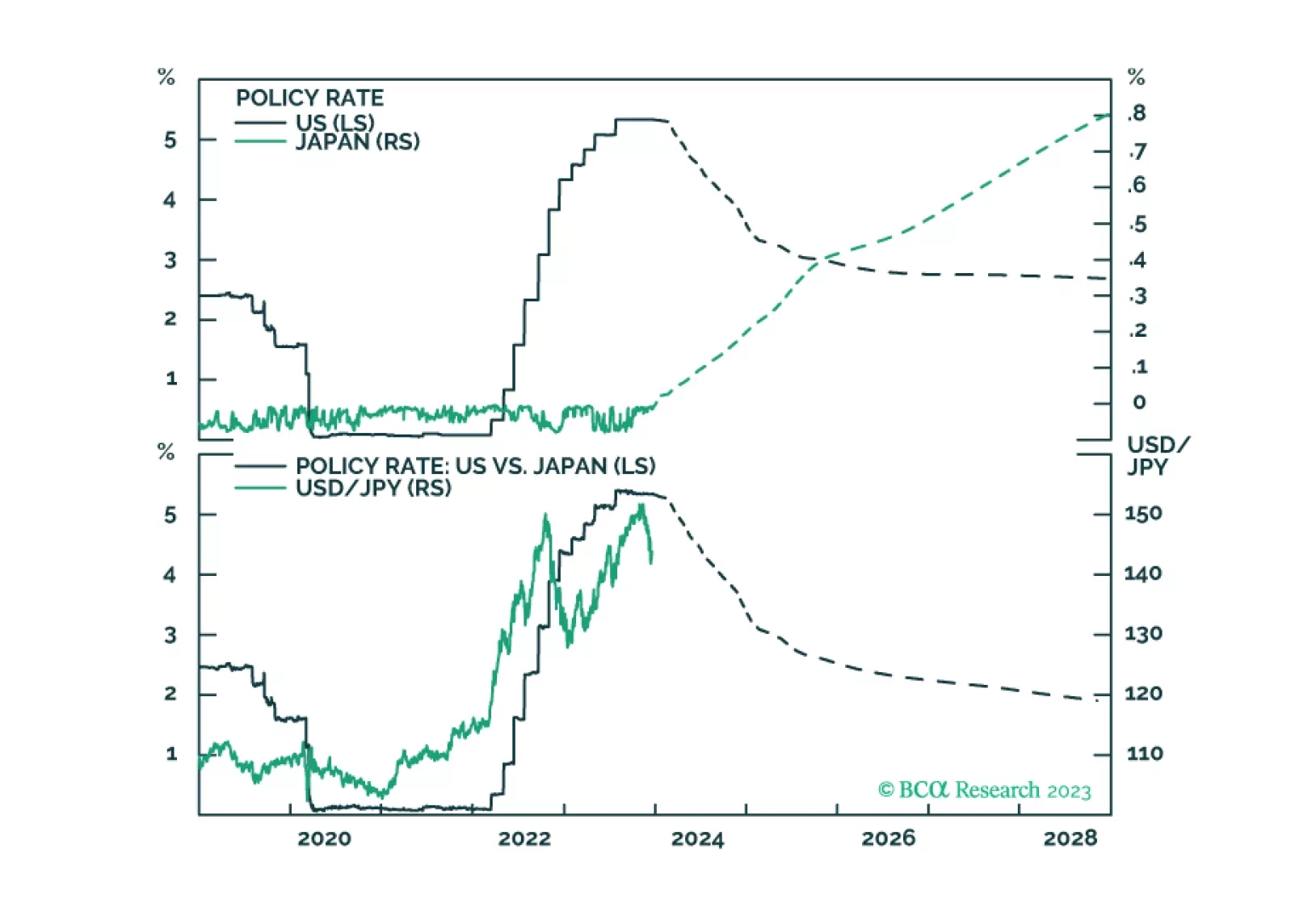

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

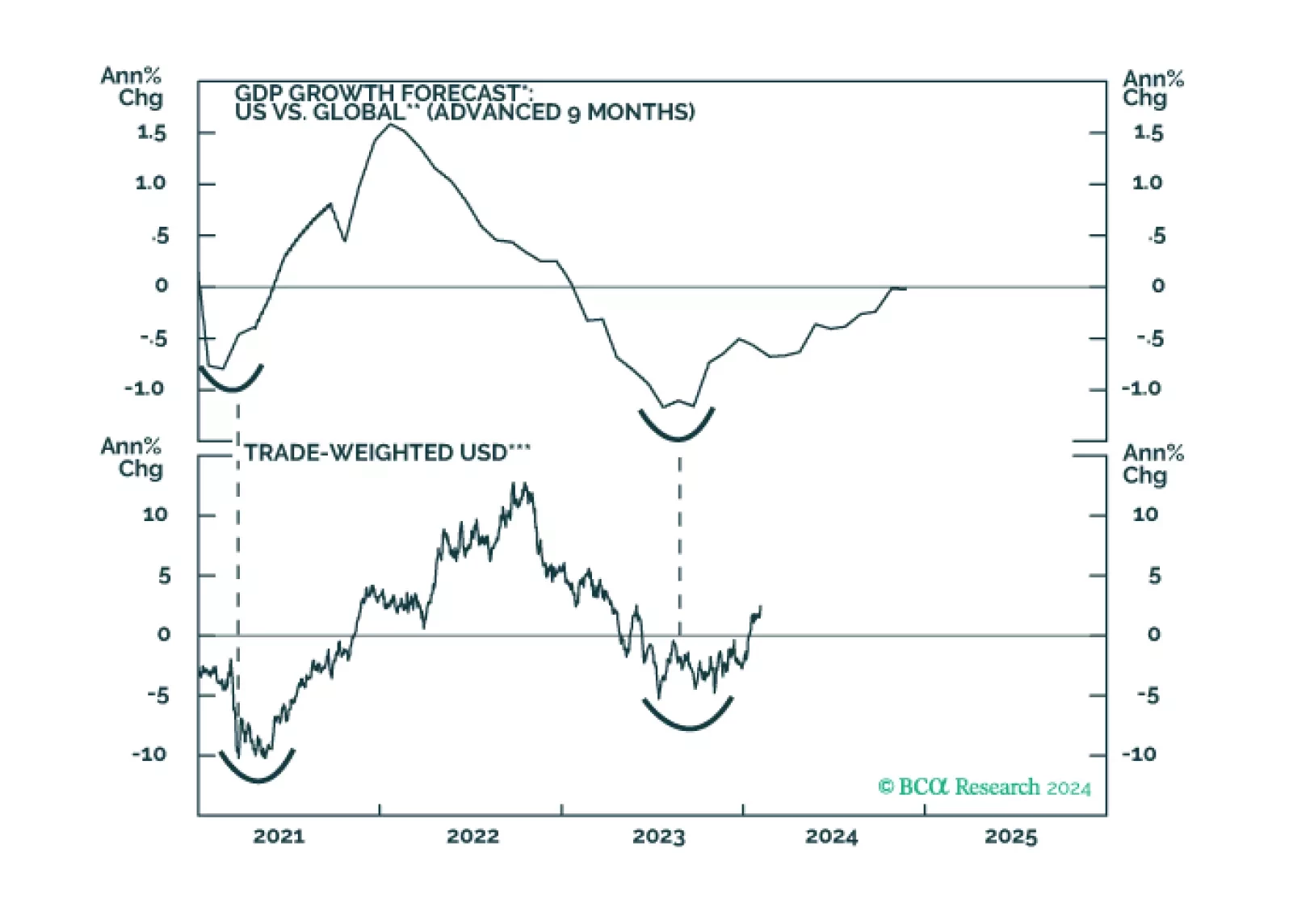

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

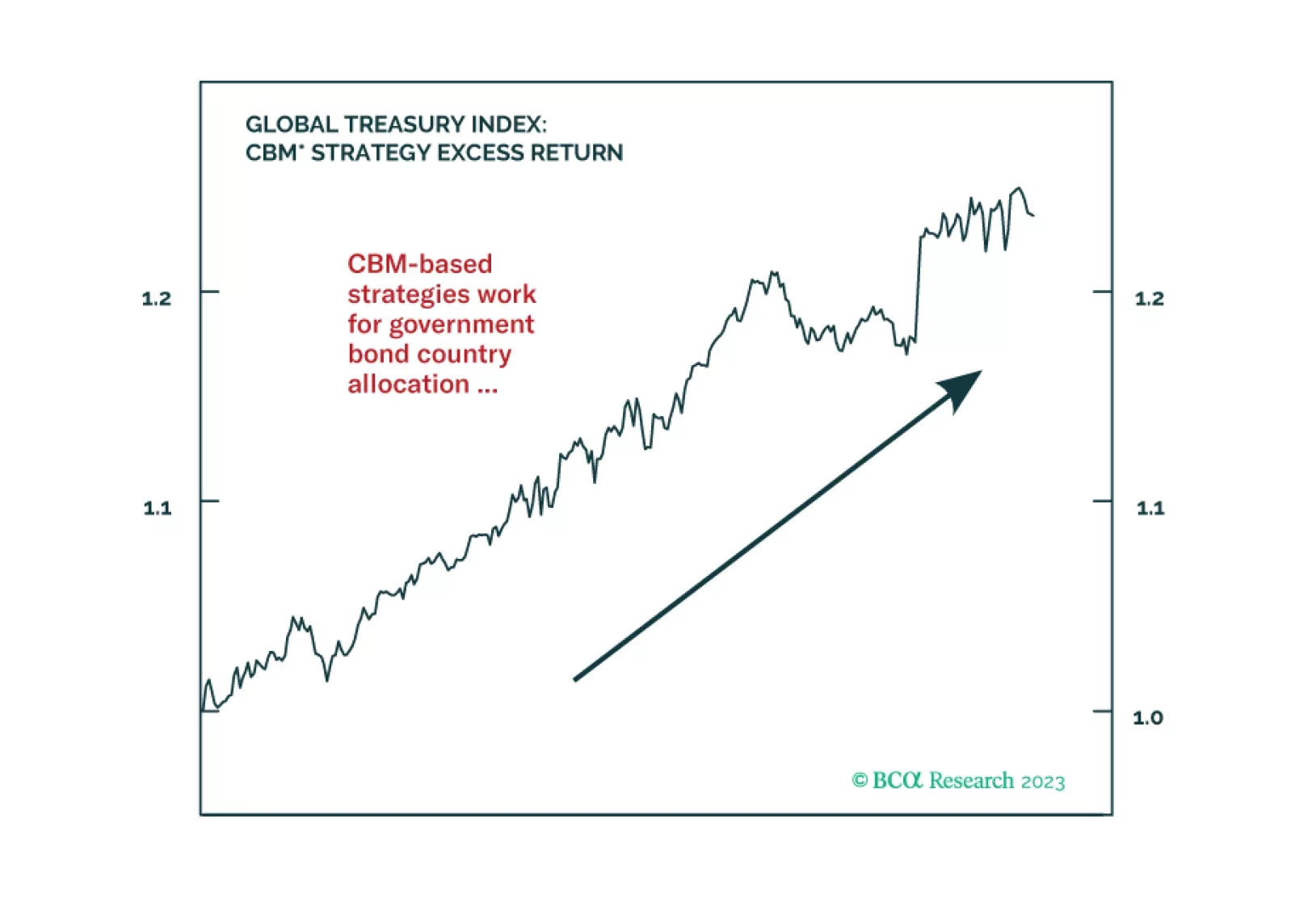

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

In this update to the two Special Reports on FX hedging of global equity portfolios with nine different home currencies, published in 2017, we show that BCA’s proprietary dynamic FX hedging strategies have consistently added value to global equity portfolios. We value quant models as an important input in our decision-making process, but we do not suggest any investor to slavishly follow them, because models cannot capture all the important fundamental changes, as demonstrated in the details of this report.