Fixed Income

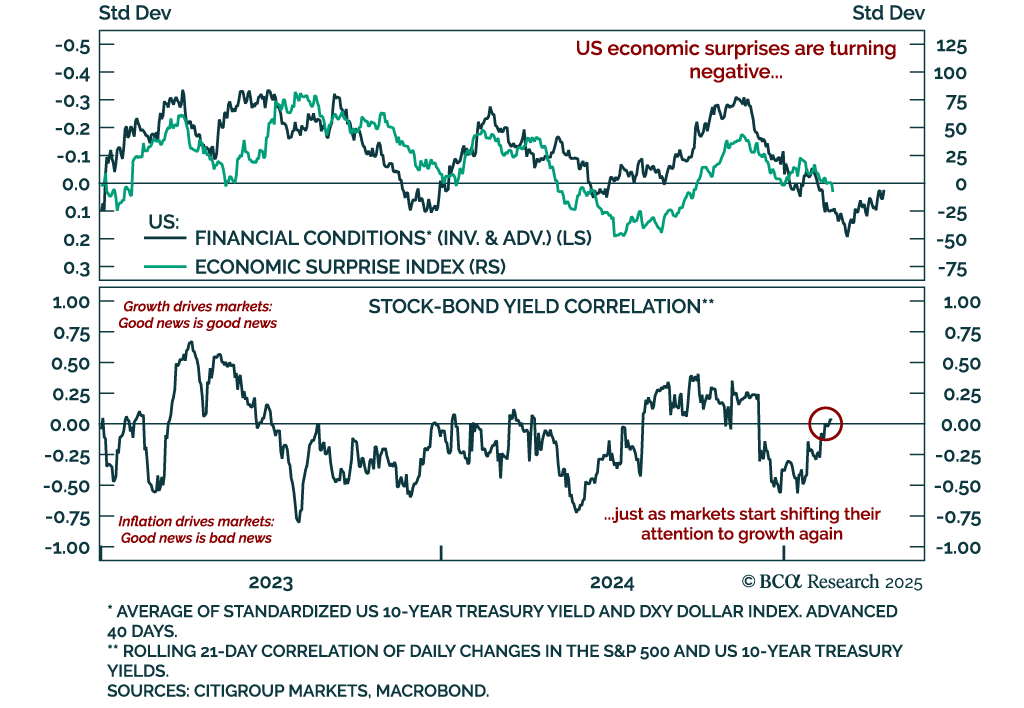

The US (and the UK) is staring down the barrel of a ‘mini-stagflation’ until a deflationary shock arrives to neutralise it. We describe a likely source for the deflationary shock and list three investment conclusions that are valid irrespective of how long it takes for the deflationary shock to arrive. Plus: RCI.B is deeply oversold and ripe for a rebound.

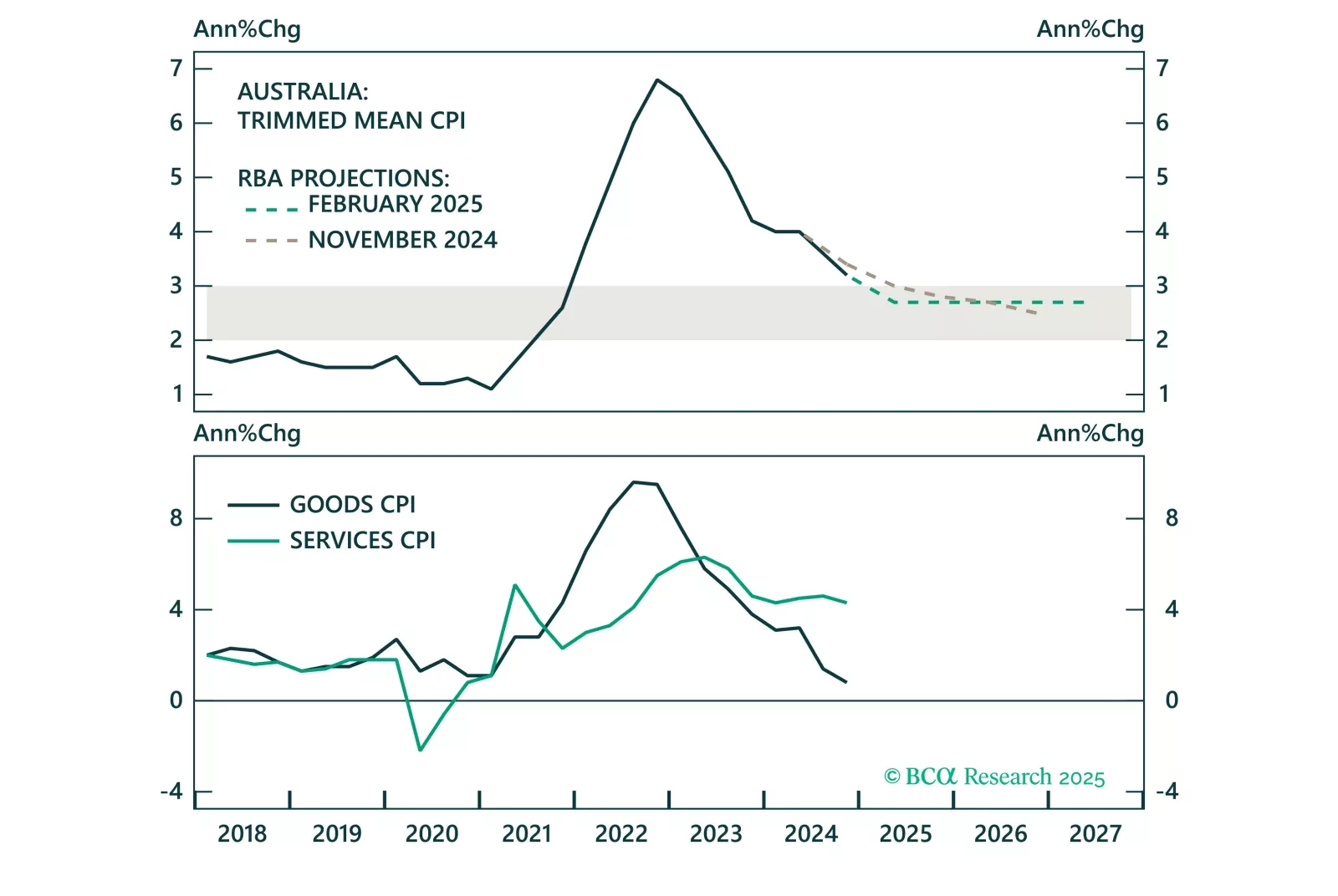

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

In lieu of all the geopolitical and economic news in media, this report looks at where next the dollar is likely to trend in the next one-to-three months. Our view is down, though on a cyclical horizon (six-to-twelve months), we would not be short the dollar, for now.

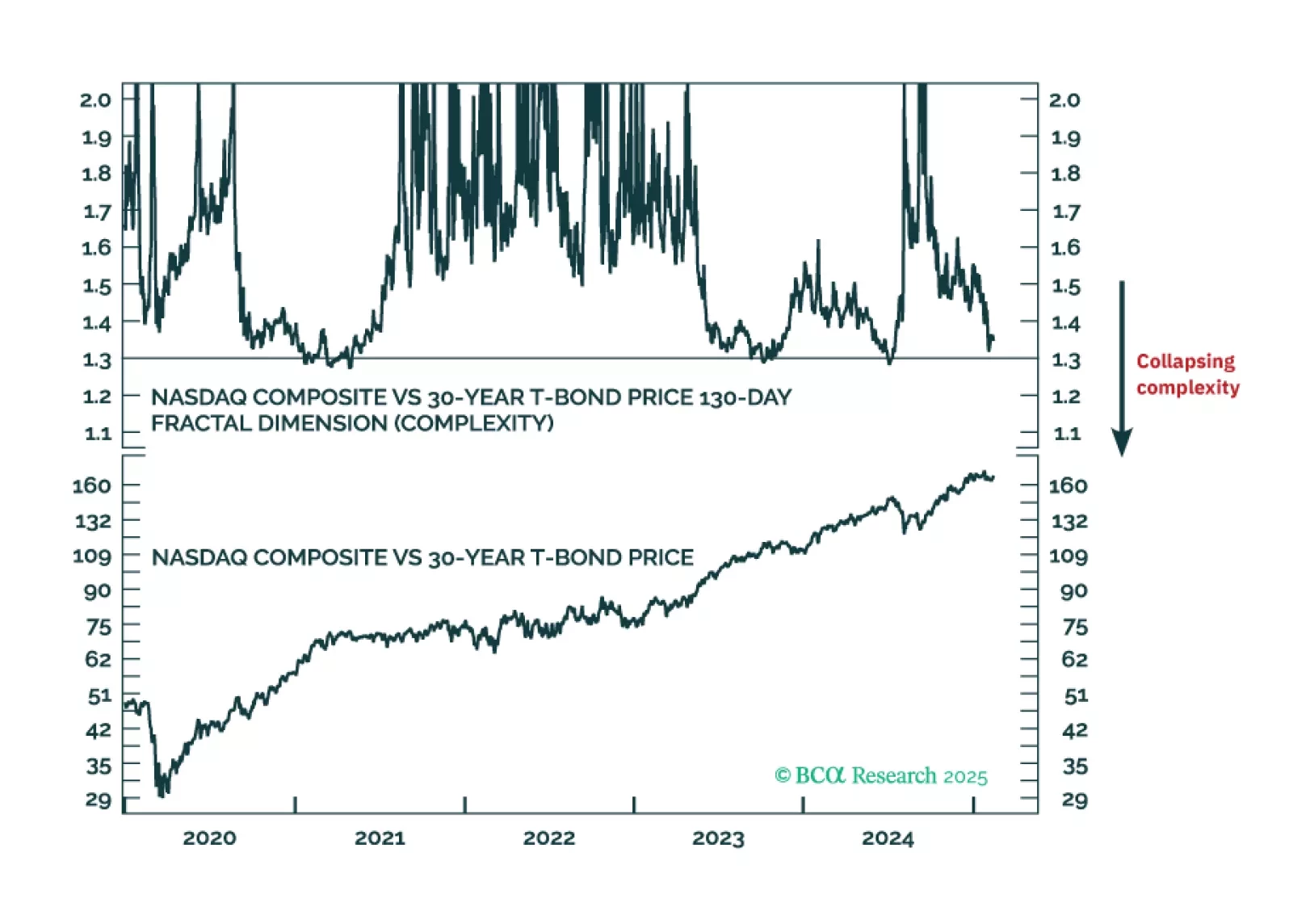

If the 130-day complexity of the Nasdaq versus 30-year T-bond collapsed to 1.30, it would signal the risk of a -20 percent market slump. This indicator, at 1.37, is not yet at critical, but we recommend that you keep a close eye on it on our website. Plus: an update on our recent trades.