Global

Investors typically associate high-flying tech stocks with high sensitivity to interest rates. The rationale is simple: Given that most of their cashflows are further into the future, their value will be more sensitive to changes in their discounter. And…

Commodities are making headlines with the prices of crude oil, copper, and gold all making sizeable gains since mid-February. Multiple forces have been cited as drivers of the rally across these commodities. Increased geopolitical risks amid concern of a…

Short speculative positions on Bitcoin at the CME are near theie highest level on record. Some financial commentators have suggested that this bearish positioning in bitcoin could act as kindle and spark a short squeeze. But looking at raw speculative…

Gold prices reached $2300 per ounce for the first time on Wednesday. They have now rallied by more than 12% so far this year. To a degree the furious rally in gold has been puzzling. Who has been buying? It certainly has not been private investors. Global…

In this report, we review our trade recommendations based on incoming data in the last month.

As a small open economy, Sweden’s economic performance is a good barometer of global growth developments. Swedish PMIs for March were overall positive. The Manufacturing PMI rose to the 50 boom-bust line following 19 consecutive months of contraction and…

The annual Prospective Plantings report released by the US Department of Agriculture (USDA) last week was slightly bullish for corn, neutral for soybeans, and slightly bearish for wheat. It forecasts a 5% drop in corn acreage, a 3% increase in soybean…

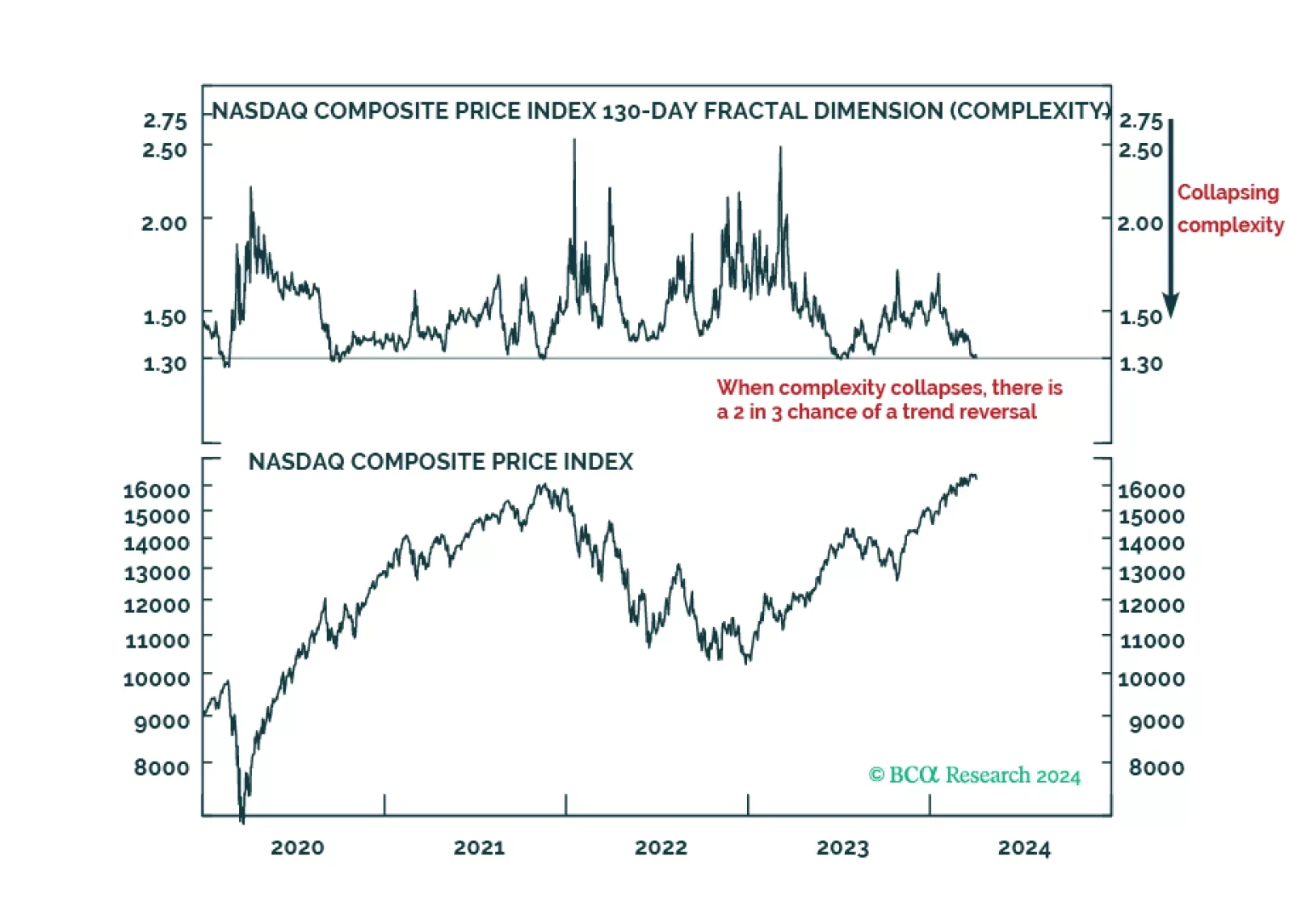

The analysis of complexity is a massive competitive advantage in investing, and from today, clients will be able to monitor the complexities of the world’s 17 major investments on our webpage in real-time.

Oil prices surged over the past two days on the back of heightened geopolitical risks to supply following increased tensions in the Middle East. Both Iran’s Supreme Leader Ayatollah Ali Khamenei and President Ebrahim Raisi warned that Israel will be punished…

The soft-landing narrative dominated the behavior of financial markets in March, with most major global risk assets posting above average returns. In particular, the burgeoning ‘risk on’ sentiment led to a rally across global equity markets. On this front,…