Financial Markets

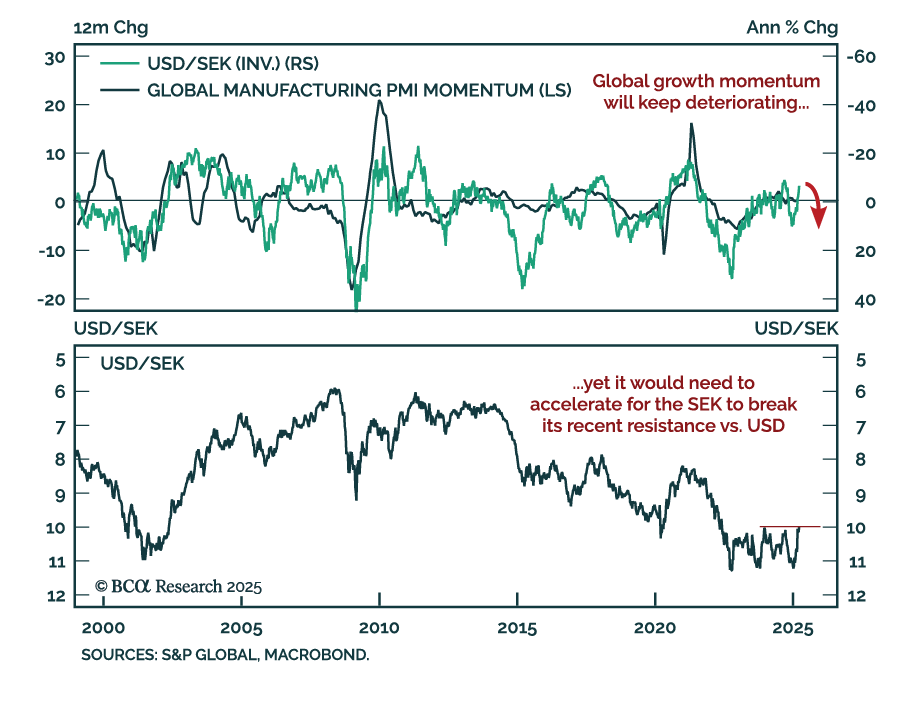

The SEK’s sharp rally is losing steam as local data weakens and EUR strength looks stretched. After appreciating more than 10% against the USD year-to-date, the krona is now showing signs of fatigue. Recent Swedish data has disappointed, with the Economic…

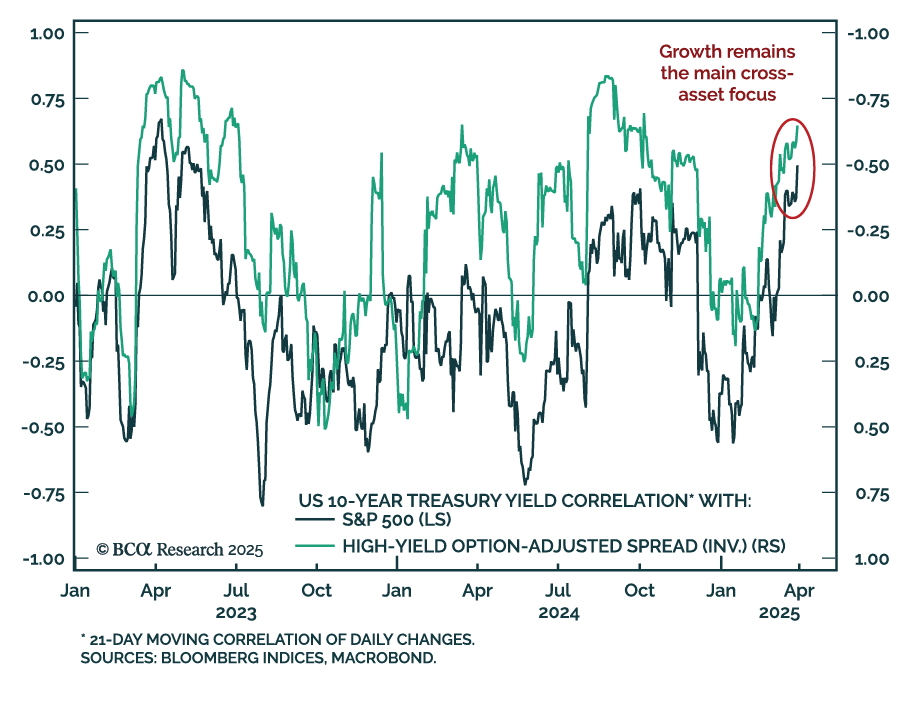

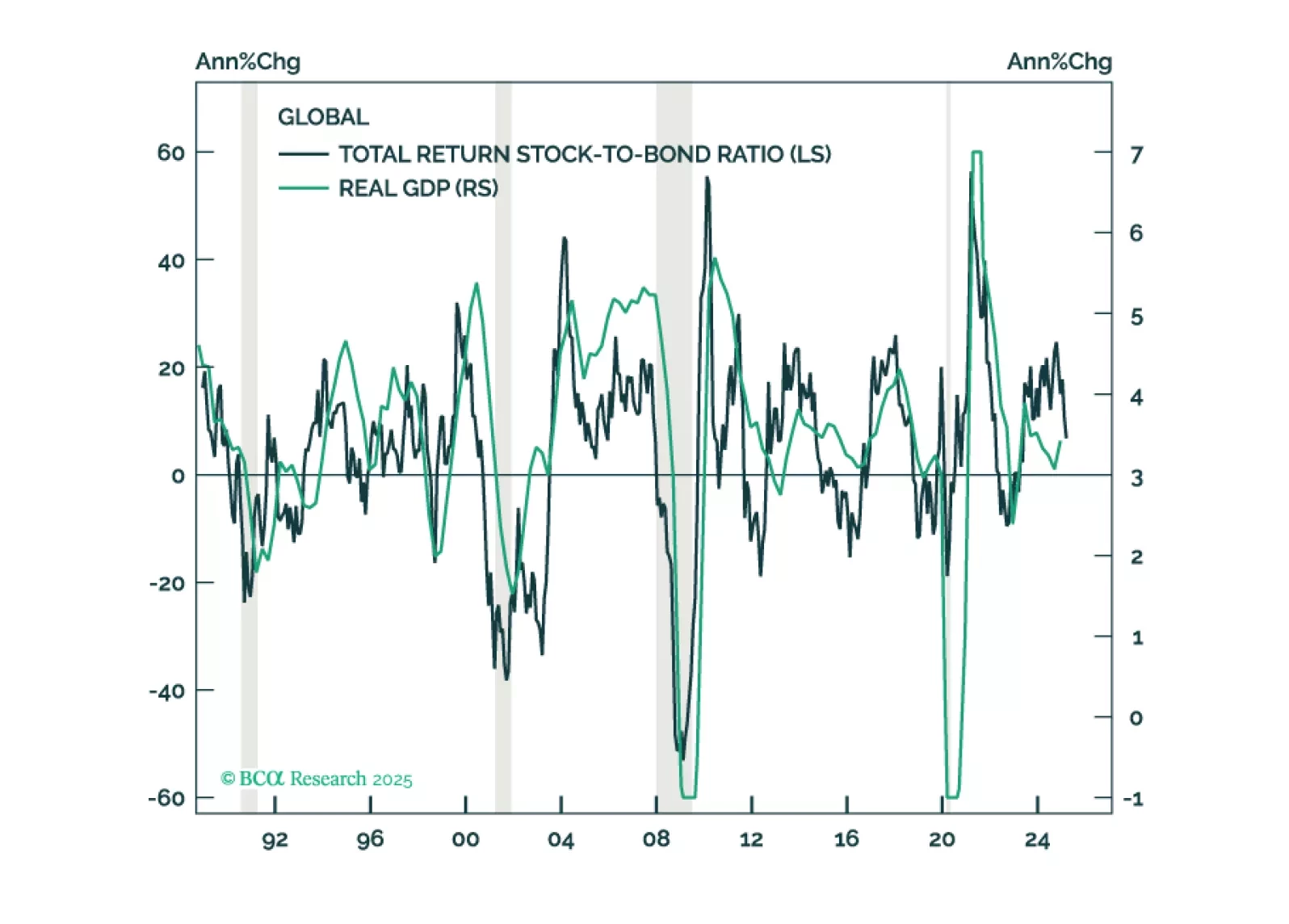

Markets are responding to the growth drag of stagflation, not the inflation impulse, reinforcing our defensive stance. Despite rising short-term inflation pressures in the US, risk assets and bond yields continue to move together, with the stock–bond yield…

Our Private Markets & Alternatives strategists remain structurally positive but cyclically underweight on Multi-Strategy Hedge Funds. While these funds have delivered consistent alpha and valuable diversification, current market conditions offer more…

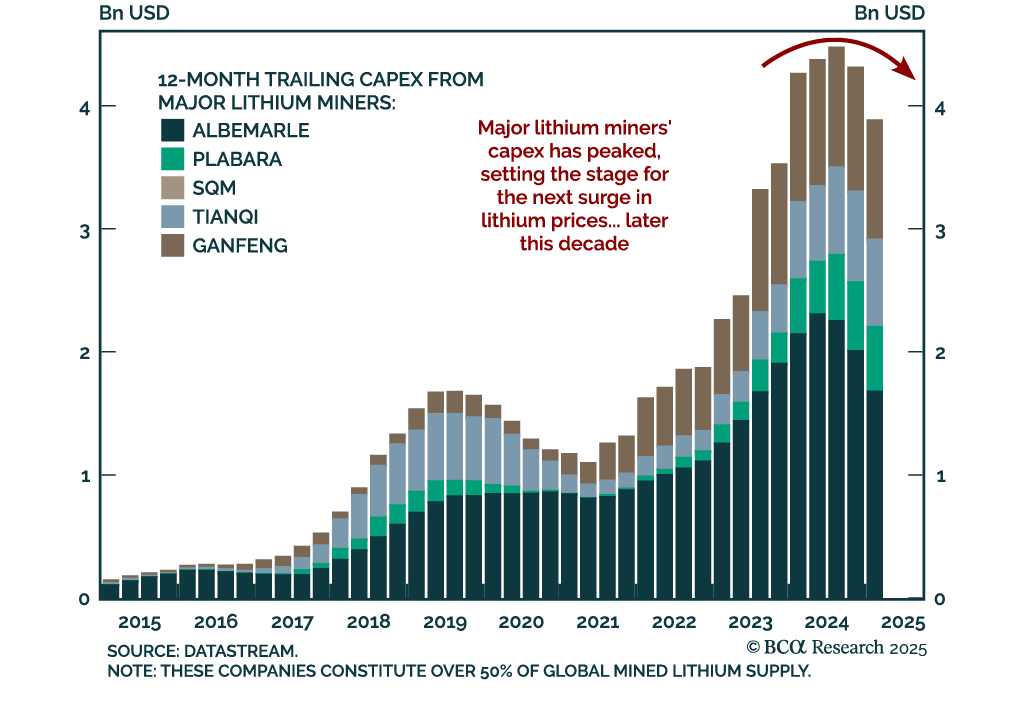

Our Commodities Strategy team advises against positioning for a near-term rebound in lithium prices, given the current headwinds from soft EV sales growth. They recommend patience, with more compelling opportunities likely to emerge later in the decade as…

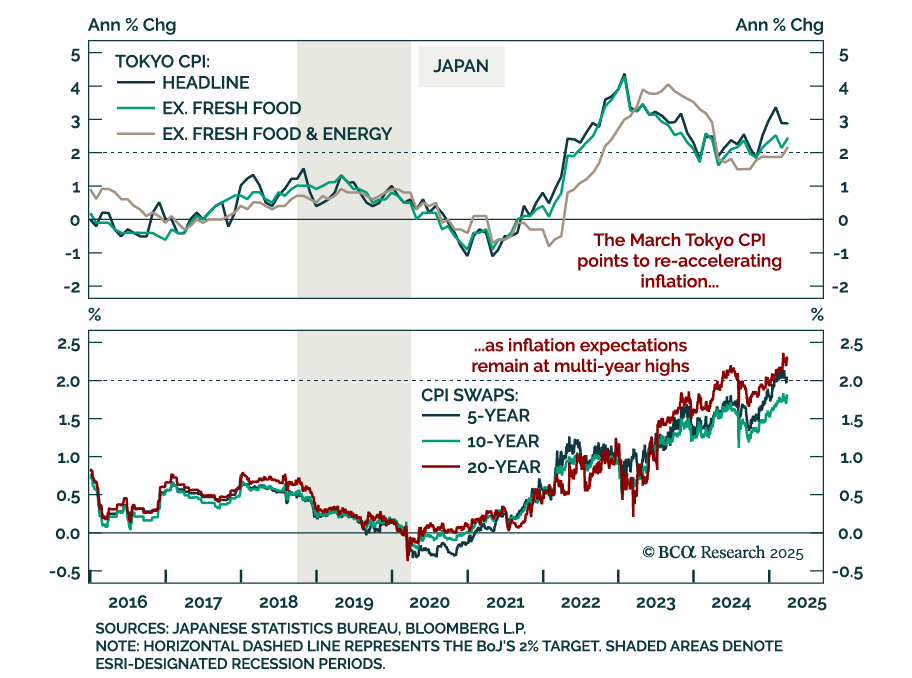

Japan’s inflation pulse remains firm, reinforcing our long JPY stance and cautious view on JGBs. Tokyo CPI for March surprised to the upside, with headline inflation slightly up at 2.9% y/y and “core core” accelerating above the BoJ’s target to 2.2% from…

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

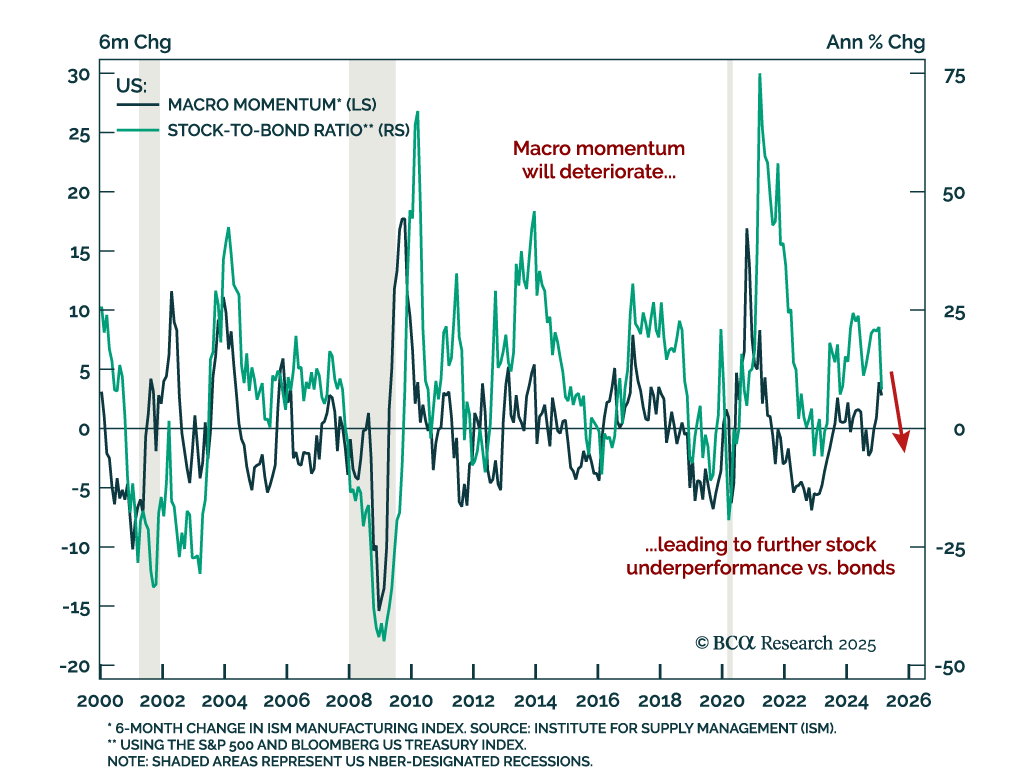

Macro momentum is deteriorating rapidly, and we remain defensively positioned as risks build. Business and consumer confidence have fallen sharply, and while the US post-election period began with optimism, policy uncertainty has since taken over, prompting a…

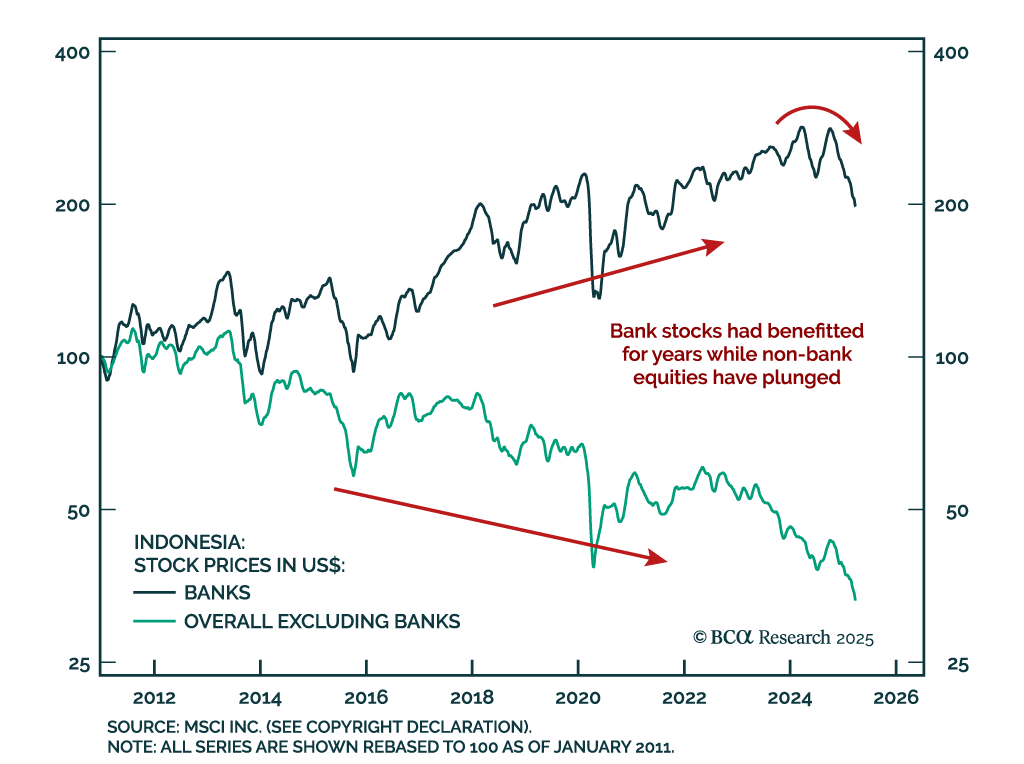

Our Emerging Markets strategists maintain a neutral view on Indonesia within EM equity and bond portfolios but continues to recommend shorting the rupiah versus the US dollar. They are closing their long Indonesian banks/short EM banks position due to…

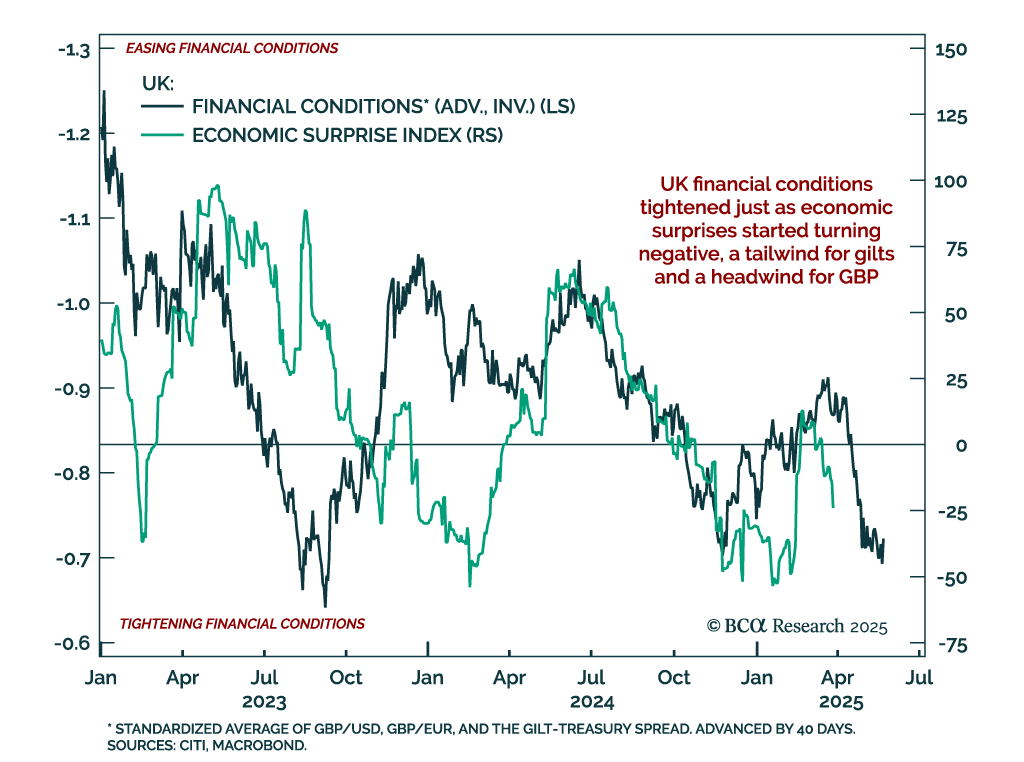

UK financial conditions have tightened just as economic surprises have turned negative, an uncomfortable combination that reinforces our tactical positioning. We remain overweight UK gilts within a global bond portfolio and are tactically short GBP/USD from…

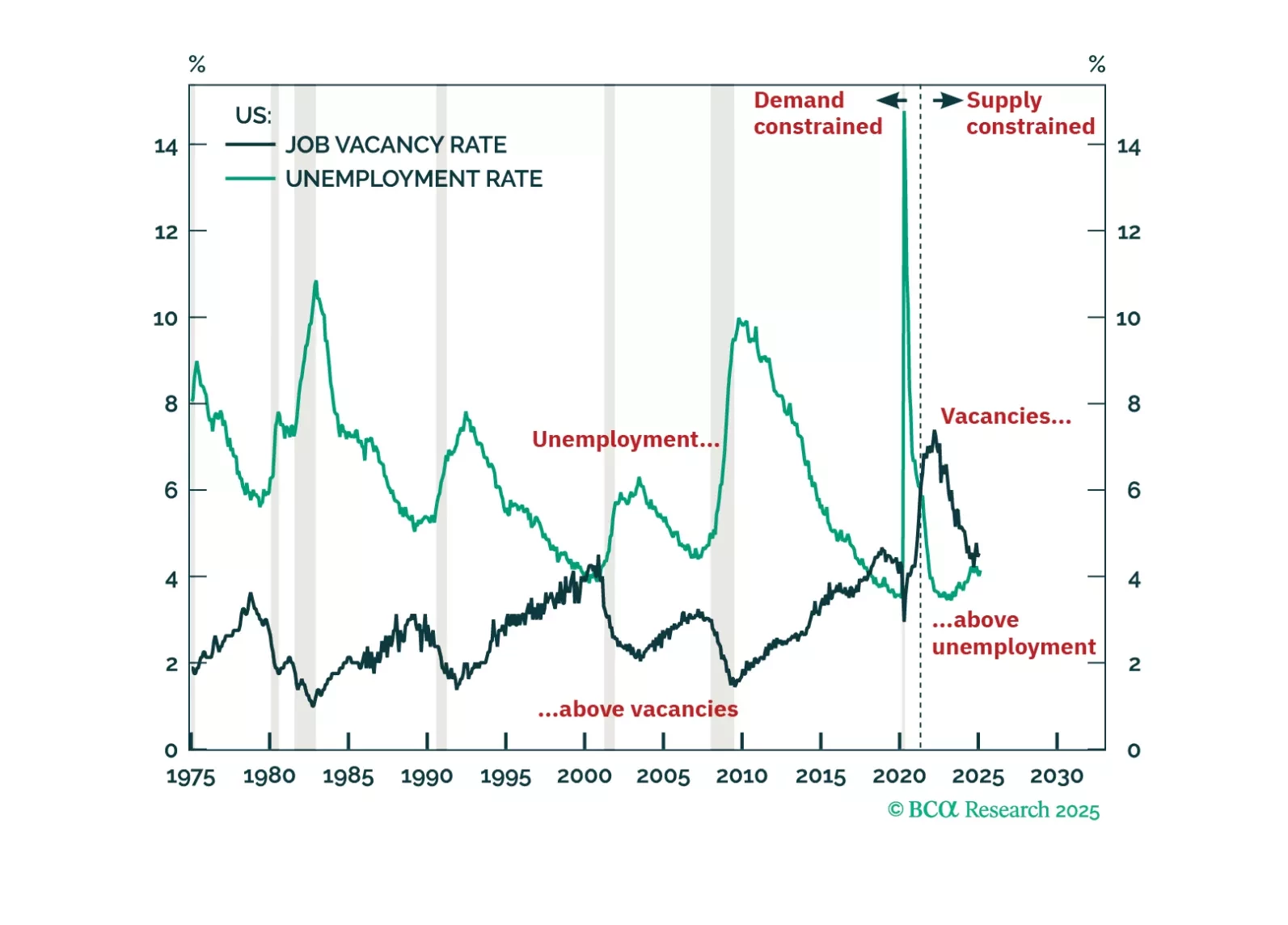

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.