Energy

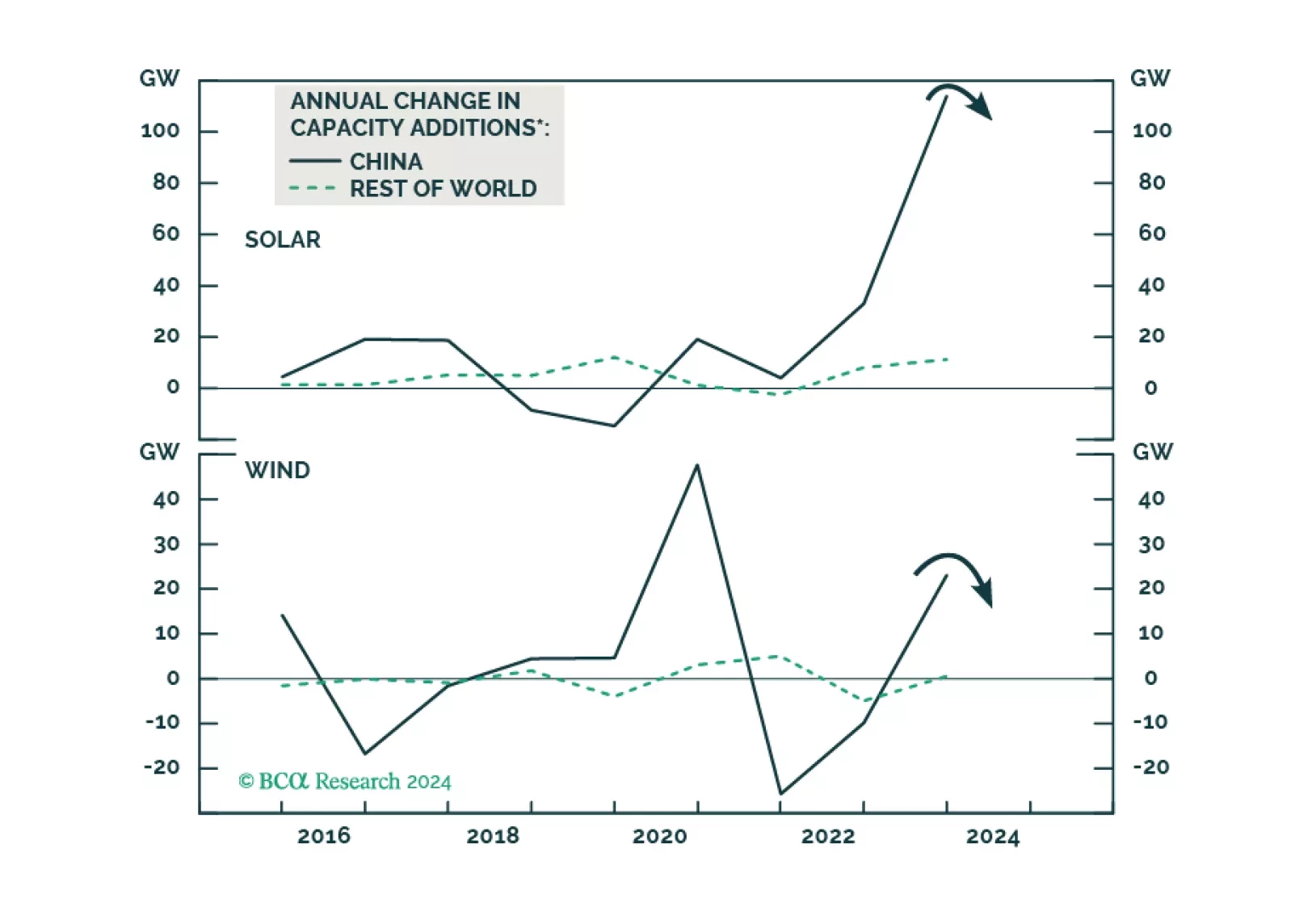

The global green energy rush faces mounting headwinds. Additional global solar and wind capacity installations will have considerable growth reduction this year. Copper prices did not drop much in 2023 due to surging demand from green power build-up. Green power will be less positive for copper demand in 2024 than in 2023. We expect more downside in global renewable energy stocks.

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

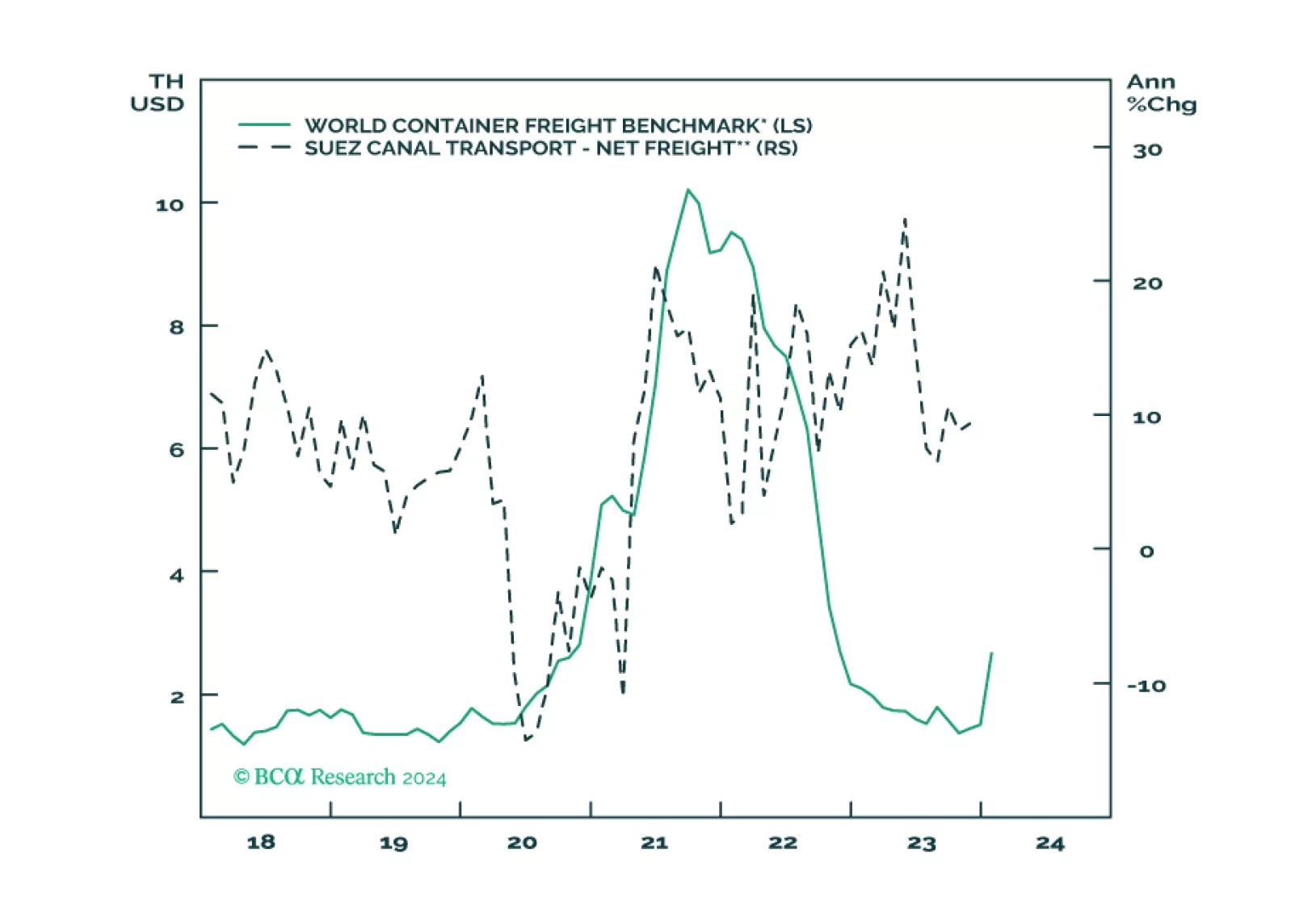

The attacks on Red Sea commercial tankers by Iran’s Yemeni proxies, the Houthi movement, are an inflation risk inasmuch as they lengthen voyage times for any shipping forced to avoid the Bab el-Mandeb Strait. The risk of an expansion of these attacks is, in our view, limited, given Iran’s inability to project naval power in the region.

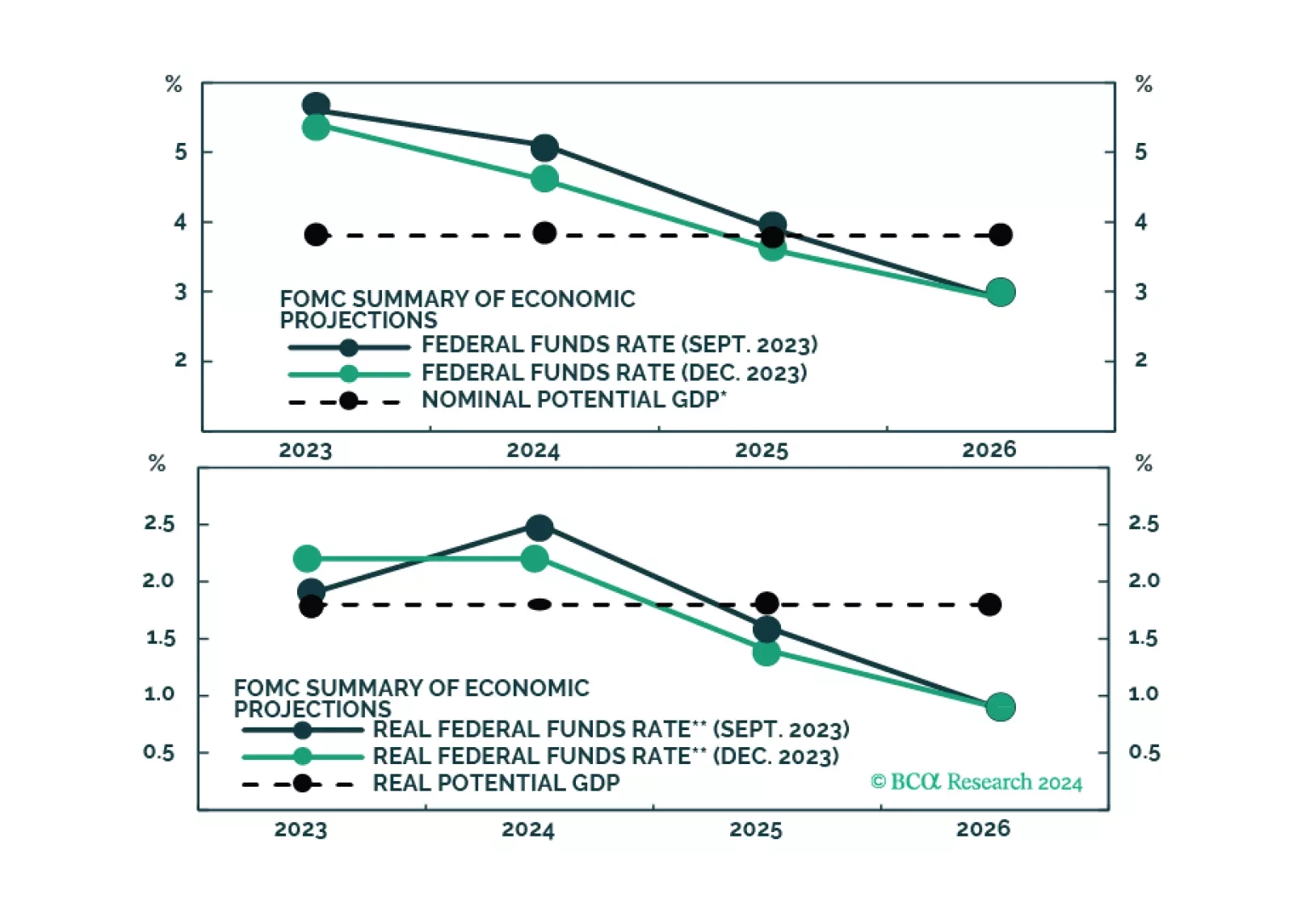

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

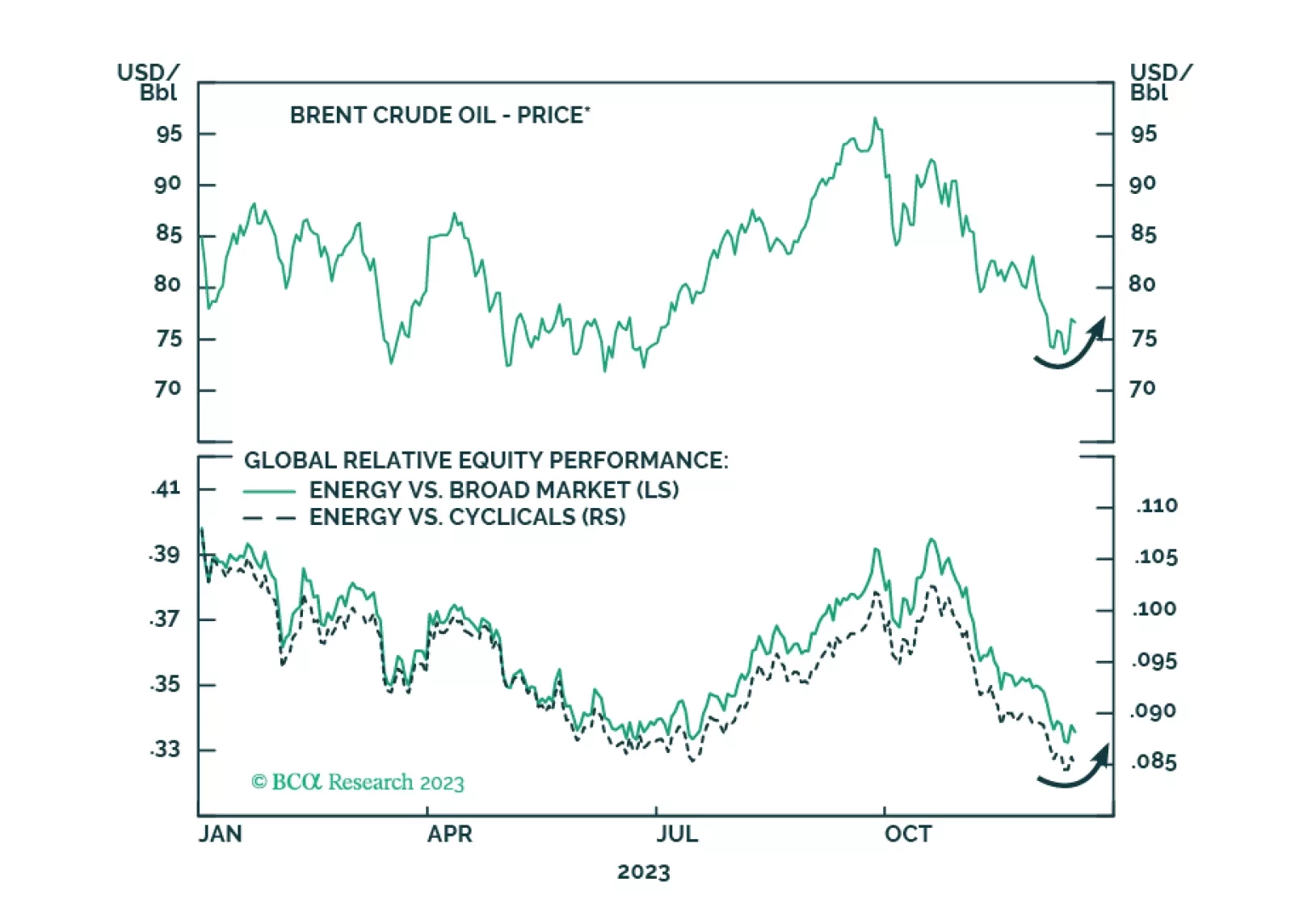

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.