Warsh’s Tactical Window

Mixed labor and inflation data should create a window for the Warsh Fed to keep rates on hold. We recently highlighted an important nuance to the communication changes so far: explicit guidance is removed, yet implicit guidance remains. The Warsh Fed will also aim to take more guidance from markets.

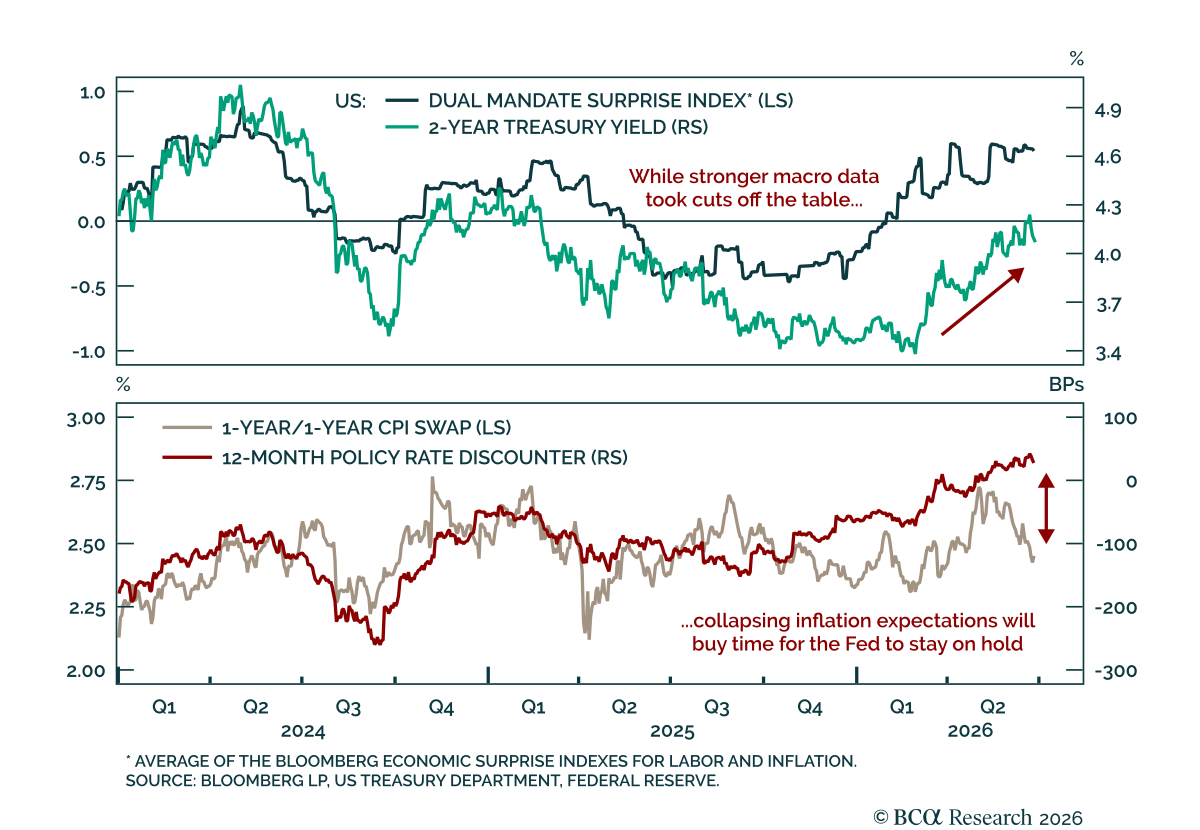

Markets are an efficient discounting mechanism, but they do not have perfect foresight, which is why economic surprises play a central role in price action. We built a simple indicator of data surprises tied to the Fed’s dual mandate, employment and inflation, which has historically been a good predictor of front-end Treasury yields. Both labor and inflation surprises ticked up since the start of the year. The labor market has shown resilience through the energy shock. Inflation has also ticked up, but has remained roughly in line with forecasts so far. That distinction matters. Elevated inflation can avoid shaking out markets as long as it continues to print at or below expectations.

Inflation is currently slightly above the Fed’s end-of-year estimates, but it should cool on the back of lower energy prices. What is notable is that cuts were priced out, and hikes priced in, just as inflation expectations collapsed alongside oil prices. In the near term, that creates a window for the Fed to stay put. While cuts are off the table, the case for significant tightening will not be straightforward unless the labor market picks up materially. Thursday’s US jobs report will therefore be key for the direction of rates and risk assets in the following weeks. For now, our US Bond strategists recommend fading the hawkishness priced into the curve. They have closed their 5-year/30-year Treasury flattener recommendation and entering 2-year/30-year steepeners.