Economy

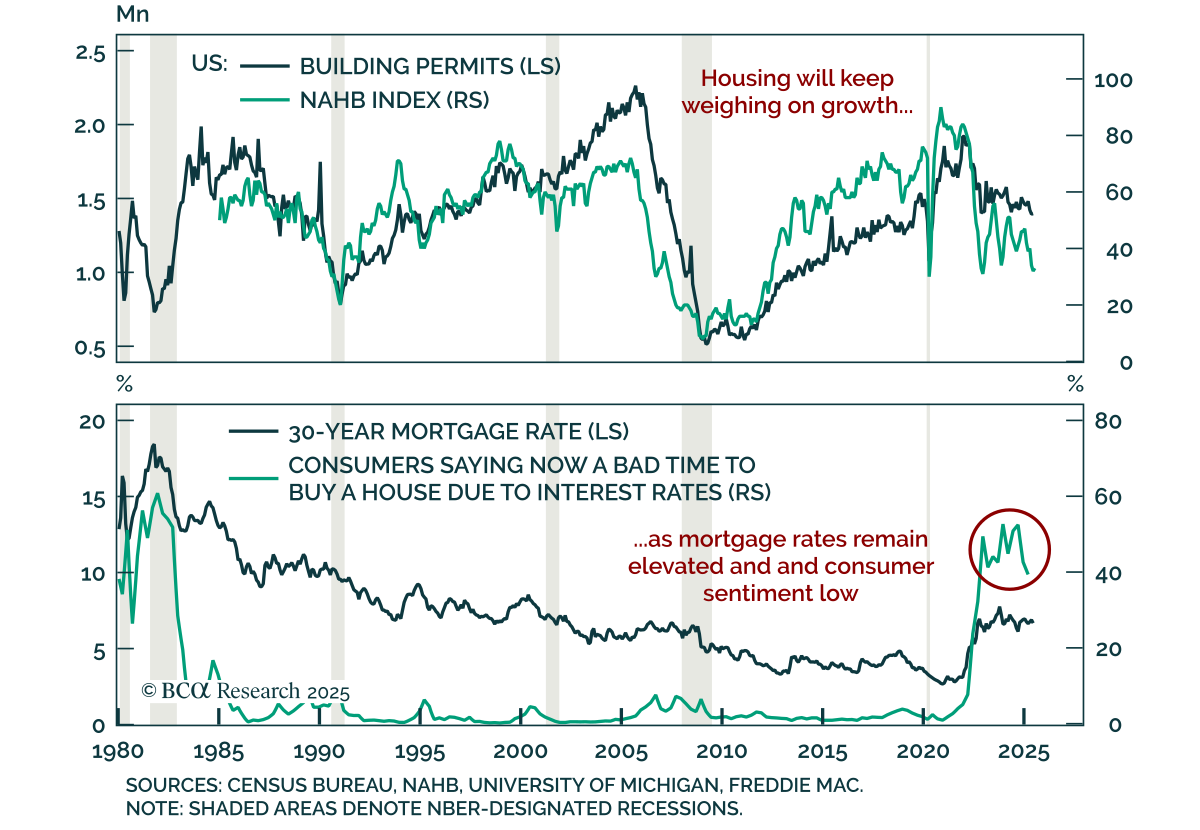

June US housing data surprised to the upside, but the broader sector is still weak, reinforcing our modest underweight on equities. Housing starts rose an annualized 4.6% m/m, and building permits ticked up 0.2% after a 2.0% decline in May. Gains were…

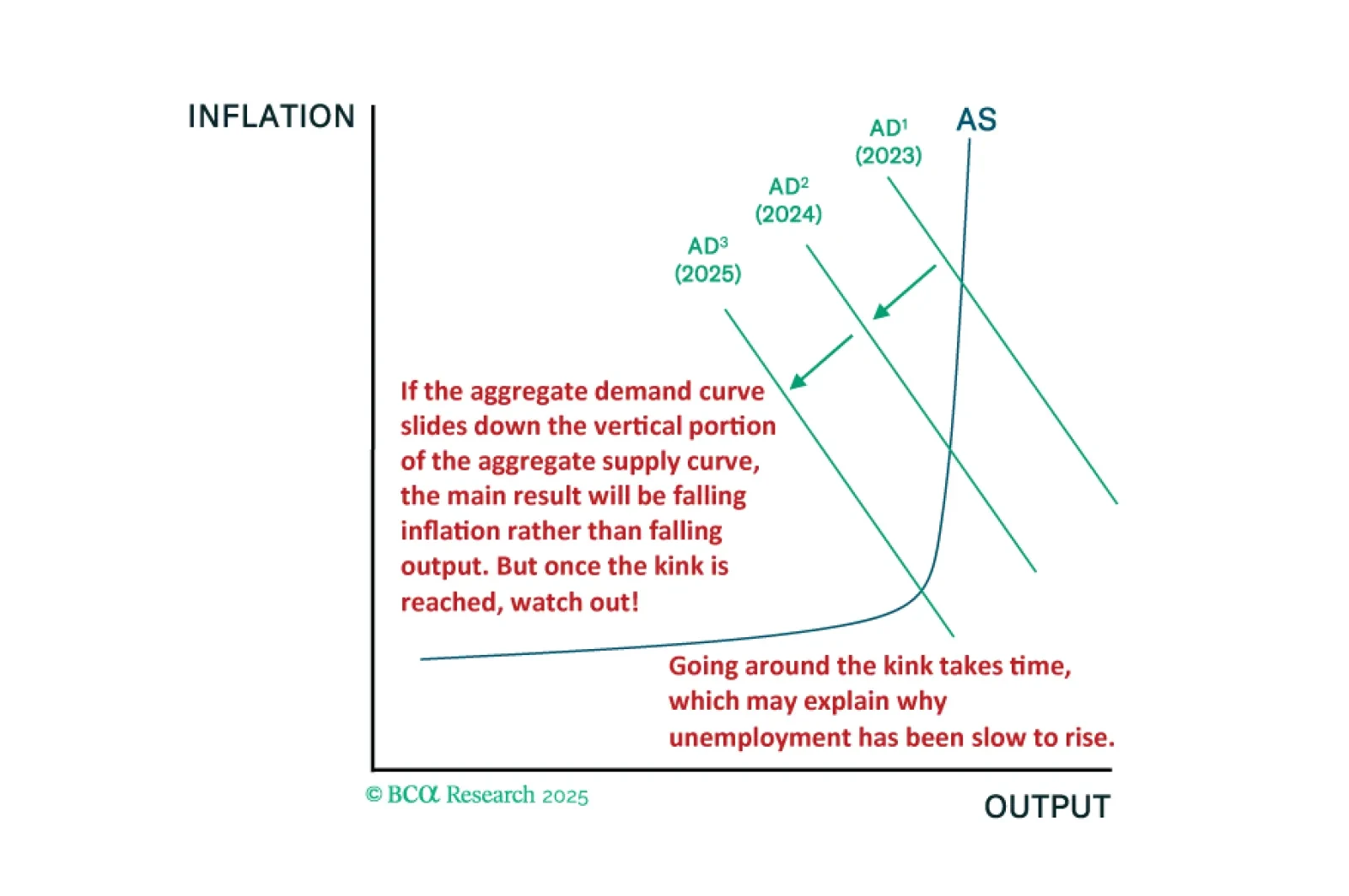

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

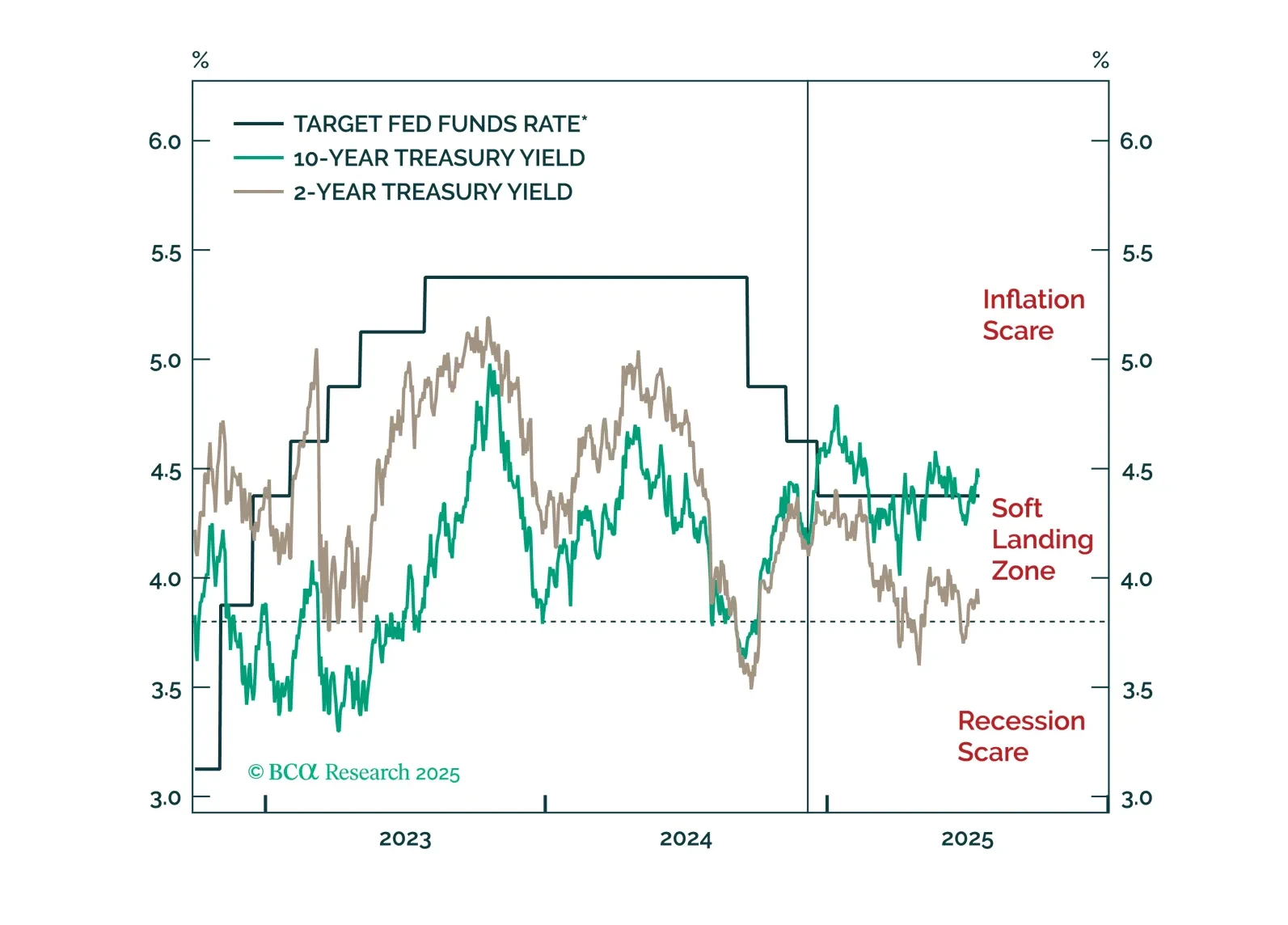

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

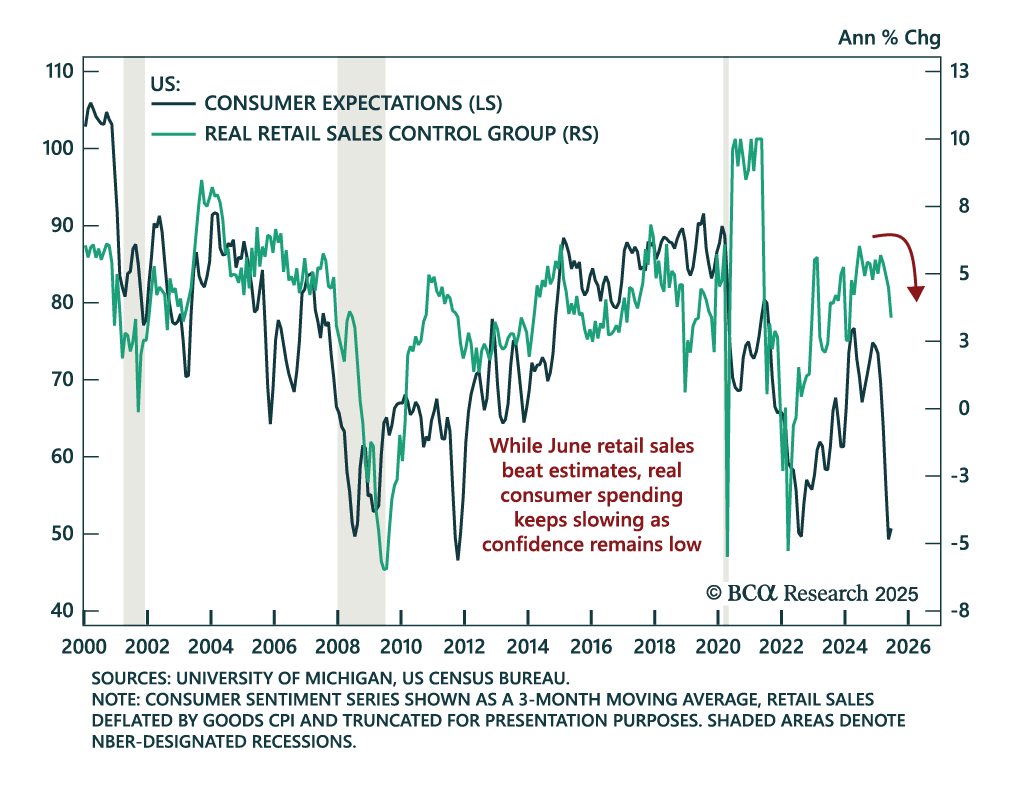

June retail sales beat across the board, but inflation and a slowing trend reinforce our defensive stance. Headline and core retail sales rose 0.6% m/m, while the control group climbed 0.5%. Spending on food services and drinking places, used as a proxy for…

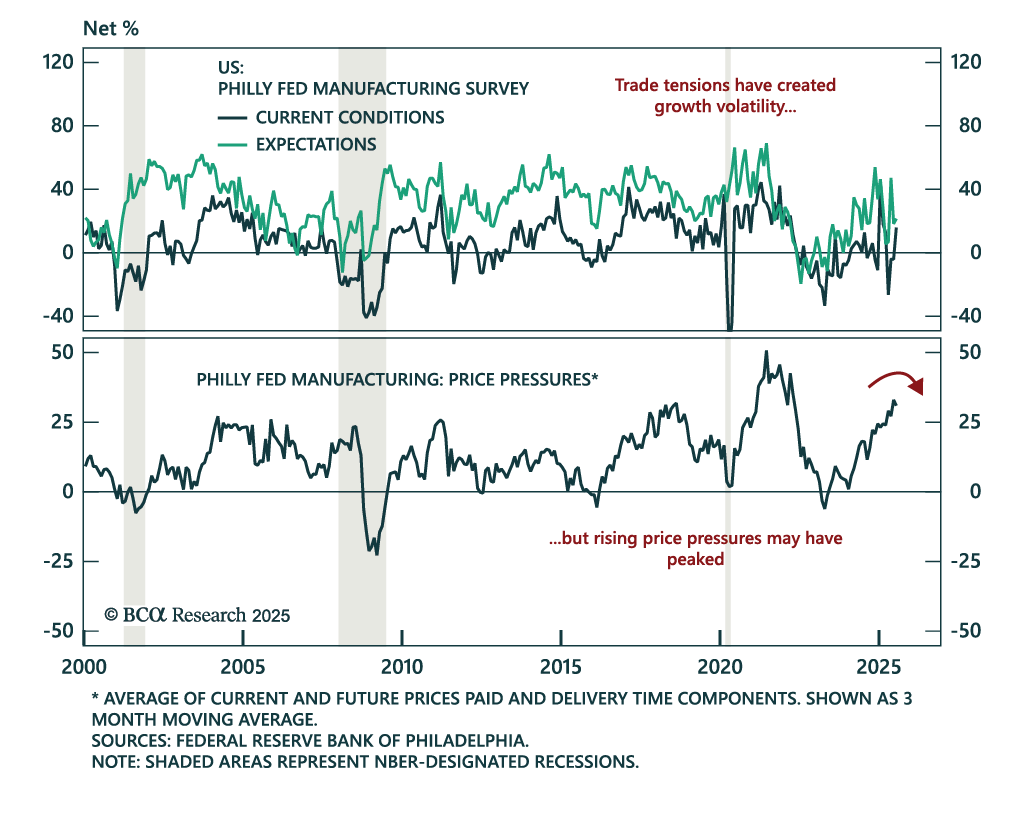

The July Philly Fed beat expectations with broad improvement in activity, but low growth, inventory buildup and margin pressure remains a risk for equities. The headline index rose to 15.9 from -4.0 in June. New orders, shipments, and employment all…

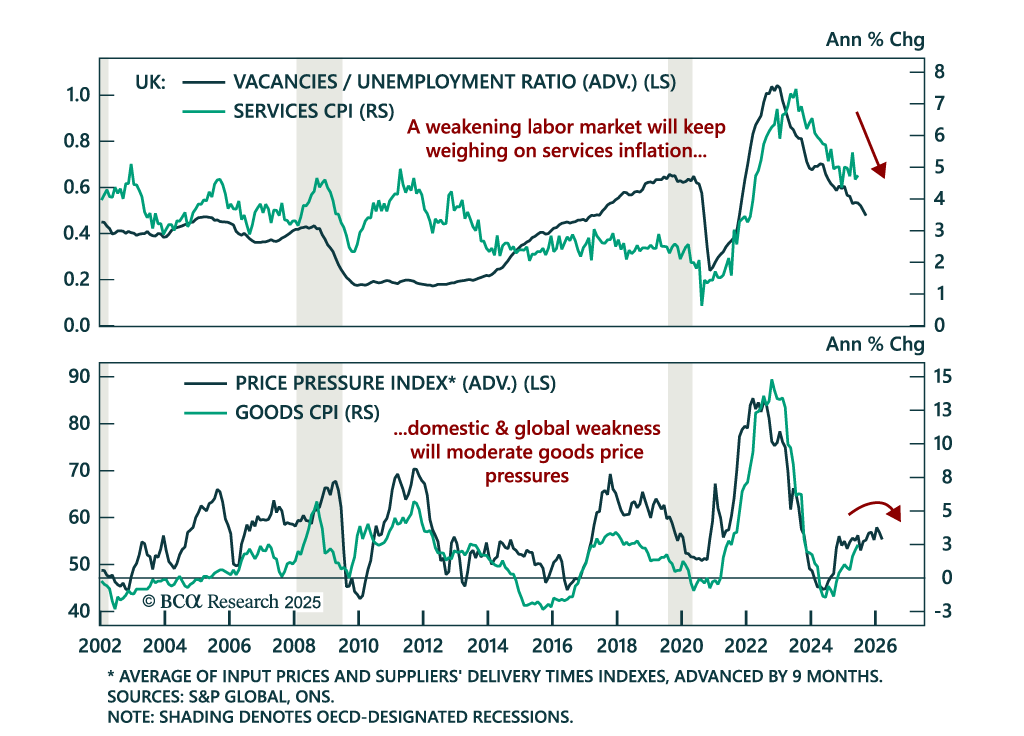

June UK CPI surprised to the upside, but weakening leading indicators point to disinflation ahead. Stay overweight Gilts. Headline inflation accelerated to 3.6% y/y from 3.4%, and core rose to 3.7% from 3.5%. Services inflation held at 4.7%, also above…

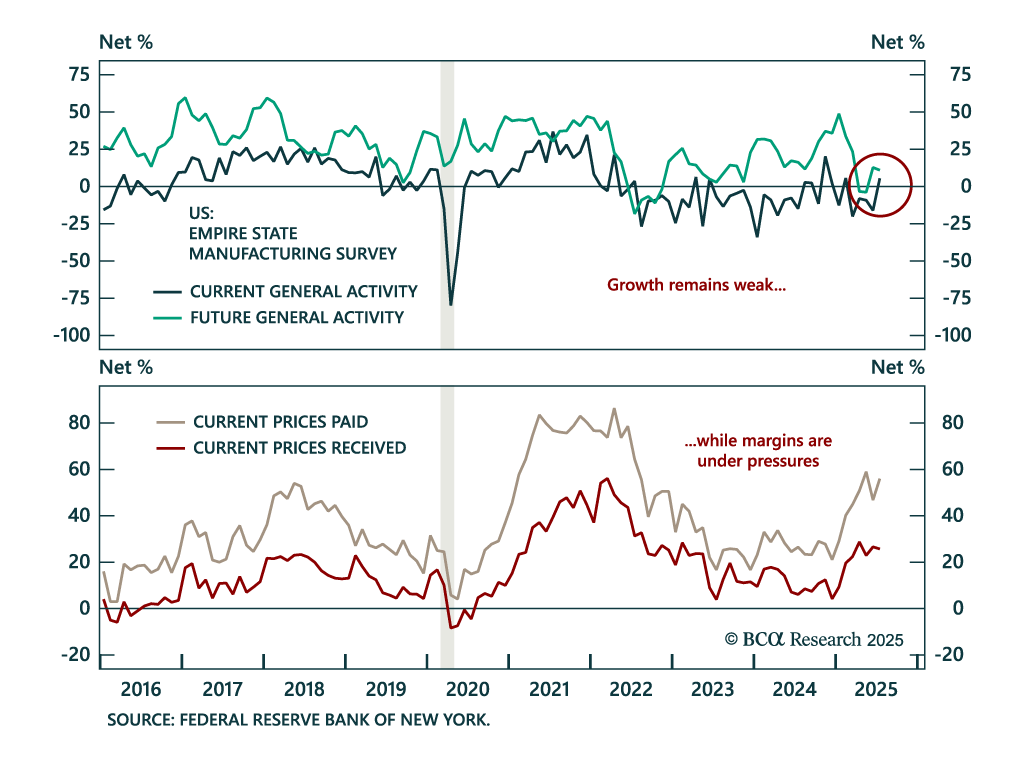

The July Empire Fed beat estimates, but survey volatility, inventory distortions, and shallow strength dampen this signal. The headline index surged to 5.5 from -16.0, supported by gains in shipments, employment, and capex intentions. However, new…

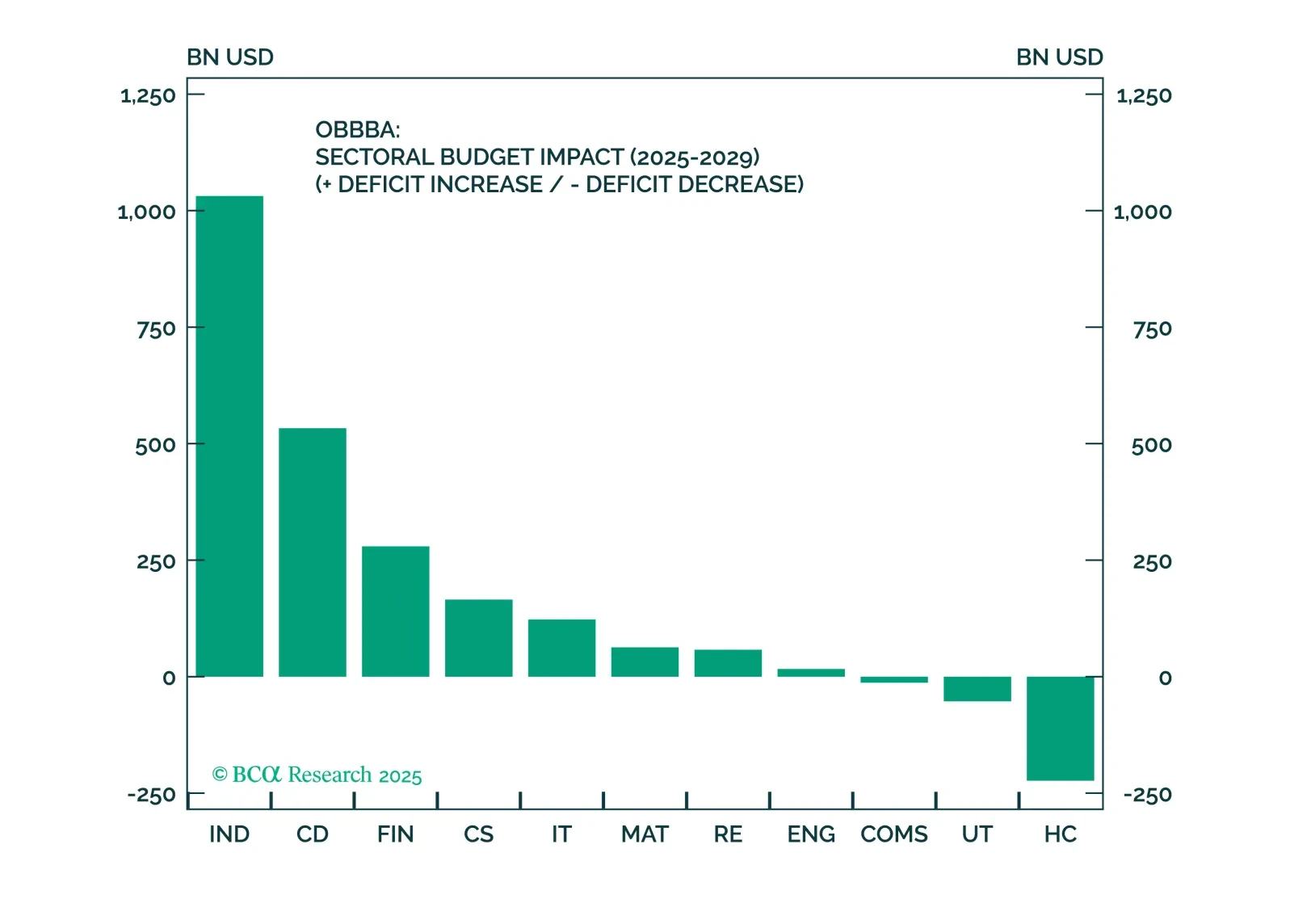

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

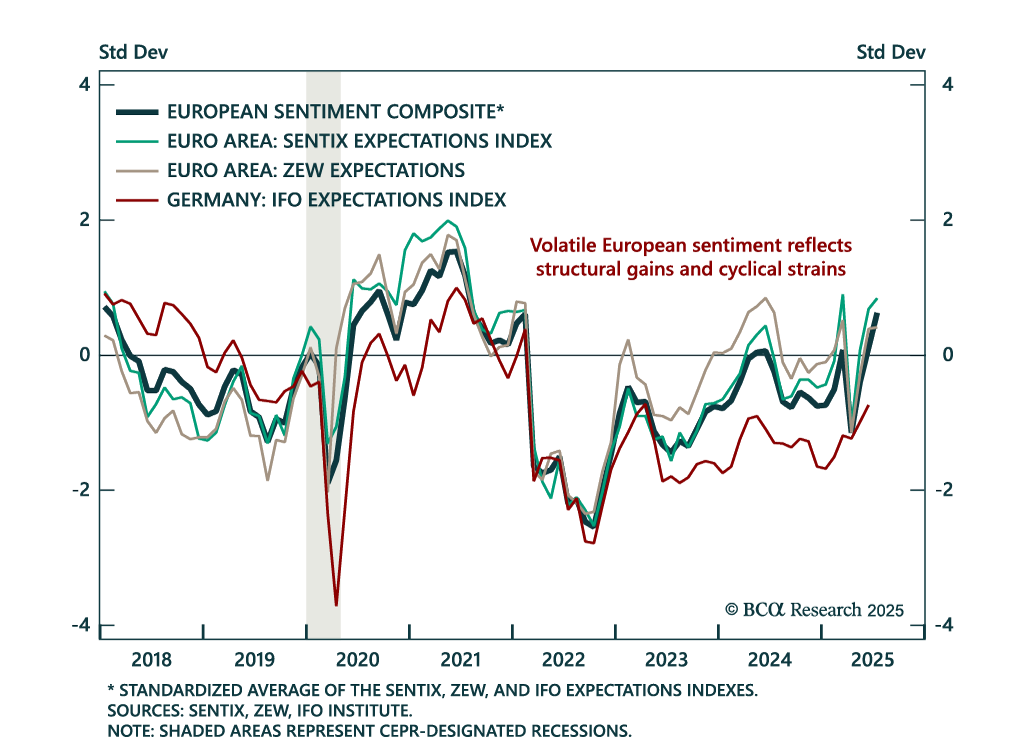

July’s ZEW data confirmed improving sentiment in Europe, but near-term conditions remain fragile, reinforcing a buy-on-dips stance for long-term investors. Euro area expectations rose to 36.1 from 35.3, with Germany also improving to beat expectations.…

June CPI was broadly in line with expectations, with tariff passthrough building in goods but broader inflation pressures likely to remain contained. Headline inflation came in slightly above expectations at 2.7% y/y (0.3% m/m), while core matched estimates…