Soybeans

The annual Prospective Plantings report released by the US Department of Agriculture (USDA) last week was slightly bullish for corn, neutral for soybeans, and slightly bearish for wheat. It forecasts a 5% drop in corn acreage, a 3% increase in soybean…

Prices of agricultural commodities have come under intensified downward pressure this year. Corn, soybean, and wheat prices have fallen by 8.6%, 8.3%, and 4.9% respectively so far this year. Multiple factors are behind the selloff. First, ag prices…

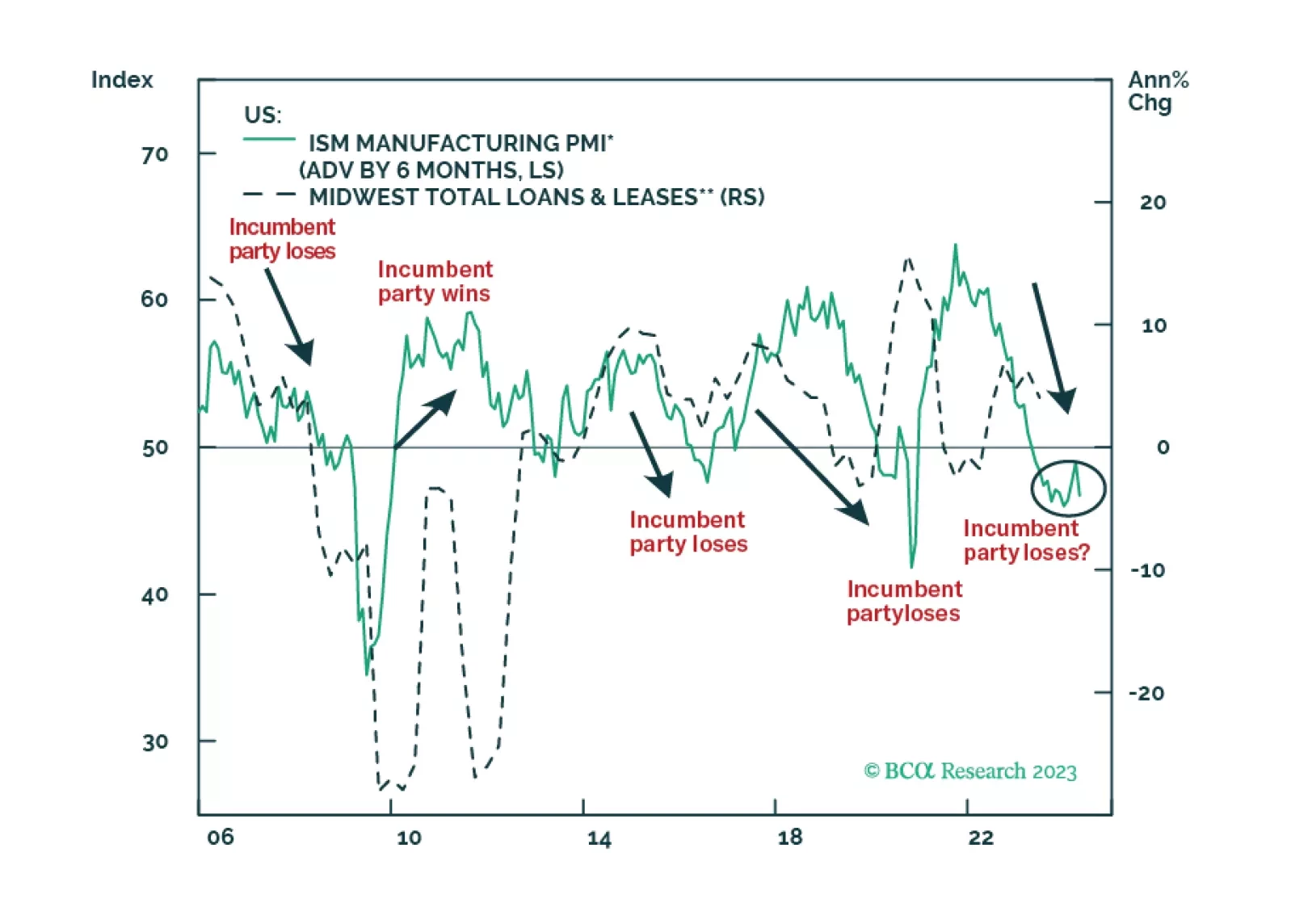

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

Wheat, corn, and soybean all traded lower at the Chicago Board of Trade on Wednesday following the US Department of Agriculture’s latest release of its monthly World Agricultural Supply and Demand Estimates (WASDE) – down 4.2%, 3.5%, and 2.4%, respectively. …

Highlights The surge in energy prices going into the Northern Hemisphere winter – particularly coal and natgas prices in China and Europe – will push inflation and inflation expectations higher into the end of 1Q22 (Chart of the Week). Over the medium-term, similar excursions into the far-right tails of price distributions will become more frequent if capex in hydrocarbon-based energy sources continues to be discouraged, and scalable back-up sources of energy are not developed for renewables. It is not clear China will continue selectively relaxing price caps for some large electricity buyers, which came close to bankrupting power utilities this year and contributed to power shortages. The current market set-up favors long commodity index products like the S&P GSCI and the COMT ETF. We remain long both. Higher energy and metals prices also will work in favor of long-only commodity index exposure over the medium term. Longer-term supply-chain issues will be sorted out. Still, higher costs will be needed to incentivize production of the base metals required to decarbonize electricity production globally, and to keep sufficient supplies of fossil fuels on hand to back up renewable generation. This will cause inflation to grind higher over time. Feature Back in February, we were getting increasingly bullish base metals on the back of surging demand from China. Most other analysts were looking for a slowdown.1 The metals rally earlier this year drew attention away from the fact that China had fundamentally altered its energy supply chain, when it unofficially banned imports of Australian thermal coal. It also altered global energy flows and will, over the winter, push inflation higher in the short run. Building new supply chains is difficult under the best of circumstances. But last winter had added dimensions of difficulty: A La Niña drawing arctic weather into the Northern Hemisphere and driving up space-heating demand; flooding in Indonesia, which limited coal shipments to China; and a manufacturing boom that pushed power supplies to the limit. Over the course of this year, Chinese coal inventories fell to rock-bottom levels and set off a scramble for liquified natural gas (LNG) to meet space-heating and manufacturing demand last winter (Chart 2).2 Chart of the WeekEnergy-Price Surge Will Lift Inflation Chart 2Coal Shortage China While this was evolving, the volume of manufactured exports from China was falling (Chart 3), even while the nominal value of these exports was rising in USD terms (Chart 4). This is a classic inflationary set-up: More money chasing fewer goods. This is occurring worldwide, as supply-chain bottlenecks, power rationing and shortages, and falling commodity inventories keep supplies of most industrial commodities tight. China's export volumes peaked in February 2021, and moved lower since then. This likely persists going forward, given the falloff of orders and orders in hand (Chart 5). Chart 3Volume Of China's Exports Falls … Chart 4… But The Nominal USD Value Rises Chart 5China's Official PMIs, Export And In-Hand Orders Weaken Space-heating and manufacturing in China are both heavily reliant on coal. Space-heating north of the Huai River is provided for free, or is heavily subsidized, from coal-fired boilers that pump heat to households and commercial establishments. This is a practice adopted from the Soviet Union in the 1950s and expanded until the 1980s, according to Fan et al (2020).3 Manufacturing pulls its electricity from a grid that produces 63% of its power from coal. China's coal output had been falling since December 2020, which complicated space heating and electricity markets, where prices were capped until this week. This meant electricity generators could not recover skyrocketing energy costs – coal in particular – and therefore ran the risk of bankruptcy.4 The loosening of price caps is now intended to relieve this pressure. Competition For Fuels Will Continue Europe was also hammered over the past year by a colder-than-normal winter brought on by a La Niña event, which sharply drew natgas inventories. The cold weather lingered into April-May, which slowed efforts to refill storage, and set off a scramble to buy up LNG cargoes (Chart 6). Chart 6The Scramble For Natgas Continues This competition has lifted global LNG prices to record levels, and continues to drive prices higher. Longer-term, the logic of markets – higher prices beget higher supply, and vice versa – virtually assures supply chains will be sorted out. However, the cost of energy generally will have to increase to incentivize production of the base metals needed to pull off the decarbonization of electricity production globally, and to keep sufficient supplies of fossil fuels on hand to back up renewable generation. This will cause inflation to grind higher over time. Decarbonization is a strategic agenda for leading governments, especially China and the European Union. China is fully committed to renewables for fear of pollution causing social unrest at home and import dependency causing national insecurity abroad. In the EU, energy insecurity is also an argument for green policy, which is supported by popular opinion. The US has greater energy security than these two but does not want to be left behind in the renewable technology race – it is increasing government green subsidies. The current set of ruling parties will continue to prioritize decarbonization for the immediate future. Compromises will be necessary on a tactical basis when energy price pressures rise too fast, as with China’s latest measures to restart coal-fired power production. The strategic direction is unlikely to change for some time. Investment Implications Over time, a structural shift in forward price curves for oil, gas and coal – e.g., a parallel shift higher from current levels – will be required to incentivize production increases. This would provide hedging opportunities for the producers of the fuels used to generate electricity, and the metals required to build the infrastructure needed by the low-carbon economies of the future. We continue to expect markets to remain tight on the supply side, which will make backwardation – i.e., prices for prompt-delivery commodities trade higher than those for deferred delivery – a persistent feature of commodities for the foreseeable future. This is because inventories will remain under pressure, making commodity buyers more willing to pay up for prompt delivery. The current market set-up favors long commodity index products like the S&P GSCI and the COMT ETF. We remain long both, given our expectation. Over the short term, inflation will be pushed higher by the rise in coal and gas prices. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Bullish According to the Energy Information Administration (EIA), industrial consumption of natgas in the US is on track to surpass its five-year average this year. Over the January-July period, US natgas consumption average 22.4 BCF/d, putting it 0.2 BCF/d over its five-year average (2016-2020). US industrial consumption of natgas peaked in 2018-19 at just over 23 BCF/d, according to the EIA (Chart 7). The EIA expects full-year 2021 industrial consumption of natgas to be 23.1 BCF/d, which would tie it with the previous peak levels. Base Metals: Bullish Following a sharp increase in refined copper usage in China last year resulting from a surge in imports, the International Copper Study Group (ICSG) is expecting a 5% decline this year on the back of falling imports. Globally, the ICSG expects refined copper consumption to be unchanged this year, and rise 2.4% in 2022. Refined copper production is expected to be 25.9mm MT next year vs. 24.9mm MT this year. Consumption is forecast to grow to 25.6mm MT next year, up to 700k MT from the 24.96mm MT usage expected this year. Precious Metals: Bullish Lower-than-expected job growth in the US pushed gold prices higher at the end of last week on the back of expectations the Fed will continue to keep policy accessible as employment weakened. All the same, gold prices remain constrained by a well-bid USD, which continues to act as a headwind, and only minimal weakening of the 10-year US bond yield, which dipped slightly below the 1.61% level hit earlier in the week (Chart 8). Ags/Softs: Neutral This week's USDA World Agricultural Supply and Demand Estimates (WASDE) were mostly neutral for grains and bearish for soybeans. Global ending bean stocks are expected to rise almost 5.4% in the USDA's latest estimate for ending stocks in the current crop year, finishing at 104.6mm tons. Corn and rice ending stocks were projected to rise 1.4% and less than 1%, ending the crop year at 301.7mm tons and 183.6mm tons, respectively. According to the department, global wheat ending stocks are the lone standout, expected to fall 2.1% to 277.2mm tons, the lowest level since the 2016/17 crop year. Chart 7 Chart 8 Footnotes 1 Please see Copper Surge Welcomes Metal Ox Year, which we published on February 11, 2021. It is available at ces.bcaresearch.com. 2 China’s move to switch to Indonesian coal at the beginning of this year to replace Aussie coal was disruptive to global markets. As argusmedia.com reported, this was compounded by weather-related disruptions in Indonesian exports earlier this year. It is worthwhile noting, weather-related delays returned last month, with flooding in Indonesia's coal-producing regions again are disrupting coal shipments. We expect these new trade flows in coal will take a few more months to sort out, but they will be sorted. 3 Please see Maoyong Fan, Guojun He, and Maigeng Zhou (2020), " The winter choke: Coal-Fired heating, air pollution, and mortality in China," Journal of Health Economics, 71: 1-17. 4 In August and September, the South China Morning Post reported coal-powered electric generators petitioned authorities to relax price caps, because they faced bankruptcy from not being able to recover the skyrocketing cost of coal. Please see China coal-fired power companies on the verge of bankruptcy petition Beijing to raise electricity prices, published by scmp.com on September 10, 2021. This month, Shanxi Province, which provides about a third of China's domestically produced coal, was battered by flooding, which forced authorities to shut dozens of mines, according to the BBC. Please see China floods: Coal price hits fresh high as mines shut published by bbc.co.uk on October 12, 2021. Power supplies also were lean because of the central government's so-called dual-circulation policies to reduce energy consumption and the energy intensity of manufacturing. This is meant to increase self-reliance of the state. Please see What is behind China’s Dual Circulation Strategy? Published by the European think tank Bruegel on September 7, 2021. Investment Views and Themes Strategic Recommendations

Highlights US crude oil output will continue its sharp recovery before leveling off by mid-2022, in our latest forecast (Chart of the Week). The recovery in US production is led by higher Permian shale-oil production, which is quietly pushing toward pre-COVID-19 highs while other basins languish. Permian output in July was ~ 143k b/d below the basin's peak in Mar20, and likely will surpass its all-time high output in 4Q21. Overall US shale-oil output remains ~ 1.1mm b/d below Nov19's peak of 9.04mm b/d, but we expect it to end the year at 7.90mm b/d and to average 8.10mm b/d for 2022. We do not expect US crude oil production to surpass its all-time high of 12.9mm b/d of Jan20 by the end of 2023. Instead, exploration & production (E&P) companies will continue to prioritize shareholders' interests. This means larger shares of free cashflow will go to shareholders, and not to drilling for the sake of increasing output. While our overall balances estimates remain largely unchanged from last month, we have taken down our expectation for demand growth this year by close to 360k b/d and moved it into 2022, due to continuing difficulties containing the COVID-19 Delta variant. Our Brent crude oil forecasts for 2H21, 2022 and 2023 remain largely unchanged at $70, $73 (down $1) and $80/bbl. WTI will trade $2-$3/bbl lower. Feature Chart 1US Crude Recovery Continues Global crude oil markets are at a transition point. The dominant producer – OPEC 2.0 – begins retuning 400k b/d every month to the market from the massive 5.8mm b/d of spare capacity accumulated during the COVID-19 pandemic. For modeling purposes, it is not unreasonable to assume this will be a monthly increment returned to the market until the accumulated reserves are fully restored. This would take the program into 2H22, per OPEC's 18 July 2021 communique issued following the meeting that produced this return of supply. Thereafter, the core group of the coalition able to increase and sustain higher production – Kuwait, the UAE, Iraq, KSA and Russia – is expected to meet higher demand from their capacity.1 There is room for maneuver in the OPEC 2.0 agreement up and down. We continue to expect the coalition to make supply available as demand dictates – a data-dependent strategy, not unlike that of central banks navigating through the pandemic. This could stretch the return of that 5.8mm b/d of accumulated spare capacity further into 2H22 than we now expect. The pace largely depends on how quickly effective vaccines are distributed globally, particularly to EM economies over the course of this year and next. US Shale Recovery Led By Permian Output While OPEC 2.0 continues to manage member-state output – keeping the level of supply below that of demand to reduce global inventories – US crude oil output is quietly recovering. We expect this to continue into 1H22 (Chart 2). Chart 2Permian Output Recovers Strongly The higher American output in the Lower 48 states primarily is due to the continued growth of tight-oil shale production in the low-cost Permian Basin (Chart 3). This has been aided in no small part by the completion of drilled-but-uncompleted (DUC) wells in the Permian and elsewhere. Chart 3E&Ps Favor Permian Assets Since last year’s slump, the rig count has increased; however, compared to pre-pandemic levels, the number of rigs presently deployed are not sufficient to sustain current production. The finishing of DUC wells means that, despite the low rig count during the pandemic, shale oil supply has not dipped by a commensurate amount. This is a major feat, considering shale wells’ high decline rates. Chart 4US Producers Remain Focused On Shareholder Priorities DUCS have played a large role in sustaining overall US crude oil production. According to the EIA, since its peak in June 2020, DUCs in the shale basins have fallen by approximately 33%. As hedges well below the current market price for shale producers roll off, and DUC inventories are further depleted, we expect to see more drilling activity and the return of more rigs to oil fields. We do not expect US crude oil output to surpass its all-time high of 12.9mm b/ of Jan20 by the end of 2023. Instead, exploration & production (E&P) companies will continue to prioritize shareholders' interests. This means only profitable drilling supporting the free cashflow that allows E&Ps to return capital to shareholders will receive funding. US oil and gas companies have a long road back before they regain investors' trust (Chart 4). Demand Growth To Slow We expect global demand to increase 5.04mm b/d y/y in 2021, down from last month's growth estimate of 5.4mm b/d. We have taken down our expectation for demand growth this year by ~ 360k b/d and moved it into 2022, because of reduced mobility and local lockdowns due to continuing difficulties in containing the COVID-19 Delta variant, particularly in Asia (Chart 5).2 We continue to expect the global rollout of vaccines to increase, which will allow mobility restrictions to ease, and will support demand. This has been the case in the US, EU and is expected to continue as Latin America and other EM economies receive more efficacious vaccines. Thus, as DM growth slows, EM oil demand should pick up (Chart 6). Chart 5COVID-19 Delta Variant's Spread Remains Public Health Challenge Chart 6EM Demand Growth Will Offset DM Slowdown Net, we continue to expect demand for crude oil and refined products to grind higher, and to be maintained into 2023, as mobility rises, and economic growth continues to be supported by accommodative monetary policy and fiscal support. If anything, the rapid spread of the Delta variant likely will predispose central banks to continue to slow-walk normalizing monetary policy and interest rates. Global Balances Mostly Unchanged Chart 7Oil Markets To Remain Balanced Although we have shifted part of the demand recovery into next year, at more than 5mm b/d of growth, our 2021 expectation is still strong. This is expected to continue next year and into 2023 although not at 2021-22 rates. Continued production restraint by OPEC 2.0 and the price-taking cohort outside the coalition will keep the market balanced (Chart 7). We expect OPEC 2.0's core group of producers – Kuwait, the UAE, Iraq, KSA and Russia – will continue to abide by the reference production levels laid out in 18 July 2021 OPEC communique. Capital markets can be expected to continue constraining the price-taking cohort's misallocation of resources. These factors underpin our call for balanced markets (Table 1), and our view inventories will continue to draw (Chart 8). Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances) To Dec23Our balances assessment leaves our price expectations unchanged from last month, with Brent's price trajectory to end-2023 intact (Chart 9). We expect Brent crude oil to average $70, $73 and $80/bbl in 2H21, 2022 and 2023, respectively. WTI is expected to trade $2-$3/bbl lower over this interval. Chart 8Inventories Will Continue To Draw Chart 9Brent Prices Trajectory Intact Investment Implications Balanced oil markets and continued inventory draws support our view Brent and refined-product forward curves will continue to backwardate, even if the evolution of this process is volatile. As a result, we remain long the S&P GSCI and the COMT ETF, which is optimized for backwardation. We continue to wait for a sell-off to get long the SPDR S&P Oil & Gas Exploration & Production ETF (XOP ETF). Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish The US EIA expects natural gas inventories at the end of the storage-injection season in October to be 4% below the 2016-2020 five-year average, at 3.6 TCF. At end-July, inventories were 6% below the five-year average (Chart 10). Colder-than-normal weather this past winter – particularly through the US Midwest and Texas natural gas fields – affected production and drove consumption higher this past winter, which forced inventories lower. Continued strength in LNG exports also are keeping gas prices well bid, as Asian and European markets buy fuel for power generation and to accumulate inventories ahead of the coming winter. Base Metals: Bullish The main worker’s union at Chile's Escondida mine, the largest in the world, and BHP reached an agreement on Friday to avoid a strike. The mine is expected to constitute 5% of total mined global copper supply for 2021. China's refined copper imports have been falling for the last three months (Chart 11). Weak economic data – China reported slower than expected growth in retail sales and manufacturing output for July – contributed to lower import levels. Precious Metals: Bullish Gold has been correcting following its recent decline, ending most days higher since the ‘flash crash’ last Monday, facilitated by a drop in real interest rates. The Jackson Hole Symposium next week will provide insights to market participants regarding the Fed’s future course of action and if it is in fact nearing an agreement to taper asset purchases. According to the Wall Street Journal, some officials believe the program could end by mid-2022 on the back of strong hiring reports. This was corroborated by minutes of the FOMC meeting which took place in July, which suggested a possibility to begin tapering the program by year-end. While the Fed stressed there was no mechanical relationship between the tapering and interest rate hikes, this could be bearish for gold, as real interest rates and the bullion move inversely. On the other hand, political uncertainty and a potential economic slowdown in China will support gold prices. Ags/Softs: Neutral Grain and bean crops are in slightly worse shape this year vs the same period in 2020, according to the USDA. The Department reported 62% of the US corn crop was in good to excellent condition for the week ended 15 August 2021, compared to 69% for the same period last year. 57% of the soybean crop was in good-to-excellent shape for the week ending on the 15th vs 72% a year ago. Chart 10 Chart 11 Footnotes 1 Please see our report of 22 July 2021, OPEC 2.0's Forward Guidance In New Baselines, which discusses the longer-term implications of this meeting and the subsequent communique containing the OPEC 2.0 core group's higher reference production levels. It is available at ces.bcareserch.com. 2 S&P Global Platts notes China's most recent mobility restrictions throughout the country will show up in oil demand figures in the near future. We expect similar reduced mobility as public health officials scramble to get more vaccines distributed. Please see Asia crude oil: Key market indicators for Aug 16-20 published 16 August 2021 by spglobal.com. Investment Views and Themes Strategic Recommendations Commodity Prices and Plays Reference Table Trades Closed In 2021 Summary of Closed Trades

Highlights Going into the new crop year, we expect the course of the broad trade-weighted USD to dictate the path taken by grain and bean prices (Chart of the Week). Higher corn stocks in the coming crop year, flat wheat stocks and lower rice stocks will leave grain markets mostly balanced vs the current crop year. Soybean stocks and carryover estimates from the USDA and International Grains Council (IGC) are essentially unchanged year-on-year (y/y). In the IGC's estimates, changes in production, trade, and consumption for the major grains and beans largely offset each other, leaving carryovers unchanged. Supply-demand fundamentals leave our outlook for grains and beans neutral. This does not weaken our conviction that continued global weather volatility will tip the balance of price risk in grains and beans over the coming year to the upside. Our strategically bearish USD view also tips the balance of price risk in grains – and commodities generally – to the upside. We believe positioning for higher-volatility weather events and a lower US dollar is best done with index products like the S&P GSCI and the COMT ETF, which tracks a version of the GSCI optimized for backwardation. Feature Chart of the WeekUSD Will Drive Global Grain Markets Chart 2Opening, Closing Grain Stocks Will Be Largely Unchanged Going into the new crop year, opening and closing stocks are expected to remain flat overall vs the current crop years, with changes in production and consumption largely offsetting each other in grain and bean markets (Chart 2).1 This will leave overall prices a function of weather – which no one can predict – and the path taken by the USD over the coming year. The IGC's forecast calls for mostly unchanged production and consumption for grains and beans globally, with trade volumes mostly flat y/y. This leaves global end-of-crop-year carryover stocks essentially unchanged at 594mm tons. The USDA expects wheat ending stocks at the end of the '21/22 crop year up a slight 0.5%; rice down ~ 4.5%, and corn up ~ 4%. Below we go through each of the grain and bean fundamentals, and assess the impact of COVID-19 on global trade in these commodities. We then summarize our overall view for the grain and bean complex, and our positioning recommendations. Rice The IGC forecasts higher global rice production and consumption, and, since they expect both to change roughly by the same amount, ending stocks are projected to remain unchanged in the '21/22 crop year relative to the current year (Chart 3). The USDA, on the other hand, is expecting global production to increase by ~ 1mm MT in the new crop year, with consumption increasing by ~ 8mm MT. This leaves ending inventories for the new crop year just under 8mm MT below '20/21 ending stocks, or 4.5%. Chart 3Global Rice Balances Roughly Unchanged Corn The IGC forecasts global corn production will rise 6.5% to a record high in the '21/22 crop year, while global consumption is expected to increase 3.6%. Trade volumes are expected to fall ~ 4.2%, leaving global carryover stocks roughly unchanged (Chart 4). In the USDA's modelling, global production is expected to rise 6.6% in the '21/22 crop year to 1,195mm MT, while consumption is projected to rise ~ 2.4% to 1,172mm MT. The Department expects ending balances to increase ~ 11mm MT, ending next year at 291.2mm MT, or just over 4% higher. Chart 4Corn Balances Y/Y Remain Flat Wheat The IGC forecasts global wheat production in the current crop year will increase by ~ 16mm MT y/y, which will be a record if realized. Consumption is expected to rise 17mm MT, with trade roughly unchanged. This leaves expected carryover largely unchanged at ~ 280mm MT globally (Chart 5). The USDA's forecast largely agrees with the IGC's in its ending-stocks assessment for the new crop year. Global wheat production is expected to increase 16.6mm MT y/y in '21/22, and consumption will rise ~ 13mm MT, or 1.7% y/y. Ending stocks for the new crop year are expected to come in at just under 292mm MT, or 0.5% higher. Chart 5Ending Wheat Stocks Mostly Unchanged Soybeans Both the IGC and USDA expect increases in soybean ending stocks for the '21/22 crop year. However, the USDA’s estimates for ending stocks are nearly double the IGC projections.2 We use the IGC's estimates in Chart 6 to depicts balances. USDA - 2021/22 global soybean ending stocks are set to increase by ~3 mm MT to 94.5 mm MT, as higher stocks from Brazil and Argentina are partly offset by lower Chinese inventories. US production is expected to make up more than 30% of total production, rising 6% year-on-year. Chart 6Higher Bean Production Meets Higher Consumption Impact Of COVID-19 On Ags Trade Global agricultural trade was mostly stable throughout the COVID-19 pandemic. China was the main driver for this resilience, accounting for most of the increase in agricultural imports from 2019 to 2020. Ex-China, global agricultural trade growth was nearly zero. During this period, China was rebuilding its hog stocks after an outbreak of the African Swine Flu, which prompted the government to grant waivers on tariffs in key import sectors, which increased trade under the US-China Phase One agreement. As a result, apart from COVID-19, other factors were influencing trade. Arita et. al. (2021) attempted to isolate the impact of COVID on global agricultural trade.3 Their report found that COVID-19 – through infections and deaths – had a small impact on global agricultural trade. Government policy restrictions and reduced mobility in response to the pandemic were more detrimental to agricultural trade flows than the virus itself in terms of reducing aggregate demand. Policy restrictions and lower mobility reduced trade by ~ 10% and ~ 6% on average over the course of the year. Monthly USDA data shows that the pandemic was not as detrimental to agricultural trade as past events. Rates of decline in global merchandise trade were sharper during the Great Recession of 2007 – 2009 (Chart 7). Many agricultural commodities are necessities, which are income inelastic. Furthermore, shipping channels for these types of commodities did not require substantial human interactions, which reduced the chances of this trade being a transmission vector for the virus, when governments declared many industries using and producing agricultural commodities as necessities. This could explain why agricultural trade was spared by the pandemic. Amongst agricultural commodities, the impact of the pandemic was heterogenous. For necessities such as grains or oilseeds, there was a relatively small effect, and in few instances, trade actually grew. For example, trade in rice increased by ~4%. The value of trade in higher-end items, such as hides, Chart 7COVID-19 Spares Ag Trade Chart 8Grains Rallied During Pandemic tobacco, wine, and beer fell during the pandemic. This was further proof of the income inelasticity of many agricultural products which kept global trade in this sector resilient. Indeed, the UNCTAD estimates global trade for agriculture foods increased 18% in 1Q21 relative to 1Q19. Over this period, Bloomberg's spot grains index was up 47.08% (Chart 8). Investment Implications We remain neutral grains and beans based on our assessment of the new crop-year fundamentals. That said, we have a strong-conviction view global weather volatility will tip the balance of price risk in grains over the coming year to the upside. Our strategically bearish USD view also tips the balance of price risk in grains – and commodities generally – to the upside. Weather-induced grain and bean prices volatility is supportive for our recommendations in the S&P GSCI and the COMT ETF, which tracks a version of the GSCI optimized for backwardation. These positions are up 5.8% and 7.9% since inception, and are strategic holdings for us. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish US natural gas prices remain well supported by increased power-generation demand due to heat waves rolling through East and West coasts, lower domestic production and rising exports. The US EIA estimates natgas demand for July rose 3.9 bcf/d vs June, taking demand for the month to 75.8 bcf/d. Exports – pipeline and LNG – rose 0.4 bcf/d to 18.2 bcf/d, while US domestic production fell to 92.7 bcf/d, down 0.2 bcf/d from June's levels. As US and European distribution companies and industrials continue to scramble for gas to fill inventories, we expect natgas to remain well bid as the storage-injection season winds down. We remain long 1Q22 call spreads, which are up ~214% since the position was recommended April 8, 2021 (Chart 9). Base Metals: Bullish Labor and management at BHP's Escondida copper mine – the largest in the world – have a tentative agreement to avoid a strike that would have crippled an already-tight market. The proposed contract likely will be voted on by workers over the next two days, according to reuters.com. Separately, the head of a trade group representing Chile's copper miners said prices likely will remain high over the next 2-3 years as demand from renewables and electric vehicles continues to grow. Diego Hernández, president of the National Society of Mining (SONAMI), urged caution against expecting a more extended period of higher prices, however, mining.com reported (Chart 10). We remain bullish base metals generally, copper in particular, which we expect to remain well-bid over the next five years. Precious Metals: Bullish US CPI for July rose 0.5% month-over-month, suggesting the inflation spike in June was transitory. While lower inflation may reduce demand for gold, it will allow the Fed to continue its expansionary monetary policy. The strong jobs report released on Friday prompted markets and some Fed officials to consider tapering asset purchases sooner than previously expected. The jobs report also boosted an increasing US dollar. A strong USD and an increase in employment were negative for gold prices on Monday. There also were media reports of a brief “flash crash” caused by an attempt to sell a large quantity of gold early in the Asian trading day, which swamped available liquidity at the time. This also was believed to trigger stops and algorithmic trading programs, which exacerbated the move. The potential economic impact of the COVID-19 Delta variant is the only unequivocally supportive development for gold prices. Not only will this increase safe-have demand for gold, but it will also prevent the Fed from being too hasty in tapering its asset purchases and subsequently raising interest rates. Chart 9 Chart 10 Footnotes 1 The wheat crop year in the US begins in June; the rice crop year begins this month; and the corn and bean crop years begin in September. 2 Historical data indicate this difference is persistent, suggesting different methods of calculating ending stocks. The USDA estimates ending stocks for the '21/22 crop year will be 94.5mm tons, while the IGC is projecting a level of 53.8mm. 3 Please refer to ‘Has Global Agricultural Trade Been Resilient Under Coronavirus (COVID-19)? Findings from an Econometric Assessment. This is a working paper published by Shawn Arita, Jason Grant, Sharon Sydow, and Jayson Beckman in May 2021. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades