Financial Markets

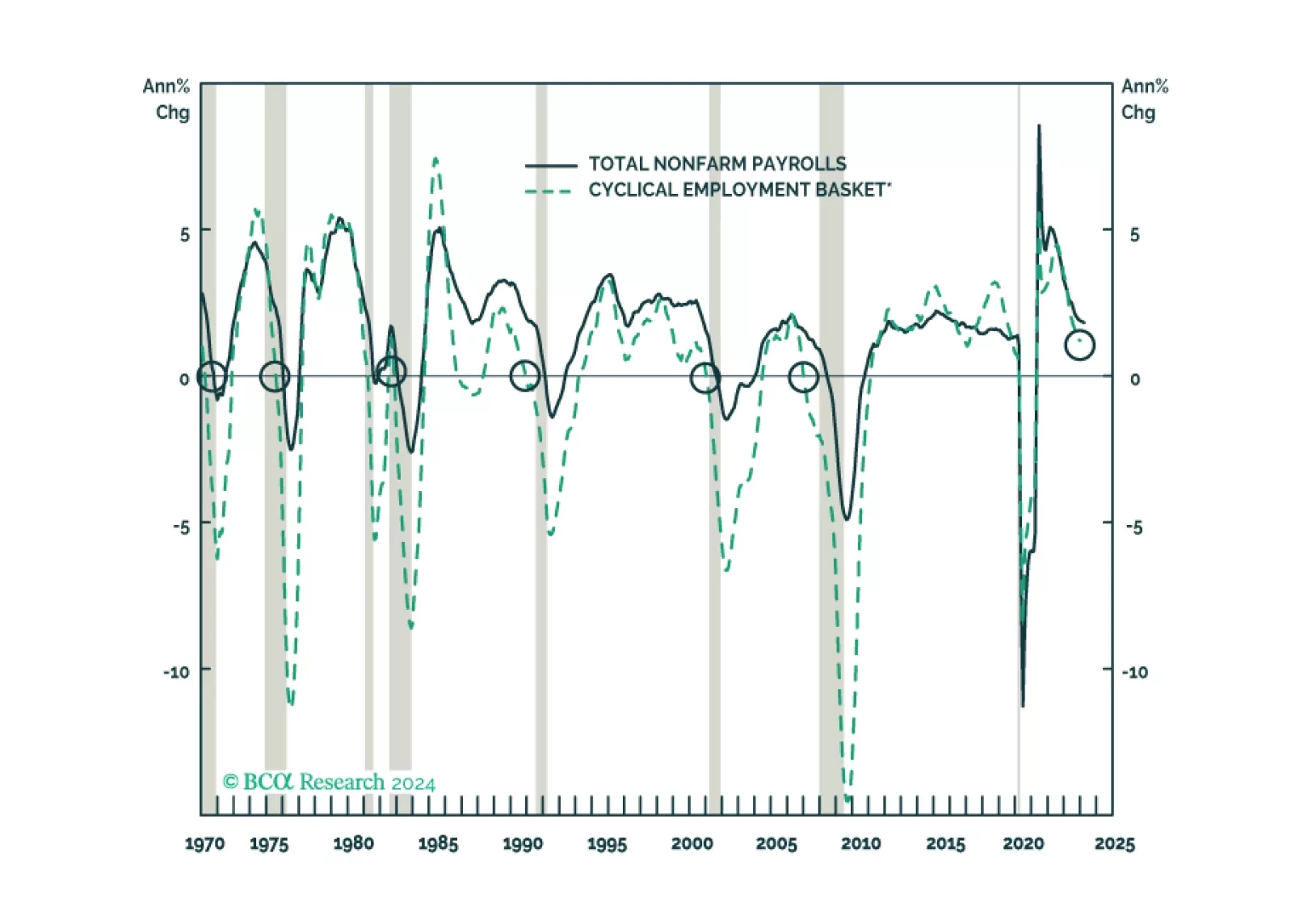

We look beneath headline data to assess the state of the labor market in cyclical goods-producing industries that have previously led overall nonfarm payrolls and in the services segments that have recently been leading the charge. The bottom-up view looks a lot like the top-down view: the labor market is softening, but very slowly, and offers no indications that a recession is at hand.

In this report, we present our quarterly review of our Model Bond Portfolio. The anti-growth bias of the portfolio allocations hurt the portfolio performance in Q1/2024 as global growth surprised to the upside. However, we anticipate some recovery of the underperformance in our base case scenario for the next six months.

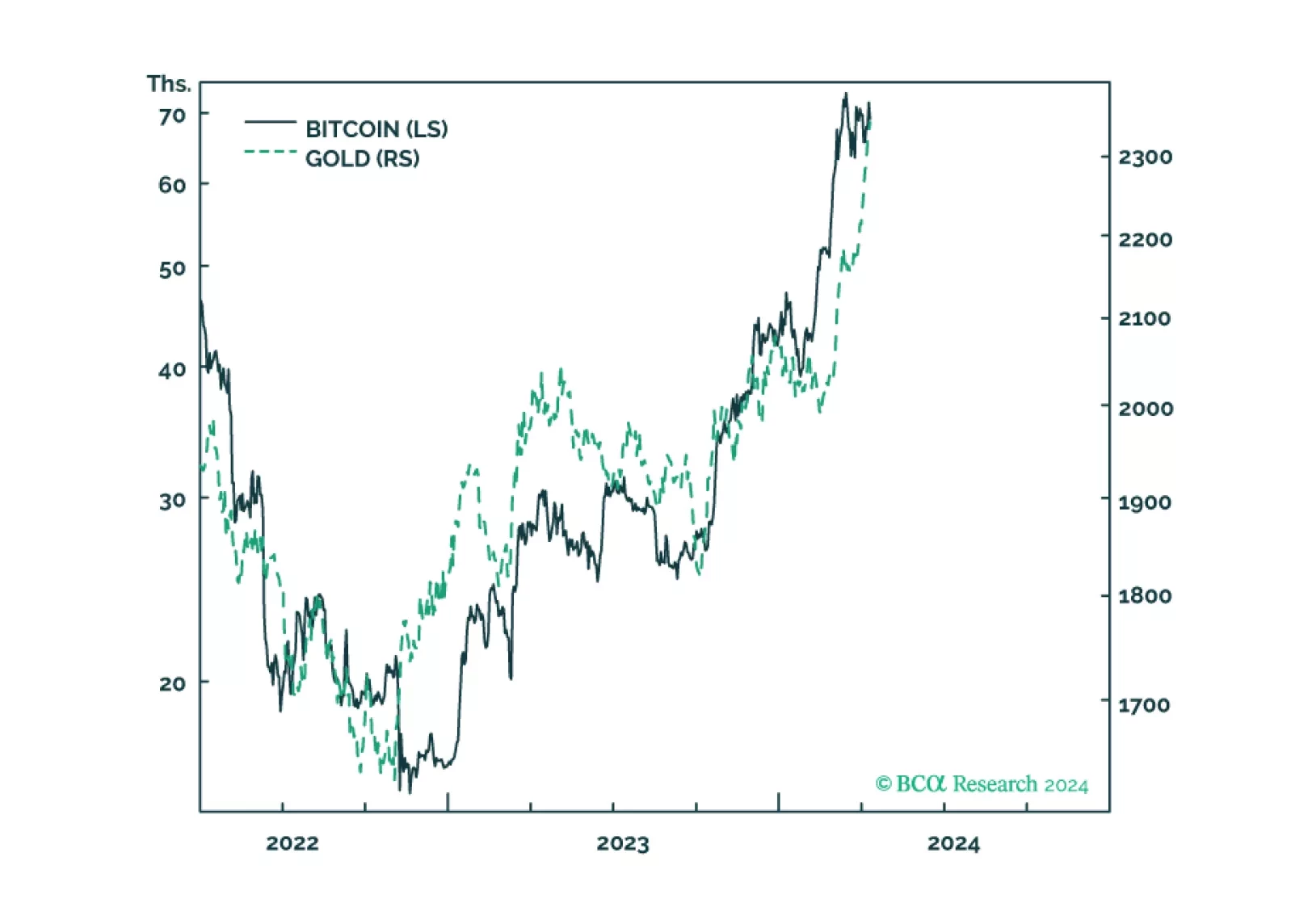

Gold and bitcoin are conceptually joined at the hip because the value of both comes from their ‘non-confiscatability’ by inflation, by bank failure, and in the case of bitcoin, by state expropriation. The sharp recent rallies in both gold and bitcoin reflect that the market has suddenly upped the value of non-confiscatability, and a plausible explanation is that recent US inflation data show that the journey to sustained 2 percent inflation has stalled, raising the risk that the Fed might balk at finishing the journey. Plus: JPM, CL, and USD/CHF are tactical reversal candidates.

Fears of a hard landing are abating as growth has been surprising to the upside. New worries are emerging, such as the trajectory of disinflation, and the pace and timing of rate cuts. In this environment, it is important to build a resilient all-weather portfolio, which protects against a correction, rising rates, or stubborn inflation but also has exposure to the AI theme.