Developed Countries

BCA’s US Beige Book Monitor – an indicator we use to gauge changes in the language of the Fed’s Beige Book report and which historically tracks US GDP growth – has improved in April. Nevertheless — and despite March's hot retail sales and February's…

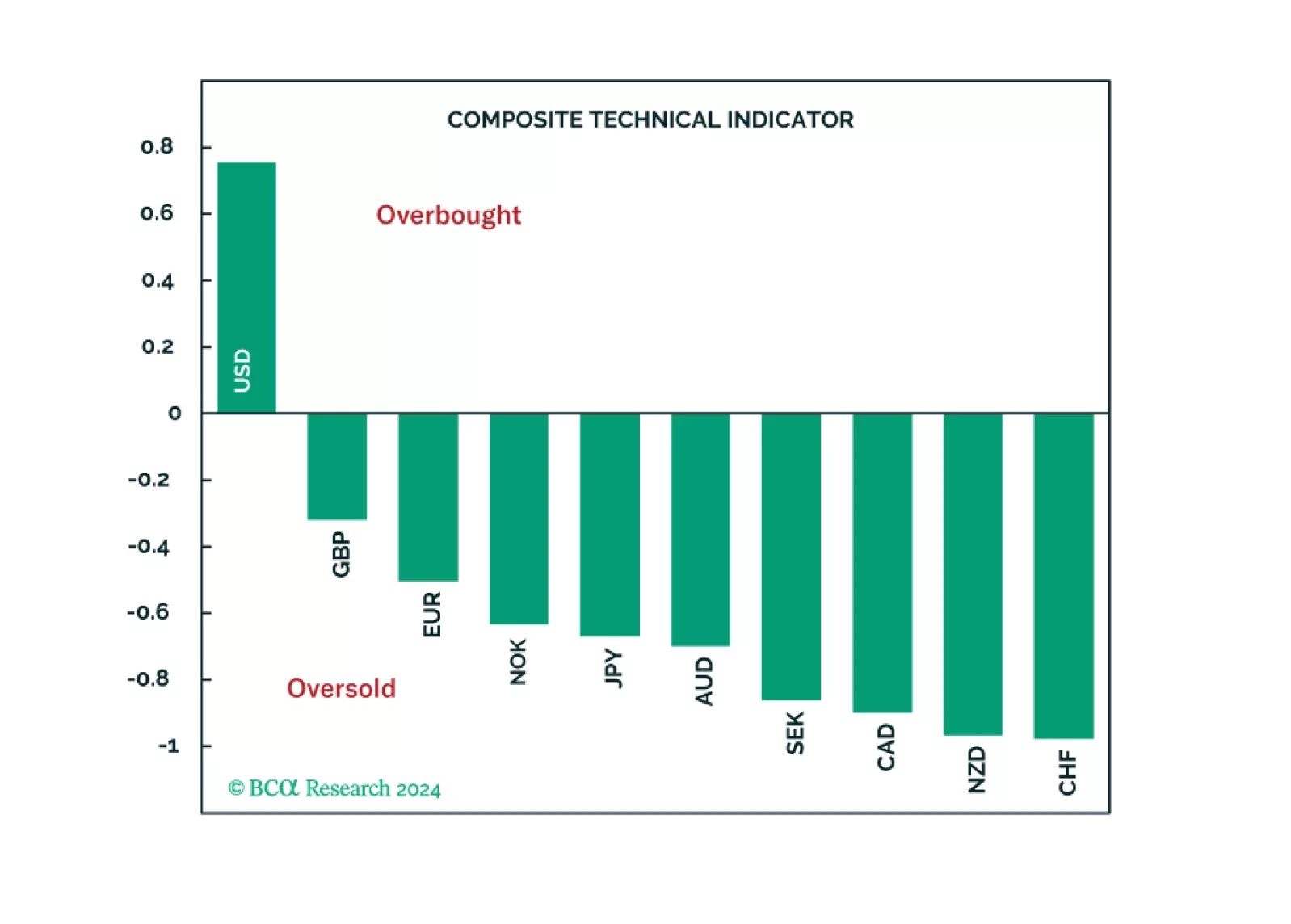

According to BCA Research’s Foreign Exchange Strategy service, an ensemble of technical indicators reveals that the dollar is overbought in the near term. The list of indicators they have compiled for this analysis is simple but potent: How are…

In this report, we review what our technical indicators are telling us about the G10 currencies.

The headline Philadelphia Fed manufacturing survey for April delivered a positive surprise on Thursday, increasing from 3.2 to a twelve-month high of 15.5 and beating expectations it would soften to 2.0. Measures of demand improved with new orders and…

Nvidia has amassed staggering sales from AI. Last year its data center revenues exploded, going from just over $4 billion in 2023 Q1, to over $18 billion in 2023 Q4. That said, its competitors have not done as well. In the same time frame that Nvidia added…

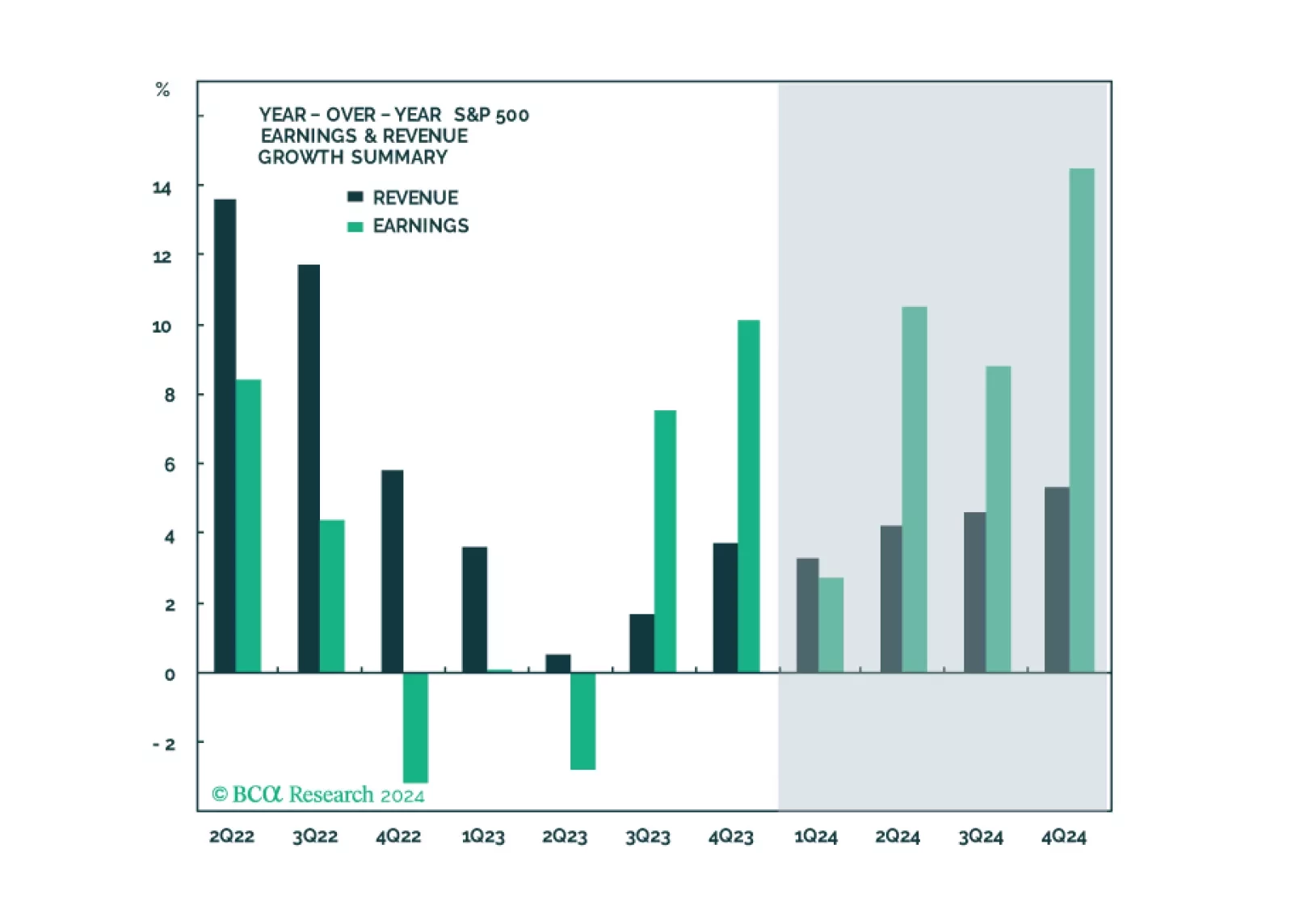

BCA Research’s US Equity Strategy service provides its take on US Q1-24 earnings expectations. Room for surprise? Positive earnings surprises have been a fixture of nearly every earnings season since the darkest days of the pandemic. This quarter will…

UK inflation came in hotter than expected in March. Headline CPI inflation was unchanged at 0.6% m/m – above expectations of a slowdown to 0.4% m/m. Moreover, while the headline and core measures both decelerated on an annual basis, they exceeded consensus…

Developments in US multi-family housing are particularly relevant for the inflation outlook since they inform the future direction of shelter inflation – an important component of CPI inflation. Indeed, the Zillow multi-family rent index leads moves in the…

The US Energy sector has shifted from a capex and growth obsessed industry to one that is more focused on shareholder returns. ESG as well as the collapse in oil prices during the 2010s were the main culprits. Divesture due to ESG mandates on portfolios…

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.