Commodities & Energy Sector

Highlights The liquidity-driven rally will soon be followed by an acceleration in global growth. The economic recovery will bump up expectations of long-term profit growth. The dollar has downside, but the euro will not benefit much. Overweight stocks relative to bonds and bet on traditional cyclical sectors and commodities. The potential for outperformance of value relative to growth favors European equities. The probability of a tech mania is escalating: how should investors factor an expanding bubble into their portfolios? Feature Chart I-1A Bull Market In Stocks And Volatility?

A Bull Market In Stocks And Volatility?

A Bull Market In Stocks And Volatility?

Despite all odds, the nCoV-2019 outbreak is barely denting the S&P 500’s frenetic rally. Plentiful liquidity, thawing Sino-US trade relations and improving economic activity in Asia, all have created ideal conditions for risk assets to appreciate on a cyclical basis. Stocks may look increasingly expensive and are primed to correct, but the bubble will expand further. After lifting asset valuations, monetary policy easing will soon boost worldwide economic activity. Consequently, earnings in the US and Europe will improve. As long as central bankers remain unconcerned about inflation, investors will bid up stocks. Investors should remember we are in the final innings of a bull market. Stocks can deliver outsized returns during this period, but often at the cost of elevated volatility, and the options market is not pricing in this uncertainty (Chart I-1). Moreover, timing the ultimate end of the bubble is extremely difficult. Hence, we prefer to look for assets that can still benefit from easy monetary conditions and rebounding growth, but are not as expensive as equities. Industrial commodities fit that description, especially after their recent selloff. The dollar remains a crucial asset to gauge the path of least resistance for assets. If it refuses to swoon, then it will indicate that global growth is in a weaker state than we foresaw. The good news is that the broad trade-weighted dollar seems to have peaked. Accommodative Monetary Conditions Are Here To Stay Easy liquidity has been the lifeblood of the S&P 500’s rally. The surge in the index coincided with the lagged impact of the rise in our US Financial Liquidity Index (Chart I-2). Low rates have allowed stocks to climb higher, yet earnings expectations remain muted. For example, since November 26, 2018, the forward P/E ratio for the S&P 500 has increased from 15.2 to 18.7, while 10-year Treasury yields have collapsed from 3.1% to 1.6%. Meanwhile, expectations for long-term earnings annual growth extracted from equity multiples using a discounted cash flow model have dropped from 2.4% to 1.2%. Historically, easier monetary policy pushes asset prices higher before it lifts economic activity. Historically, easier monetary policy pushes asset prices higher before it lifts economic activity. Yet, stocks and risk assets normally continue to climb when the economy recovers. Even without any additional monetary easing, as long as policy remains accommodative, risk assets will generate positive returns. Expectations for stronger cash flow growth become the force driving asset prices higher. Policy will likely remain accommodative around the world. Within this framework, peak monetary easing is probably behind us, even though liquidity conditions remain extremely accommodative. Nominal interest rates remain very low, and real bond yields are still falling. Unlike in 2018 and 2019, dropping TIPs yields reflect rising inflation expectations (Chart I-3). Those factors together indicate that policy is reflationary, which is confirmed by the gold rally. Chart I-2A Liquidity Driven Rally

A Liquidity Driven Rally

A Liquidity Driven Rally

Chart I-3Today, Lower TIPS Yields Are Reflationary

Today, Lower TIPS Yields Are Reflationary

Today, Lower TIPS Yields Are Reflationary

Chart I-4Economic Activity To Respond To Liquidity

Economic Activity To Respond To Liquidity

Economic Activity To Respond To Liquidity

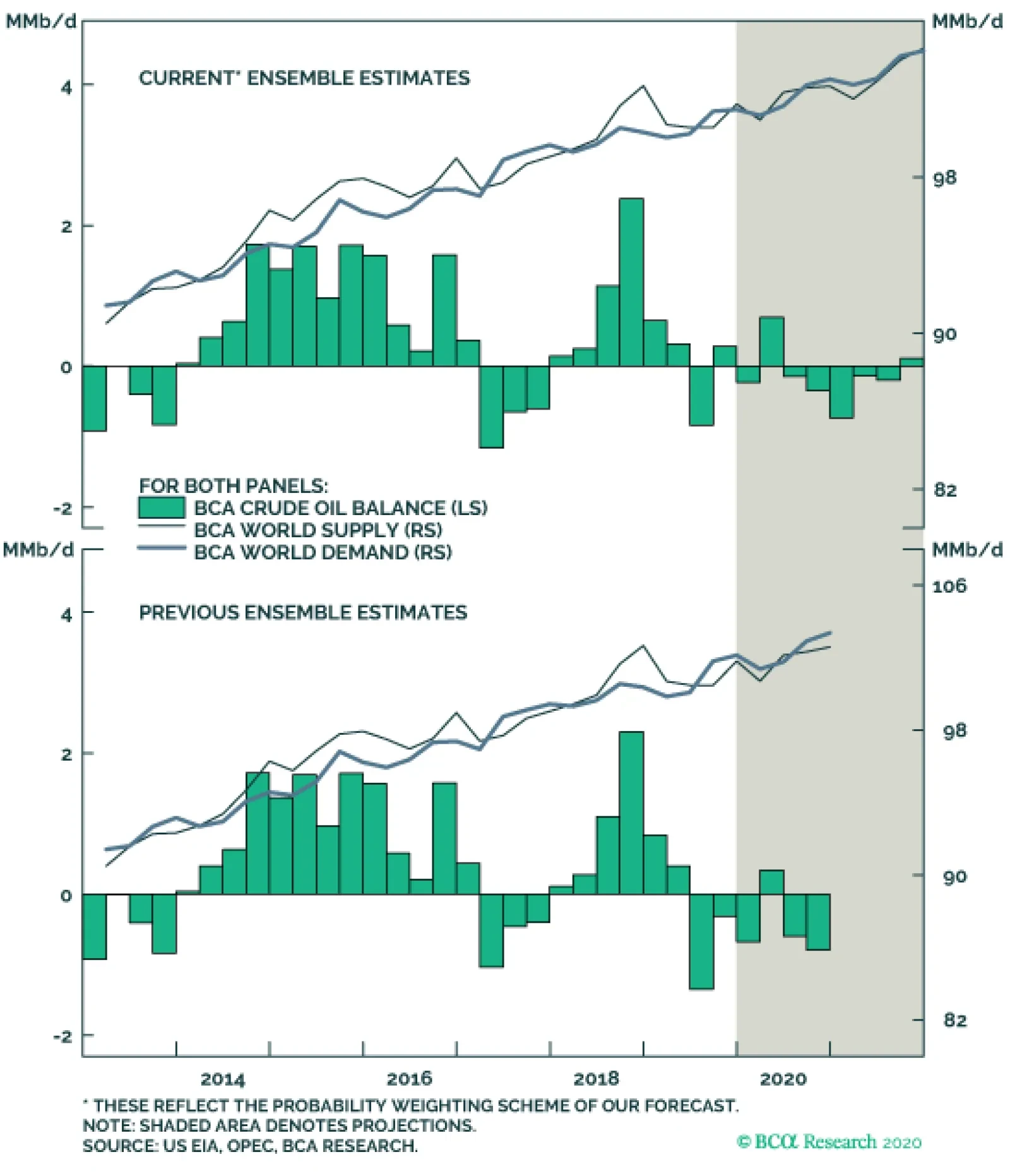

Based on the historical lags between monetary easing and manufacturing activity, the global industrial sector is set to mend (Chart I-4). Moreover, the liquidity-driven surge in stock prices, combined with low yields and compressed credit spreads, has eased financial conditions, which creates the catalyst for an industrial recovery. Where will the growth come from? First, worldwide inventory levels have collapsed after making negative contributions to growth since mid-2018 (Chart I-5). Thus, there is room for an inventory restocking. Secondly, auto sales in Europe and China have rebounded to 18.5% from -23% and to -0.1% from -16.4%, respectively. Thirdly, China’s credit and fiscal impulse has improved. The uptick in Chinese iron ore imports indicates that the pass-through from domestic reflation to global economic activity will materialize soon (Chart I-6). Finally, following the Phase One Sino-US trade deal, global business confidence is bottoming, as exemplified by Belgium’s business confidence, Switzerland KOF LEI, Korea's manufacturing business survey, or US CFO and CEO confidence measures. The increase in EM earnings revisions shows that US capex intentions should soon re-accelerate, which bodes well for investment both in the US and globally (Chart I-7). Chart I-5Room For Inventory Restocking

Room For Inventory Restocking

Room For Inventory Restocking

Chart I-6China Points To Stronger Global Growth

China Points To Stronger Global Growth

China Points To Stronger Global Growth

Construction activity, a gauge of the monetary stance, is looking up across the advanced economies. In the US, housing starts – a leading indicator of domestic demand – have hit a 13-year high. A pullback in this volatile data series is likely, but it should be limited. Vacancies remain at a paltry 1.4%, household formation is solid and affordability is not demanding (Chart I-8). In Europe, construction activity has been relatively stable through the economic slowdown. Even in Canada and Australia, housing transactions have gathered steam quickly following declines in mortgage rates (Chart I-9). Chart I-7Capex Is Set To Recover

Capex Is Set To Recover

Capex Is Set To Recover

Chart I-8US Housing Is Robust

US Housing Is Robust

US Housing Is Robust

Chart I-9Even The Canadian And Australian Housing Markets Are Stabilizing

Even The Canadian And Australian Housing Markets Are Stabilizing

Even The Canadian And Australian Housing Markets Are Stabilizing

Consumers will remain a source of strength for the global economy. The dichotomy between weak manufacturing PMIs and the stable service sector reflects a healthy consumer spending. December retail sales in Europe and the US corroborate this assessment. The stabilization in US business confidence suggests that household incomes are not in as much jeopardy as three months ago. As household net worth and credit growth improve further, a stable outlook for household income will underwrite greater gains in consumption. Policy will likely remain accommodative around the world. For the time being, US inflationary pressures are muted. The New York Fed’s Underlying Inflation Gauge has rolled over, hourly earnings growth has moved back below 3%, our pipeline inflation indicator derived from the ISM is weak, and core producer prices are flagging (Chart I-10). This trend is not US-specific. In the OECD, core consumer price inflation is set to decelerate due to the lagged impact of the manufacturing slowdown. Central banks are also constrained to remain dovish by their own rhetoric. The Fed's statement this week was a testament to this reality. Central banks are increasingly looking to set symmetrical inflation targets. After a decade of missing their targets, a symmetric target would imply keeping policy easier for longer, even if realized inflation moves back above 2%. A rebound in global growth and weak inflation should create a poisonous environment for the US dollar. Finally, fiscal policy will make a small positive contribution to growth in most major advanced economies in 2020, particularly in Germany and the UK (Table I-1). Chart I-10Limited Inflation Will Allow The Fed To Remain Easy

Limited Inflation Will Allow The Fed To Remain Easy

Limited Inflation Will Allow The Fed To Remain Easy

Table I-1Modest Fiscal Easing In 2020

February 2020

February 2020

The Dollar And The Sino-US Phase One Deal At first glance, a rebound in global growth and weak inflation should create a poisonous environment for the US dollar (Chart I-11). As we have often argued, the dollar’s defining characteristic is its pronounced counter-cyclicality. Chart I-11A Painful Backdrop For The Greenback

February 2020

February 2020

Deteriorating dollar fundamentals make this risk particularly relevant. US interest rates are well above those in the rest of the G10, but the gap in short rates has significantly narrowed. Historically, the direction of rates differentials and not their levels has determined the trend in the USD (Chart I-12). Moreover, real differentials at the long end of the curve support the notion that the maximum tailwinds for the dollar are behind us (Chart I-12, bottom panel). Furthermore, now that the US Treasury has replenished its accounts at the Federal Reserve, the Fed’s addition of excess reserves in the system will likely become increasingly negative for the dollar, especially against EM currencies. Likewise, relative money supply trends between the US, Europe, Japan and China already predict a decline in the dollar (Chart I-13). Chart I-12Interest Rate Differentials Do Not Favor The Dollar...

Interest Rate Differentials Do Not Favor The Dollar...

Interest Rate Differentials Do Not Favor The Dollar...

Chart I-13...Neither Do Money Supply Trends

...Neither Do Money Supply Trends

...Neither Do Money Supply Trends

Chart I-14The Phase One Deal Is Ambitious

February 2020

February 2020

The recent Sino-US trade agreement obscures what appears to be a straightforward picture. According to the Phase One deal signed mid-January, China will increase its US imports by $200 billion in the next two years vis-à-vis the high-water mark of $186 billion reached in 2017. This is an extremely ambitious goal (Chart I-14). Politically, it is positive that China has committed to buy manufactured goods and services in addition to commodities. However, the scale of the increase in imports of US manufactured goods is large, at $77 billion. China cannot fulfill this obligation if domestic growth merely stabilizes or picks up just a little, especially now that the domestic economy is in the midst of a spreading illness. It will have to substitute some of its European and Japanese imports with US goods. A consequence of this trade deal is that the euro’s gains will probably lag those recorded in normal business cycle upswings. Historically, European growth outperforms the US when China’s monetary conditions are easing and its marginal propensity to consume is rising (Chart I-15). However, given the potential for China to substitute European goods in favor of US ones, China’s economic reacceleration probably will not benefit Europe as much as it normally does. China may not ultimately follow through with as big of US purchases as it has promised, but it is likely, at least initially, to show good faith in the agreement. The euro’s gains will probably lag those recorded in normal business cycle upswings. While the trade agreement is a headwind for the euro, it is a positive for the Chinese yuan. The US output gap stands at 0.1% of potential GDP and the US labor market is near full employment. The US industrial sector does not possess the required spare capacity to fulfill additional Chinese demand. To equilibrate the market for US goods, prices will have to adjust to become more favorable for Chinese purchasers. The simplest mechanism to achieve this outcome is for the RMB to appreciate. Meanwhile, the euro is trading 16% below its equilibrium, which will allow European producers to fulfill US domestic demand. A widening US trade deficit with Europe would undo improvements in the trade balance with China. The probability that US equities correct further in the short-term is elevated. The implication for the dollar is that the broad trade-weighted USD will likely outperform the Dollar Index (DXY). The euro represents 18.9% of the broad trade-weighted dollar versus 57.6% of the DXY. Asian currencies, EM currencies at large, the AUD and the NZD, all should benefit from their close correlation with the RMB (Chart I-16). Chart I-15Europe Normally Wins When China Recovers

Europe Normally Wins When China Recovers

Europe Normally Wins When China Recovers

Chart I-16EM, Asian, And Antipodean Exchange Rates Love A Strong RMB

EM, Asian, And Antipodean Exchange Rates Love A Strong RMB

EM, Asian, And Antipodean Exchange Rates Love A Strong RMB

Obviously, before the RMB and the assets linked to it can appreciate further, the panic surrounding the coronavirus will have to dissipate. However, the economic damage created by SARS was short lived. This respiratory syndrome resulted in a 2.4% contraction Hong-Kong’s GDP in the second quarter of 2003. The economy of Hong Kong recovered that loss quickly afterward. Investment Forecasts BCA continues to forecast upside in safe-haven yields. Global interest rates remain well below equilibrium and a global economic recovery bodes poorly for bond prices (Chart I-17). However, inflation expectations and not real yields will drive nominal yield changes. The dovish slant of global central banks and the growing likelihood that symmetric inflation targets will become the norm is creating long-term upside risks for inflation. Moreover, if symmetric inflation targets imply lower real short rates in the future, then they also imply lower real long rates today. Investors should begin switching their risk assets into industrial commodity plays, especially after their recent selloff. Easy monetary conditions, decreased real rates and an improvement in economic activity are also consistent with an outperformance of assets with higher yields. High-yield bonds, which offer attractive breakeven spreads, will benefit from this backdrop (Chart I-18). Furthermore, carry trades will likely continue to perform well. In addition to low interest rates across most of the G10, the low currency volatility caused by an extended period of easy policy will continue to encourage carry-seeking strategies. Chart I-17Bonds Are Still Expensive

Bonds Are Still Expensive

Bonds Are Still Expensive

Chart I-18Where Is The Value In Credit?

Where Is The Value In Credit?

Where Is The Value In Credit?

An environment in which growth is accelerating and monetary policy is accommodative argues in favor of stocks. Our profit growth model for the S&P 500 has finally moved back into positive territory. As earnings improve, investors will likely re-rate depressed long-term growth expectations for cash flows (Chart I-19). The flip side is that equity risk premia are elevated, especially outside the US (Chart I-19). Hence, as long as accelerating growth (but not tighter policy) drives up yields, equities should withstand rising borrowing costs. The use of passive investing and the prevalence of “closet indexers” accentuates the risk that a tech mania could blossom. The 400 point surge in the S&P 500 since early October complicates the picture. The probability that US equities correct further in the short-term is elevated, based on their short-term momentum and sentiment measures, such as the put/call ratio (Chart I-20). Foreign equities will continue to correct along US ones, even if they are cheaper. Chart I-19Elevated Stock Multiples Reflect Low Yields, Not Growth Exuberance

Elevated Stock Multiples Reflect Low Yields, Not Growth Exuberance

Elevated Stock Multiples Reflect Low Yields, Not Growth Exuberance

Chart I-20Tactical Risks For Stocks

Tactical Risks For Stocks

Tactical Risks For Stocks

Chart I-21Buy Commodities/Sell Stocks?

Buy Commodities / Sell Stocks?

Buy Commodities / Sell Stocks?

The coronavirus panic seems to be the catalyst for such a correction. When a market is overextended, any shock can cause a pullback in prices. Moreover, as of writing, medical professionals still have to ascertain the virus’s severity and potential mutations. Therefore, risk assets must embed a significant risk premium for such uncertainty, even if ultimately the infection turns out to be mild. However, that risk premium will likely prove to be short lived. During the SARS crisis in 2003, stocks bottomed when the number of reported new cases peaked. The tech sector has plentiful downside if the correction gathers strength. As indicated in BCA’s US Equity Sector Strategy, Apple, Microsoft, Google, Amazon and Facebook account for 18% of the US market capitalization, which is the highest market concentration since the late 1990s tech bubble. Investors should begin switching their risk assets into industrial commodity plays, especially after their recent selloff. Commodity prices are trading at a large discount to US equities. Moreover, the momentum of natural resource prices relative to stocks has begun to form a positive divergence with the price ratio of these two assets (Chart I-21). Technical divergences such as the one visible in the ratio of commodities to equities are often positive signals. Low real rates, an ample liquidity backdrop, a global economic recovery, a weak broad trade-weighted dollar and a strong RMB, all benefit commodities over equities. Tech stocks underperform commodities when the dollar weakens and growth strengthens. Moreover, our positive stance on the RMB justifies stronger prices for copper, oil and EM equities (Chart I-22). Chart I-22The Winners From A CNY Rebound

February 2020

February 2020

Our US Equity Strategy Service has also reiterated its preference for industrials and energy stocks, and it recently upgraded materials stocks to neutral.1 All three sectors trade at significant valuation discounts to the broad market and to tech stocks in particular. They are also oversold in relative terms. Finally, their operating metrics are improving, a trend which will be magnified if global growth re-accelerates. Do not make these bets aggressively. A weakening broad trade-weighted dollar would allow for a rotation into foreign equities and an outperformance of value relative to growth stocks. The share of US equities in the MSCI All-Country World Index is a direct function of the broad trade-weighted dollar (Chart I-23). Moreover, since 1971, the dollar and the relative performance of growth stocks versus value stocks have exhibited a positive correlation (Chart I-24). Thus, the dollar’s recent strength has been a key component behind the run enjoyed by tech stocks. Chart I-23Global Stocks Love A Soft Dollar

Global Stocks Love A Soft Dollar

Global Stocks Love A Soft Dollar

Chart I-24Value Stocks Needs A Weaker Dollar To Outperform Growth Stocks

Value Stocks Needs A Weaker Dollar To Outperform Growth Stocks

Value Stocks Needs A Weaker Dollar To Outperform Growth Stocks

Despite the risks to the euro discussed in the previous section, European equities could still outperform US equities. Such a move would be consistent with value stocks beating growth equities (Chart I-24, bottom panel). This correlation exists because the euro area has a combined 17.7% weighting to tech and healthcare stocks compared with a 37.1% allocation in US benchmarks. Moreover, a cheap euro should allow European industrials and materials to outperform their US counterparts. Finally, the recent uptick in the European credit impulse indicates that an acceleration in European profit growth is imminent, a view that is in line with our preference for European financials (Chart I-25).2 Chart I-25Euro Area Profits Should Improve

Euro Area Profits Should Improve

Euro Area Profits Should Improve

Bottom Line: The current environment remains favorable for risk assets on a 12-month investment horizon. As such, we expect stocks and bond yields to continue to rise in 2020. Moreover, a pick-up in global growth, along with a fall in the broad trade-weighted dollar, should weigh on tech and growth stocks, and boost the attractiveness of commodity plays, industrial, energy and materials stocks, as well as European and EM equities. Forecast Meets Strategy Liquidity-driven rallies, such as the current one, can carry on regardless of the fundamentals. As Keynes noted 90 years ago: “Markets can remain irrational longer than you can stay solvent.” The gap between forecast and strategy can be great. The use of passive investing and the prevalence of “closet indexers” accentuates the risk that a tech mania could blossom. We assign a substantial 30% probability to the risk of another tech mania. Outflows from equity ETFs and mutual funds have been large. Investors will be tempted to move back into those vehicles if stocks continue to rally on the back of plentiful liquidity and improving global growth (Chart I-26). In the process, the new inflows will prop up the over-represented, over-valued, and over-extended tech behemoths. Chart I-26Depressed Equity Flows Should Pick Up

Depressed Equity Flows Should Pick Up

Depressed Equity Flows Should Pick Up

The current tech bubble can easily run a lot further. Based on current valuations, the NASDAQ trades at a P/E ratio of 31 compared with 68 in March 2000 (Chart I-27). Moreover, momentum is becoming increasingly favorable for the NASDAQ and other high-flying tech stocks. The NASDAQ is outperforming high-dividend stocks and after a period of consolidation, its relative performance is breaking out. Momentum often performs very well in liquidity-driven rallies. Chart I-27Where Is The Bubble?

Where Is The Bubble?

Where Is The Bubble?

Chart I-28Debt Loads Are Already High Everywhere

Debt Loads Are Already High Everywhere

Debt Loads Are Already High Everywhere

A full-fledged tech mania would make our overweight equities / underweight bonds a profitable call, but it would invalidate our sector and regional recommendations. Moreover, with a few exceptions in China and Taiwan, the major tech bellwethers are listed in the US. A tech bubble would most likely push our bearish dollar stance to the offside. Bubbles are dangerous: participating on the upside is easy, but cashing out is not. Moreover, financial bubbles tend to exacerbate the economic pain that follows the bust. During manic phases, capital is poorly invested and the economy becomes geared to the sectors that benefit from the financial excesses. These assets lose their value when the bubble deflates. Moreover, bubbles often result in growing private-sector indebtedness. Writing off or paying back this debt saps the economy’s vitality. Making matters worse, today overall indebtedness is unprecedented and central banks have little room to reflate the global economy once the bubble bursts (Chart I-28). Finally, US/Iran tensions will create additional risk in the years ahead. Matt Gertken, BCA’s Geopolitical Strategist, warns that the ratcheting down of tensions following Iran’s retaliation to General Soleimani’s assassination is temporary.3 As a result, the oil market remains a source of left-handed tail-risk. Section II discusses other potential black swans lurking in the geopolitical sphere. We continue to recommend that investors overweight industrials and energy, upgrade materials to neutral, Europe to overweight, and curtail their USD exposure as long as US inflation remains well behaved and the US inflation breakeven rate stays below the 2.3% to 2.5% range. However, do not make these bets aggressively. Moreover, some downside protection is merited. Due to our very negative view on bonds, we prefer garnering these hedges via a 15% allocation to gold and the yen. The yen is especially attractive because it is one of the few cheap, safe-haven plays (Chart I-29). Chart I-29The Yen Offers Cheap Portfolio Protection

The Yen Offers Cheap Portfolio Protection

The Yen Offers Cheap Portfolio Protection

Mathieu Savary Vice President The Bank Credit Analyst January 30, 2020 Next Report: February 27, 2020 II. Five Black Swans In 2020 Our top five geopolitical “Black Swans” are risks that the market is seriously underpricing. With the “phase one” trade deal signed, Chinese policy could become less accommodative, resulting in a negative economic surprise. The trade deal may fall victim to domestic politics, raising the risk of a US-China military skirmish. A Biden victory at the Democratic National Convention or a Democratic takeover of the White House could trigger social unrest and violence in the US. A pickup in the flow of migrants to Europe would fundamentally undermine political stability there. Russia’s weak economy will add fuel to domestic unrest, risking an escalation beyond the point of containment. Over the past four years, BCA’s Geopolitical Strategy service has started off each year with their top five geopolitical “Black Swans.” These are low-probability events whose market impact would be significant enough to matter for global investors. Unlike the great Byron Wien’s perennial list of market surprises, we do not assign these events a “better than 50% likelihood of happening.” We offer risks that the market is seriously underpricing by assigning them only single-digit probabilities when we think the reality is closer to 10%-15%, a level at which a risk premium ought to be assigned. Some of our risks below are so obscure that it is not clear how exactly to price them. We exclude issues that are fairly probable, such as flare-ups in Indo-Pakistani conflict. The two major risks of the year – discussed in our Geopolitical Strategy’s annual outlook – are that either US President Donald Trump or Chinese President Xi Jinping overreaches in a major way. But what would truly surprise the market would be a policy-induced relapse in Chinese growth or a direct military clash between the two great powers. That is how we begin. Other risks stem from domestic affairs in the US, Europe, and Russia. Black Swan 1: China’s Financial Crisis Begins Chart II-1A Crackdown On Financial Risk Could Cause China's Economy To Derail

A Crackdown On Financial Risk Could Cause China's Economy To Derail

A Crackdown On Financial Risk Could Cause China's Economy To Derail

The risk of Xi Jinping’s concentration of power in his own person is that individuals can easily make mistakes, especially if unchecked by advisors or institutions. Lower officials will fear correcting or admonishing an all-powerful leader. Inconvenient information may not be relayed up the hierarchy. Such behavior was rampant in Chairman Mao Zedong’s time, leading to famine among other ills. Insofar as President Xi’s cult of personality successfully imitates Mao’s, it will be subject to similar errors. If President Xi overreaches and makes a policy mistake this year, it could occur in economic policy or other policies. We begin with economic policy, as we have charted the risks of Xi’s crackdown on the financial system since early 2017 (Chart II-1). This year is supposed to be the third and final year of Xi Jinping’s “three battles” against systemic risk, pollution, and poverty. The first battle actually focuses on financial risk, i.e. China’s money and credit bubble. The regime has compromised on this goal since mid-2018, allowing monetary easing to stabilize the economy amid the trade war. But with a “phase one” trade deal having been signed, there is an underrated risk that economic policy will return to its prior setting, i.e. become less accommodative (Chart II-2). When Xi launched the “deleveraging campaign” in 2017, we posited that the authorities would be willing to tolerate an annual GDP growth rate below 6%. This would not only cull excesses in the economy but also demonstrate that the administration means business when it says that China must prioritize quality rather than quantity of growth. While Chinese authorities are most likely targeting “around 6%” in 2020, it is entirely possible that the authorities will allow an undershoot in the 5.5%-5.9% range. They will argue that the GDP target for 2020 has already been met on a compound growth rate basis (Chart II-3), as astute clients have pointed out. They may see less need for stimulus than the market expects. Chart II-2Easing Of Trade Tensions May Re-Incentivize Tighter Policy

Easing Of Trade Tensions May Re-Incentivize Tighter Policy

Easing Of Trade Tensions May Re-Incentivize Tighter Policy

Chart II-3Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Similarly, while urban disposable income is ostensibly lagging its target of doubling 2010 levels by 2020, China’s 13th Five Year Plan, which concludes in 2020, conspicuously avoided treating urban and rural income targets separately. If the authorities focus only on general disposable income, then they are on track to meet their target (Chart II-4). This would reduce the impetus for greater economic support. The Xi administration may aim only for stability, not acceleration, in the economy. There are already tentative signs that Chinese authorities are “satisfied” with the amount of stimulus they have injected: some indicators of money and credit have already peaked (Chart II-5). The crackdown on shadow banking has eased, but informal lending is still contracting. The regime is still pushing reforms that shake up state-owned enterprises. Chart II-4Lower Impetus For Economic Support Due To Improvements In National Income?

Lower Impetus For Economic Support Due To Improvements In National Income?

Lower Impetus For Economic Support Due To Improvements In National Income?

Chart II-5Has China's Stimulus Peaked?

chart 5

Has China's Stimulus Peaked?

Has China's Stimulus Peaked?

An added headwind for the Chinese economy stems from the currency. The currency should track interest rate differentials. Beijing’s incremental monetary stimulus, in the form of cuts to bank reserve requirement ratios (RRRs), should also push the renminbi down over time (Chart II-6). However, an essential aspect of any trade deal with the Trump administration is the need to demonstrate that China is not competitively devaluing. Hence the CNY-USD could overshoot in the first half of the year. This is positive for global exports to China, but it tightens Chinese financial conditions at home. A stronger than otherwise justified renminbi would add to any negative economic surprises from less accommodative monetary and fiscal policy. Conventional wisdom says China will stimulate the economy ahead of two major political events: the centenary of the Communist Party in 2021 and the twentieth National Party Congress in 2022. The former is a highly symbolic anniversary, as Xi has reasserted the supremacy of the party in all things, while the latter is more significant for policy, as it is a leadership reshuffle that will usher in the sixth generation of China’s political elite. But conventional wisdom may be wrong – the Xi administration may aim only for stability, not acceleration, in the economy. It would make sense to save dry powder for the next US or global recession. The obvious implication is that China’s economic rebound may lose steam as early as H2 – but the black swan risk is that negative surprises could cause a vicious spiral inside of China. This is a country with massive financial and economic imbalances, a declining potential growth profile, and persistent political obstacles to growth both at home and abroad. Corporate defaults have spiked sharply. While the default rate is lower than elsewhere, the market may be sniffing out a bigger problem as it charges a much higher premium for onshore Chinese bonds (Chart II-7). Chart II-6CNY/USD Overshoot Would Tighten Chinese Financial Conditions

CNY-USD Overshoot Would Tighten Chinese Financial Conditions

CNY-USD Overshoot Would Tighten Chinese Financial Conditions

Chart II-7Is China's Bond Market Sniffing Out A Problem?

Is China's Bond Market Sniffing Out A Problem?

Is China's Bond Market Sniffing Out A Problem?

Bottom Line: Our view is that China’s authorities will remain accommodative in 2020 in order to ensure that growth bottoms and the labor market continues to improve. But Beijing has compromised its domestic economic discipline since 2018 in order to fight trade war. The risk now, with a “phase one” deal in hand, is that Xi Jinping returns to his three-year battle plan and underestimates the downward pressures on the economy. The result would be a huge negative surprise for the Chinese and global economy in 2020. Black Swan 2: The US And China Go To War In 2013, we predicted that US-China conflict was “more likely than you think.” This was not just an argument for trade conflict or general enmity that raises the temperature in the Asia-Pacific region – we included military conflict. At the time, the notion that a Sino-American armed conflict was the world’s greatest geopolitical threat seemed ludicrous to many of our clients. We published this analysis in October of that year, months after the Islamic State “Soldier’s Harvest” offensive into Iraq. Trying to direct investors to the budding rivalry between American and Chinese naval forces in the South China Sea amidst the Islamic State hysteria was challenging, to say the least. Chart II-8Americans’ Attitudes Toward China Plunged…

February 2020

February 2020

The suggestion that an accidental skirmish between the US and China could descend into a full-blown conflict involved a stretch of the imagination because China was not yet perceived by the American public as a major threat. In 2014, only 19%of the US public saw China as the “greatest threat to the US in the future.” This came between Russia, at 23%, and Iran, at 16%. Today, China and Russia share the top spot with 24%. Furthermore, the share of Americans with an unfavorable view of China has increased from 52% to 60% in the six intervening years (Chart II-8). The level of enmity expressed by the US public toward China is still lower than that toward the Soviet Union at the onset of the Cold War in the 1950s (Chart II-9). However, the trajectory of distrust is clearly mounting. We expect this trend to continue: anti-China sentiment is one of the few sources of bipartisan agreement remaining in Washington, DC (Chart II-10). Chinese sentiment toward the United States has also darkened dramatically. The geopolitical rivalry is deepening for structural reasons: as China advances in size and sophistication, it seeks to alter the regional status quo in its favor, while the US grows fearful and seeks to contain China. Chart II-9…But Not Yet To War-Inducing Levels

February 2020

February 2020

Chart II-10Distrust Of China Is Bipartisan

February 2020

February 2020

Chart II-11Newfound American Concern For China’s Repression

February 2020

February 2020

One example of rising enmity is the US public’s newfound concern for China’s domestic policies and human rights, specifically Beijing’s treatment of its Uyghur minority in Xinjiang. A Google Trends analysis of the term “Uyghur” or “Uyghur camps” shows a dramatic rise in mentions since Q2 of 2018, around the same time the trade war ramped up in a major way (Chart II-11). While startling revelations of re-education camps in Xinjiang emerged in recent years, the reality is that Beijing has used heavy-handed tactics against both militant groups and the wider Uyghur minority since at least 2008 – and much earlier than that. As such, the surge of interest by the general American public and legislators – culminating in the Uyghur Human Rights Policy Act of 2019 – is a product of the renewed strategic tension between the two countries. The same can be said for Hong Kong: the US did not pass a Hong Kong Human Rights and Democracy Act in 2014, during the first round of mass protests, which prompted Beijing to take heavy-handed legal, legislative, and censorship actions. It passed the bill in 2019, after the climate in Washington had changed. Why does this matter for investors? There are two general risks that come with a greater public engagement in foreign policy. First, the “phase one” trade deal between China and the US could fall victim to domestic politics. This deal envisions a large step up in Sino-American economic cooperation. But if China is to import around $200 billion of additional US goods and services over the next two years – an almost inconceivable figure – the US and China will have to tamp down on public vitriol. This is notably the case if the Democratic Party takes over the White House, given its likely greater focus on liberal concerns such as human rights. And yet the latest bills became law under President Trump and a Republican Senate, and we fully expect a second Trump term to involve a re-escalation of trade tensions to ensure compliance with phase one and to try to gain greater structural concessions in phase two. Second, mounting nationalist sentiment will make it more difficult for US and Chinese policymakers to reduce tensions following a potential future military skirmish, accidental or otherwise. While our scenario of a military conflict in 2013 was cogent, the public backlash in the United States was probably manageable.3 Today we can no longer guarantee that this is the case. The “phase one” trade deal risks falling victim to domestic politics due to greater public engagement in foreign policy. China has greater control over the domestic narrative and public discourse, but the rise of the middle class and the government’s efforts to rebuild support for the single-party regime have combined to create an increase in nationalism. Thus it is also more difficult for Chinese policymakers to contain the popular backlash if conflict erupts. In short, the probability of a quick tamping down of public enmity is actively being reduced as American public vilification of China is closing the gap with China’s burgeoning nationalism at an alarming pace. Another of our black swan risks – Taiwan island – is inextricably bound up in this dangerous US-China dynamic. To be clear, Washington will tread carefully, as a conflict over Taiwan could become a major war. Nevertheless Taiwan’s election, as we expected, has injected new vitality into this already underrated geopolitical risk. It is not only that a high-turnout election (Chart II-12) gave President Tsai Ing-wen a greater mandate (Chart II-13), or that her Democratic Progressive Party retained its legislative majority (Chart II-14). It is not only that the trigger for this resounding victory was the revolt in Hong Kong and the Taiwanese people’s rejection of the “one country, two systems” formula for Taiwan. It is also that Tsai followed up with a repudiation of the mainland by declaring, “We don’t have a need to declare ourselves an independent state. We are an independent country already and we call ourselves the Republic of China, Taiwan.” Chart II-12Tsai Ing-Wen Enjoys A Greater Mandate On Higher Turnout…

February 2020

February 2020

Chart II-13…Popular Support…

February 2020

February 2020

Chart II-14…And A Legislative Majority

February 2020

February 2020

This statement is not a minor rhetorical flourish but will be received as a major provocation in Beijing: the crystallization of a long-brewing clash between Beijing and Taipei. Additional punitive economic measures against Taiwan are now guaranteed. Saber-rattling could easily ignite in the coming year and beyond. Taiwan is the epicenter of the US-China strategic conflict. First, Beijing cannot compromise on its security or its political legitimacy and considers the “one China principle” to be inviolable. Second, the US maintains defense relations with Taiwan (and is in the process of delivering on a relatively large new package of arms). Third, the US’s true willingness to fight a war on Taiwan’s behalf is in doubt, which means that deterrence has eroded and there is greater room for miscalculation. Bottom Line: A US-China military skirmish has been our biggest black swan risk since we began writing the BCA Geopolitical Strategy. The difference between then and now, however, is that the American public is actually paying attention. Political ideology – the question of democracy and human rights – is clearly merging with trade, security, and other differences to provoke Americans of all stripes. This makes any skirmish more than just a temporary risk-off event, as it could lead to a string of incidents or even protracted military conflict. Black Swan 3: Social Unrest Erupts In America There are numerous lessons that one can learn from the ongoing unrest in Hong Kong, but perhaps the most cogent one is that Millennials and Generation Z are not as docile and feckless as their elders think. Images of university students and even teenagers throwing flying kicks and Molotov cocktails while clad in black body armor have shocked the world. Perhaps all those violent video games did have a lasting impact on the youth! What is surprising is that so few commentators have made the cognitive leap from the ultra-first world streets of Hong Kong to other developed economies. Perhaps what is clouding analysts’ minds is the idiosyncratic nature of the dispute in Hong Kong, the “one China” angle. However, Hong Kong youth are confronted with similar socio-economic challenges that their peers in other advanced economies face: overpriced real estate and a bifurcated service-sector labor market with few mid-tier jobs that pay a decent wage. There is a risk of rebellion from Trump’s most ardent supporters if he loses the White House. In the US, Millennials and Gen Z are also facing challenges unique to the US. First, their debt burden is much more toxic than that of the older cohorts, given that it is made up of student loans and credit card debt (Chart II-15). Second, they find themselves at odds – demographically and ideologically – with the older cohorts (Chart II-16). Chart II-15Younger American Cohorts Plagued By Toxic Debt

February 2020

February 2020

Chart II-16Younger And Older Cohorts At Odds Demographically

February 2020

February 2020

Chart II-17Massive Turnout To The 2016 Referendum On Trump

February 2020

February 2020

The adage that the youth are apolitical and do not turn out to vote may have ended thanks to President Trump. The 2018 midterm election, which the Democratic Party successfully turned into a referendum on the president, saw the youth (18-29) turnout nearly double from 20% to 36% (the 30-44 year-old cohort also saw a jump in turnout from 35.6% to 48.8%). The election saw one of the highest turnouts in recent memory, with a 53.4% figure, just two points off the 2016 general election figure (Chart II-17). Despite the high turnout in 2018, the-most-definitely-not-Millennial Vice President Joe Biden continues to lead the Democratic Party in the polls. His probability of winning the nomination is not overwhelming, but it is the highest of any contender. In recent polls, Biden comes third place in Millennial/Gen-Z vote preferences (Chart II-18). Yet he is hardly out of contention, especially for the 30-44 year-old cohort. The view that “Uncle Joe” does not fit the Democratic Party zeitgeist has become so entrenched in the Democratic Party narrative that it became conventional wisdom last year, pulling oddsmakers and betting markets away from the clear frontrunner (Chart II-19). Chart II-18Biden Unpopular Among Young American Voters

February 2020

February 2020

Chart II-19Bookies Pulled Down 'Uncle Joe’s' Odds, Capturing Democratic Party Zeitgeist

February 2020

February 2020

As such, a Biden victory at the Democratic National Convention in Milwaukee, Wisconsin on July 13-16 may come as an affront to the left-wing activists who will surely descend on the convention. This will particularly be the case if Biden wins despite the progressive candidates amassing a majority of overall delegates, which is possible judging by the combined progressive vote share in current polling (Chart II-20). He would arrive in Milwaukee without clearing the 1990 delegate count required to win on the first ballot. On the second ballot, his presidency would then receive a boost from “superdelegates” and those progressives who are unwilling to “rock the boat,” i.e. unify against an establishment candidate with the largest share of votes. This is also how Mayor Michael Bloomberg could pull off a surprise win. Chart II-20Progressives Come Closest To Victory

February 2020

February 2020

Such a “brokered” – or contested – convention has not occurred since 1952. However, several Democratic Party conventions came close, including 1968, 1972, and 1984. The 1968 one in Chicago was notable for considerable violence and unrest. Even if the Milwaukee Democratic Party convention does not produce unrest, it could sow the seeds for unrest later in the year. First, a breakout Biden performance in the primaries is unlikely. As such, he will likely need to pledge a shift to the left at the convention, including by accepting a progressive vice-presidential candidate. Second, an actual progressive may win the primary. Chart II-21Zealots In Both Parties Perceive Each Other As A National Threat

February 2020

February 2020

It is likely that either of the two options would be seen as an existential threat to many of Trump’s loyal supporters across the United States. President Trump’s rhetoric often paints the scenario of a Democratic takeover of the White House in apocalyptic terms. And data suggests that the zealots in both parties perceive each other as a “threat to the nation’s wellbeing” (Chart II-21). The American Civil War in the nineteenth century began with the election of a president. This is not just because Abraham Lincoln was a particularly reviled figure in the South, but because the states that ultimately formed the Confederacy saw in his election the demographic writing-on-the-wall. The election was an expression of a general will that, from that point onwards, was irreversible. Given demographic trends in the US today, it is possible that many would see in Trump’s loss a similar fait accompli. If one perceives progressive Democrats as an existential threat to the US constitution, rebellion is the obvious and rational response. Bottom Line: Year 2020 may be a particularly violent one for the US. First, left wing activists may be shocked and angered to learn that Joe Biden (or Bloomberg) is the nominee of the Democratic Party come July. With so much hype behind the progressive candidates throughout the campaign, Biden’s nomination could be seen as an affront to what was supposed to be “the big year” for left-wing candidates. Second, investors have to start thinking about what happens if Biden – or a progressive candidate – goes on to defeat President Trump in the general election. While liberal America took Trump’s election badly, it has demographics – and thus time – on its side. Trump’s most ardent supporters may conclude that his defeat means the end of America as they know it. Black Swan 4: Europe’s Migration Crisis Restarts It is a testament to Europe’s resilience that we do not have a Black Swan scenario based on an election or a political crisis set on the continent in 2020. Support for the common currency and the EU as a whole has rebounded to its highest since 2013. Even early elections in Germany and Italy are unlikely to produce geopolitical risk. The populists in the former are in no danger of outperforming whereas the populists in the latter barely deserve the designation. But what if one of the reasons for the surge in populism – unchecked illegal immigration – were to return in 2020? Chart II-22Decline In Illegal Immigration Dampened European Populism

February 2020

February 2020

The data suggests that the risk of migrant flows has massively subsided. From its peak of over a million arrivals in 2015, the data shows that only 125,472 migrants crossed into Europe via land and sea routes in the Mediterranean last year (Chart II-22). Why? There are five reasons that we believe have checked the flow of migrants: Supply: The civil wars in Syria, Iraq, and Libya have largely subsided. Heterogenous regions, cities, and neighborhoods have been ethnically cleansed and internal boundaries have largely ossified. It is unlikely that any future conflict will produce massive outflows of refugees as the displacement has already taken place. These countries are now largely divided into armed, ethnically homogenous, camps. Enforcement: The EU has stepped up border enforcement since 2015, pouring resources into the land border with Turkey and naval patrols across the Mediterranean. Individual member states – particularly Italy and Hungary – have also stepped up border enforcement policy. While most EU member states have publicly chided both for “draconian” policies, there is no impetus to force Rome and Budapest to change policy. Libyan Imbroglio: Conflict in Libya has flared up in 2019 with military warlord Khalifa Haftar looking to wrest control from the UN-backed Government of National Accord led by Fayez al-Serraj. The Islamic State has regrouped in the country as well. Ironically, the conflict is helping stem the flow of migrants as African migrants from sub-Saharan countries dare not cross into Libya as they did in 2015 when there was a brief lull in fighting. Turkish benevolence: Ankara is quick to point out that it is the only thing standing between Europe and a massive deluge of migrants. Turkey is said to host somewhere between two and four million refugees from various conflicts in the Middle East. Fear of the crossing: If crossing the Mediterranean was easy, Europe would have experienced a massive influx of migrants throughout the twentieth century. Not only is it not easy, it is costly and quite deadly, with thousands lost each year. Furthermore, most migrants are not welcomed when they arrive to Europe, many are held in terrible conditions in holding camps in Italy and Greece. Over time, migrants who made it into Europe have reported these dangers and conditions, reducing the overall demand for illegal migration. We do not foresee these five factors changing, at least not all at once. However, there are several reasons to worry about the flow of migrants in 2020. US-Iran tensions have sparked outright military action, while unrest is flaring up across Iran’s sphere of influence. Going forward, Iran could destabilize Iraq or fuel Shia unrest against US-backed regimes. Second, Afghanistan has been the source of most migrants to Europe via sea and land Mediterranean routes – 19.2%. The conflict in the country continues and may flare up with President Trump’s decision to formally withdraw most US troops from the country in 2020. Third, a break in fighting in Libya may encourage sub-Saharan migrants to revisit routes to Europe. Migrants from Guinea, Cote d’Ivoire, and the Democratic Republic of Congo make up over 10% of migrants to Europe. Finally, Turkish relationship with the West could break up further in 2020, causing Ankara to ship migrants northward. We highly doubt that President Erdogan will risk such a break, given that 50% of Turkish exports go to Europe. A European embargo on Turkish exports – which would be a highly likely response to such an act – would crush the already decimated Turkish economy. Bottom Line: While we do not see a return to the 2015 level of migration in 2020, we flag this risk because it would fundamentally undermine political stability in Europe. Black Swan 5: Russia Faces A “Peasant Revolt” Our fifth and final black swan risk for the year stems from Russia. This risk may seem obvious, since the US election creates a dynamic that revives the inherent conflict in US-Russian relations. Russia could seek to accomplish foreign policy objectives – interfering in US elections, punishing regional adversaries. The Trump administration may be friendly toward Russia but Trump is unlikely to veto any sanctions passed by the House and Senate in an election year, should an occasion for new sanctions arise. Conversely Russia could anticipate greater US pressure if the Democrats win in November. Yet it is Russia’s domestic affairs that represent the real underrated risk. Putin’s fourth term as president has been characterized by increased focus on domestic political control and stability as opposed to foreign adventurism. The creation of a special National Guard in 2016, reporting directly to Putin and responsible for quelling domestic unrest, symbolizes the shift in focus. So too does Russia’s adherence to the OPEC 2.0 regime of production control to keep oil prices above their budget breakeven level. Meanwhile Putin’s courting of Europe for the Nordstream II pipeline, and his slight peacemaking efforts with Ukraine, has suggested a slightly more restrained international posture. Strategically it makes little sense for Russia to court negative attention at a time when the US and Europe are at odds over trade and the Middle East, the US is preoccupied with China and Iran, and Russia itself faces mounting domestic problems. The domestic problems are long in coming. The central bank has maintained a stringent monetary policy for the better part of the decade. Despite cutting interest rates recently, monetary and credit conditions are still tight, hurting domestic demand. Moscow has also imposed fiscal austerity, namely by cutting back on state pensions and hiking the value added tax. Real wage growth is weak (Chart II-23), retail sales are falling, and domestic demand looks to weaken further, as Andrija Vesic of BCA Emerging Markets Strategy observes in a recent Special Report. The effect of Russia’s policy austerity has been a drop in public approval of the administration (Chart II-24). Protests erupted in 2019 but were largely drowned out by the larger and more globally significant protests in Hong Kong. These were met by police suppression that has not removed their underlying cause. Putin’s first major decision of the new year was to reshuffle the government, entailing Prime Minister Dmitri Medvedev’s transfer to a new post and the appointment of a new cabinet. This move reveals the need to show some accountability to reduce popular pressure. While Moscow now has room to cut interest rates and ease fiscal policy, it is behind the curve and the weak economy will add fuel to domestic unrest. Chart II-23Sluggish Wage Growth Threatens Russian Stability

Sluggish Wage Growth Threatens Russian Stability

Sluggish Wage Growth Threatens Russian Stability

Chart II-24Austerity Weighed On The Administration's Popularity In Russia

Austerity Weighed On The Administration's Popularity In Russia

Austerity Weighed On The Administration's Popularity In Russia

Meanwhile Putin’s efforts to alter the Russian constitution so he can stay in power beyond current term limits, effectively becoming emperor for life, like Xi Jinping, should not be dismissed merely because they are expected. They reflect a need to take advantage of Putin’s popular standing to consolidate domestic political power at a time when the ruling United Russia party and the federal government face discontent. They also ensure that strategic conflict with the United States will take on an ideological dimension. Russia's recent cabinet shakeup is positive from the point of view of economic reform. And the country's monetary and fiscal room provide a basis for remaining overweight equities within EM, as our Emerging Markets Strategy recommends. However, Russian equities have rallied hard and the political risk is understated. Chart II-25Russian Political Risk Is Unsustainably Low

Russian Political Risk Is Unsustainably Low

Russian Political Risk Is Unsustainably Low

Bottom Line: It is never easy predicting Putin’s next international move. Our market-based indicators of Russian political risk have hit multi-year lows, but both the domestic and international context suggest that these lows will not be sustained (Chart II-25). A new bout of risk can emanate from Putin, or from changes in Washington, or from the Russian people themselves. What would take the world by surprise would be domestic unrest on a larger scale than Russia can easily suppress through the police force. Housekeeping We are closing our long European Union / short Chinese equities strategic trade with a 1.61% loss since inception on May 10, 2019. Dhaval Joshi of BCA’s European Investment Strategy downgraded the Eurostoxx 50 to underweight versus the S&P 500 and the Nikkei 225 this week. He makes the point that the Euro Area bond yield 6-month impulse hit 100 bps – a critical technical level – and will be a strong headwind to growth. We will look to reopen this trade at a later date when the euphoria over the “phase one” trade deal subsides, as we still favor European equities and DM bourses over EM. We will reinstitute our long Brent crude H2 2020 versus H2 2021 tactical position, which was stopped out on January 9, 2020. We remain bullish on oil fundamentals and expect Middle East instability to add a political risk premium. China's stimulus and the oil view also give reason for us to reinitiate our long Malaysian equities relative to EM as a tactical position. The Malaysian ringgit will benefit as oil prices move higher, helping Malaysian companies make payments on their large pile of dollar-denominated debt and improving household purchasing power. Higher oil prices also correlate with higher equity prices, while China's stimulus and the US trade ceasefire will push the US dollar lower and help trade revive in the region. Marko Papic Chief Strategist, Clocktower Group Matt Gertken Geopolitical Strategist III. Indicators And Reference Charts The S&P 500 rally looks increasingly vulnerable from a tactical perspective. The US benchmark is overbought, and the percentage of NYSE stocks above their 30-week and 10-week moving averages is rolling over at elevated levels. Additionally, the number of NYSE new highs minus new lows has moved in a parabolic fashion and has hit levels that in previous years have warned of an imminent correction. The spread of nCoV-2019 is likely to be the catalyst to a pullback that could cause the S&P 500 to retest its October 2019 breakout. An improving outlook for global growth, limited inflationary pressures and global central banks who maintain an accommodative monetary stance bode well for stocks. Therefore, the anticipated equity correction will not morph into a bear market. For now, our Monetary Indicator remains at extremely elevated levels. Furthermore, our Composite Technical Indicator has strengthened. Additionally, our BCA Composite Valuation index suggests that stocks are expensive, but not so much as to cancel out the supportive monetary and technical backdrop. Finally, our Speculation Indicator is elevated, but is not so high as to warn of an imminent market top. This somewhat muted level of speculation is congruent with the expectation of low long-term growth rates for profits embedded in equity prices. In contrast to our Revealed Preference Indicator, our Willingness-to-Pay (WTP) is moving in accordance with our constructive cyclical stance for stocks. Indeed, the WTP for the US, Japan and Europe continues to improve. The WTP indicator tracks flows, and thus provides information on what investors are actually doing, as opposed to sentiment indexes that track how investors are feeling. This broad-based improvement therefore bodes well for equities. Meanwhile, net earnings revisions appear to be forming a trough. 10-year Treasury yields remain extremely expensive. Moreover, according to our Composite Technical Indicator, T-Note prices are losing momentum. The fear surrounding the spread of the new coronavirus has cause bonds to rally again, but this is likely to be the last hurrah for the Treasury markets before a major reversal takes hold. The rising risk premia linked to the coronavirus is also helping the dollar right now, but signs that global growth is bottoming, such as the stabilization in the global PMIs, the pick-up in the German ZEW and Belgium’s Business Confidence surveys, or the improvement in Asia’s export growth, point to a worsening outlook for the counter-cyclical US dollar. Moreover, the dollar trades at a large premium of 24.5% relative to its purchasing-power parity equilibrium. Additionally, the negative divergence between the dollar and our Composite Momentum Indicator suggests that the dollar is technically vulnerable. In fact, the very modest pick-up in the dollar in response to the severe fears created by the spreading illness in China argues that dollar buying might have become exhausted. Finally, commodity prices have corrected meaningfully in response to the stronger dollar and the growth fears created by the spread of the coronavirus. However, they have not pulled back below the levels where they traded when they broke out in late 2019. Moreover, the advance/decline line of the Continuous Commodity Index remains at an elevated level, indicating underlying strength in the commodity complex. Natural resources prices will likely become the key beneficiaries of both the eventual pullback in virus-related fears and the weaker dollar. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4Revealed Preference Indicator

Revealed Preference Indicator

Revealed Preference Indicator

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot

Chart III-30US Growth Outlook

US Growth Outlook

US Growth Outlook

Chart III-31US Cyclical Spending

US Cyclical Spending

US Cyclical Spending

Chart III-32US Labor Market

US Labor Market

US Labor Market

Chart III-33US Consumption

US Consumption

US Consumption

Chart III-34US Housing

US Housing

US Housing

Chart III-35US Debt And Deleveraging

US Debt And Deleveraging

US Debt And Deleveraging

Chart III-36US Financial Conditions

US Financial Conditions

US Financial Conditions

Chart III-37Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Chart III-38Global Economic Snapshot: China

Global Economic Snapshot: China

Global Economic Snapshot: China

Mathieu Savary Vice President The Bank Credit Analyst Footnotes 1 Please see US Equity Strategy Weekly Report "Three EPS Scenarios," dated January 13, 2020, available at uses.bcaresearch.com; US Equity Strategy Insight Report "Bombed Out Energy," dated January 8, 2020, available at uses.bcaresearch.com; US Equity Strategy Special Report "Industrials: Start Your Engines," dated January 21, 2020, available at uses.bcaresearch.com 2 Please see The Bank Credit Analyst Monthly Report "January 2020," dated December 20, 2019 available at bca.bcaresearch.com; The Bank Credit Analyst Monthly Report "OUTLOOK 2020: Heading Into The End Game," dated November 22, 2019 available at bca.bcaresearch.com 3 Please see Geopolitical Strategy "A Reprieve Amid The Bull Market In Iran Tensions," dated January 8, 2020, available at gps.bcaresearch.com 4 Observe how little attention the public paid to US-China saber-rattling around China’s announcement of an Air Defense Identification Zone in the East China Sea that year.

Highlights The US election cycle is an understated risk to US equities – and the risk of a left-wing populist outperforming in the Democratic primary election is frontloaded in February. The US-Iran conflict is unresolved and remains market-relevant. Iraq is at the center of the conflict and oil supply disruption there or elsewhere in the region is a substantial risk. Even if war does not erupt, Iran has the potential to give President Trump’s foreign policy a black eye and thus could marginally impact the election dynamic. Feature Stocks have rallied mightily since our August report on Trump’s “tactical trade retreat,” but new headwinds face the market. In this report we call attention to four hurdles arising from US election uncertainty. Then we focus on the status of Iran and Iraq in the wake of this month’s hostilities, which brought the US and Iran to the brink of outright war. We maintain that the Iran risk is unresolved and will remain market-relevant in advance of the US election. Primarily due to the US Democratic primary election, we urge caution on US equities in the near term, along with our Global Investment Strategy, despite our cyclically bullish House View. Four Hurdles In The US Election Cycle The US election cycle is the chief political risk to the bull market this year – and geopolitical risks largely radiate from it. There are four immediate hurdles that financial markets are underestimating: Risks to Trump's re-election: Global investors have come around to our view since 2018 that Trump is slightly favored to win re-election (Chart 1). Bets on the related question of which party will hold the White House have flipped from Democratic to Republican (Chart 2). Everyone now recognizes that Trump will not be removed from office through impeachment. Chart 1Trump Re-election Odds Add To Risk-On

Trump Re-election Odds Add To Risk-On

Trump Re-election Odds Add To Risk-On

Chart 2Republicans Now Favored For White House

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Yet, anecdotally, investors may be becoming complacent about Trump’s chances. He is not a shoo-in. Subjectively we have argued that his odds of victory are 55%. Our quantitative election model shows that Wisconsin has shifted to the Republican camp since November, but it places the odds of winning that state (and Pennsylvania) at less than 52% (Chart 3). This gives Trump 289 electoral votes, only 19 more than necessary. If both of these states tipped in the opposite direction then investors would be facing a major policy reversal in the United States. Chart 3Our US 2020 Election Model Shows Trump Win With 289 Electoral College Votes

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Chart 4The US Economy Is Still A Risk To Trump

The US Economy Is Still A Risk To Trump

The US Economy Is Still A Risk To Trump

Trump’s low approval rating remains a liability – and in this sense impeachment is still relevant, in that it can either help or hurt his approval, or prompt him to seek distractions abroad that could deliver negative surprises. Moreover the US manufacturing sector and labor market are not out of the woods yet (Chart 4). In short, the election is still ten months away and a lot can happen between now and then. We see Trump as only slightly favored. Moreover other hurdles are more immediate than the benefits of policy continuity upon a Trump win. 2. Risks to Biden's nomination: Throughout last year we maintained that former Vice President Joe Biden was the frontrunner for the Democratic nomination, albeit with very low conviction. In particular, after Vermont Senator Bernie Sanders’s poor showing in the third debate and subsequent heart attack, we expected Massachusetts Senator Elizabeth Warren to consolidate the progressive vote and trigger a policy-induced selloff in US equities. This never occurred because Biden held firm, Sanders recovered, and Warren fell. The risk to equities from a left-wing populist Democratic nominee is frontloaded in February and March. Now, however, the risk to equities is back. The Democratic Party faces a last-ditch effort from its left or “progressive” wing and anti-establishment voters to oppose Biden. With the primary election now upon us – the Iowa Caucus is February 3 – national opinion polls show that Sanders is pushing up against Biden (Chart 5). It is less clear if Sanders is breaking through in the primary polling state-by-state, where multiple candidates remain competitive (Chart 6). But online gamblers are reasserting Biden over Sanders at just the moment when progressives are set to launch their biggest push (Chart 7). Meanwhile New York Mayor Michael Bloomberg is finally gaining some traction – and he eats away at Biden’s support from centrist voters. Everything is in flux, which warrants caution. Chart 5Biden Is The Frontrunner, But Sanders Is Challenger

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Chart 6Biden Not A Shoo-In For Early Democratic Primary States

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Biden is still favored to win the nomination, but he has not clinched it. The market faces volatility during the period when Democrats get “cold feet” about nominating another establishment candidate. Moreover the fundamental knock against Sanders – that he is not as “electable” as Biden – is debatable, judging by head-to-head polls against Trump (Chart 8). This means that a shift in momentum – for instance, if Biden lurches from disappointments in early states to underperformance in his bulwark of South Carolina – would have legs. Ultimately a “contested convention” is not impossible. This would be a negative surprise to market participants currently assuming that the world faces the relatively benign choice of two known quantities: an establishment Democrat or a continuation of Trump policies. Chart 7Betting Markets Overlooking Party 'Cold Feet' Over Biden

Betting Markets Overlooking Party 'Cold Feet' Over Biden

Betting Markets Overlooking Party 'Cold Feet' Over Biden

Chart 8Electability Fears May Not Stop Sanders Rally

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Risks to the Republican Senate: Assuming Biden clinches the nomination, he has a 45% chance of winning the election – and in that case, his chance of bringing the Senate over to the Democrats is higher than investors realize. This is another risk that the market will awaken to later this year. Chart 9Democrats Underestimated In Senate

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

The consensus holds that Republicans will hold the Senate, particularly with Republican senators in Maine and Iowa leading their Democratic challengers in polling. The problem is that for Democrats to unseat an incumbent president they will necessarily have generated strong turnout from key demographic groups: young people, suburbanites, women, and minorities. If that is the case, then the election will not be as tight as expected and Republicans will be less likely to hold the Senate. This would require rising unemployment or some other blow that fundamentally damages the Trump administration’s popular support in key swing states. At least until it becomes clear that the manufacturing sector is out of the woods, the Democrats should be seen as far more likely to take the Senate than the Republicans are to retake the House of Representatives – yet this goes against the consensus (Chart 9). Rising odds of a Senate victory would mean that even a “centrist” Democrat like Biden would have fewer political constraints in office – he would pose a greater threat of increasing taxes, minimum wages, and passing legislative regulation than the market currently expects. In short, Biden would be pulled to the left of the political spectrum by his party and expectations of an establishment Democrat posing a minimal threat to corporate profits would be greatly disappointed. Risks of Trump's second term: Finally, assuming the manufacturing sector rebounds and that Trump’s odds of re-election rise above 55%, market complacency becomes an even bigger concern for a long-term investor. For in his second term Trump would become virtually unshackled with regard to economic and financial constraints, since he cannot run for office again. He would still face the senate, the Supreme Court, and other constraints, but these would certainly not preclude a doubling down on trade war (or confrontations with nuclear-aspirants like Iran or North Korea). We have argued that Trump will not instigate a trade war with Europe, at least until the economy has clearly rebounded, and most likely not until his second term. But we fully expect chapter two of the trade war to begin in 2021 – and this could mean China, Europe, or even a two-front war. Re-election could go to Trump’s head and prompt him to overreach on the global stage. Hence we expect the relief rally on Trump’s re-election to be short-lived and would be looking to sell the news. But the S&P 500 faces more immediate hurdles anyway, and that is why we urge caution in the very near term. Iran is still a major geopolitical risk this year. Bottom Line: None of these hurdles are insurmountable, but the US election cycle is now an understated risk to the equity bull market. We agree with our Global Investment Strategy that it is prudent to shift to a neutral position tactically on US equities, especially for the February and March period when uncertainty rises over the Democratic Party primary. This does not change our view that the underlying global economy is improving, largely on China’s rebound, and that the cyclical outlook is positive. Don’t Bet On Regime Collapse In Iran (Yet) The January 8 Iranian attack on US bases in Iraq was intended to serve as a breather for Iranian leaders. It was meant to put on pause the rapid escalation in US-Iran tensions – allowing Iranian leaders to recover from the assassination of top military commander Qassem Suleimani – all the while appeasing the public through a public show of revenge. As fate would have it, however, the Iranian regime was granted no such respite. Days later, domestic unrest descended on the Islamic Republic as protesters returned to the streets across the country, criticizing the regime’s downing of a civilian airliner and re-stating their long-running complaints against the regime. Civil strife is not uncommon in Iran (Table 1). Economic inefficiencies, corruption, and discriminatory policies which serve to reward regime loyalists while suppressing the private sector are only some of the grievances faced by Iranians.1 Table 1Civil Strife Ongoing Problem In Iran

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Today’s strife is relevant, however, because it is fueled by US-imposed “maximum pressure” sanctions that have created an even bleaker economic reality. Iranian exports were down 37% in 2019 following an 18% decline the previous year. Oil exports fell to 129 thousand barrels per day in December 2019, down from an average 2.1 million barrels per day in 2017 (Chart 10). Households are facing the brunt, experiencing a 17% unemployment rate and a whopping 36% inflation rate (Chart 11). Chart 10US 'Maximum Pressure' Sanctions On Iranian Oil Exports

US 'Maximum Pressure' Sanctions On Iranian Oil Exports

US 'Maximum Pressure' Sanctions On Iranian Oil Exports

Chart 11Iranian Households Bear Brunt Of Economic Shock

Iranian Households Bear Brunt Of Economic Shock

Iranian Households Bear Brunt Of Economic Shock

The 2020-21 budget, released in December and described as a weapon of “resistance against US sanctions,” intends to plug the deficit using state bonds and state property sales (Chart 12). However Iran’s fiscal condition is shaky. The International Monetary Fund estimates a fiscal breakeven oil price of $194.6 per barrel for Iran, more than 3 times higher than current oil prices. Chart 12Iran’s Fiscal Condition Is Shaky

Market Hurdles: From Sanders To Iran

Market Hurdles: From Sanders To Iran

Chart 13Iran Avoiding Devaluation Under Trump