Global

Most developed market central banks have paused hiking interest rates. With interest-rate differentials having been the most important driver of currencies over the last two years or so, the focus might now shift to other factors. One such factor could be…

Global cyclical sectors are outperforming defensive sectors on a year-to-date basis. The bulk of this outperformance occurred in the first seven months of the year. Relative valuations contributed to this dynamic as last year's selloff was more pronounced…

BCA Research's Commodity & Energy Strategy service concludes that lithium demand will rise over the long run. Lithium prices are continuing the selloff that began earlier this year, which was caused by strong production and mining capex increases. …

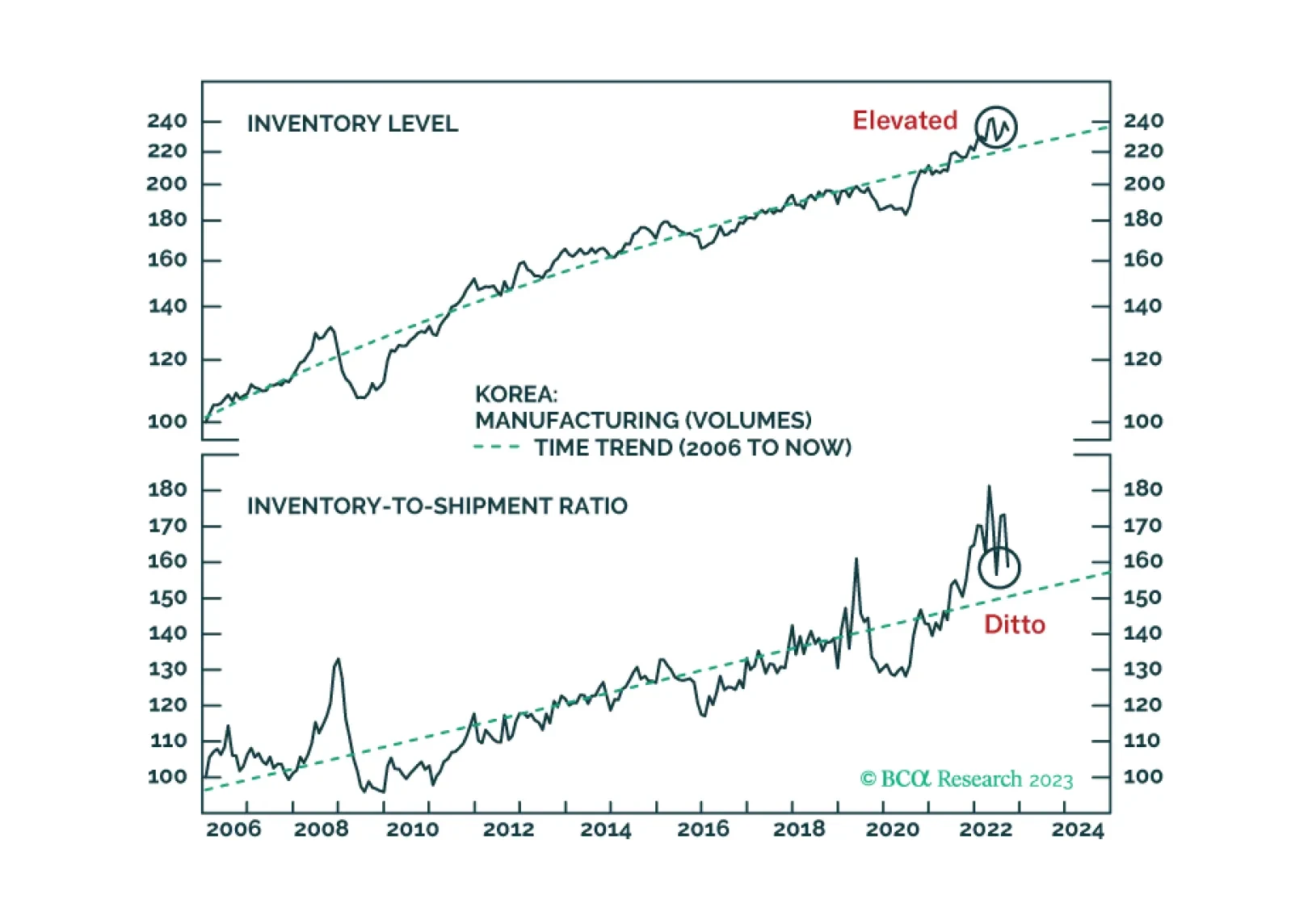

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

Global equities have had a stellar 2023, rising by 16% year-to-date and outperforming global bonds by roughly the same amount. However, the large concentration of US stocks in the Magnificent Seven has called into question the legitimacy of this rally. There…

After dipping into negative territory between June and early August, the Global Economic Surprise Index has since rebounded, signalling an improvement in economic momentum. Initially, this rebound was isolated to the US. However, the trend has been broadening…

To the extent that Taiwanese export orders act as a bellwether for global trade dynamics, we often monitor the release to gain a sense of the state of the manufacturing cycle. On this front, the October update provided a positive signal. The pace of decline…

Singapore is a small open economy that is highly sensitive to fluctuations in the global manufacturing activity. As such, Singapore’s non-oil domestic exports (NODX) are a bellwether for global growth. Singapore’s NODX delivered an upside surprise on…

BCA Research's Commodity & Energy Strategy service continues to expect Russia to reduce oil exports next year by up to 2mm b/d (25% probability), in an effort to reduce US President Biden’s chances of being re-elected. Resilient oil exports and global…

Throughout most of the second half of this year, the copper-to-gold ratio has been relatively stable, gyrating within a tight range. However, it is starting to show some tentative signs of bottoming. After the copper-to-gold ratio initially fell in the first…