Making Fed-Watching Great Again

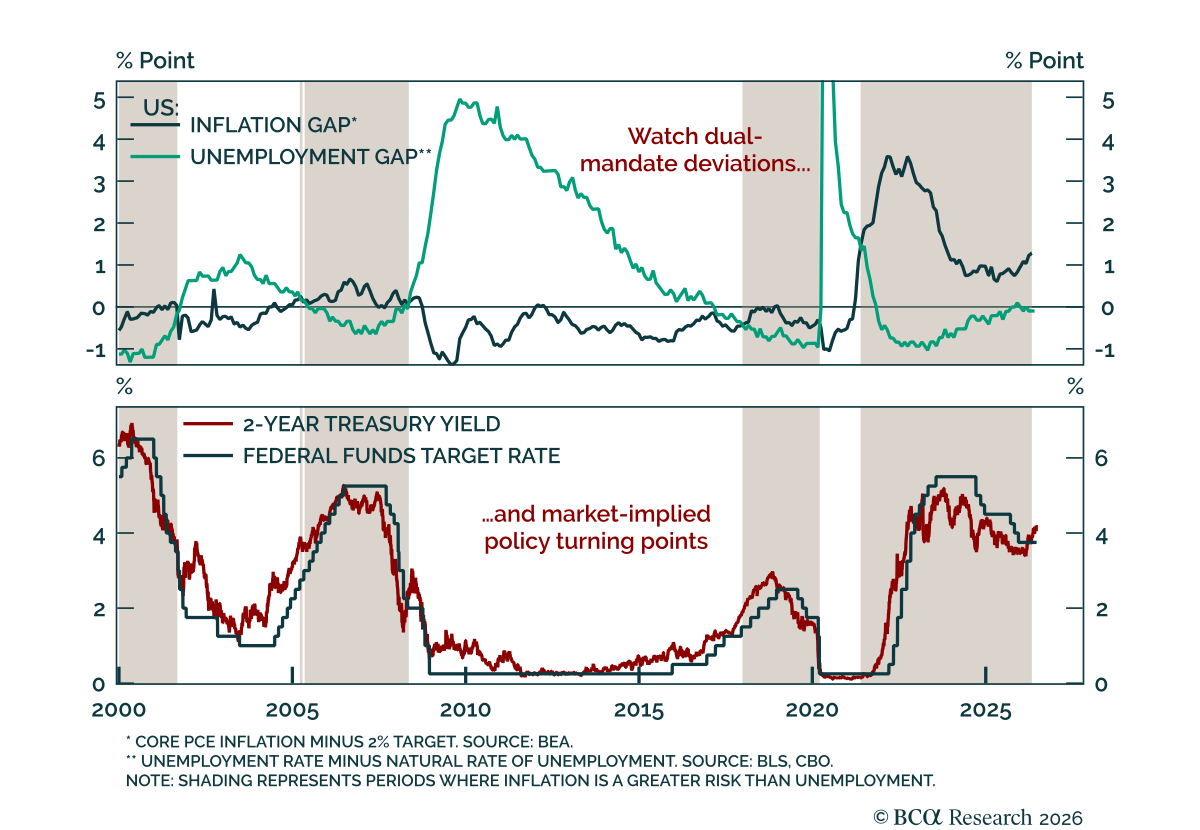

New Fed Chair Kevin Warsh wants to make Fed-watching great again. The Warsh Fed will speak less and guide less. There is, however, an important nuance to the communication changes so far. While explicit guidance was removed, some implicit guidance remains, as inflation was prioritized over employment. Two charts can help investors navigate this new era.

First, the Fed’s focus tends to be determined by how far inflation and unemployment deviate from their dual-mandate benchmarks. Periods when inflation exceeds target more than unemployment are associated with tighter monetary policy, and vice versa. Second, Warsh also wants to avoid giving too much guidance to get cleaner market signals not distorted by Fed forecasts. Investors should therefore monitor the spread between the 2-year Treasury yield and the federal funds rate. Instances when the 2-year yield, a proxy for markets’ short-term policy expectations, crosses below or above the federal funds rate have historically preceded or coincided with turning points in the business cycle, and thus monetary policy.

More volatility can be expected around economic data releases, especially employment and inflation reports. However, the timing of introducing more uncertainty and volatility around Fed decisions may not matter much, as the economy currently does not depend heavily on interest rates. A bit more valuation volatility will likely be overshadowed by a strong earnings profile.