Consumer

Recent data releases have painted a mixed picture of US housing market dynamics. On the one hand, housing starts and building permits unexpectedly increased on a month-on-month basis in October. After falling in 2022, housing starts have somewhat…

Oil prices have relapsed despite the supply cuts and the geopolitical volatility stemming from the Middle East. Odds are that global oil demand is downshifting. The chart above illustrates that there is a tight relationship between crude oil prices and the…

The latest house price data indicate that China's housing market remains weak. The prices of newly built homes across 70 medium and large Chinese cities declined by 0.4% m/m in October – a faster pace of decline than the 0.3% m/m drop registered in September…

The US retail sales release delivered a mixed signal about US consumption. Although the headline figure contracted by 0.1% m/m in October, it was better than expectations of a 0.3% m/m decline. Moreover, the September increase was revised up from 0.7% m/m to…

On the surface, the acceleration in Chinese retail sales and industrial production growth in October suggests that the economy is holding up. Retail sales expanded by 7.6% y/y last month – beating expectations of 7.0% y/y following a 5.5% y/y increase in…

According to BCA Research’s China Investment Strategy service, Chinese policymakers are facing the Impossible Trinity. When faced with rapid currency depreciation in August-September, the PBoC deliberately tightened liquidity and steered interest rates…

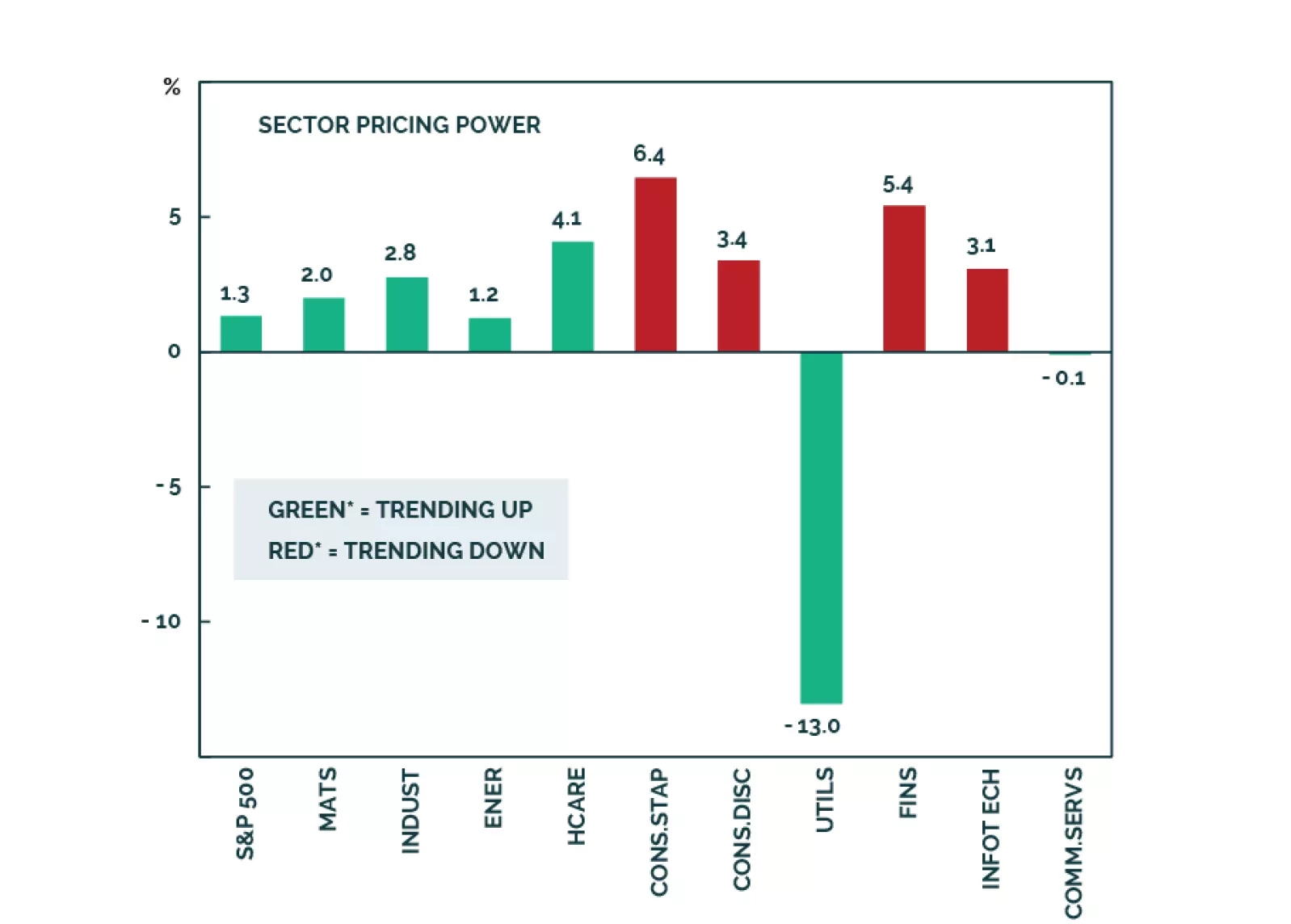

To the extent that US small businesses are typically more exposed to domestic economic conditions than larger firms, results of the NFIB Small Business Economic Trends survey are instructive. One important trend is that the October survey results…

China's money and credit data remained weak in October. New total social financing amounted to RMB 1.85 trillion – less than the RMB 1.95 trillion anticipated and below the prior month's increase of RMB 4.12 trillion. Similarly, loans extended by banks fell…

Our equally weighted global cyclical equity index has outperformed equally weighted defensives for most of this year. By October 17, this outperformance stood at about 12.6%. This outperformance is consistent with US Treasury market dynamics. The relative…

Q3 earnings commentary has been broadly positive, despite intensifying macro headwinds. Going forward, a negative growth outlook and geopolitical risks, are a threat to buoyant earnings expectations. We project that earnings growth for 2024 will move lower than currently projected - a negative for equities. This Santa Claus rally is unlikely to be the start of a new bull market.