Equities

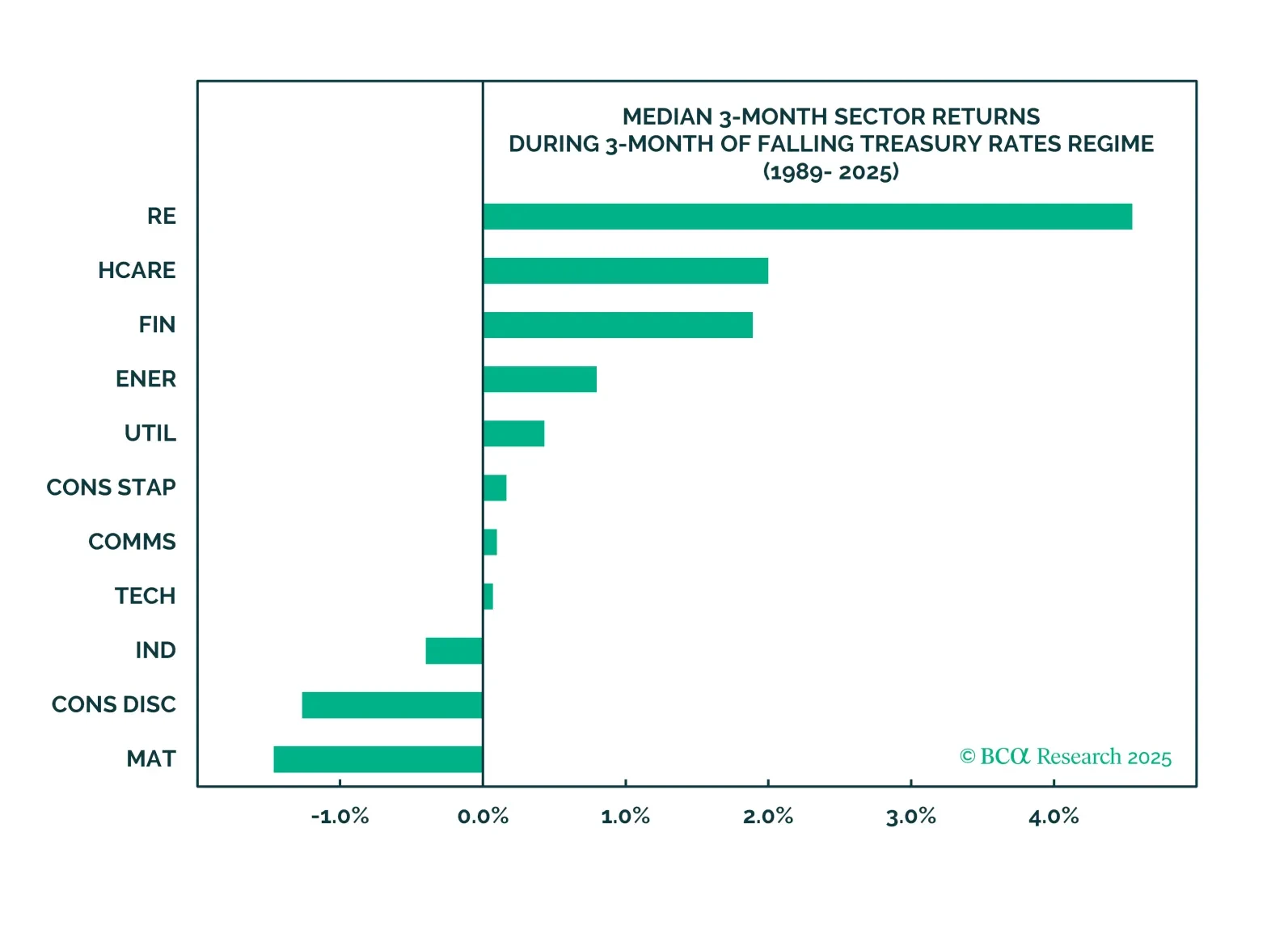

Real Estate performance is contingent upon the Fed rate-cutting cycle. Yet, we worry about a hawkish Fed surprise and are closing our overweight in the sector. We also recommend a granular approach to subsector selection.

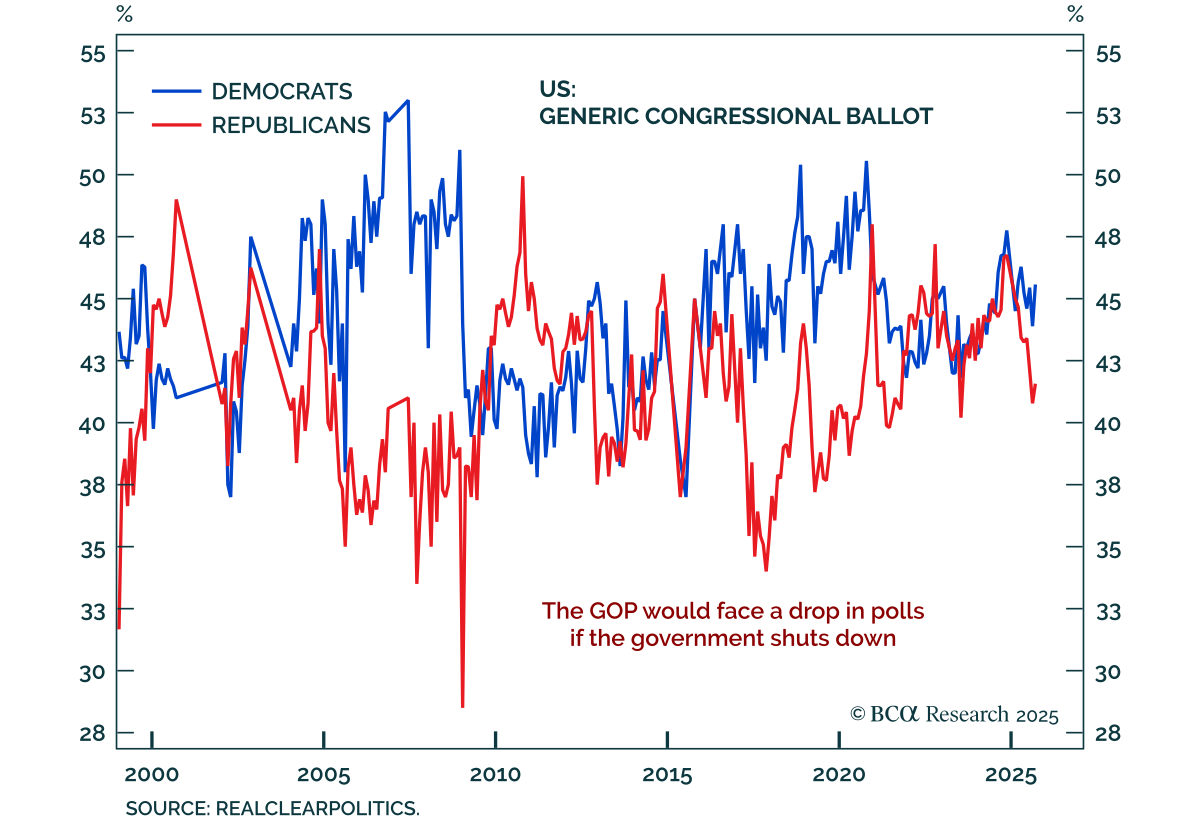

Will the US federal government shutdown on October 1? Congressional leaders are meeting with President Trump in the White House as we go to press. If eight Democratic senators do not vote with Republicans to pass a no-frills "continuing resolution" by…

European sentiment surveys disappointed in September, pointing to a tactical headwind for assets even as the long-term outlook stays constructive. The flash consumer confidence print beat expectations but remained sluggish, while the Sentix and ZEW surveys…

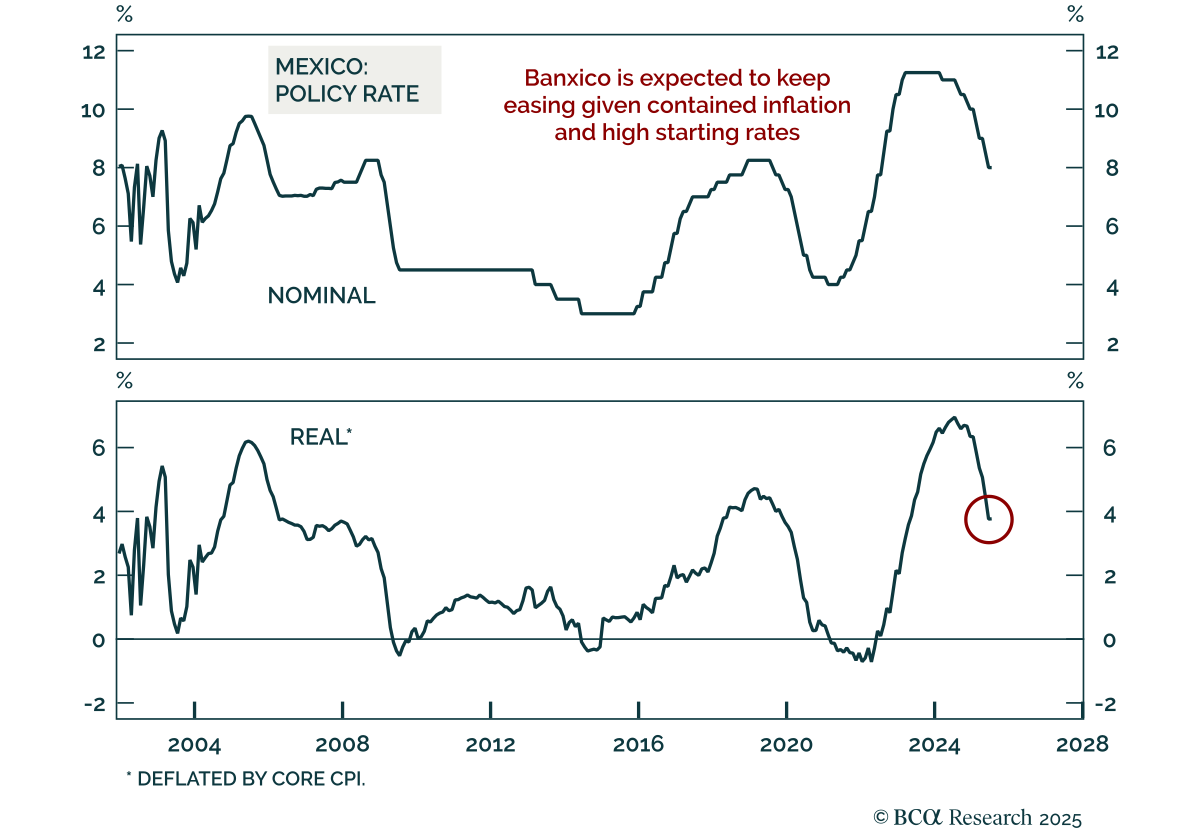

Banxico cut rates to 7.5%, reinforcing our call to go long Mexican local bonds and overweight Mexico across EM portfolios. Inflation is within target, giving policymakers space to ease. Sound fiscal management and strong external accounts continue to support…

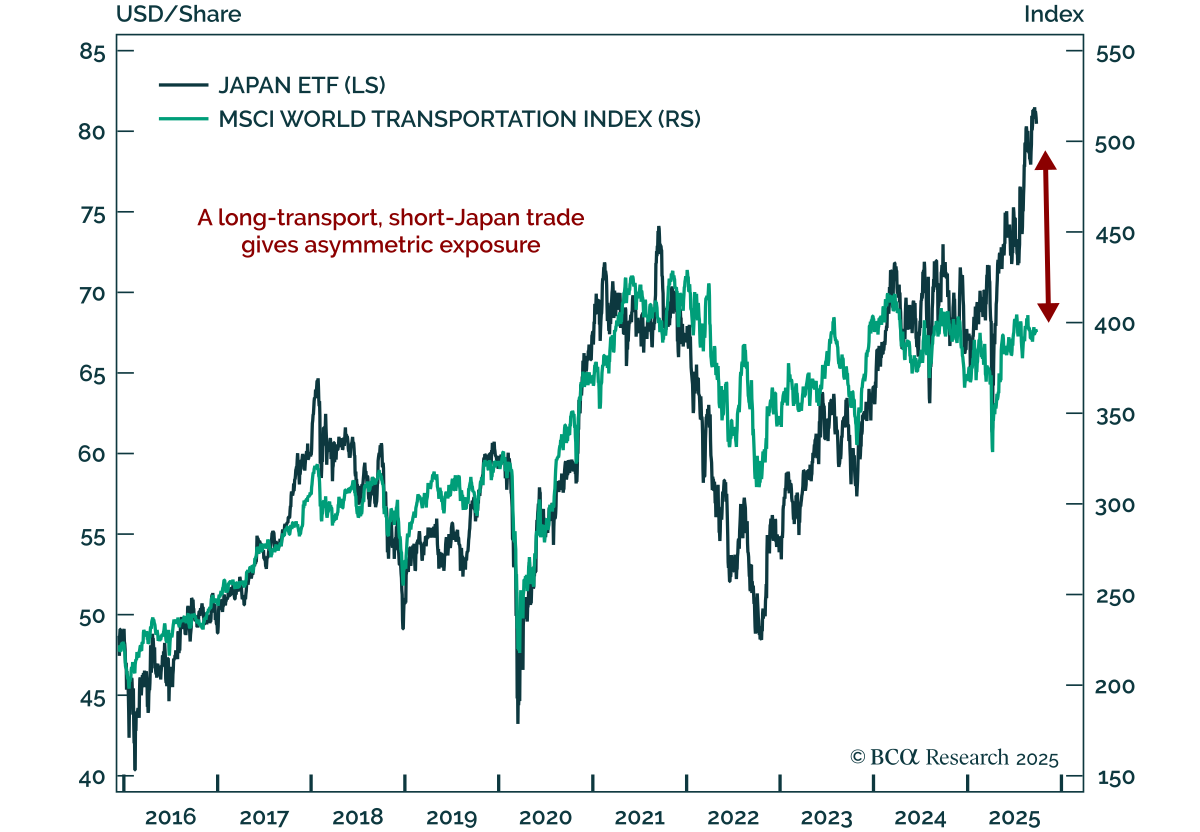

Sell Japanese equities and buy global transportation stocks to capture an overdue mean-reversion in trade-exposed assets. Our Chart Of The Week comes from Mathieu Savary, Chief DM ex. US Strategist. The post-Liberation Day rally lifted the unhedged…

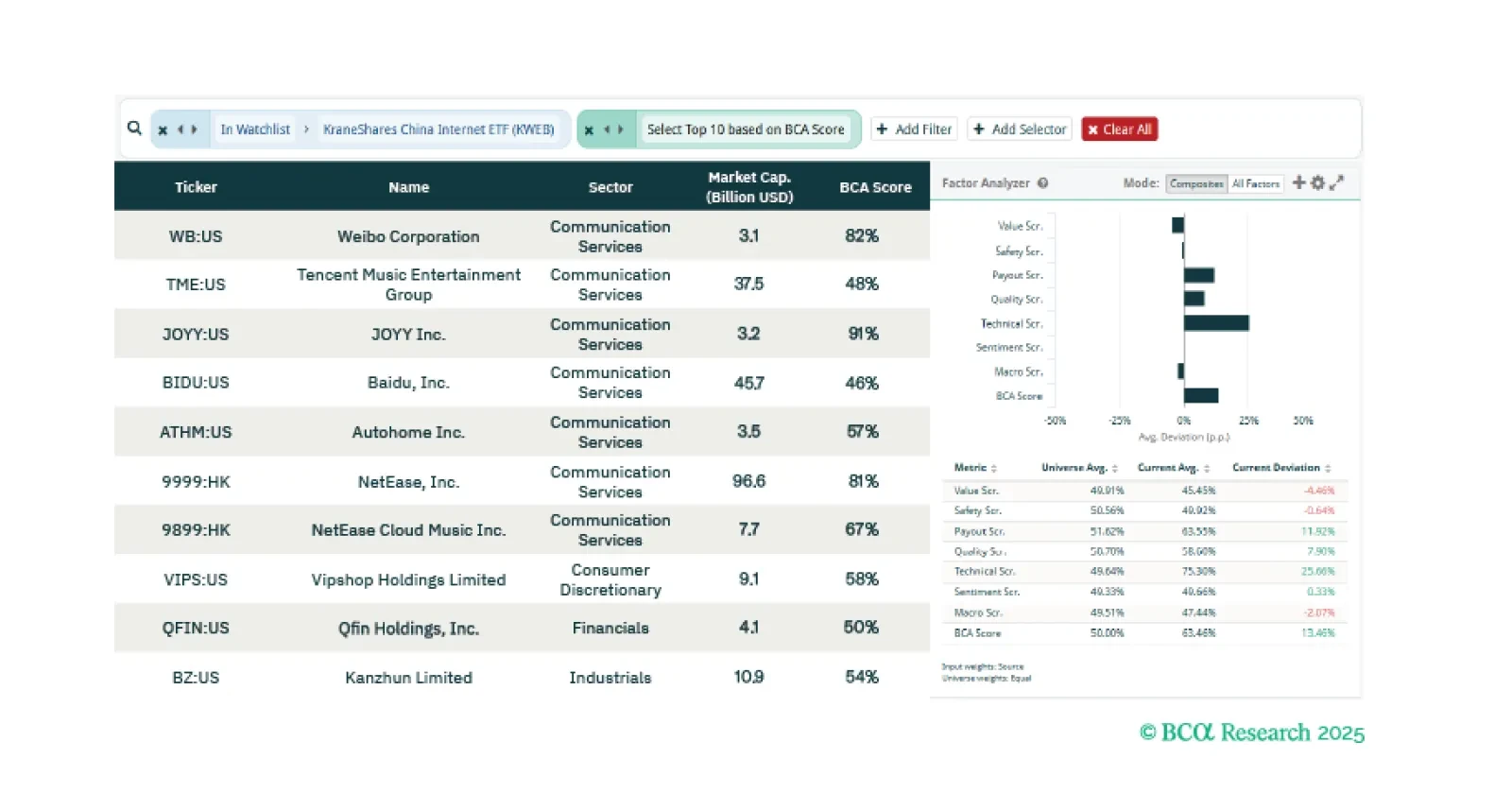

This week our screeners explore offshore Chinese internet stocks, US Healthcare equities, and sectoral opportunities in the Canadian bourse.

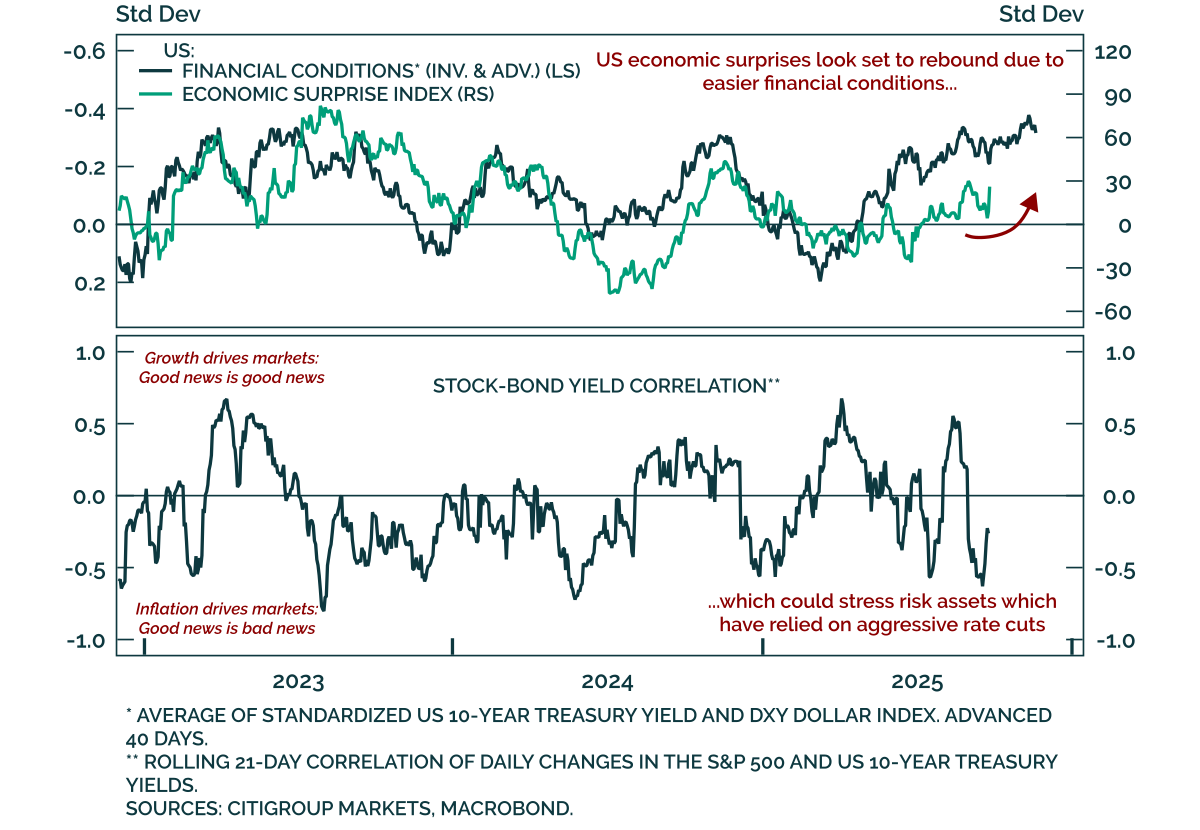

Our tactical framework, which tracks the reflexive loop between financial conditions and economic surprises, points to stronger near-term growth, leaving equities vulnerable if inflation re-accelerates. Data surprises move markets, while bond yields and the…

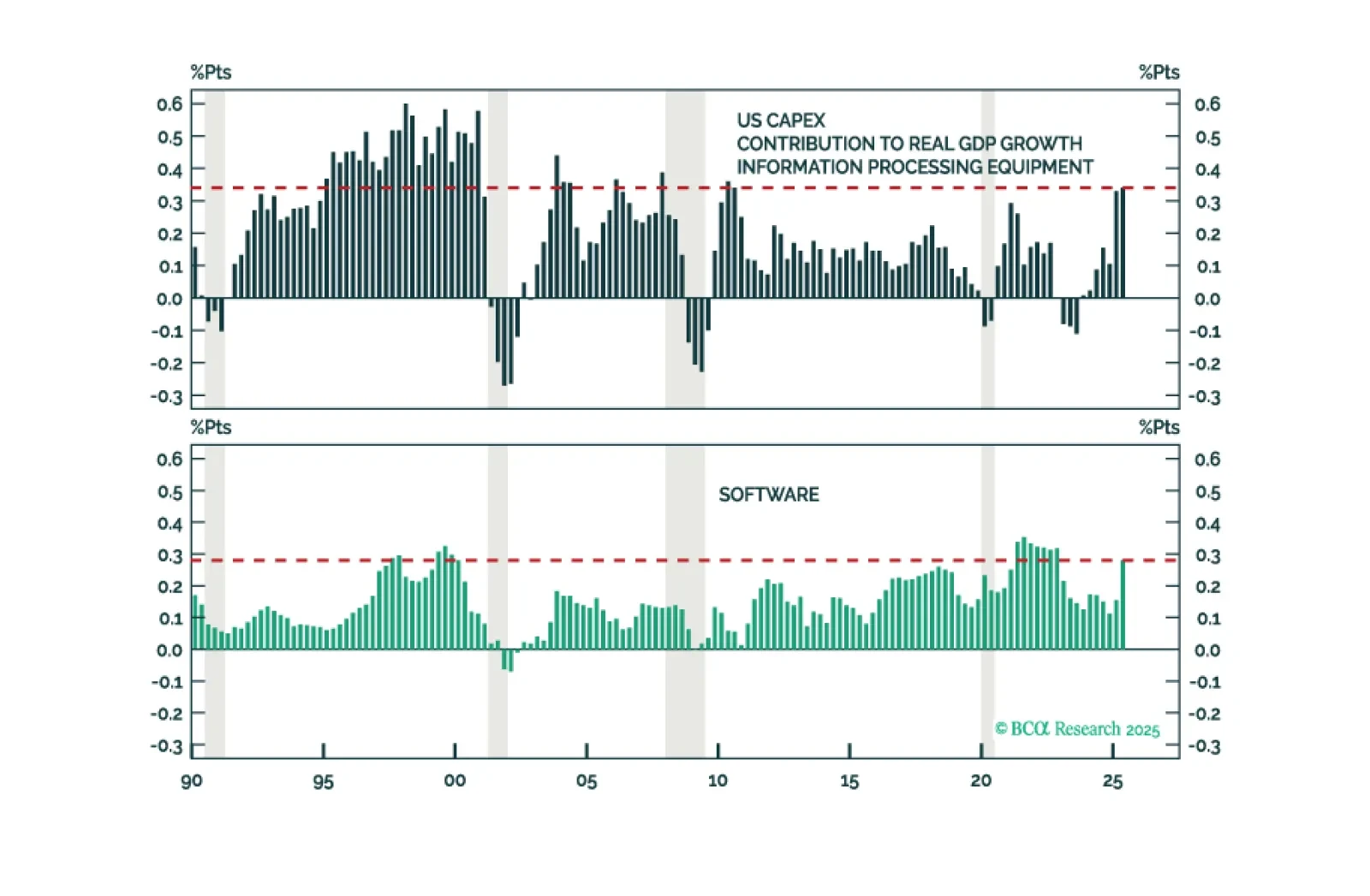

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

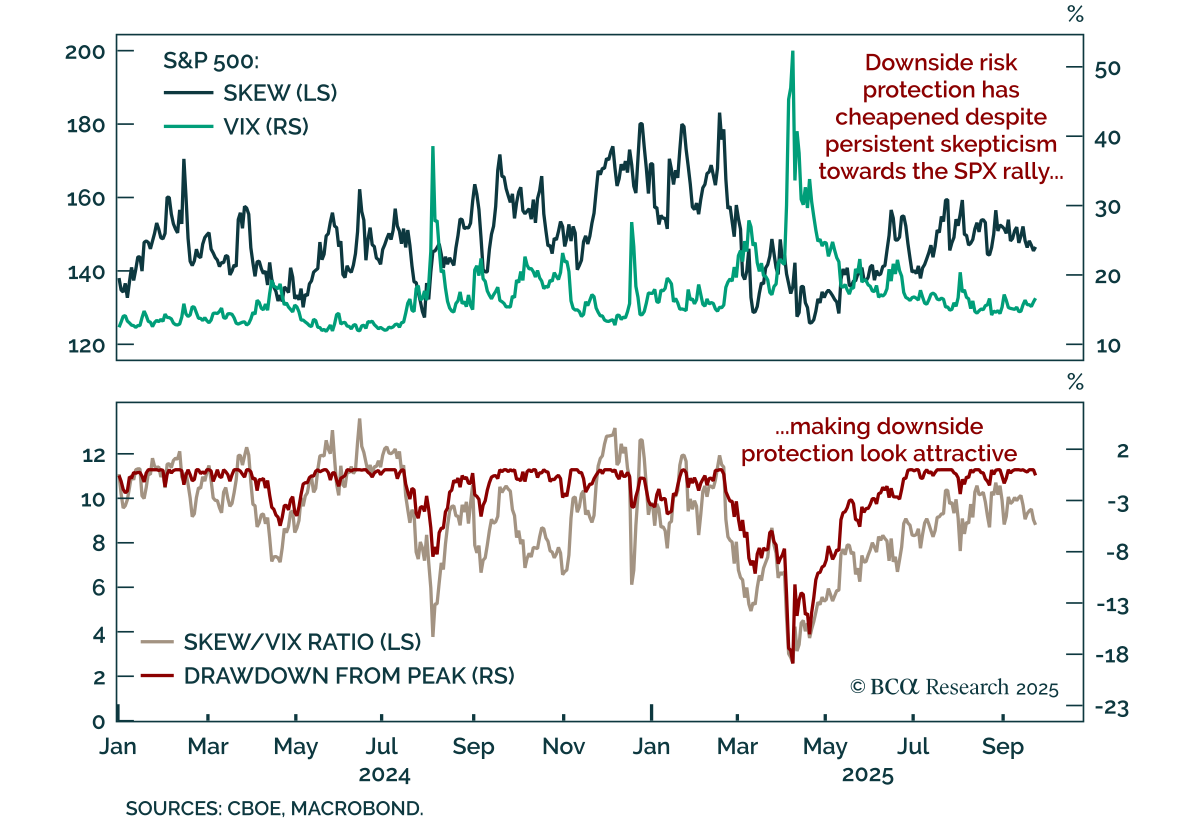

Despite talk of September seasonality, the S&P 500 has not pulled back, and the pain trade remains higher. The sell-off many expected failed to materialize. Positioning is not stretched, and in an environment where dip-buying remains instantaneous, any…

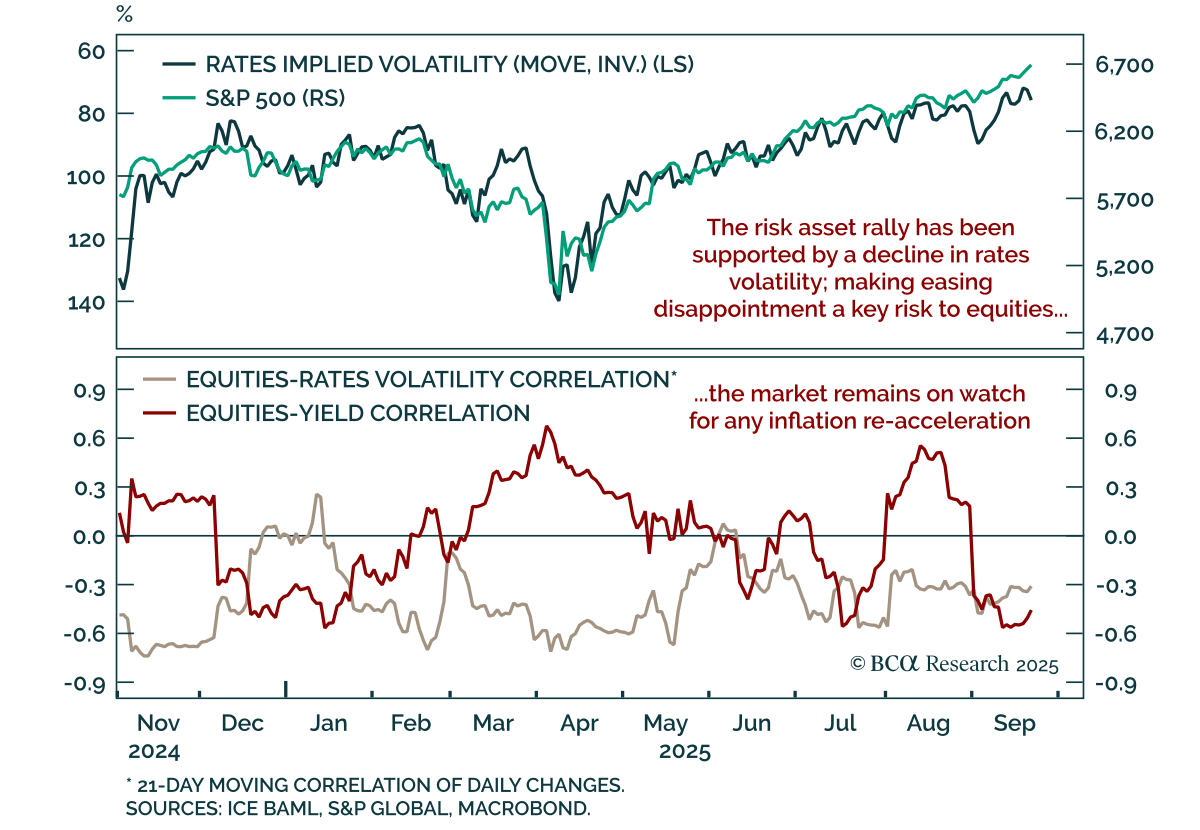

Low rates volatility has been a key tailwind for equities, but the fragile equilibrium leaves markets exposed to AI sentiment and inflation risks. Rates volatility, measured by the MOVE index, has drifted to multi-year lows and sits below its 20th percentile…