UK

UK retail sales plunged 2.3% m/m in April from a downwardly revised 0.2% m/m contraction in March, significantly undershooting expectations of a 0.5% m/m decline. Household goods as well as clothing and footwear stores led the shortfall. Retailers have…

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less than the moderation embedded in…

Preliminary GDP estimates suggest that the UK economy started growing again in Q1, thus exiting a technical recession in the past two quarters. Q1 growth came in at 0.6%, improving from a 0.3% contraction last quarter, surpassing expectations of 0.4%. On a…

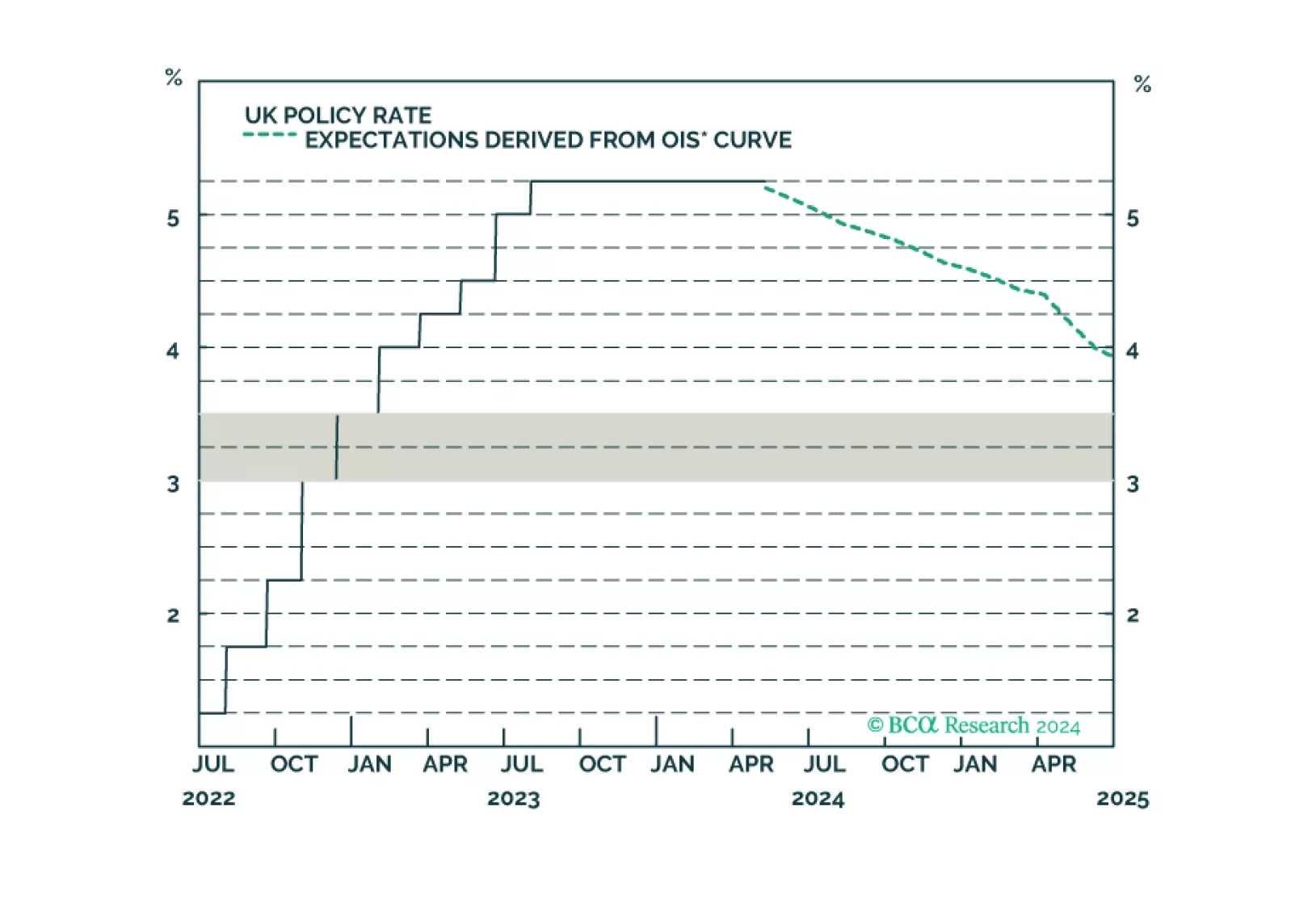

In a widely expected move, the Bank of England (BoE) maintained its policy rate at 5.25% in May. Nevertheless, two Committee Members voted in favor of cutting rates, one more than was anticipated. The tone of the report was overall dovish. The BoE…

An update to our views on UK rates and currency following today’s Bank of England meeting.

According to BCA Research’s Global Fixed Income Strategy service, a hard landing is the only way to solve the UK inflation problem. Sticky inflation and lingering inflation pressures have made the BoE’s job much more challenging. The UK economy weakened in…

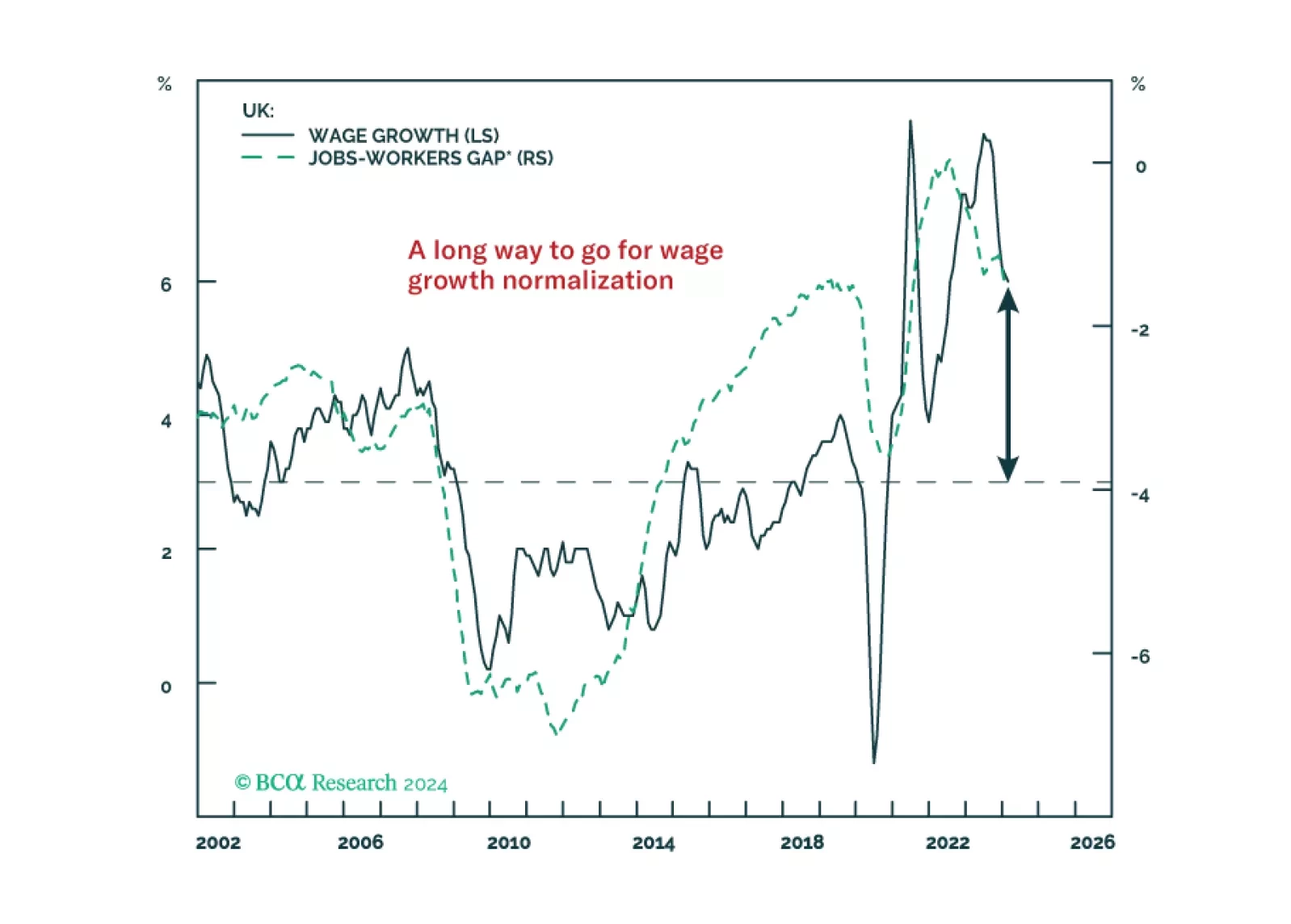

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

UK retail sales volumes were flat in March, a decrease from the 0.1% growth registered in February and disappointing expectations of a 0.3% m/m increase. The details were mixed, with automotive fuel and non-food stores sales volumes…

UK inflation came in hotter than expected in March. Headline CPI inflation was unchanged at 0.6% m/m – above expectations of a slowdown to 0.4% m/m. Moreover, while the headline and core measures both decelerated on an annual basis, they exceeded consensus…

UK stocks posted one of the largest positive abnormal returns (z-score) among the major financial markets we tracked in March. The MSCI UK index has gained 2% relative to Eurozone stocks since late February. However, the relative performance of UK equities…