Policy

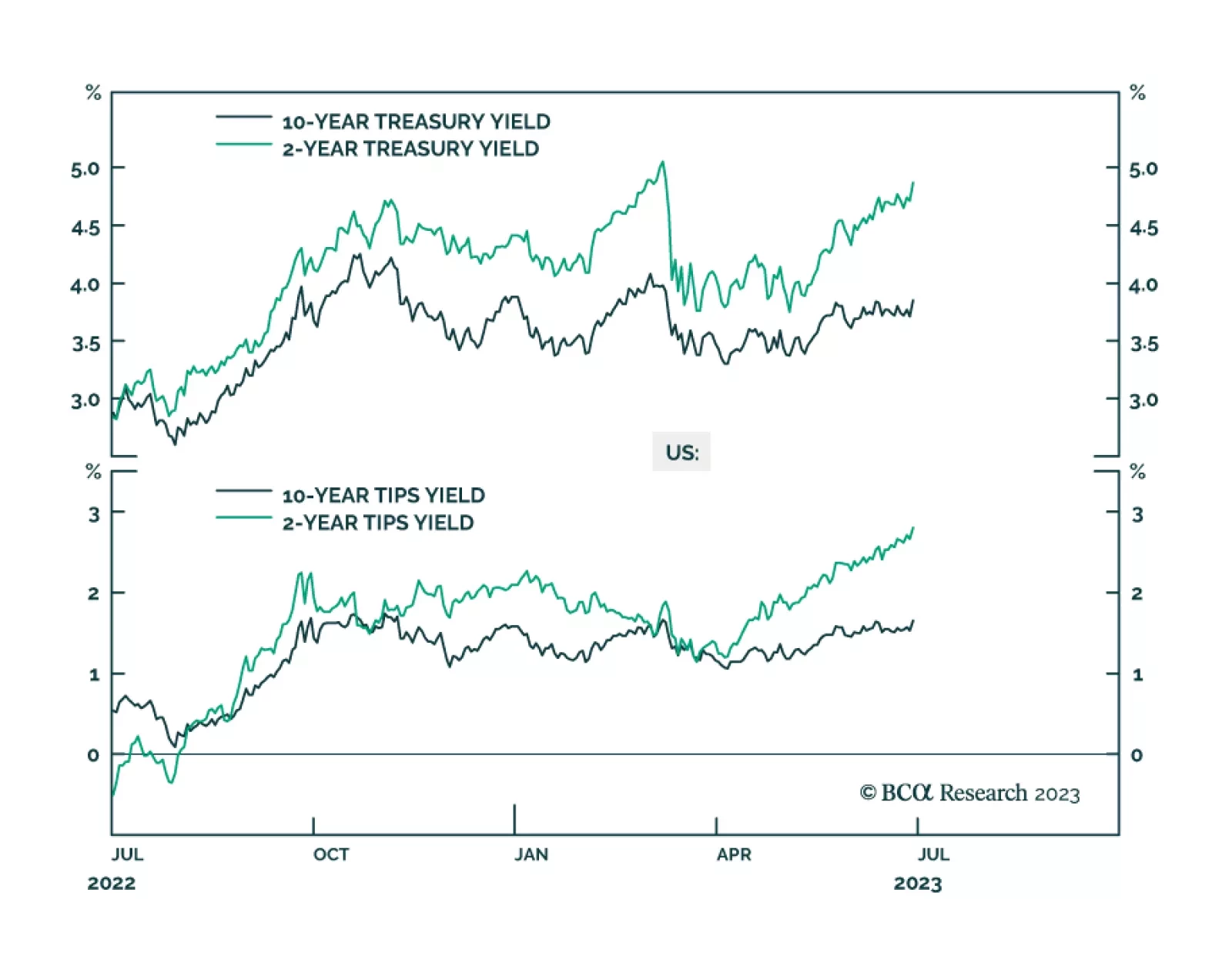

A look at how US bond yields responded to yesterday’s strong economic data and this morning’s soft inflation print.

We build a four-stage business cycle framework based on economic growth and capacity utilization, and then analyze historical returns for most major asset allocation decisions for each stage. Given that we are in the early recession stage (negative growth coupled and an overheated economy), our framework recommends a defensive positioning across all asset classes.

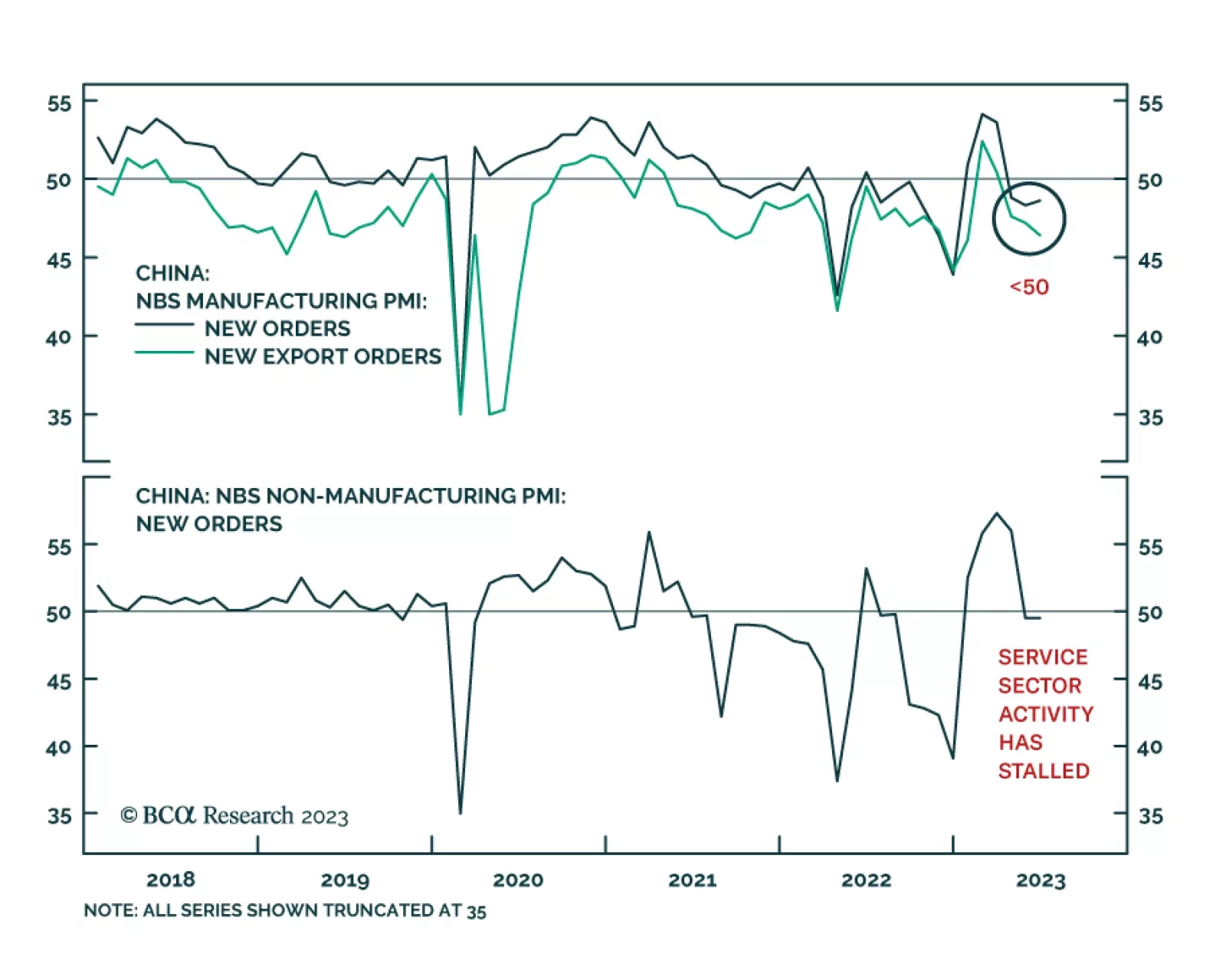

The combination of a global manufacturing recession and tight/tightening policy is raising a red flag for global non-TMT stocks. In China, households are entering a liquidity trap, and deflationary pressures are heightening. Authorities need to reduce interest rates considerably and allow the currency to depreciate. By doing so, China will export its deflation to the rest of the world.